One Out of Ten: The June 2026 Broker Scorecard

Ten analyst reports. Seven immediate rejections. Two forensic audits. One stock that cleared every hard gate — and one that failed all three.

Ten professional analyst reports landed on the Singapore Exchange this week, loaded with loud buy ratings and grand growth narratives. If you are managing a retirement portfolio built for steady monthly distributions, those headlines contain a serious warning. Out of all ten public broker calls, exactly one company survived the hard gates of my forensic balance sheet screen — the set of non-negotiable thresholds I apply before any stock qualifies for a retirement income portfolio.

If you are chasing capital growth and share price momentum, a higher-risk profile may clear your hurdle. But if you are a retiree focused on wealth preservation and dependable drawdown income, my forensic standard is built to protect your capital. It is not built to accommodate a momentum trade that could derail twenty years of compounding.

Most financial content is built around excitement — what is surging, what is breaking out, what you might be missing. I am deliberately building something different. Retirement-grade investing is not exciting. It is disciplined, forensic, and it is designed to still be working when you need it most.

As part of my ongoing Analyst Rating Review series, I spent the weekend dissecting these institutional research papers to do a thorough stock take for our community. Professional analysts get paid to project long-term earnings. But your utility bills must be paid with real cash today. Let us run these popular stock picks through the framework to see what the big broker firms are leaving out of their glossy brochures.

In This Article:

Section 1: The Full June 2026 Broker Activity Table

Section 2: Which Calls Are Relevant for a Retirement Dividend Investor

Section 3: ComfortDelGro C52 — The Forensic Verdict

Section 4: Sembcorp Industries U96 — The Forensic Verdict

Section 5: The Triple-Table Comparative Audit

Section 6: What the Broker Table Actually Tells Us

Section 1: The Full June 2026 Broker Activity Table

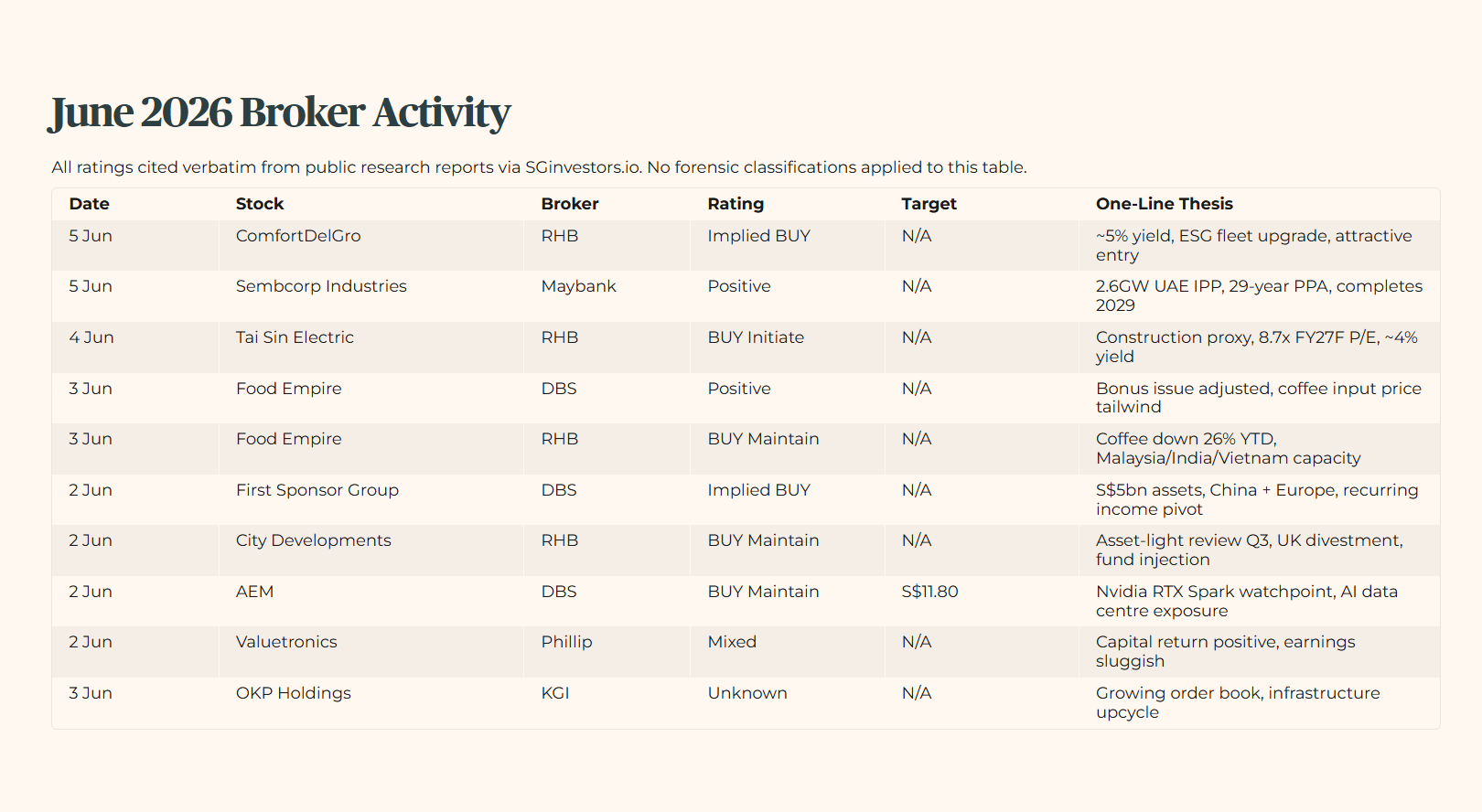

The data below represents a factual summary of recent analyst activity. All broker ratings and observations are cited verbatim from public research reports via SGinvestors.io. No forensic classifications or personal tracking adjustments have been applied to this specific table.

Broker Activity Summary: June 2026

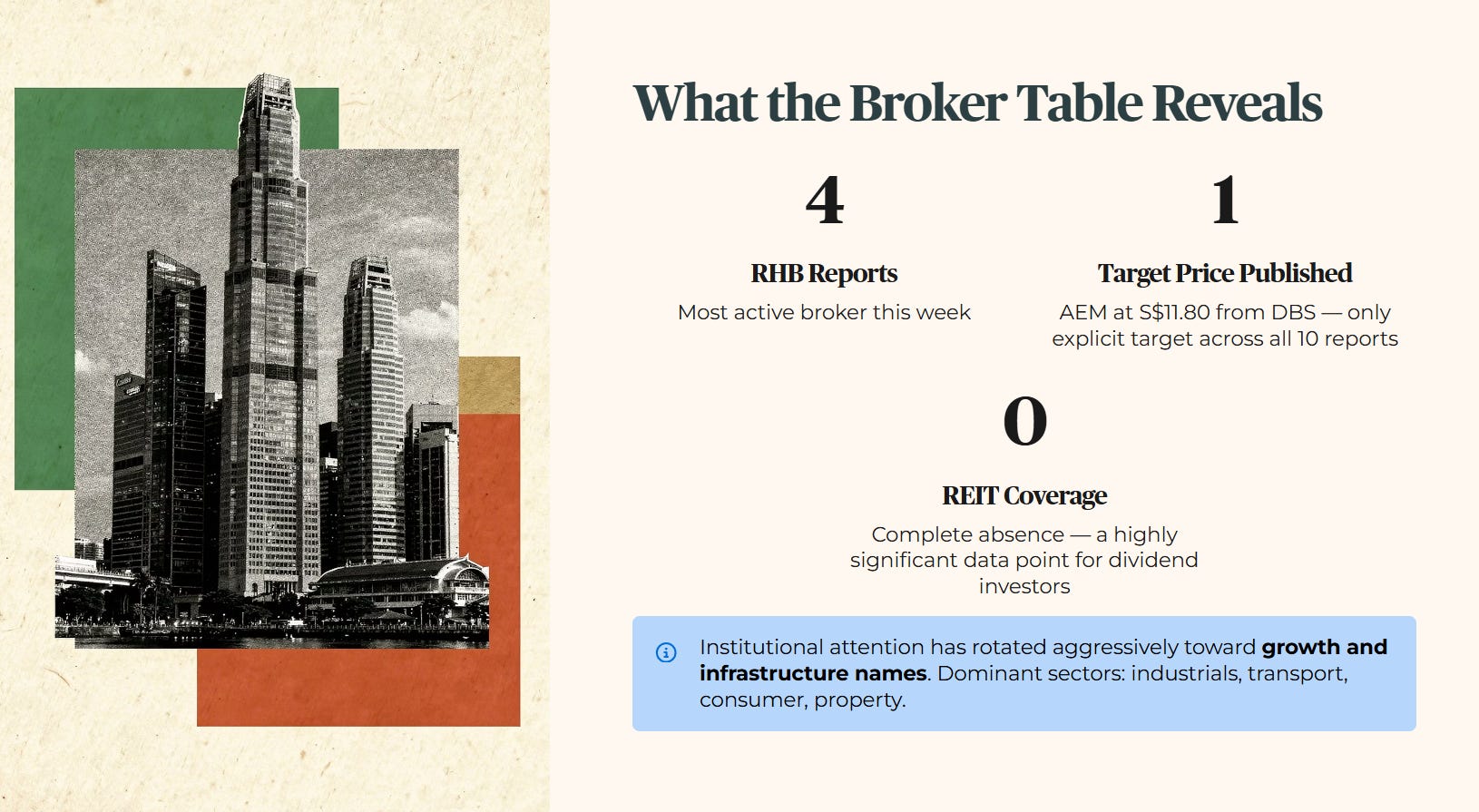

RHB Research was the most active broker this week with four reports. Only one explicit target price was published across all ten reports, which was AEM at S$11.80 from DBS. No REIT (Real Estate Investment Trust) coverage was initiated this week. The dominant sectors across the research desks were industrials, transport, consumer, and property.

For a retirement dividend audience, the complete absence of REIT coverage this week is itself a highly significant data point. Institutional attention has rotated aggressively toward growth and infrastructure names.

Section 2: Which Calls Are Relevant for a Retirement Dividend Investor

Not all ten names in that table belong in a serious retirement income conversation. We need to filter out the noise immediately so we can focus our analytical energy where it matters.

The Immediate Rejections (Growth Lane Only)

City Developments and First Sponsor Group are property developers. They do not possess a guaranteed distribution structure. Their cash flows depend on lumpy property development cycles. Tai Sin Electric is an industrial infrastructure proxy, but its projected yield of approximately 4% fails our minimum hurdle on face value. Food Empire is a consumer growth story expanding its production capacity across India and Vietnam. It does not fit a dividend income blueprint.

AEM is a semiconductor testing equipment manufacturer with zero dividend angle for retirees. The stock fell 7.98% in the week ending June 5, even as DBS maintained its optimistic S$11.80 target price. AEM appeared previously in EP1641 as a stock failing the central retirement test. No re-rating will be issued here. Readers seeking that specific structural audit should refer directly to that episode. Finally, OKP Holdings and Valuetronics present insufficient public data to conduct a reliable financial screen this week.

The Real Targets for Forensic Scrutiny

That leaves exactly two counters relevant for income analysis: ComfortDelGro and Sembcorp Industries. Both operate in yield-adjacent sectors. Both received positive institutional coverage this week. Neither has a prior zone verdict in our tracking registry. They will receive the full forensic treatment below.

Section 3: ComfortDelGro C52 — The Forensic Verdict

The institutional case from RHB flags an attractive entry point based on an expected 5% yield for the financial year 2026, progress on a cleaner vehicle fleet, and protected transport fares. The stock is currently trading at S$1.29. That is down 17.0% from its 52-week high of S$1.555.

Iggy Forensic Screen

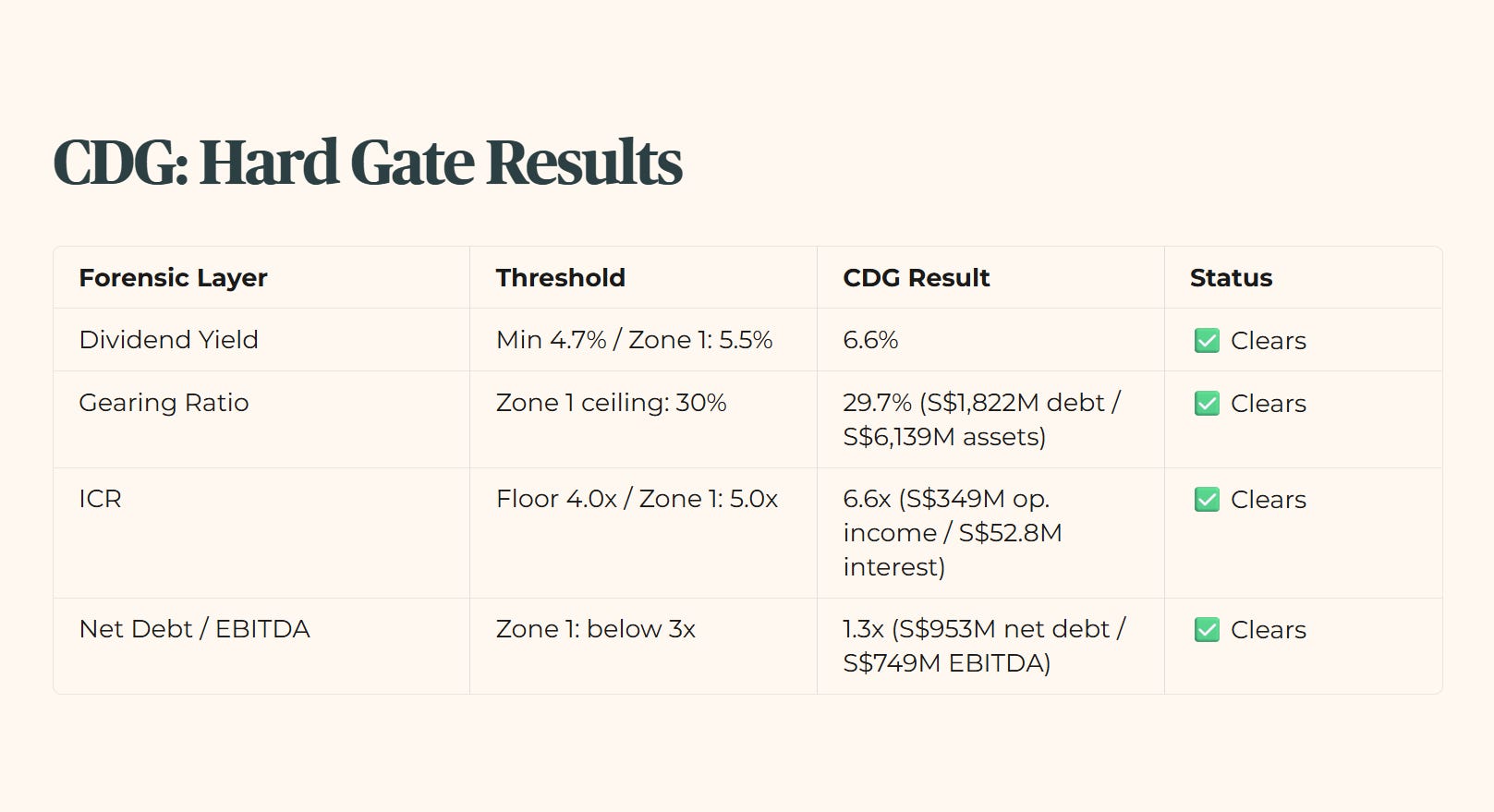

Yield Layer: ComfortDelGro pays a 6.6% yield at the current price of S$1.29, according to verified data from InvestingPro. This easily clears our 4.7% absolute minimum hurdle — the income threshold I require before any stock qualifies for a retirement portfolio. It also sits comfortably above the 5.5% Zone 1 threshold.

Gearing Layer: Gearing is a measure of financial leverage — it shows how much of a company’s assets are funded by debt rather than its own equity. Total debt stands at S$1,822M against total assets of S$6,139M. This works out to a gearing ratio of 29.7%, clearing my 30% Zone 1 ceiling.

ICR Layer: The ICR (interest coverage ratio) measures how many times a company’s operating profit can cover its interest expenses. A higher number means the company is more comfortably able to service its debt. ComfortDelGro’s operating income of S$349M against gross interest expense of S$52.8M gives an ICR of 6.6x — well above the 4.0x defensive floor and above the 5.0x Zone 1 threshold.

Net Debt to EBITDA Layer: EBITDA stands for earnings before interest, taxes, depreciation, and amortisation — a standard measure of a company’s operating cash-generating ability. The Net Debt to EBITDA ratio tells you how many years of that operating cash flow it would take to pay off all debt after subtracting cash reserves. Net debt of S$953M against an EBITDA of S$749M gives a clean 1.3x ratio, well below the conservative 3x Zone 1 threshold.

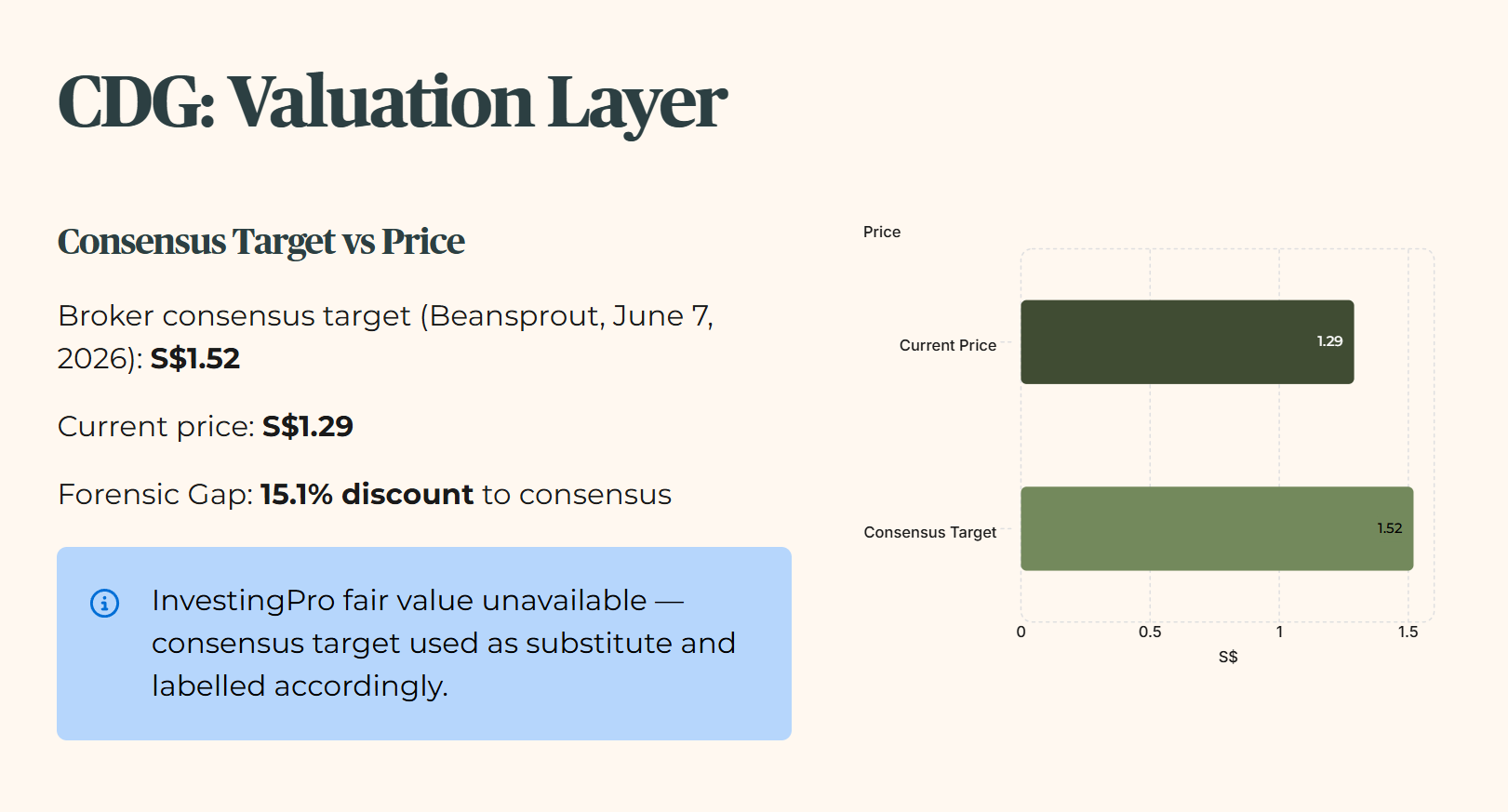

Valuation Layer: The broker consensus target price, based on analyst estimates compiled by Beansprout as at June 7, 2026, is S$1.52. At the current price of S$1.29, ComfortDelGro is trading at a 15.1% discount to that consensus figure. The Forensic Gap — the difference between the independent analyst consensus and the current market price — shows the stock is trading below where the professional community values it.

Soft Flag Assessment

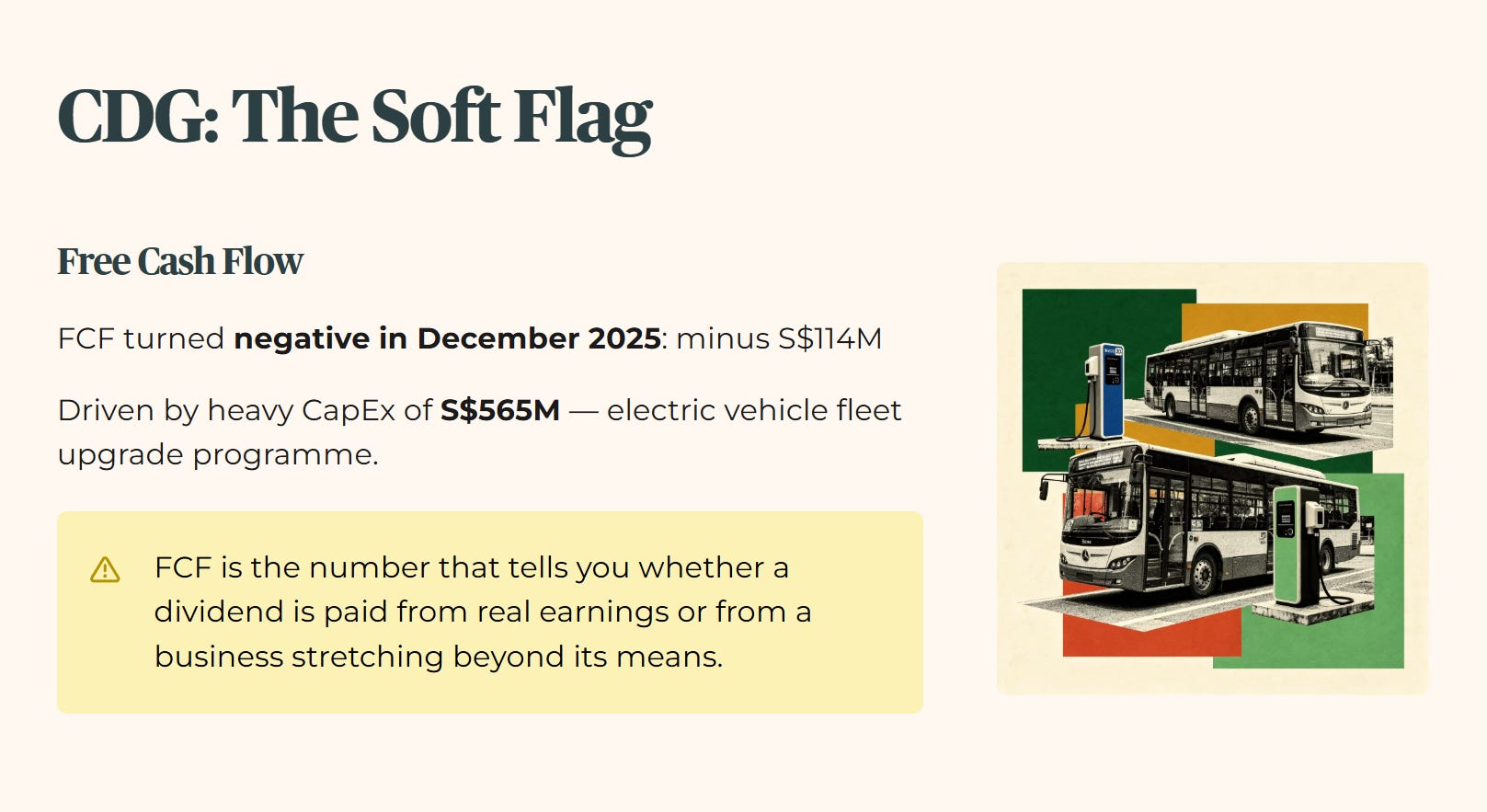

ComfortDelGro clears all four hard gates and triggers one soft flag. Free cash flow turned negative in December 2025. Free cash flow is the actual cash a business generates after paying its operating expenses and investing in equipment and infrastructure — it is the number that tells you whether a dividend is being paid from real earnings or from a business stretching beyond its means. ComfortDelGro’s free cash flow came in at minus S$114M, driven by a heavy capital expenditure programme of S$565M as the company upgrades its bus fleet to electric vehicles.

With one soft flag present, Zone 1 cannot be assigned — Zone 1 requires a clean screen with no soft flags at all. The single flag is the only thing standing between this stock and a Zone 1 Fortress classification.

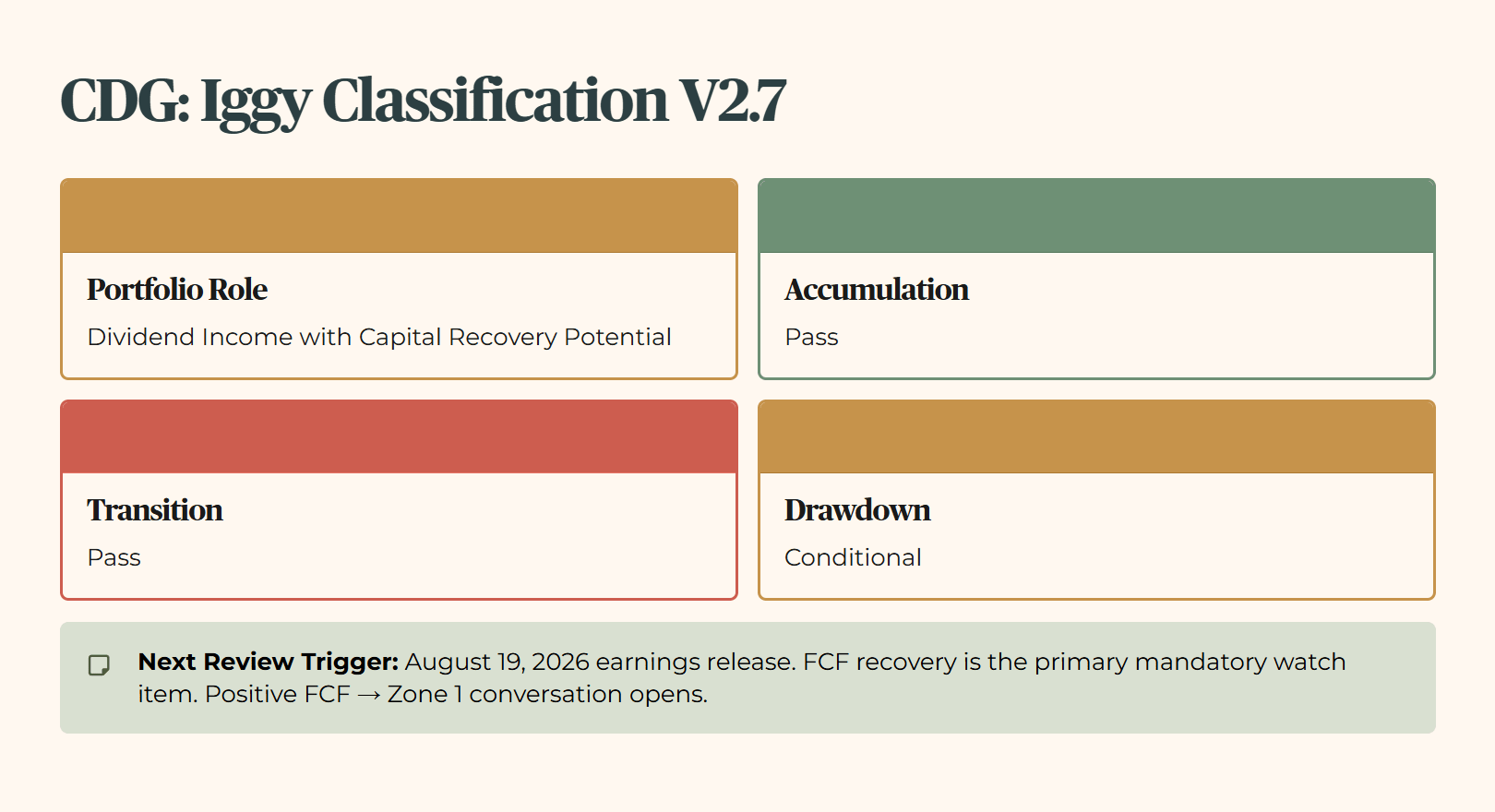

Iggy Classification V2.7

Iggy’s Forensic Zone: Zone 2 — Watchlist

Heartland Wallet Impact

At S$1.29, ComfortDelGro pays a 6.6% yield while trading 15.1% below the broker consensus target. For a 58-year-old investor in Bedok managing an SRS drawdown portfolio, that combination matters. A yield that clears every hard gate, a gearing ratio below 30%, and a price sitting well below what professional analysts collectively consider fair value — this is not a combination the forensic screen surfaces often.

The single open question is whether the negative free cash flow of the last twelve months is a temporary drag from the fleet upgrade cycle or the beginning of a structural deterioration in earnings. The August results will give us the answer.

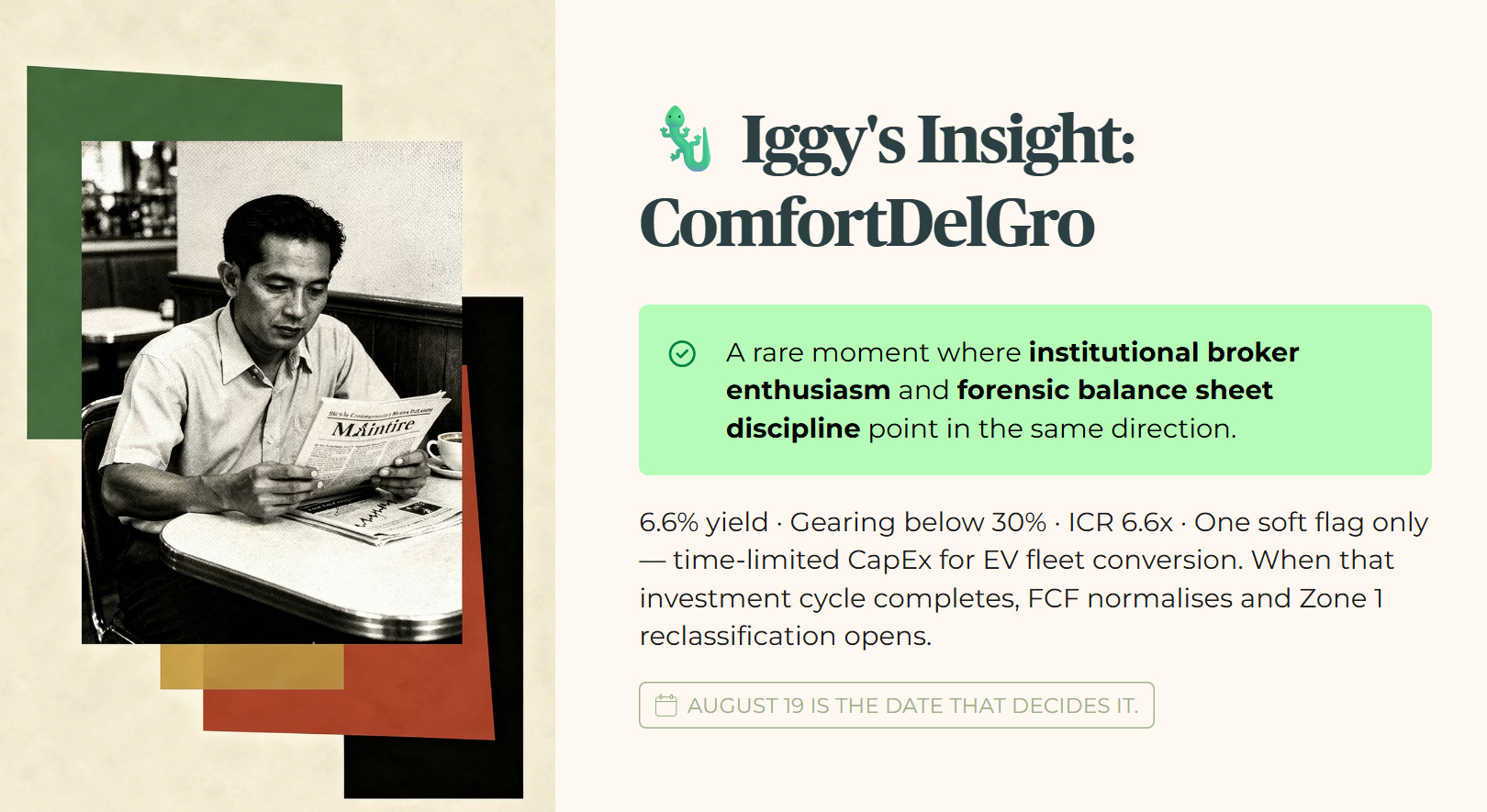

🦎 Iggy’s Insight

ComfortDelGro presents a rare moment where institutional broker enthusiasm and forensic balance sheet discipline point in the same direction. A 6.6% dividend yield backed by gearing below 30% and an ICR of 6.6x provides a very comfortable cushion for retirement capital. The only flag on the screen is free cash flow, which has turned negative because of a large but time-limited capital expenditure programme for electric vehicle fleet conversion. When that investment cycle completes, the FCF position should normalise — and with it, the path to a Zone 1 reclassification opens. August 19 is the date that decides it.

The free cash flow figure above fails the clean Zone 1 standard on paper — but when you run that negative S$114M through the same yield, gearing, ICR, and net debt to EBITDA gates in the Triple-Table Comparative Audit, the classification outcome for ComfortDelGro’s retirement-grade status looks very different from what a single red number suggests.