Oversubscribed Doesn't Mean Overperforming: What Singapore's Latest IPOs Are Actually Teaching Investors

Foundation Healthcare and JustCo both drew strong institutional demand, and both fell below their offer price anyway. Here's what that gap actually means, and why AirTrunk's upcoming listing is the ne

By Angela, Market Correspondent, The Investing Iguana

A note before we begin: my role here is to report on analyst research, earnings results, and market developments as they stand, without applying Iggy’s forensic analysis. If you’re looking for Iggy’s forensic audit on any of these names, that’s a separate piece and will be linked where available. What you’re reading here is a faithful summary of what the market and its analysts are saying, nothing more and nothing less.

Initial Public Offering Demand Fails to Predict Secondary Market Performance on the Singapore Exchange

Substantial oversubscription rates and high institutional interest during the initial listing phase do not guarantee stable secondary market pricing for new equities on the local bourse.

The Singapore Exchange has seen a renewed wave of initial public offerings, first-time sales of shares by private companies to the public, this year. Investors frequently watch public subscription levels and cornerstone commitments, which represent guaranteed institutional allocations before public trading begins, as gauges of long-term performance. Recent debuts on the local exchange have highlighted a distinct disconnect between initial subscription demand and subsequent secondary market trading behavior.

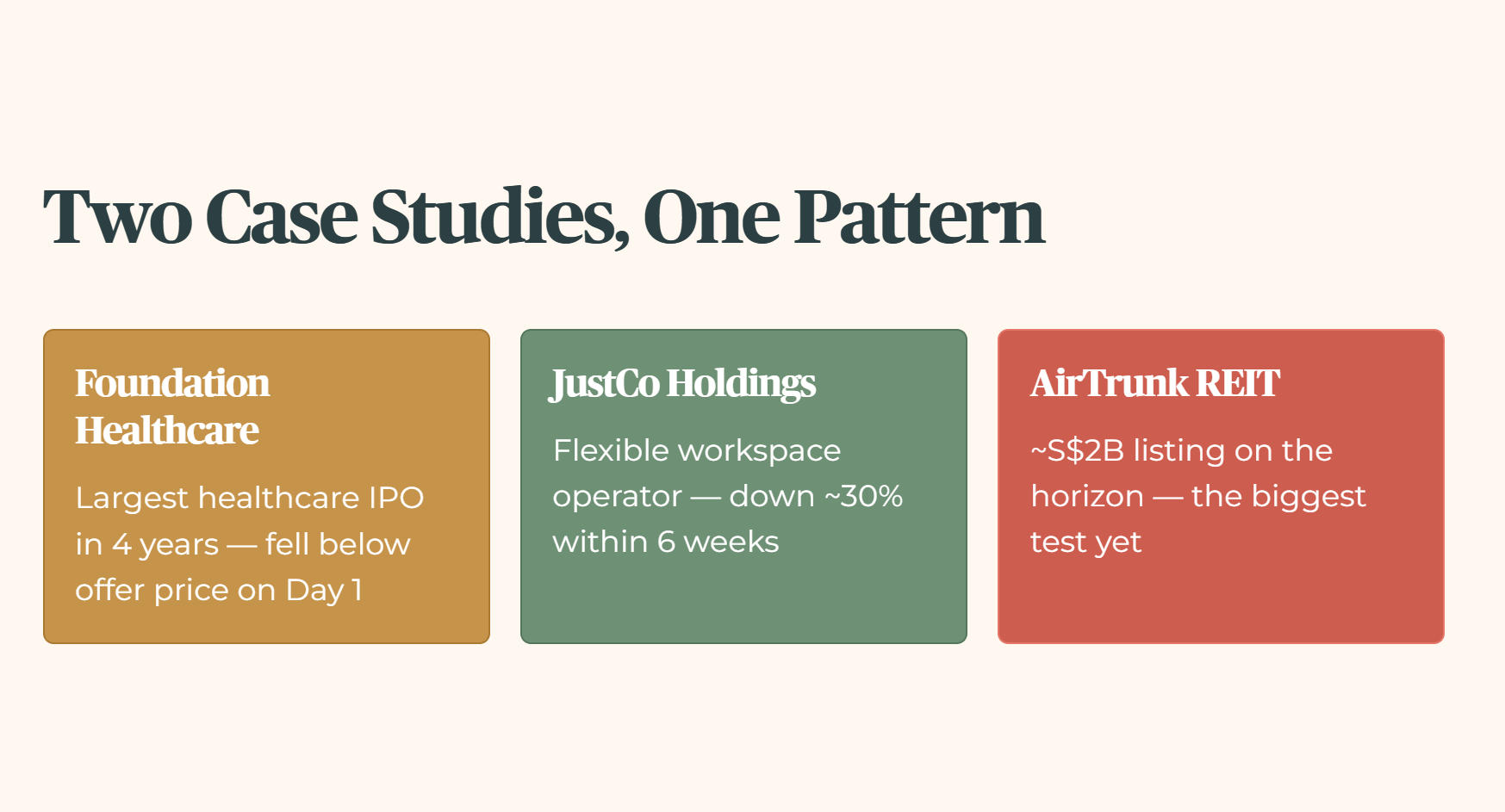

This piece looks at the recent market introductions of Foundation Healthcare Holdings Limited and JustCo Holdings Limited, and how intense primary demand shifted into immediate price pressure. It also considers the upcoming proposed listing of AirTrunk as a real estate investment trust, a pooled investment vehicle holding income-generating property assets, to see how this pattern might apply to the largest market debut in years.

Foundation Healthcare and the Reality of Day-One Price Reversals

Angela’s Observation

JustCo and the Slower Bleed of Post-Listing Revaluations

The Disconnect Between Primary Demand and Market Pricing

Angela’s Observation

The Window Is Already Open

AirTrunk and the Upcoming Test of Bourse Liquidity

Key Takeaways

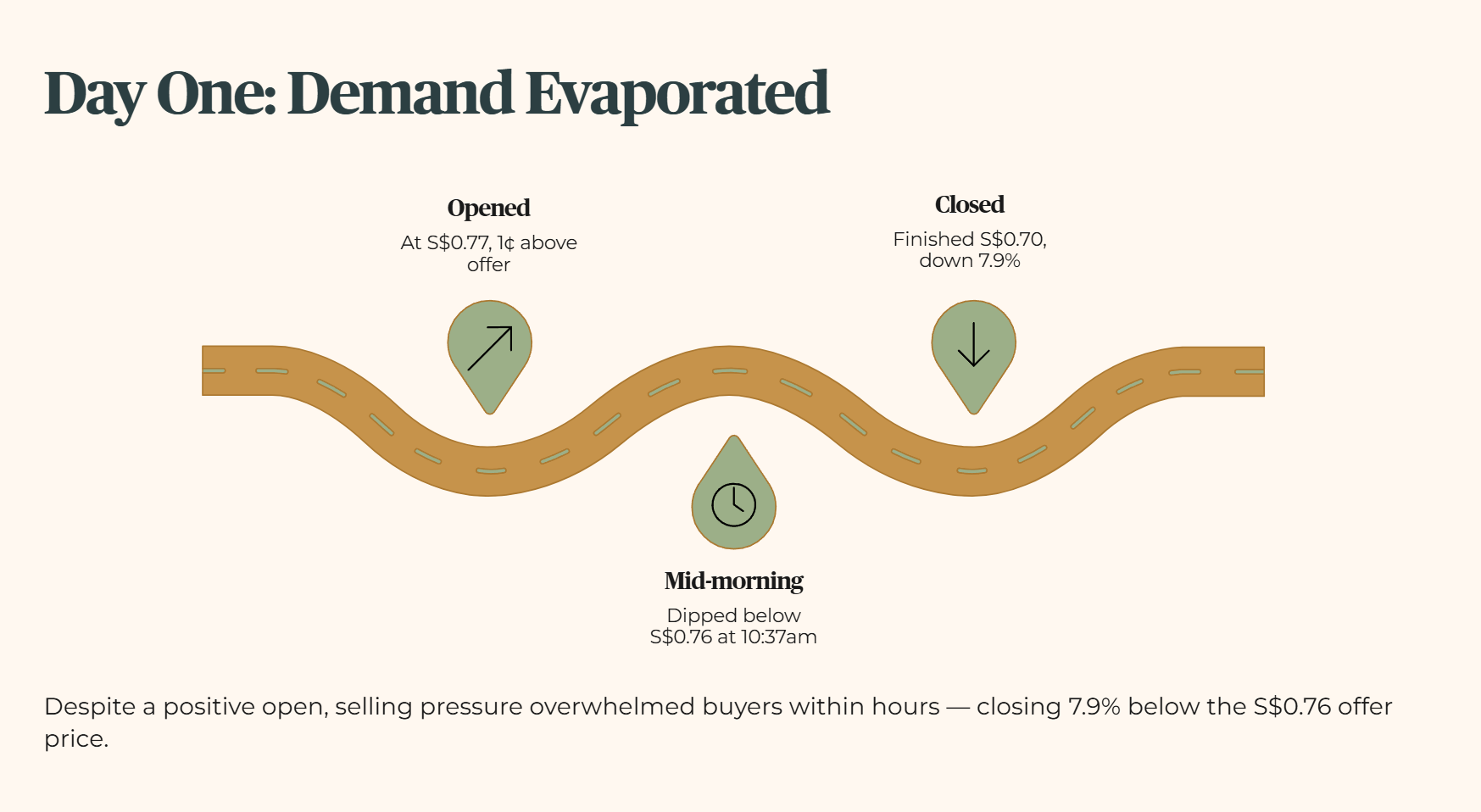

Foundation Healthcare and the Reality of Day-One Price Reversals

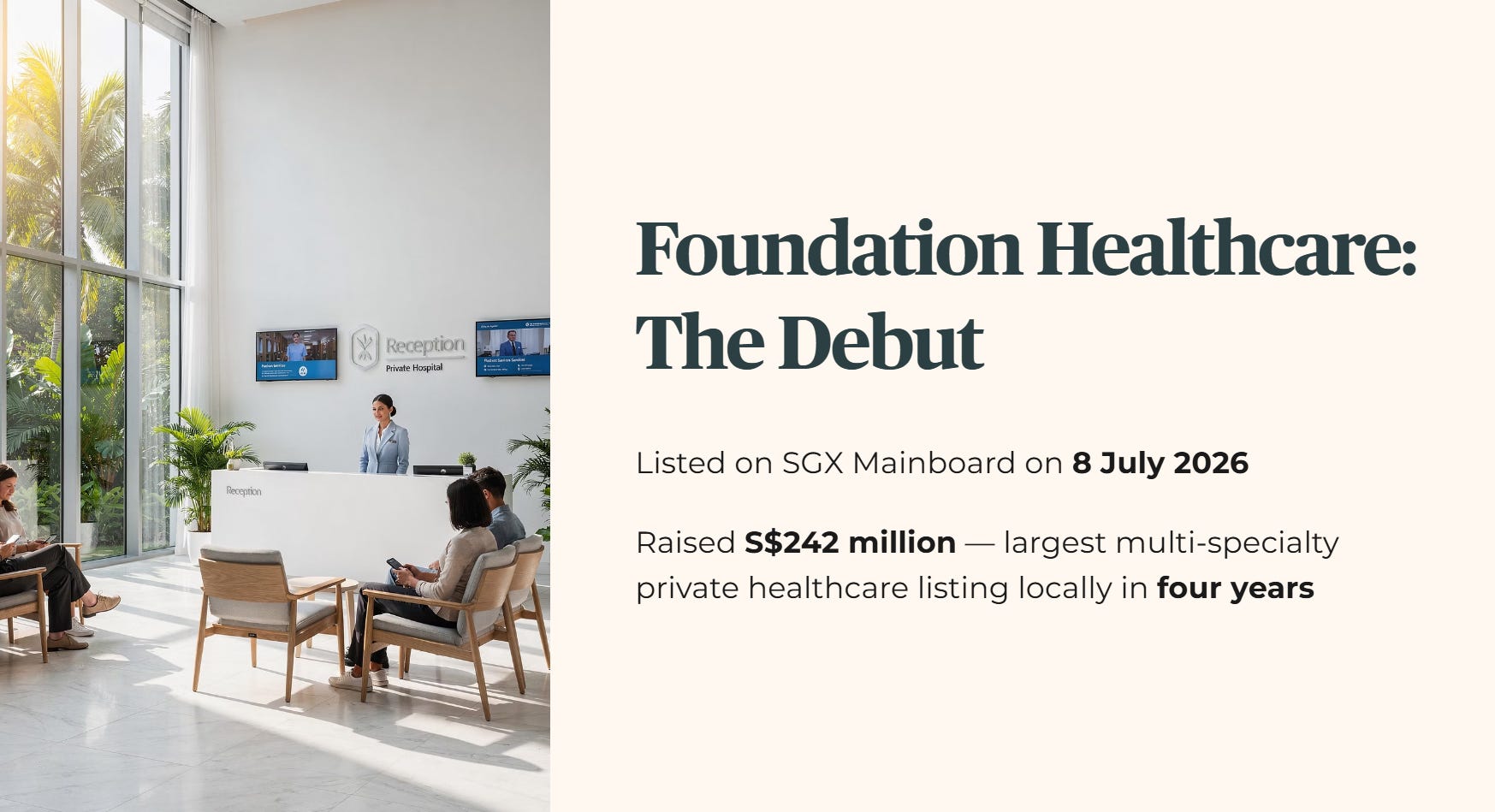

Foundation Healthcare Holdings Limited made its highly anticipated market debut on the Mainboard, the primary equity listing platform of the Singapore Exchange, on July 8, 2026. The initial public offering raised gross proceeds of S$242 million, making it the largest multi-specialty private healthcare platform to list locally in four years.

Primary demand for the issue looked exceptionally resilient during the capital raising phase. The company reported its Singapore public offer tranche of 87 million shares was approximately 9.4 times subscribed, drawing more than 3,800 valid retail applications. Total demand across both the international placement and retail tranches reached 3.8 times subscription capacity. The raise also secured commitments from ten institutional cornerstone backers, including Amova Asset Management Asia, Lion Global Investors, Manulife Investment Management, and UBS AG.

Despite these positive demand metrics, secondary market trading revealed immediate selling pressure that overwhelmed initial buyers. The stock opened its first trading session at S$0.77, a modest one-cent premium above its initial public offering price of S$0.76. This upward momentum proved short-lived: the equity dropped below its listing price at 10:37 in the morning. Selling pressure intensified through the afternoon, pulling the counter down to close its opening session at S$0.70, a 7.9 percent decline from the initial public offering price.

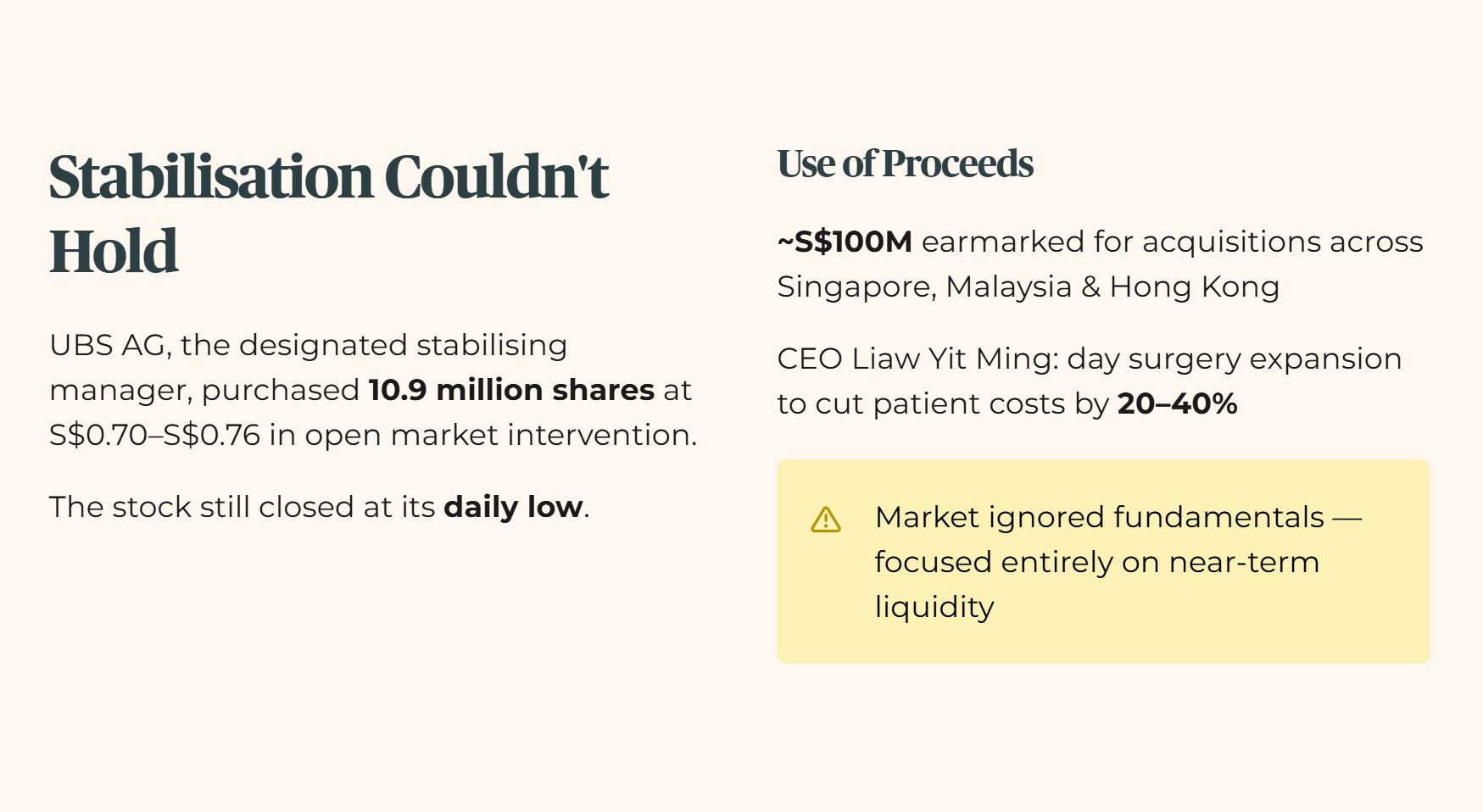

The first-day decline occurred despite active intervention by UBS AG, the designated stabilizing manager for the listing. Under local exchange rules, a stabilizing manager can buy shares in the open market to support the stock price during the initial trading period. UBS disclosed after the market closed that it had purchased 10.9 million shares in the open market at prices ranging between S$0.70 and S$0.76. The stock still closed at its daily low despite millions of dollars in institutional buying support.

Management intends to deploy approximately S$100 million of the listing proceeds to fund acquisitions of specialist practices and day surgery centres across Singapore, Malaysia, and Hong Kong. Chief Executive Officer Liaw Yit Ming noted the group aims to expand day surgery access to reduce overall patient costs by 20 to 40 percent, though early market trading appears focused entirely on near-term liquidity dynamics.

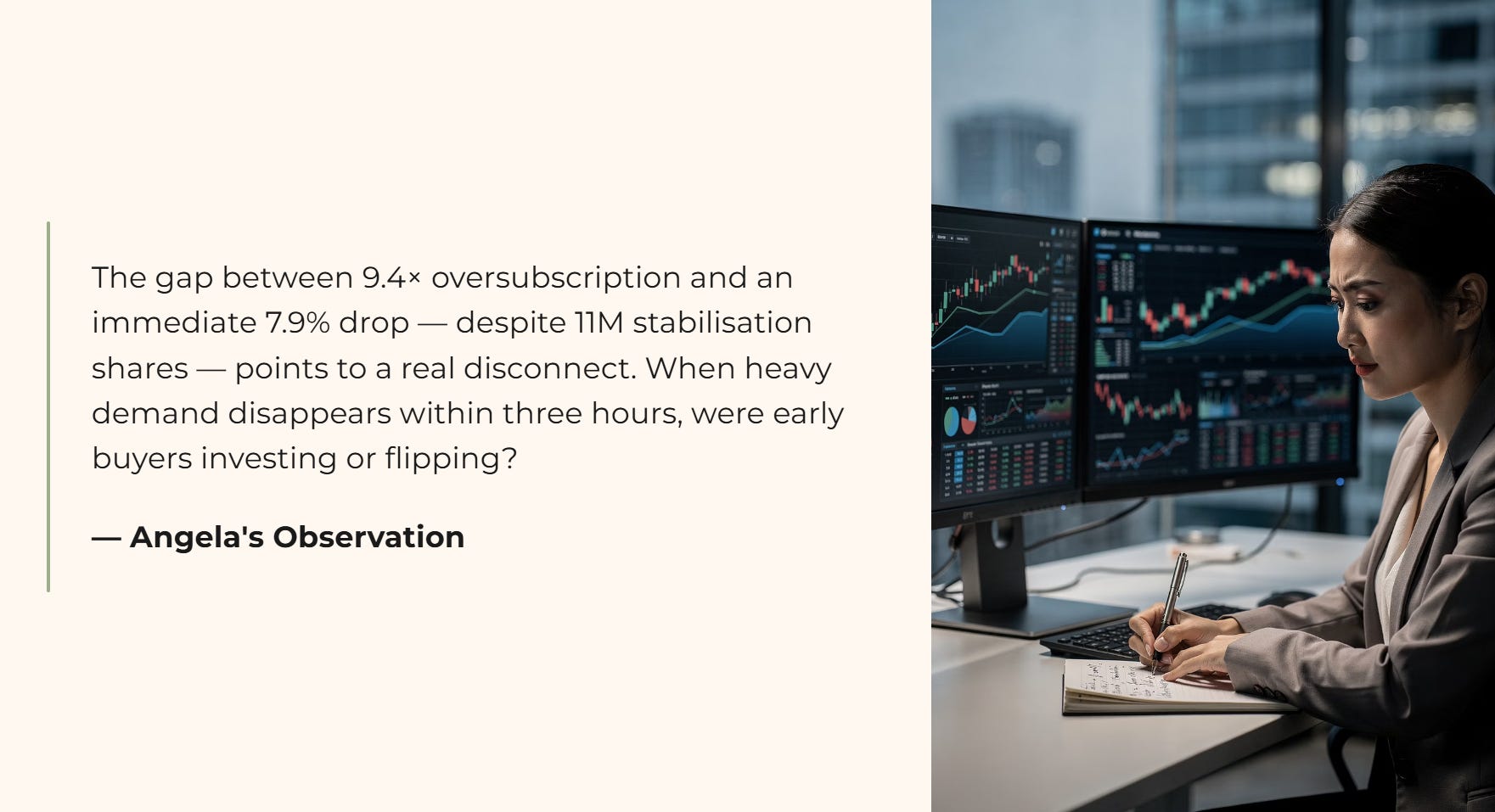

🟠 Angela’s Observation

The gap between a 9.4 times oversubscribed public tranche and an immediate 7.9 percent price drop, despite nearly 11 million stabilization shares bought, points to a real disconnect in how retail demand and post-listing conviction line up. When heavy initial demand disappears within three hours of the opening bell, it raises the question of whether early buyers were investing for the long haul or simply flipping allocations for a quick premium. Whether the stabilizing manager can establish a firm floor once the official price support window closes is worth watching.

JustCo and the Slower Bleed of Post-Listing Revaluations

The pattern of post-listing price weakness extends beyond immediate day-one reversals into longer-term secondary market revaluations. JustCo Holdings Limited, a flexible workspace operator, completed its initial public offering six weeks before this reporting period, raising S$100 million. The company offered 32.1 million shares at S$0.94 per share, including a dedicated public tranche of 6.3 million shares.

Alongside the public offer, the company secured cornerstone commitments for 74.3 million shares from institutional investors, netting approximately S$92 million after underwriting costs. The capital was raised to fund regional capital expenditure, with the goal of expanding from 54 centres to more than 100 locations by 2029.

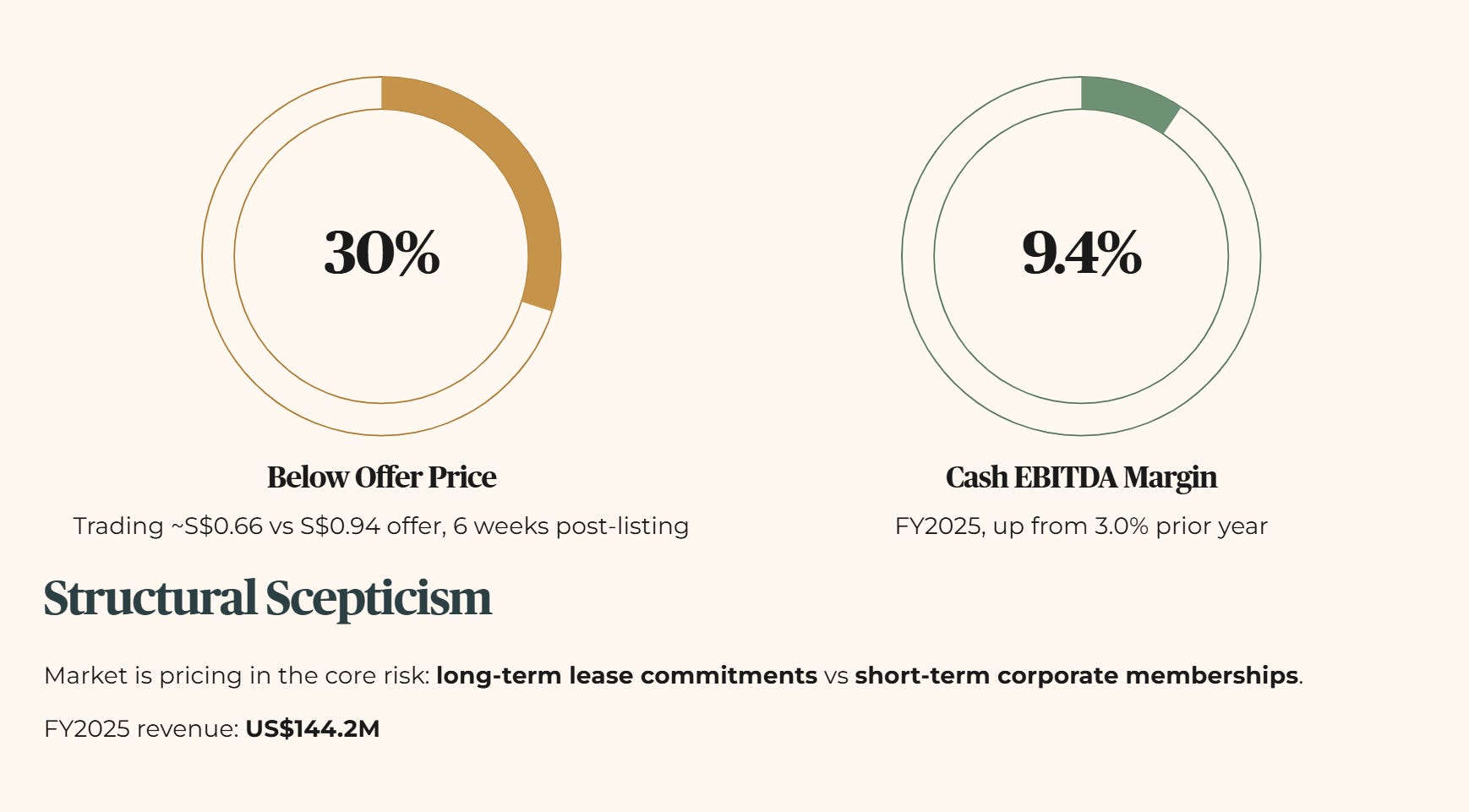

The secondary market performance has diverged sharply from the initial raise. Six weeks into public trading, the stock is trading at a working estimate of approximately S$0.66, roughly 30 percent below its S$0.94 offer price. The drop reflects broader market skepticism about the structural risks of flexible office operators, who take on medium- to long-term lease commitments with landlords while relying on short-term memberships from corporate tenants.

For financial year 2025, the company posted revenue of US$144.2 million and a cash EBITDA margin of 9.4 percent, up from 3.0 percent the year before.

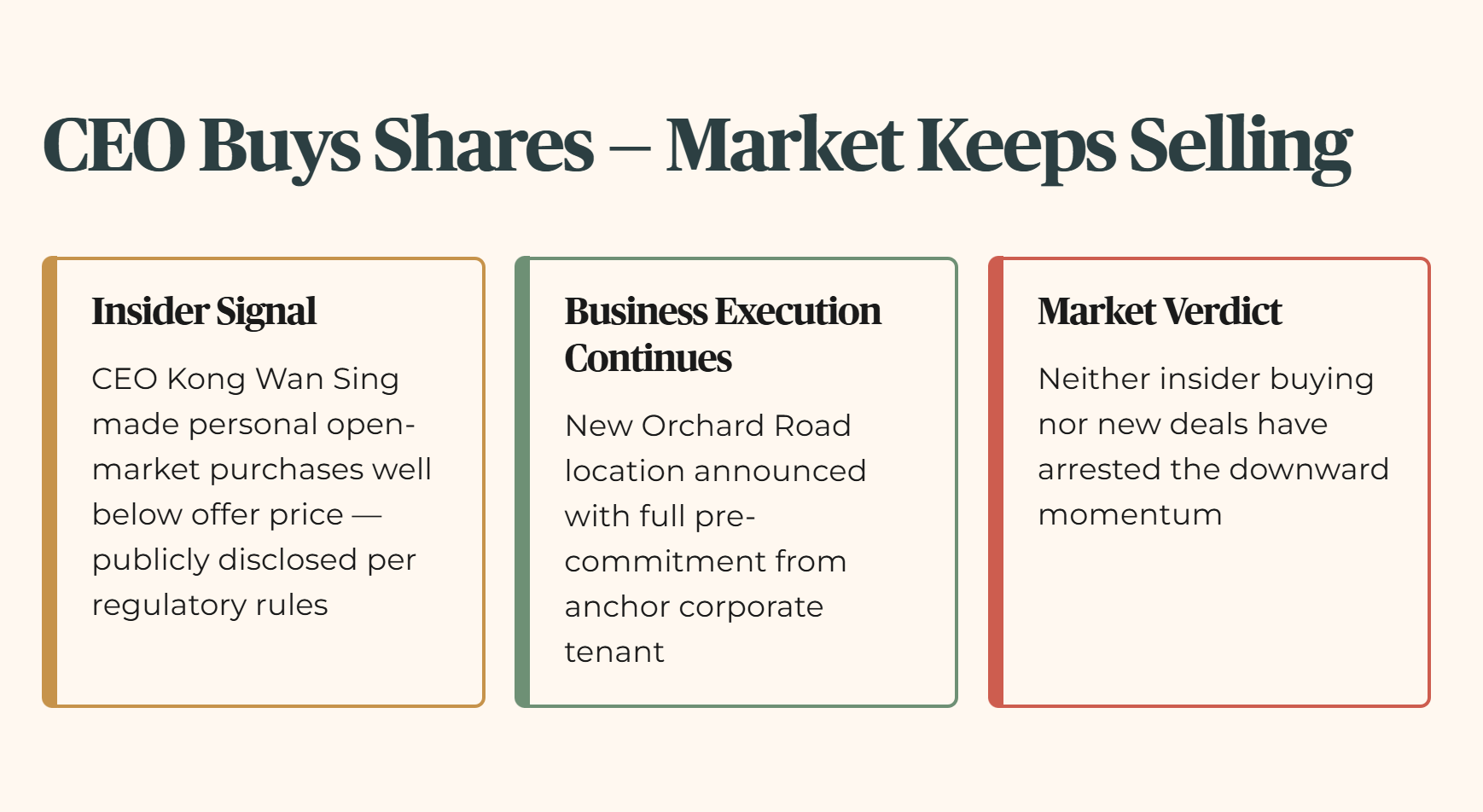

In response to the prolonged price decline, Chief Executive Officer Kong Wan Sing has made personal open-market share purchases at levels significantly below the offer price. Under regulatory guidelines, insider purchases must be disclosed publicly, and are often read as a signal of executive alignment with minority shareholders. These purchases haven’t yet arrested the downward momentum. The company recently announced a new Orchard Road location with full pre-commitment from an anchor corporate tenant, showing continued business execution alongside the market’s revaluation.

The Disconnect Between Primary Demand and Market Pricing

Foundation Healthcare and JustCo’s trading histories are a useful case study on the limits of IPO demand metrics. Institutional cornerstone backing and high oversubscription multiples are often promoted as assurances of quality, but they reflect primary market demand, not secondary market equilibrium.

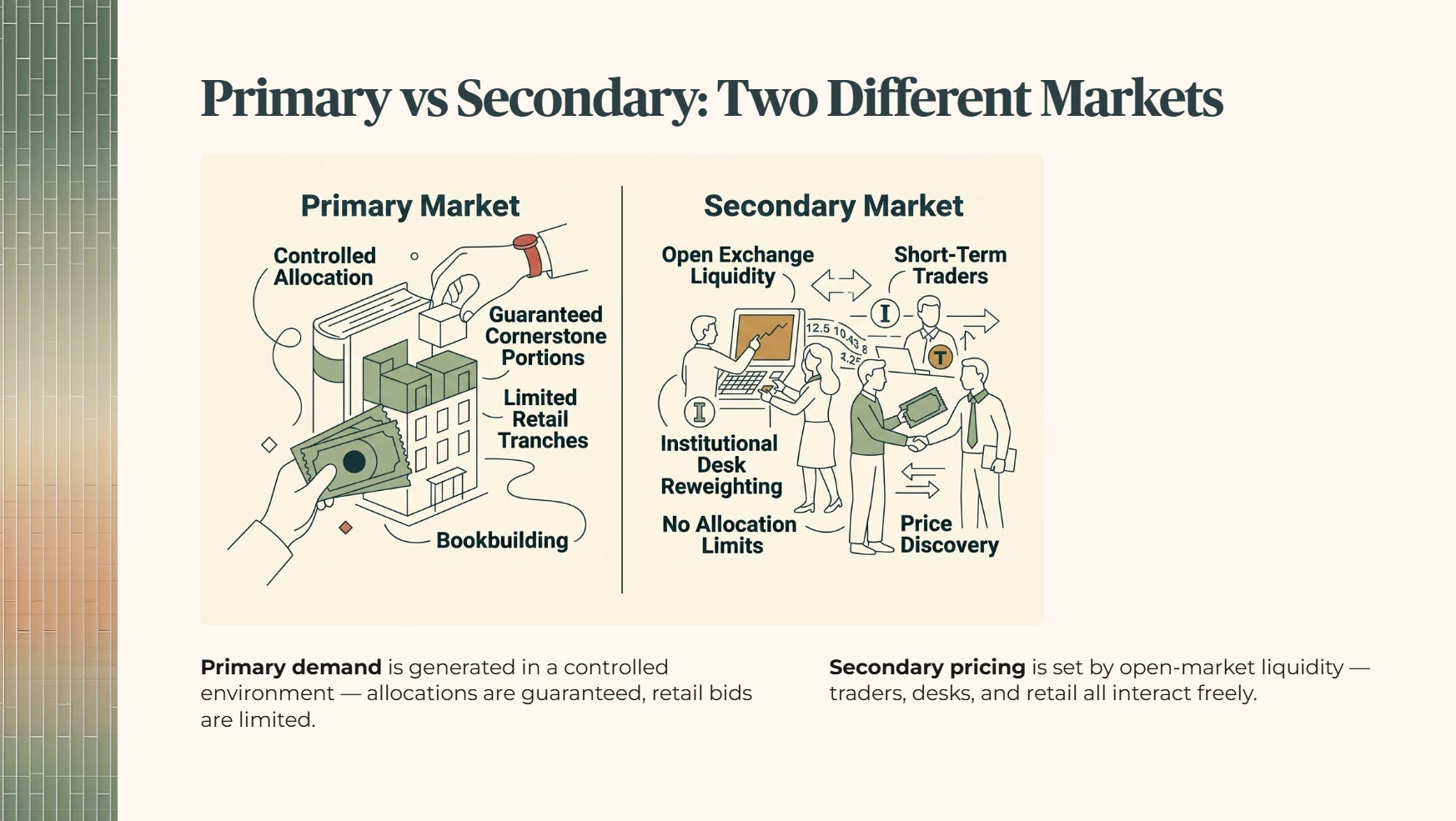

Primary demand is generated in a controlled environment where institutional allocators receive guaranteed portions and retail investors bid for limited tranches. Once trading begins on the exchange, pricing shifts entirely to secondary market liquidity, where short-term traders, institutional desks adjusting weights, and retail participants interact without allocation limits.

Cornerstone investors can sometimes create a false sense of security for retail buyers. While these institutions commit to a lock-up period, that doesn’t stop other pre-listing shareholders, underwriters, or allocation flippers from selling on opening day. In Foundation Healthcare’s case, the heavy retail oversubscription increased the pool of smaller investors who may have been looking for an immediate opening premium. When that premium didn’t materialise, selling pressure quickly overwhelmed the stabilizing manager and drove the price down.

This suggests high subscription levels are often a trailing indicator of marketing success rather than a leading indicator of price stability. A company that fills its order book during the roadshow has maximised its capital intake at the highest valuation the market would bear. For secondary market buyers, a fully priced listing leaves very little margin for error if early results or conditions shift. The immediate revaluation of two very different businesses, one in healthcare, one in real estate, suggests the market is demanding higher discount rates than the original bookrunners priced in.

🟠 Angela’s Observation

Seeing cornerstone backing fail to hold up secondary pricing across two different sectors makes me wonder whether the current IPO pricing model is out of step with actual exchange liquidity. When a company’s own CEO feels the need to buy shares in the open market just weeks after listing, it tells you the public market is pricing risk more aggressively than the banks that structured the deal. I keep coming back to whether a high oversubscription headline should read as reassurance, or as a caution sign.

The Window Is Already Open

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

The pattern in Foundation Healthcare and JustCo’s pricing tells you how AirTrunk’s targeted 6.0 percent yield and planned S$2 billion raise need to be stress-tested against actual secondary liquidity in the next section.