Parkway Life REIT: Boring Yield, Elite Returns? My Honest Take

Are You Missing Asia's Most Defensive Healthcare REIT Play? Why Institutions Are Quietly Buying While Retail Investors Walk Away

Most Singapore investors chase high-yield REITs and miss the bigger picture. Here’s why Parkway Life REIT’s “boring” 3.7% yield might be your portfolio’s best insurance policy against the next market storm—and the three red flags you must know before investing.

You know that feeling when you see a REIT yielding 3.7% and move on? Many retail investors do that. They want their kopi money now—8% to 10% yields that look exciting on paper.

Yet institutions have been quietly buying while retail sold. That gap is worth attention. Large funds are not chasing thrills. They want resilient cash flows, downside protection, and assets that hold value when markets wobble.

This piece breaks down Parkway Life REIT as a core defensive holding. We will cover what makes it strong, what could hurt returns, and how to position as a Singapore investor. You will get the three green flags, the three red flags, and a clear verdict. The goal is simple: give a full map so you can act with conviction.

The Healthcare REIT That Refuses to Break

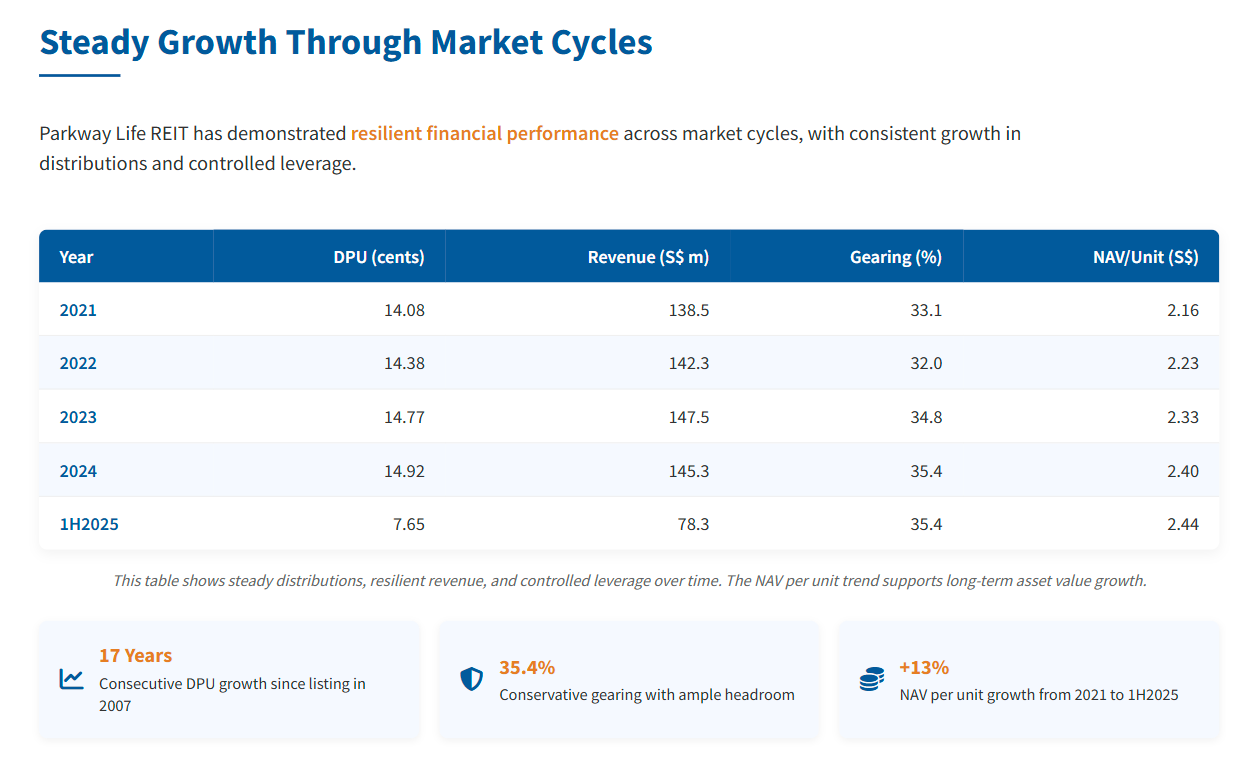

Parkway Life REIT has grown its DPU every year since listing in 2007. Through the Global Financial Crisis, COVID-19, rate shocks, and inflation spikes, it did not cut. That is rare. The 1H 2025 results showed gross revenue up 8.1% to S$78.3 million, NPI up 8.0% to S$73.8 million, and distributable income up 9.5% to S$49.9 million. DPU rose 1.5% year on year to 7.65 cents, or 15.30 cents annualised, based on an enlarged unit base. As at 30 June 2025, gearing stood at 35.4%, interest cover at 9.1 times, and roughly 97% of borrowings were on fixed rates.

Why does this matter? Because healthcare demand is not cyclical. People need care in all markets. When the portfolio is locked into long leases with built-in escalations, cash flow stays predictable. That is the core edge here. It is defensive by design, not by accident.

The second factor is asset quality. The Singapore hospitals in the portfolio are crown jewels. The master lease embeds growth mechanics, including fixed 3% annual step-ups through FY2025 and an annual rent review formula from FY2026 to FY2042. Pair this with careful overseas expansion and strong risk controls, and you get a sleep-well-at-night setup.

Table: Parkway Life REIT Key Financials (FY2021–1H2025)

This table shows steady distributions, resilient revenue, and controlled leverage over time. The NAV per unit trend supports long-term asset value growth, which helps justify a valuation premium even with a lower headline yield. Numbers reflect reported results and 1H 2025 balance sheet levels.