Should You Follow DBS’s $4.74 BUY Call on Parkway Life REIT? | Iggy ARR EP1627 🦖

The Stock the Banks Love That Your Retirement Cannot Afford

Introduction

This REIT pays out 3.81%. That is less than the 4.0% you earn risk-free in your CPF Special Account. If you are managing money for retirement, ask yourself this. Why take on the risk of a single hospital and borrowed money, only to earn less than what the government guarantees you? This review explains why the gap between what analysts promise and what is safe for retirement income keeps getting wider.

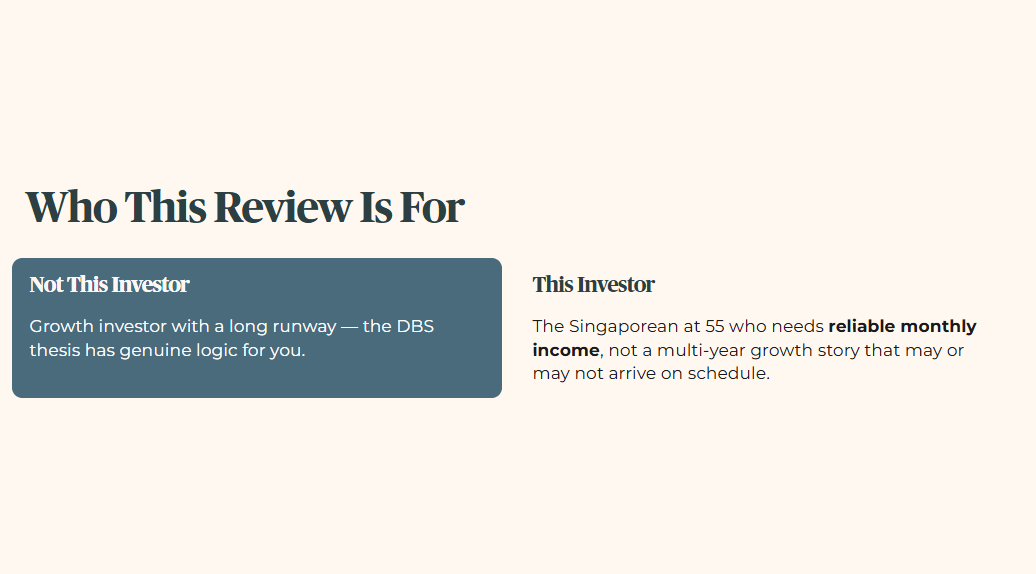

If you are a growth investor with a long runway, the DBS thesis on this stock has genuine logic — master lease renewal, CPI-linked rent escalation, and a pipeline of Japanese acquisitions. This review is not written for that investor. It is written for the Singaporean at 55 who needs their capital to generate reliable monthly income, not a multi-year growth story that may or may not arrive on schedule.

I have received many questions about Singapore’s bigger REITs over the past few weeks. I understand why Parkway Life REIT catches your eye. A major local bank just put out a new report with a bold price target. But we need to look past the headline.

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips — the interest coverage, the gearing, the free cash flow sustainability — so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

In This Article:

The Analyst's Case

Iggy's Forensic Screen

Financial Health Checklist

The Dividend Trajectory

The Forensic Gap

Iggy's Insight 1

Ownership Signal

What To Watch Next

Iggy's Insight 2

Iggy Classification — V2.7

Closing — The Forensic Stance

Section 1 — The Analyst’s Case

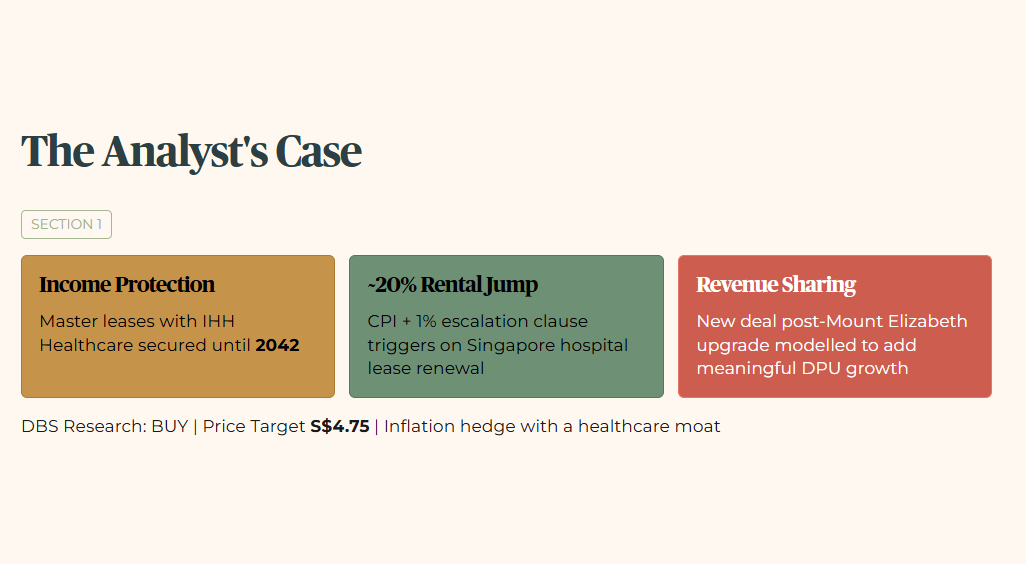

DBS Research has repeated its BUY call on Parkway Life REIT with a price target of S$4.75. Their argument rests on three ideas.

First, they say the REIT’s income is protected until 2042 through long-dated master leases with IHH Healthcare. Second, they believe rental income will jump nearly 20% when the Singapore hospital leases are renewed, triggered by the CPI plus 1% escalation clause embedded in the lease structure. Third, they see significant upside from a new revenue-sharing arrangement once the Mount Elizabeth Hospital upgrade completes — a deal they model as adding meaningful DPU growth on top of the base lease renewal.

Their inflation logic runs like this. Rising consumer prices in Singapore automatically trigger the rent escalation clause, which flows directly into distribution income. For a fund with a long time horizon, that makes this stock look like an inflation hedge with a healthcare moat.

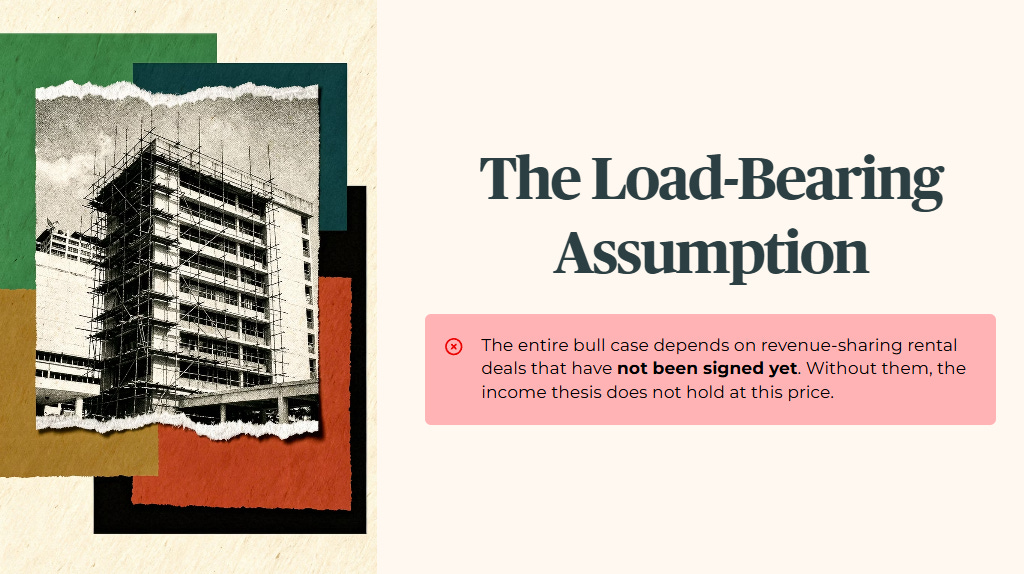

THE LOAD-BEARING ASSUMPTION: The entire bull case depends on revenue-sharing rental deals that have not been signed yet. The analysts need those deals to happen exactly as modelled, just to rescue the current low yield. Without them, the income thesis does not hold at this price.

Section 2 — Iggy’s Forensic Screen

Let us stop looking at the narrative and run this counter through a cold, hard screen.

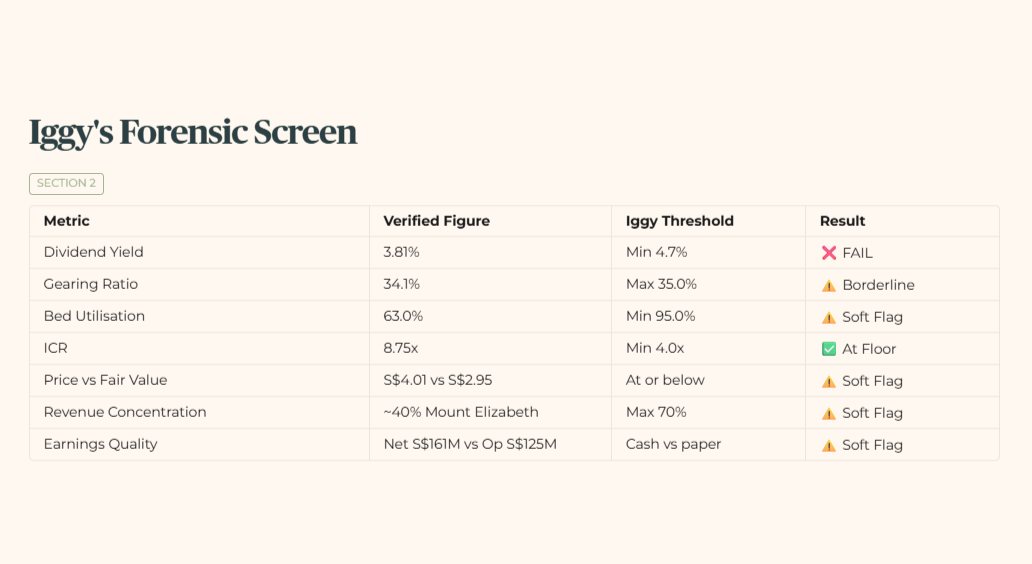

Financial Health Checklist

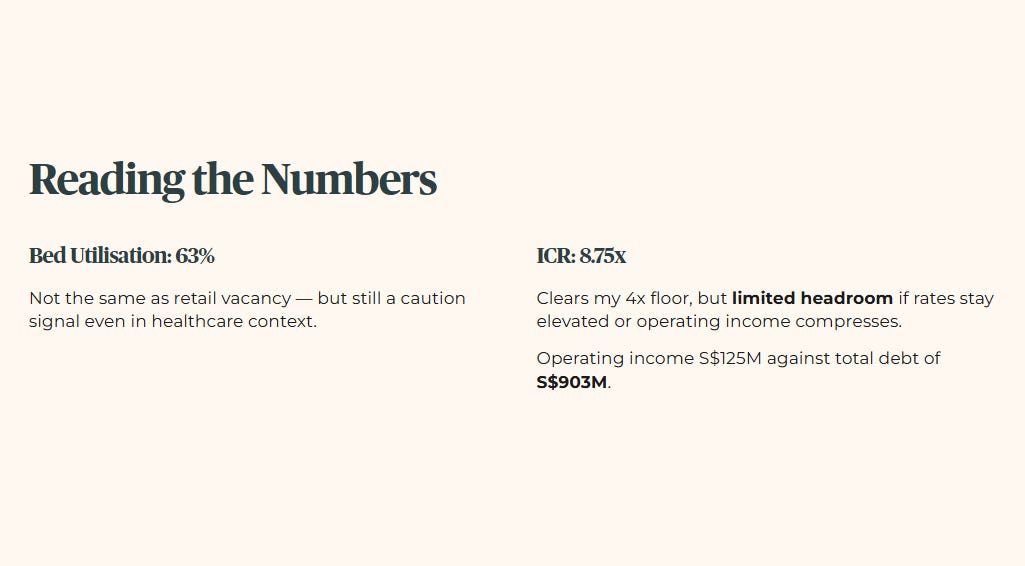

A note on occupancy. Healthcare REITs measure bed use, not empty office or retail space. A 63% bed utilisation rate is not the same as a 63% vacancy rate in a shopping mall. My 95% threshold is a high standard for a reason, and even with the healthcare sector context, this number is a caution signal.

Now the interest coverage ratio — the number that tells you whether the REIT earns enough to comfortably pay its interest bill. With operating income of S$125M against total debt of S$903M, the verified ICR sits at 8.75x. That clears my 4x minimum floor, but it leaves limited headroom if interest rates stay elevated or operating income compresses further.

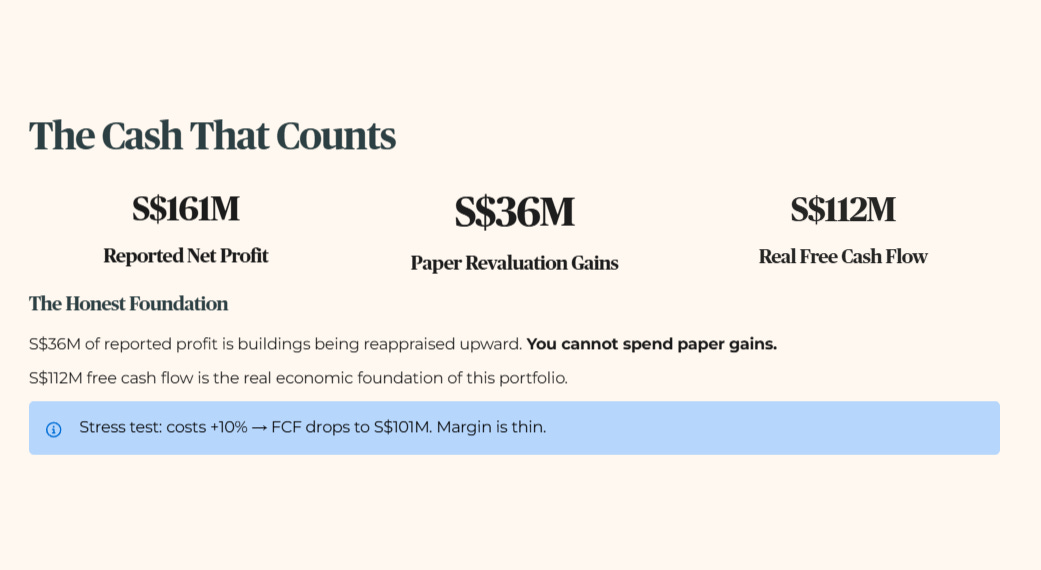

I count three soft flags. The stock trades 26.4% above its InvestingPro fair value of S$2.95. It draws approximately 40% of revenue from a single hospital, Mount Elizabeth. And its reported net profit of S$161M is inflated by S$36M in revaluation gains from property reappraisals — paper gains that do not generate cash. Combined with the yield hard gate failure, this counter goes into Zone 4 Caution.

Iggy’s Forensic Zone: Zone 4 — Caution

Section 3 — The Dividend Trajectory

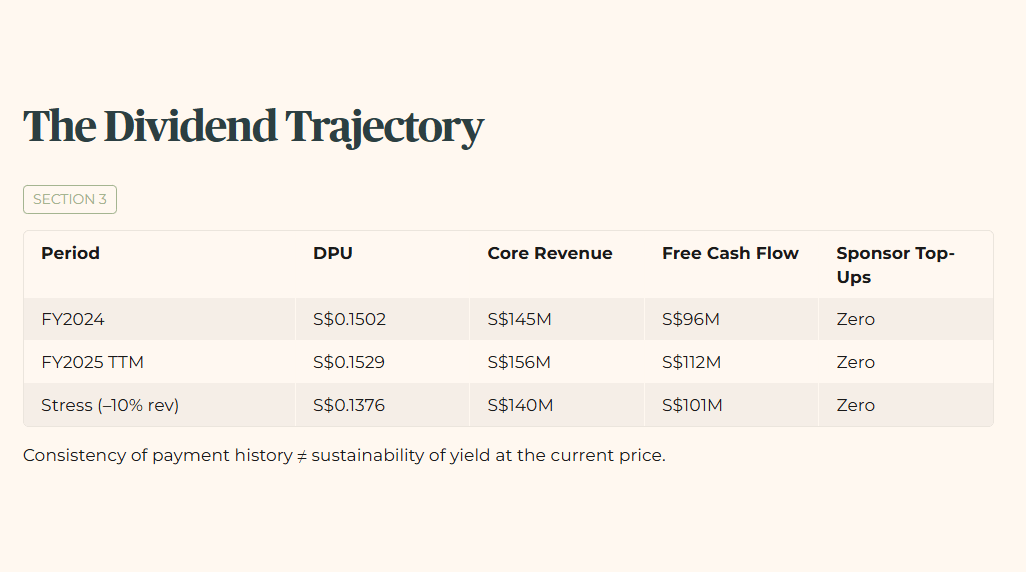

This REIT has a long history of raising its distribution slowly and steadily. That consistency is real, and it explains the loyal retail following. But consistency of payment history is not the same as sustainability of yield at the current price. The cash tells the real story.

Dividend Trajectory

The forward stress test is what matters here. If costs rise 10% — from energy, wages, or financing — free cash flow drops to S$101M. That is still above the distribution requirement, but the margin is thin.

Here is the number that matters most. The reported net profit of S$161M sounds reassuring. But S$36M of that is paper gains from revaluing buildings upward. That is not cash you can spend. The real cash supporting your distribution cheque is the free cash flow figure of S$112M. That is the honest economic foundation of this portfolio, and it is what I base the forensic verdict on — not the accounting profit line.

The free cash flow strip above clears the accounting noise — but the S$1.80 valuation gap in the next section reveals exactly what assumptions you are paying for when you buy at S$4.01 today.