ParkwayLife REIT 1H 2025: Slide-by-Slide Deep Dive — Why The Premium Still Makes Sense

Most Singapore investors see a REIT trading at a 68% premium to NAV and immediately think “overvalued.” That’s an easy take—but it overlooks what ParkwayLife REIT’s latest results really mean ......

ParkwayLife REIT 1H 2025: Slide-by-Slide Deep Dive — Why The Premium Still Makes Sense

"Why does ParkwayLife REIT trade at such a crazy premium to book value?" If you've asked this, you're not alone—and the 1H 2025 business update gives us the clearest answers yet. Let me take you through the 10 most important slides that reveal exactly what's driving this healthcare REIT's continued outperformance, and why institutions keep paying up despite the "expensive" label.

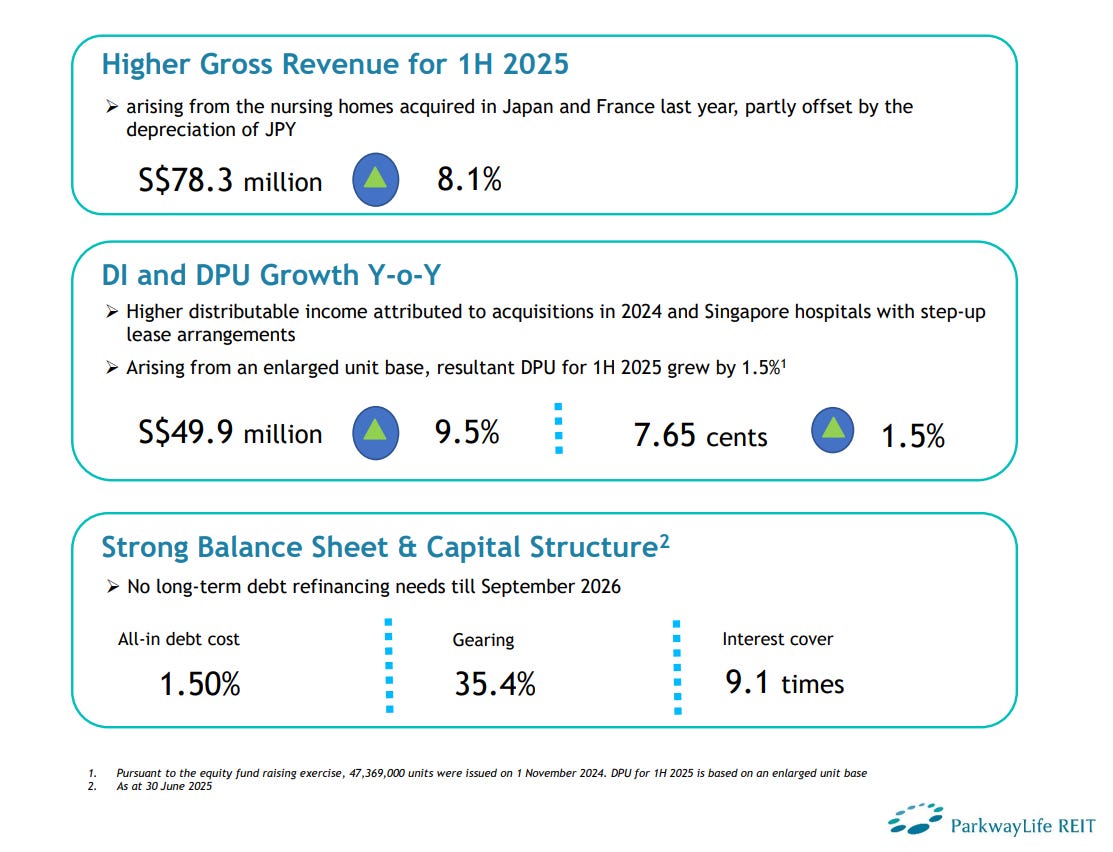

Slide 4: 1H 2025 Key Highlights — The Foundation of Quality

This opening slide immediately establishes why ParkwayLife commands premium valuations. The 9.5% growth in distributable income to S$49.9 million represents the fruits of strategic acquisitions made in 2024, particularly the August Japan nursing home purchase and December's French portfolio acquisition. What's remarkable is that despite an enlarged unit base following the November 2024 equity fundraising, DPU still managed 1.5% growth to 7.65 cents.