[PREMIUM] Safe Dividends: Which SG Bank (DBS / OCBC / UOB) Actually Survives a Recession?

We stress-tested the Big Three against Covid, the GFC, and current 2025 valuations. The winner for capital preservation isn’t who you think.

If you walk into any kopitiam in Singapore and ask for a stock recommendation, nine out of ten uncles will shout “DBS!”

And they aren’t wrong. DBS has been a growth monster, executing flawlessly under Piyush Gupta and continuing that momentum into late 2025. But here is the uncomfortable truth that momentum investors often forget: The stock that goes up the fastest often falls the hardest.

For the 45-year-old accumulator or the 60-year-old retiree using CPF and SRS funds, “Growth” is secondary. The primary objective is Capital Preservation and Income Stability. When the next inevitable recession hits, you don’t need a Ferrari; you need a tank.

Today, I am putting the “Big Three” (DBS, UOB, and OCBC) through a rigorous stress test. We aren’t looking at who made the most money last quarter. We are looking at who survives the best when the world catches fire.

We are testing for the “Fortress Factor.”

In This Article:

• Round 1: The “Covid Crash” Test (Resilience)

• Round 2: The “Dividend Shield” Test (Reliability)

• Round 3: The “Fortress” Check (Asset Quality)

• InvestingPro Reality Check

• Round 4: Valuation (The Price You Pay)

• The Iguana Playbook: The “Rotation” Strategy

• Iggy’s Verdict: The “Barbell” ApproachRound 1: The “Covid Crash” Test (Resilience)

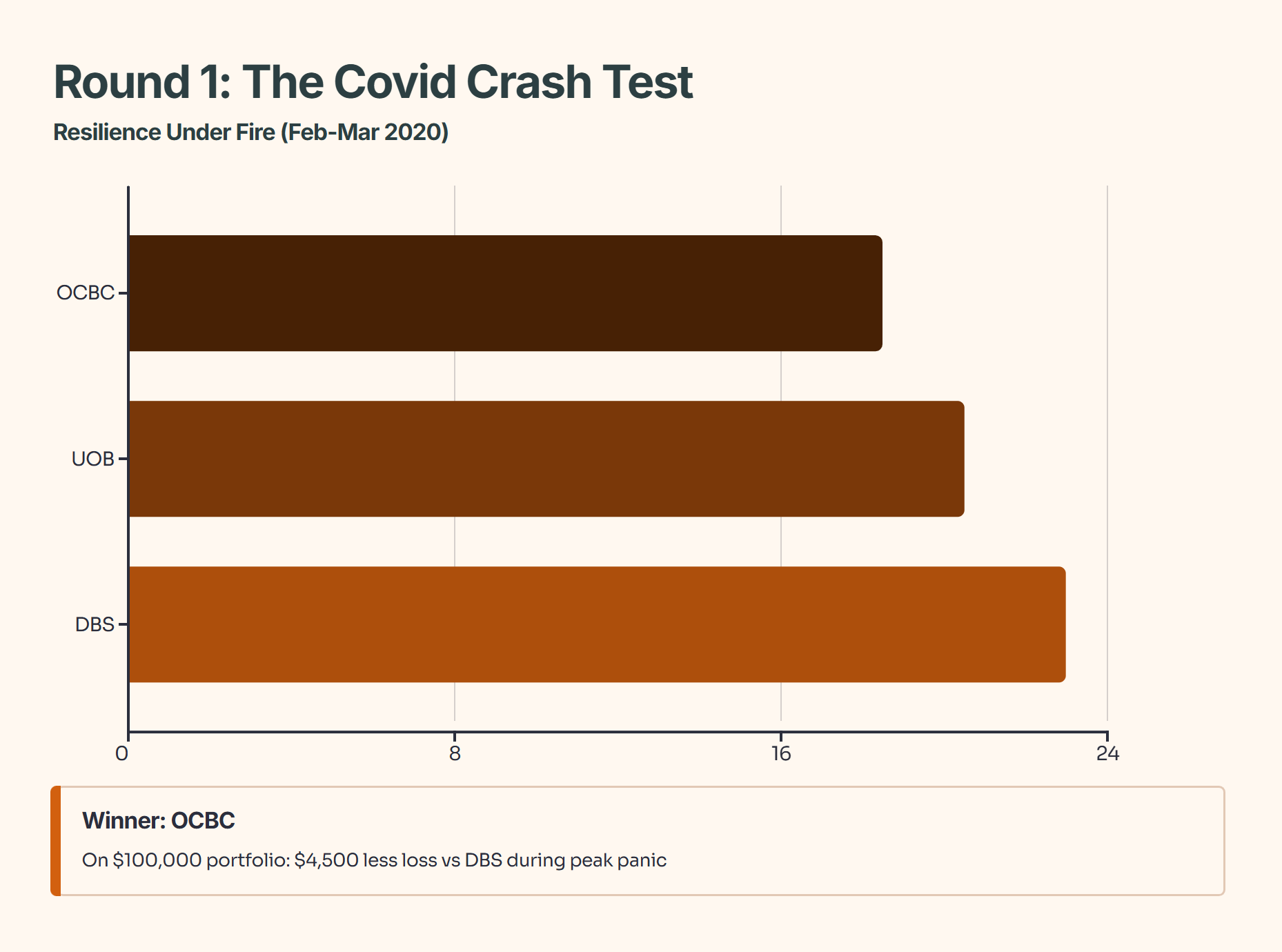

The best way to predict how a bank behaves in a crisis is to look at the last time the world almost ended. In February and March 2020, fear was at its peak. Here is how the banks handled the drawdown.

While the difference between 18.5% and 23.0% might seem small on paper, on a $100,000 portfolio, that is a difference of $4,500 in pure paper loss during a time of extreme panic.

Iggy’s Insight:

The market perceives OCBC as the “boring” bank. Good. In a crash, boring is your best friend. OCBC’s lower beta (volatility) during the Covid crash suggests that its shareholder base is stickier and less prone to speculative selling than DBS’s. If you panic easily, OCBC is the structural choice for your portfolio.

🛑 Stop Here.

In the next section, we analyze the Dividend Safety (one bank is at risk), reveal the Institutional Fair Value Models (one bank has 17.5% upside), and give the final Buy/Sell/Hold verdict.

Premium Members also get access to the exclusive InvestingPro discount code (50% off) inside this post, which pays for your subscription instantly.

Round 2: The “Dividend Shield” Test (Reliability)

For most of my readers, dividends aren’t just a bonus; they are the grocery bill. A bank that cuts dividends during a crisis is failing its primary duty to income investors.

Here we have a split verdict. In the modern era (2020), UOB showed the most resistance to dividend cuts, slicing their payout marginally less than DBS.

However, we must give credit to OCBC’s history. During the 2008 Global Financial Crisis—a crisis specifically centered on banking solvency—OCBC was the only local bank that maintained its dividend (S$0.28).

Iggy’s Take:

History rhymes. OCBC’s conservative management style (often criticized by growth investors) is exactly what allows them to maintain payouts when liquidity dries up. However, right now in late 2025, UOB is the income king. With a forecasted yield nearing 6%, you are getting paid a significant risk premium to hold UOB compared to the pricier DBS.

Round 3: The “Fortress” Check (Asset Quality Q3 2025)

A bank is only as good as its loan book. If the economy slows down in 2026, which bank has the highest exposure to bad debts? Let’s look at the Q3 2025 numbers.