The Order Book Is Full. The Bank Account Is Empty. | EP1654🦖

The CSE Global Forensic Audit: When Accounting Profit and Bank Account Reality Tell Two Different Stories

CSE GLOBAL — ANALYST RATING REVIEW

The Order Book Is Full. The Bank Account Is Empty.

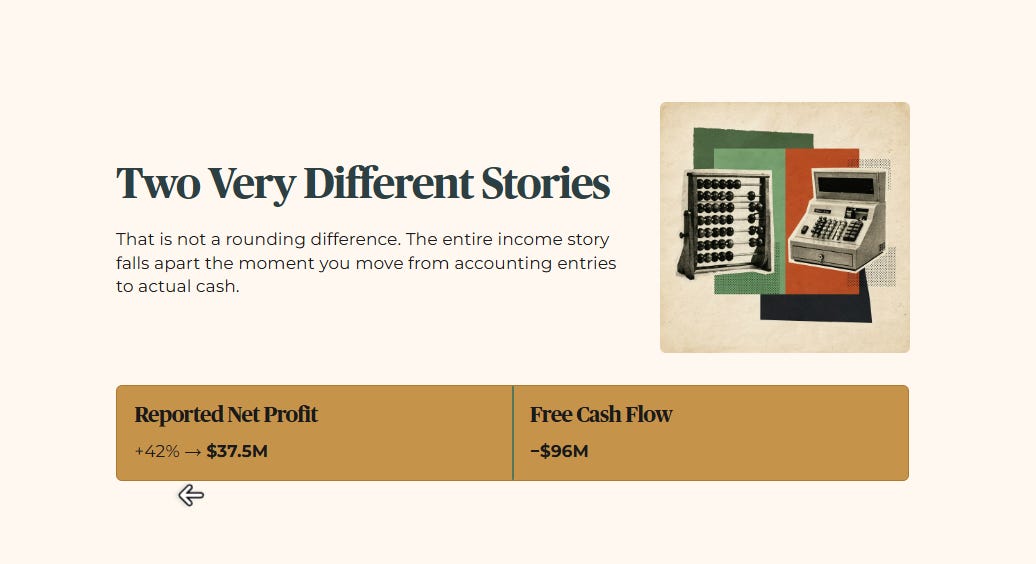

Reported net profit is up 42% to thirty-seven point five million dollars. But actual free cash flow has collapsed to negative ninety-six million dollars. That is not a rounding difference. That is the entire income story falling apart the moment you move from accounting entries to actual cash.

Who This Analysis Is For

Sell-side analysts covering CSE Global are largely optimistic. KGI Securities carried a BUY rating with a price target of one dollar forty-five as recently as March 2026. The five-analyst consensus sits at one dollar ninety-five on average. If you are a growth investor with a multi-year runway and a high tolerance for balance sheet turbulence, that optimism has a logical foundation: the data centre electrification order book is real, revenue growth is real, and the engineering business has genuine long-cycle tailwinds.

This forensic review is not built for that investor.

It is built for the Singaporean who is five to ten years from retirement, or already in it, managing CPF savings and SRS capital that cannot afford a structural write-down. For that investor, the order book headline and the cash flow reality are telling two completely different stories. This review reads the second one.

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips, the interest coverage, the gearing, the free cash flow sustainability, so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

In This Article:

CSE Global Analyst Rating Review

The Institutional Thesis

The Forensic Gap

Dimension One: Valuation

Dimension Two: Income

Dimension Three: Execution Risk

Dimension Four: Ownership Signal

Dimension Five: Who Is This For

Financial Health Checklist

Dividend Trajectory

Peer Comparison

The Zone Gate

Iggy's Insight

What This Means For You

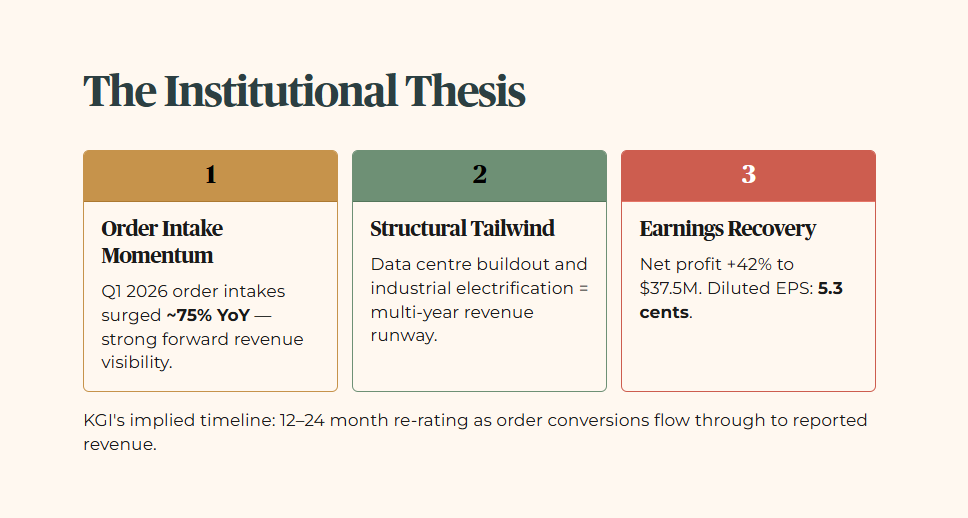

The Institutional Thesis

KGI Securities maintained a BUY rating on CSE Global in March 2026 with a price target of one dollar forty-five. The broader sell-side consensus across five analyst houses sits at an average target of one dollar ninety-five, representing significant upside from current levels.

The institutional case rests on three pillars. First, order intake momentum: first-quarter 2026 order intakes surged approximately 75% year on year, signalling strong forward revenue visibility in the company’s electrification and automation segments. Second, structural tailwind: the global push for data centre buildout and industrial electrification creates a multi-year revenue runway for an engineering services business of this profile. Third, earnings recovery: reported net profit for full-year 2025 rose 42% to thirty-seven point five million dollars, and diluted earnings per share increased to five point three cents.

KGI’s valuation methodology applies a forward price-to-earnings multiple to the expected earnings recovery. The implied timeline for the thesis is a twelve to twenty-four month re-rating as order conversions flow through to reported revenue and earnings.

That is the growth investor’s case, stated fairly and completely.

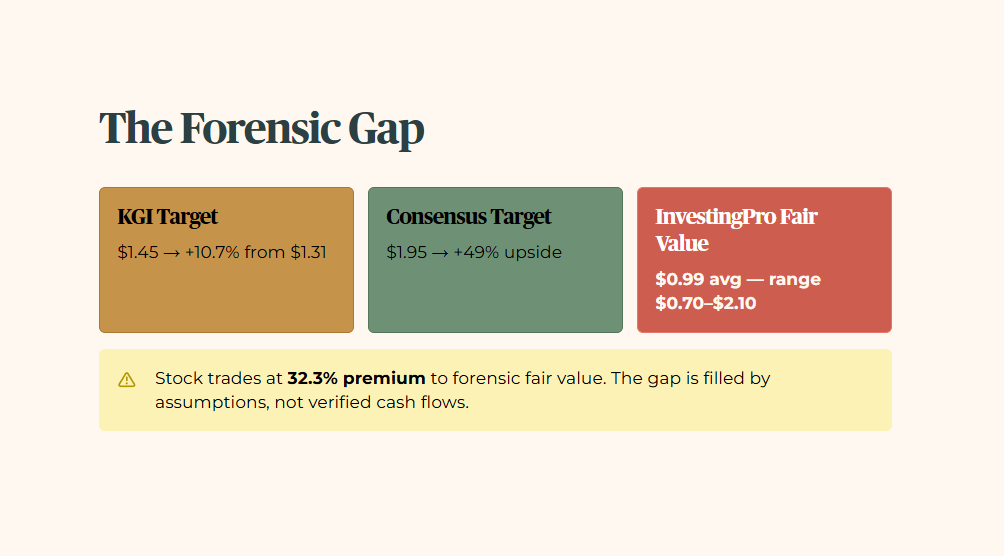

The Forensic Gap

KGI’s price target of one dollar forty-five implies a 10.7% premium to today’s price of one dollar thirty-one. The five-analyst consensus of one dollar ninety-five implies upside of approximately 49%.

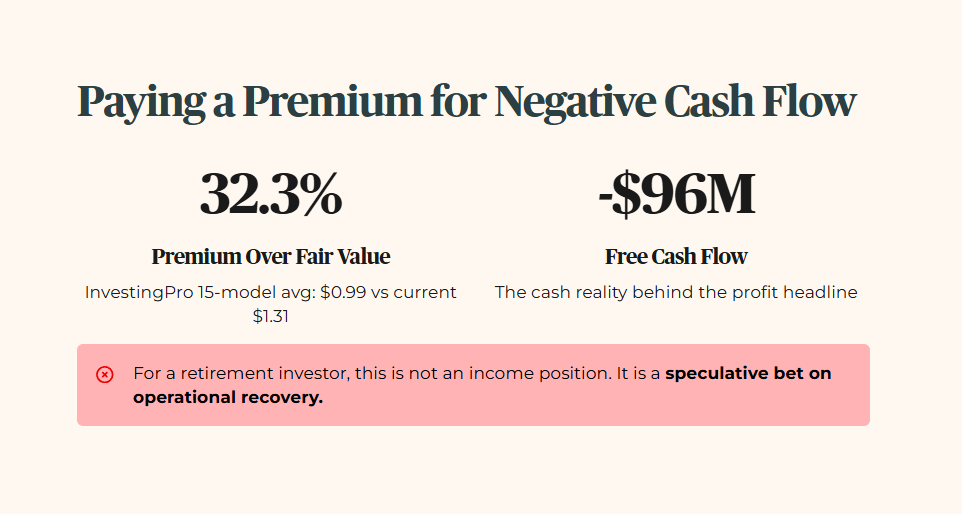

InvestingPro’s fair value model, which aggregates fifteen independent valuation methodologies across discounted cash flow, earnings multiples, and dividend models, places the average fair value at ninety-nine cents. At one dollar thirty-one, the stock is trading at a 32.3% premium to that forensic estimate. The fair value range runs from seventy cents to two dollars ten, reflecting genuine uncertainty in a business where cash flow and reported profit have diverged sharply.

The gap between the institutional price targets and the InvestingPro fair value is not filled by verified cash flows. It is filled by assumptions about order conversion, margin recovery, and working capital normalisation. None of those assumptions are visible in the current cash account.

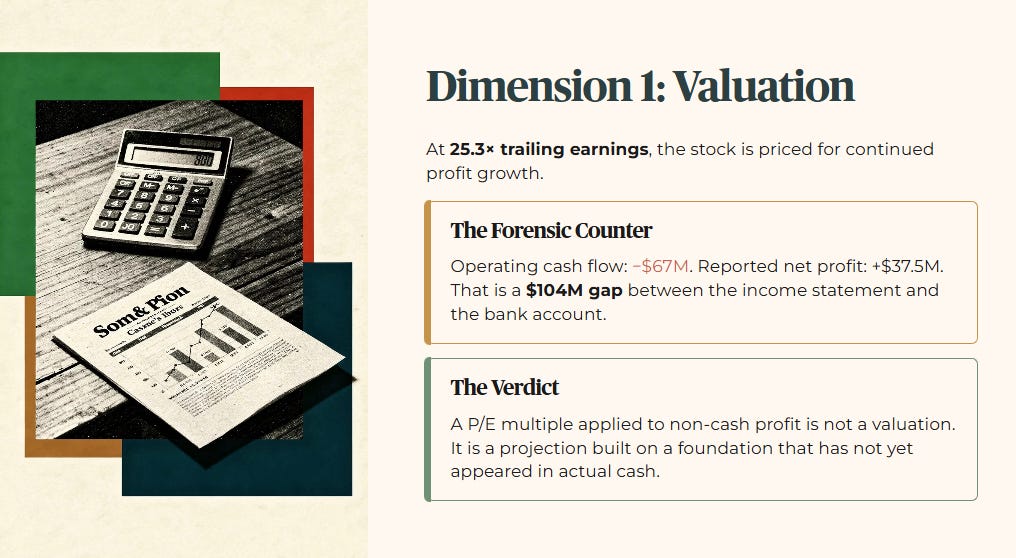

Dimension One: Valuation

The institutional valuation anchor is a forward price-to-earnings multiple applied to the earnings recovery narrative. At twenty-five point three times trailing earnings, the stock is priced for continued profit growth.

The forensic counter is simple. Earnings without cash are an accounting construction, not a financial reality. When operating cash flow is negative sixty-seven million dollars in the same period that reported net profit is thirty-seven point five million dollars, you have a one-hundred-and-four-million-dollar gap between what the income statement says and what the bank account says. A forward price-to-earnings multiple applied to non-cash profit is not a valuation. It is a projection built on a foundation that has not yet appeared in the company’s actual cash position.

InvestingPro’s fifteen-model average of ninety-nine cents, sitting 32.3% below the current price of one dollar thirty-one, reflects that cash flow reality more honestly than a multiple applied to reported earnings.

For a retirement investor, paying a 32.3% premium over forensic fair value for a business burning ninety-six million dollars in free cash flow is not an income position. It is a speculative bet on operational recovery.

Dimension Two: Income

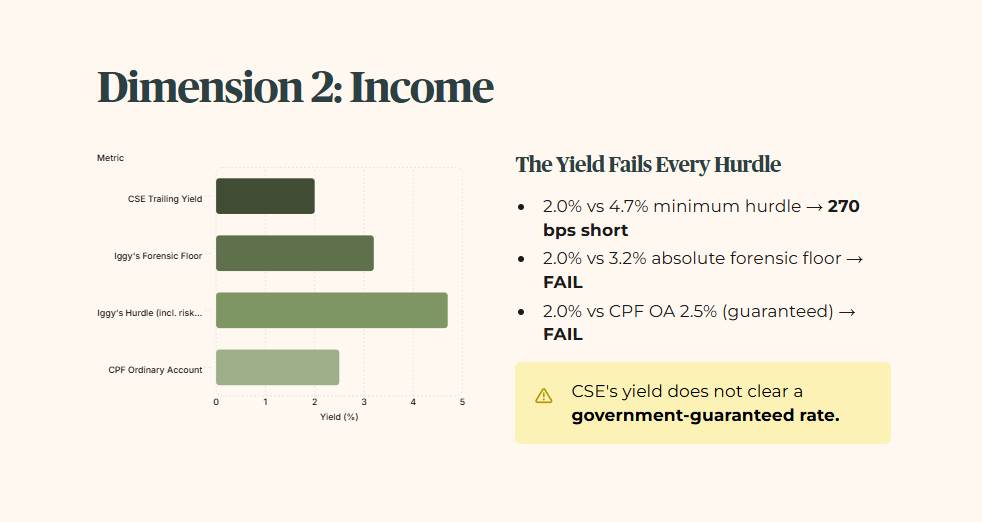

The trailing dividend yield at the current price of one dollar thirty-one is 2.0%.

Iggy’s minimum yield hurdle is 4.7%. That is the 3.2% personal forensic floor plus 150 basis points of mandatory risk premium, representing the minimum return that justifies the risks of being in the open market: gearing risk, distribution cuts, and the possibility of permanent capital loss.

At 2.0%, the yield fails the 4.7% hurdle by 270 basis points. It also fails the 3.2% absolute forensic floor.

For context: the CPF Ordinary Account pays 2.5% with a government guarantee. CSE Global’s trailing yield of 2.0% does not clear a guaranteed government rate. The six-month Singapore Treasury Bill last cleared at 1.60% per annum at the 31 December 2025 auction. Even at that depressed level, the yield spread over a risk-free instrument is barely forty basis points, before accounting for any equity risk.

The yield has already failed the 4.7% forensic hurdle on headline numbers — but the next section’s cash flow and debt funding trail shows why this apparent “2.0% income play” is actually a leveraged liability in disguise.