RetireBy50’s Investment Playbook—Can It Work for Singaporeans Seeking Early Retirement?

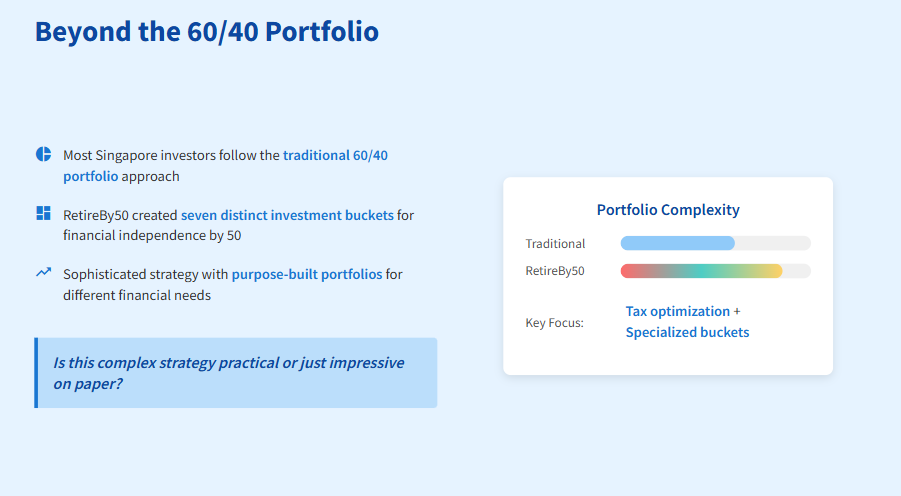

The big question: Is this complex strategy actually practical for your retirement, or just financial engineering that sounds impressive on paper?

Most Singapore investors chase the same boring 60/40 portfolio, but RetireBy50 built seven distinct investment buckets to hit financial independence by 50. The big question: Is this complex strategy actually practical for your retirement, or just financial engineering that sounds impressive on paper?

After analyzing RetireBy50's detailed portfolio breakdown, I'm seeing both brilliant tax optimization moves and some concerning red flags that could derail early retirement dreams. Let me break down what works, what doesn't, and whether you should copy this approach.

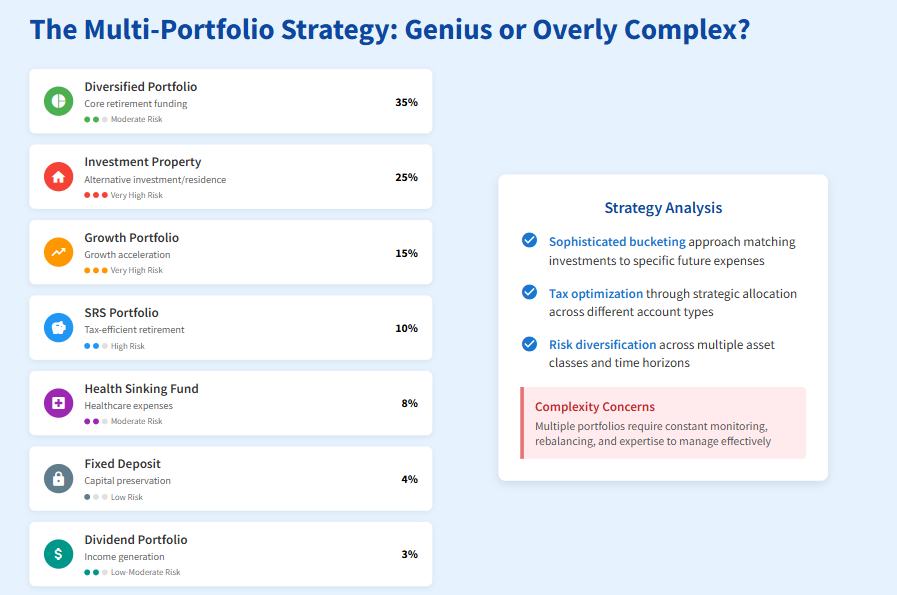

The Multi-Portfolio Strategy: Genius or Overly Complex?

RetireBy50 doesn't just throw money into a single investment account. Instead, he's created seven separate portfolios, each with specific purposes and time horizons. Here's the complete breakdown of his approach:

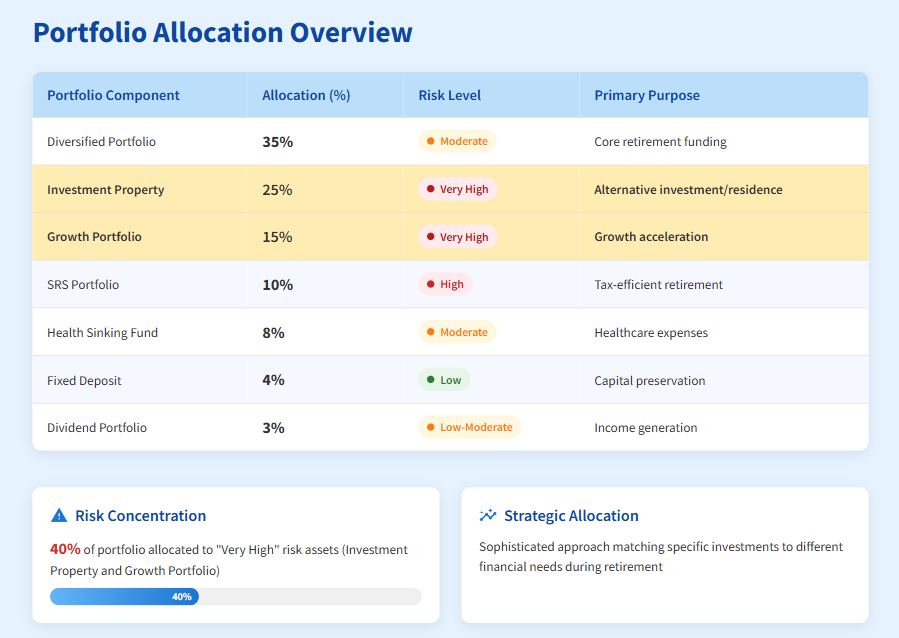

Table: RetireBy50's Portfolio Allocation Overview

This table provides a bird's-eye view of the entire strategy. It immediately shows that while the "Diversified Portfolio" forms the core, a significant 40% is allocated to "Very High" risk assets (Investment Property and Growth Portfolio). This distribution is crucial for understanding the strategy's aggressive tilt and where the primary risks lie.

The strategy shows sophisticated thinking about different financial needs during retirement. Rather than hoping one portfolio handles everything, he's matching specific investments to specific future expenses. But complexity brings its own risks.

Portfolio-by-Portfolio Analysis: The Good, Bad, and Concerning

Here is a look at the different parts of the portfolio.

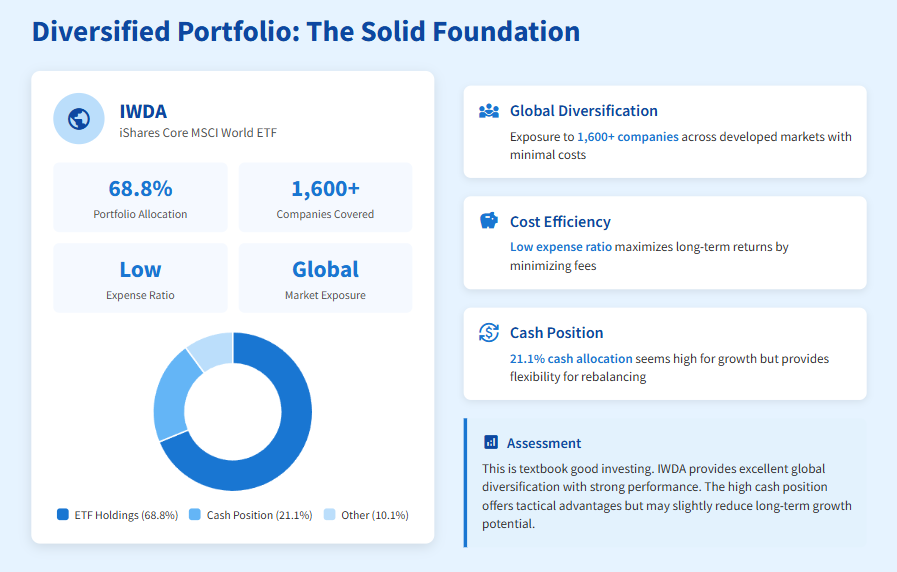

Diversified Portfolio: The Solid Foundation

The core holding centers on IWDA (iShares Core MSCI World ETF). This ETF has delivered strong performance. At a 68.8% allocation with a low expense ratio, this provides excellent global diversification.

My Assessment: This is textbook good investing. IWDA gives exposure to over 1,600 companies across developed markets with minimal costs. The 21.1% cash position seems high for long-term growth. But it provides flexibility for rebalancing opportunities.