RHB Says Hold Tight on OCBC: Is That 5.7% Yield Worth the Wait Through More Earnings Pain?

We break down the bull case (wealth management) vs. the bear case (profit squeeze) ahead of Q3 results.

RHB Bank Singapore just put out a “neutral” call on OCBC ahead of third-quarter results. Translation? They’re not jumping up and down with excitement. The big question: should you hold through another round of profit declines, or is that juicy 5.7% dividend yield enough reason to stay put?

OCBC will report its third-quarter numbers on November 7, 2025. RHB expects the bank to post another mid-single-digit profit drop compared to last year. The culprits are the same ones that hurt second-quarter results: squeezed lending margins and weaker trading income. But here’s the twist—investors won’t just be looking at the numbers. They’ll be scanning every word of management’s guidance for clues about 2026, especially with CEO Helen Wong passing the baton to Tan Teck Long on January 1, 2026.

Let me break down what’s really happening with OCBC, why RHB is cautious, and whether this stock deserves a spot in your Singapore portfolio.

In This Article:

• The Profit Squeeze Is Real

• Trading Income Won’t Save the Day Either

• Wealth Management: The Silver Lining

• Asset Quality Remains Rock Solid

• The CEO Succession: What to Watch on November 7

• The 5.7% Yield: Is It Enough?

• CPF and SRS Suitability

• Risks to Consider

• The Verdict: Hold for the Yield, but Don’t Expect FireworksThe Profit Squeeze Is Real

OCBC’s first half of 2025 already showed the pain. Net profit fell 6% year-on-year to S$3.70 billion. The second quarter alone saw a 7% drop to S$1.82 billion. RHB thinks the third quarter will follow the same pattern—down mid-single digits from last year.

The main problem is net interest income, which makes up the bulk of bank earnings. This is the money banks make from the difference between what they charge on loans and what they pay on deposits. OCBC’s NII fell 5% in the first half, dragged down by margin compression.

What’s margin compression? Think of it this way: when benchmark interest rates like SORA and HIBOR fall fast, the rates banks charge on loans drop faster than the rates they pay on deposits. OCBC’s net interest margin shrank 25 basis points in the first half to 1.98%. In the second quarter alone, NIM fell to 1.92%—down 28 basis points year-on-year and 12 basis points from the first quarter.

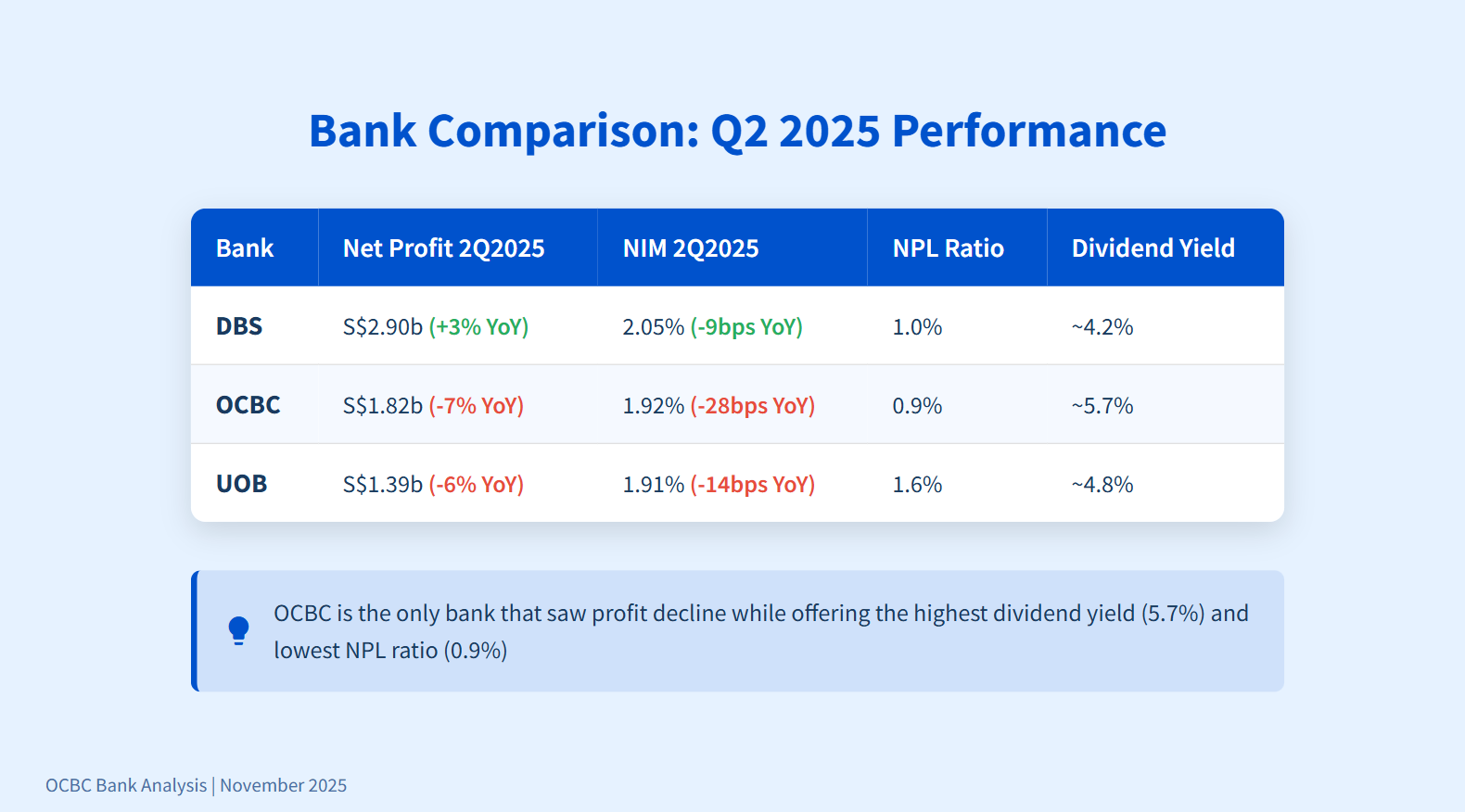

OCBC cut its full-year NIM guidance to 1.90-1.95%, down from around 2% previously. For context, OCBC’s NIM compression is sharper than its peers. DBS saw only a 9-basis-point drop to 2.05%, while UOB fell 14 basis points to 1.91% in the second quarter. OCBC’s bigger hit stems from higher sensitivity to Singapore dollar and Hong Kong dollar rate changes. About half of OCBC’s loan book is in these currencies, with 80% of Singapore dollar loans and nearly all Hong Kong dollar loans on floating rates.

Here’s a table showing how OCBC stacks up against DBS and UOB in the second quarter of 2025:

OCBC is the only one of the three big banks that saw profit fall in a tough quarter, while DBS managed to grow. But OCBC does have the highest dividend yield and the lowest NPL ratio, which we’ll dig into shortly.

Iggy’s Take: The margin squeeze is hitting OCBC harder than DBS or UOB. If you’re counting on lending income to drive earnings, OCBC is not your best bet right now. DBS has better hedging in place and a more balanced deposit base, which explains why it posted profit growth while OCBC and UOB declined. But don’t write OCBC off yet—there are bright spots.

Trading Income Won’t Save the Day Either

OCBC enjoyed strong trading income in the first half, up 6% to S$771 million. Customer flow treasury income rose 10%, helped by both wealth clients and corporate customers. But RHB expects trading income to cool off in the third quarter compared to the second quarter.

Why? Market volatility has settled down. The big trading wins in the first half came from clients repositioning ahead of rate cuts and shifting between fixed deposits and investment products. That rush has eased. Without a fresh wave of market turbulence or aggressive client moves, trading desks won’t deliver the same punch.

Iggy’s Take: Trading income is a nice bonus but it’s lumpy and unpredictable. You can’t count on it to bail out weak lending income every quarter. OCBC’s trading strength in the first half was real, but it’s not a sustainable earnings driver. If you’re investing in OCBC, focus on the wealth management story, not trading wins.

Wealth Management: The Silver Lining

Here’s where OCBC shines. Wealth management income grew 4% to S$2.66 billion in the first half, making up 37% of total income. Net fee income surged 19% to S$1.13 billion, driven by wealth management fees, which climbed 25%.

OCBC’s banking wealth management assets under management hit an all-time high of S$310 billion, up 11% from a year ago. This came from net new money flowing in and positive market valuations. Wealth management is now a core pillar for OCBC, and the bank is doubling down on this segment.

The wealth surge isn’t unique to OCBC. All three Singapore banks reported strong wealth fee growth in the first half as affluent clients ramped up trading activity and moved assets into the city-state. But OCBC’s 25% wealth fee growth is impressive and shows the bank is winning in this competitive space.

Here’s a breakdown of OCBC’s income sources in the first half of 2025:

Non-interest income is carrying the load as NII declines. Fee income and trading both grew, while insurance took a hit from mark-to-market effects on Great Eastern’s contract liabilities as rates fell.

Iggy’s Take: Wealth management is OCBC’s ace. If you believe Singapore will continue attracting high-net-worth individuals and family offices, OCBC is positioned to capture that growth. The 11% jump in AUM and 25% surge in wealth fees show the bank is executing well. This is the reason to own OCBC despite the margin squeeze. Just remember—wealth fees can be volatile and depend on market sentiment and client activity.

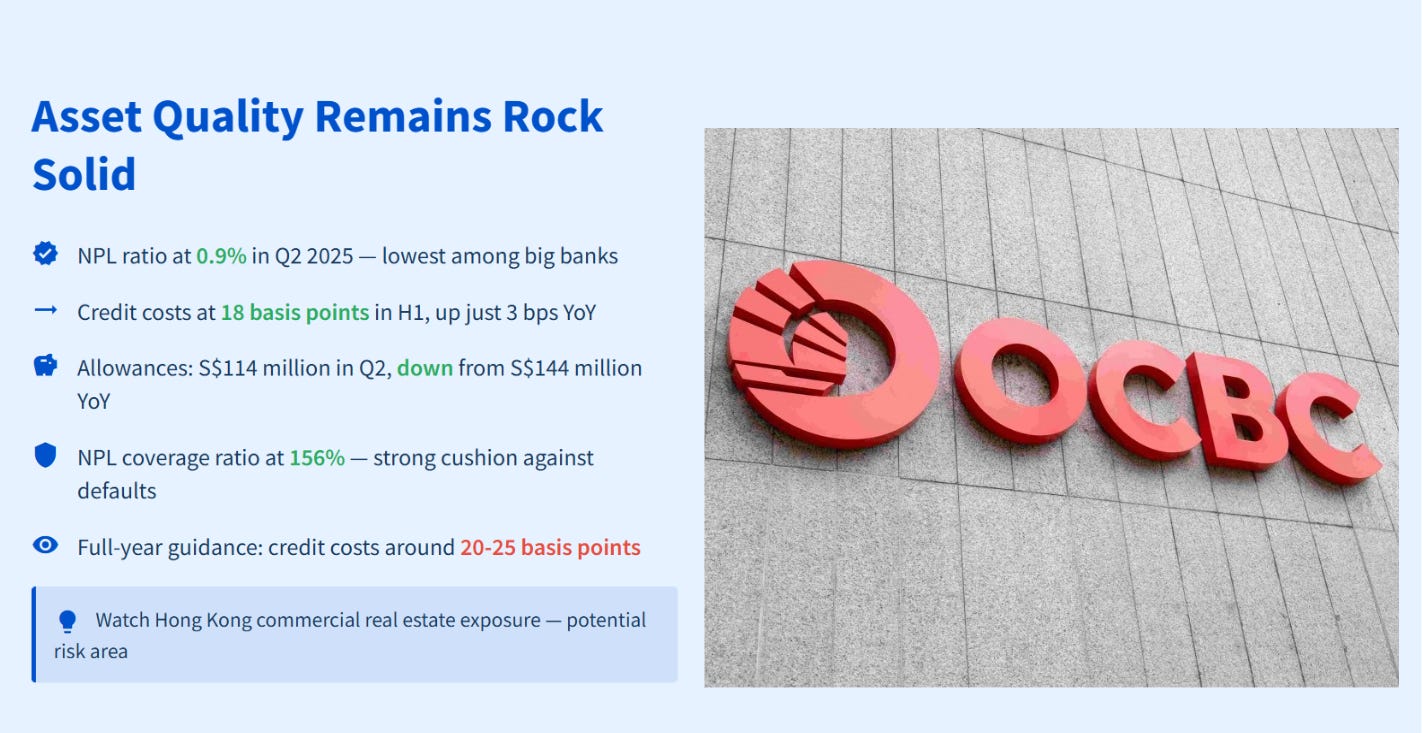

Asset Quality Remains Rock Solid

OCBC’s non-performing loan ratio stayed at 0.9% in the second quarter—the lowest among the three big banks. Credit costs stood at 18 basis points in the first half, up just 3 basis points from last year. The bank set aside S$114 million in allowances in the second quarter, down from S$144 million a year ago.

OCBC’s NPL coverage ratio is 156%, meaning the bank has plenty of cushion if loans go bad. Management has guided for credit costs to remain around 20-25 basis points for the full year, which is manageable.

There is one area to watch: Hong Kong commercial real estate. OCBC has exposure to mid-tier commercial properties in Hong Kong, a sector that’s under pressure. Management said they’re monitoring this closely and working with clients to provide support. RHB and other analysts expect further recognition of non-performing loans and credit losses in the second half, particularly for OCBC and UOB.

Iggy’s Take: Asset quality is strong but not bulletproof. The 0.9% NPL ratio is excellent and shows disciplined underwriting. But keep an eye on Hong Kong commercial real estate. If this sector deteriorates further, OCBC could see higher credit costs and NPL formation in 2026. For now, the risk is manageable, but it’s a yellow flag, not a green light.

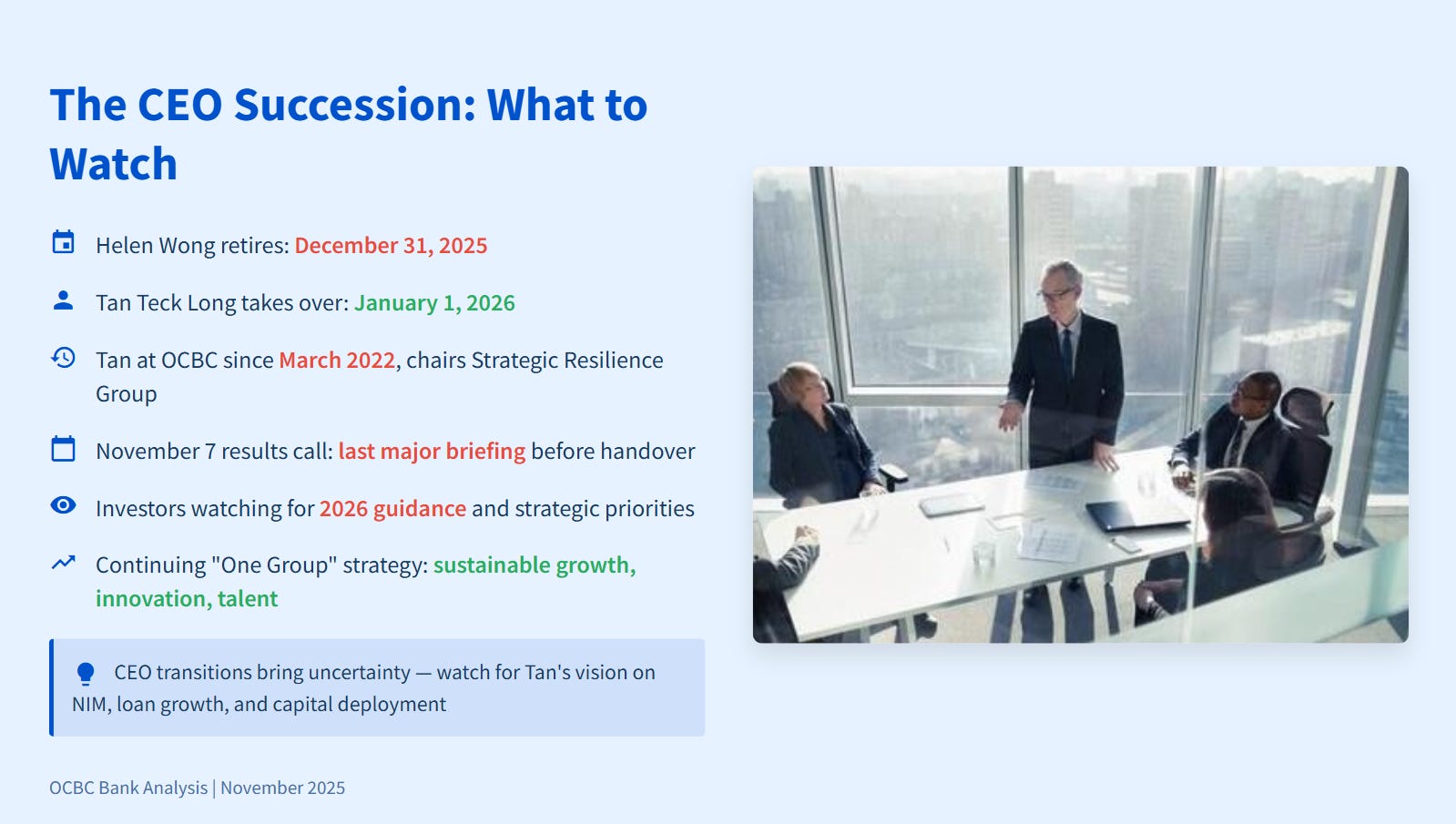

The CEO Succession: What to Watch on November 7

Helen Wong will retire on December 31, 2025, after a strong five-year run. She’ll be succeeded by Tan Teck Long, currently head of global wholesale banking and newly appointed deputy CEO. Tan has been at OCBC since March 2022 and chairs the OCBC Strategic Resilience Group, which is recalibrating the bank’s position in a changing global landscape.

The November 7 results call will be one of the last major earnings briefings before the handover. Investors will be listening for clues about 2026 guidance and strategic priorities. Tan has already signaled he’ll continue the “One Group” strategy, focusing on sustainable growth, innovation, and talent development. But will he tweak the approach? Will he double down on wealth management? Will he streamline operations or push harder into regional markets?

Here’s the CEO succession timeline:

Iggy’s Take: CEO transitions are tricky. Wong delivered strong results, but the macro environment is turning tougher. Tan’s track record in wholesale banking is solid, but he’s stepping into the top job at a challenging time with margin pressure, rate uncertainty, and geopolitical risks. The third-quarter results call is your chance to hear Tan’s vision and assess whether he’s the right leader for the next phase. Pay close attention to his comments on 2026 NIM, loan growth, and capital deployment.

The 5.7% Yield: Is It Enough?