S&P Global Ratings APAC Sector Watch: What It Means for Singapore Investors

Four Sectors, One Question: Are You Positioned or Exposed?

S&P Global Ratings has just released an Asia-Pacific sector analysis that strips away the usual brokerage house marketing. They are a global credit ratings agency with a mandate to look at structural risks, not to pump up stock prices. When a global institution flags regional economic shifts, it carries serious weight for someone managing a CPF or Supplementary Retirement Scheme portfolio in Singapore.

Four of the five sectors highlighted by S&P Global Ratings have direct consequences for your investable cash, your utility bills, or both. Here is the plain-language reality of what their credit analysts are seeing.

Gaming: The Premium Turf War

REITs: Supply Bottlenecks vs. Asset Reality

Technology: The AI Infrastructure Gamble

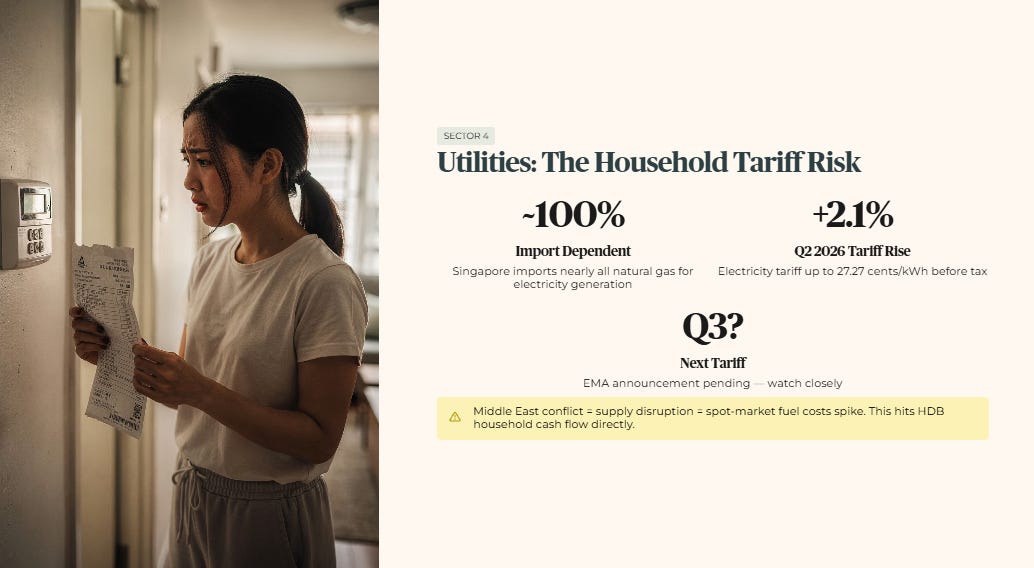

Utilities: The Household Tariff Risk

The Bottom Line

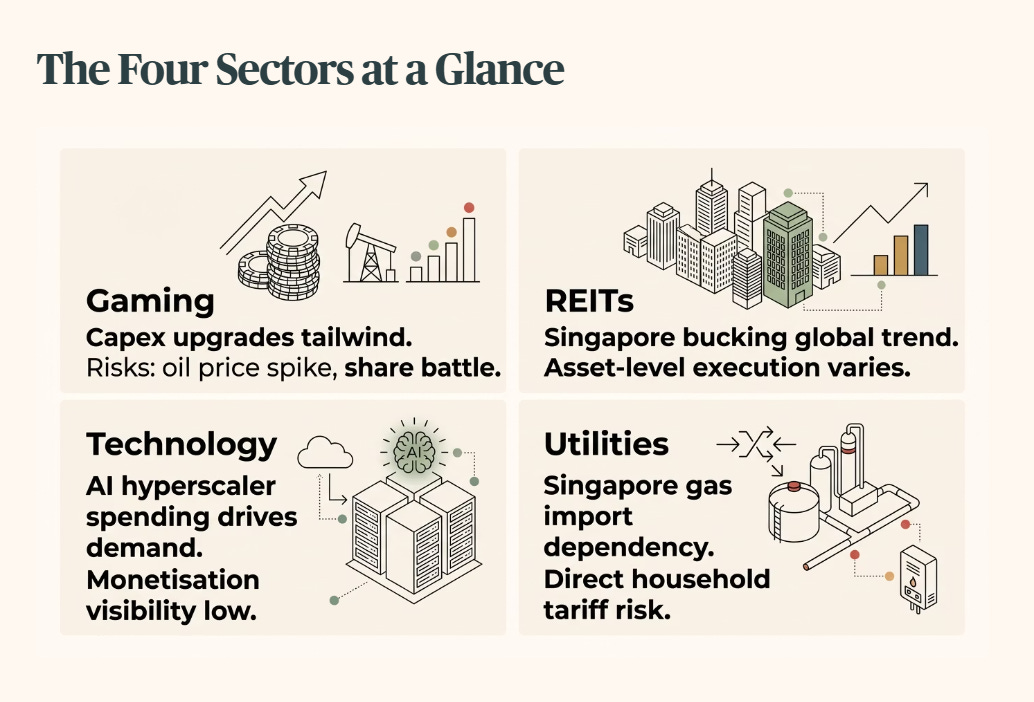

1. Gaming: The Premium Turf War

S&P Global Ratings expects gross gaming revenue, meaning the total amount of money collected from casino operations before deducting expenses, to climb across Singapore and Malaysia. The drivers are higher visitor numbers, major asset upgrades, and regional tourism campaigns.

The report highlights that Marina Bay Sands completed a 1.8 billion US dollar multi-year reinvestment programme in 2025. Meanwhile, Resorts World Sentosa, operated by Genting Singapore, is rolling out new attractions under its 6.8 billion Singapore dollar transformation plan. S&P Global Ratings notes that Genting Malaysia is similarly positioned to capture regional volume.

The major risk flagged by the ratings agency is geopolitical friction in the Middle East. If tensions escalate, oil prices could spike, driving up travel costs and squeezing the budgets of price-sensitive holidaymakers.

🟠Angela’s Observation

What I keep noticing here is that both of Singapore’s integrated resorts are going through the same capital-heavy reinvestment phase at the same time. That means they are about to fight over the exact same pool of premium international travellers, just with newer hardware. The question I cannot shake is whether Singapore’s tourism market is growing fast enough to feed both pipelines, or whether this turns into an expensive share battle between two heavily capitalised giants. Brent crude has cooled to somewhere between 72 and 75 US dollars a barrel recently, which helps, but any flare-up in the Middle East wipes that out fast, pushing up airfares and denting visitor numbers right when both properties need to start earning back their billions in capex.

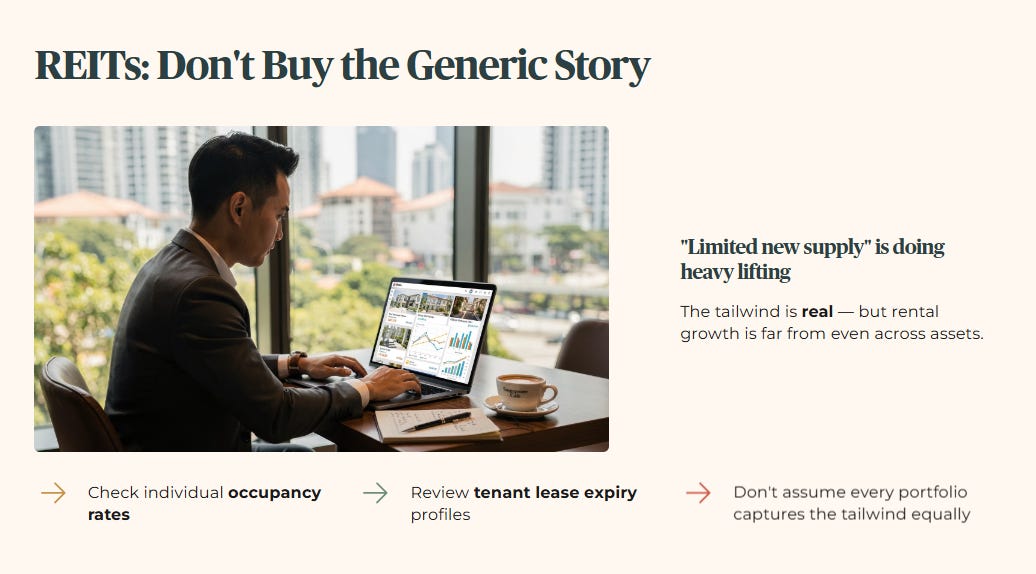

2. REITs: Supply Bottlenecks vs. Asset Reality

The recovery of office and retail spaces faces structural delays in several global gateway cities. However, S&P Global Ratings explicitly points out that Singapore and Tokyo are bucking this negative trend.

Singapore’s office sector is proving resilient due to steady corporate demand matched with limited new supply. The real pressure point for the wider sector remains funding costs, meaning the interest rates paid by landlords to service their corporate debt. S&P Global Ratings warns that if interest rates rise faster than expected or if property revenues stagnate, core credit metrics will deteriorate.

🟠Angela’s Observation

I think the phrase “limited new supply” is doing a lot of heavy lifting in the optimistic story for Singapore commercial real estate. When new office completions are low and corporate demand holds steady, landlords keep good pricing power at lease renewal. In theory that protects net property income. But when I look past the sector averages at asset-level performance inside our larger commercial REITs, the rental growth is far from even. The tailwind S&P Global Ratings describes is real, but individual asset execution varies a lot. I would not assume every property portfolio captures this tailwind equally. You still need to check individual occupancy and tenant lease expiry profiles rather than buy the generic sector story.

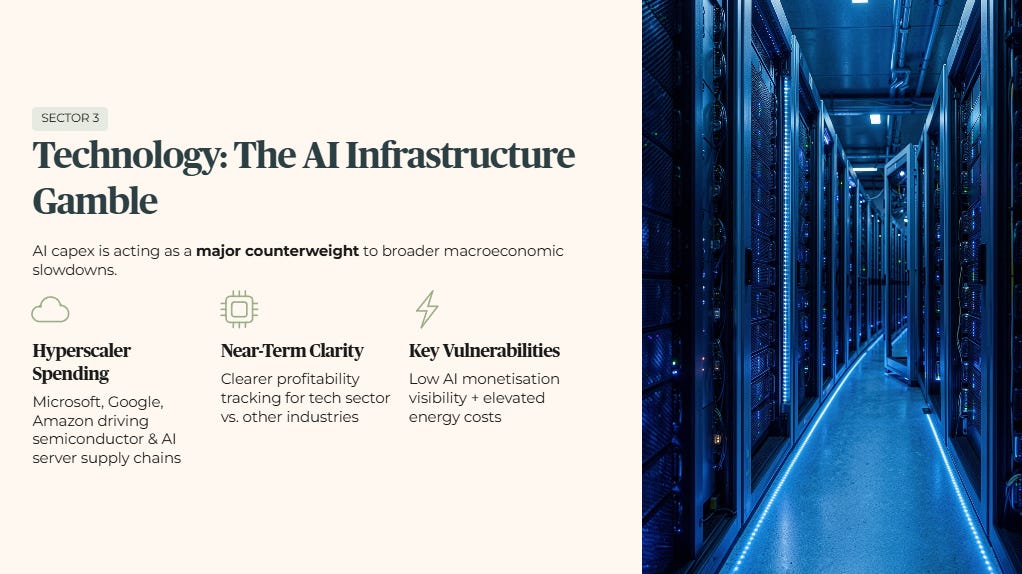

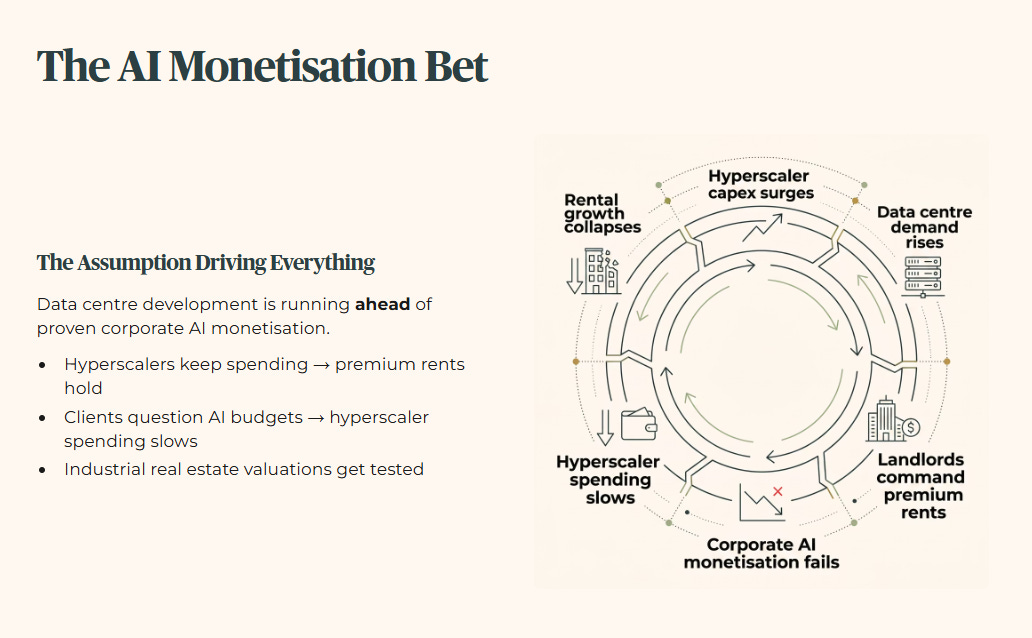

3. Technology: The AI Infrastructure Gamble

Artificial intelligence is acting as a major capital counterweight to broader macroeconomic slowdowns. S&P Global Ratings notes that surging capital expenditure from hyperscalers, meaning massive cloud service providers like Microsoft, Google, and Amazon, is directly benefiting the semiconductor and AI server supply chains. This provides the tech sector with much clearer near-term profitability tracking.

However, the agency underscores two key structural vulnerabilities: very low visibility on how companies will actually monetise AI at scale, and elevated energy costs. High energy costs or a sudden slowdown in data centre build-outs could weaken global computer chip demand.

🟠Angela’s Observation

The tension S&P Global Ratings points to here is very visible in industrial and specialised property too. The underlying demand for data processing capacity is real. Every cloud workspace and digital transaction needs physical servers somewhere. But data centre development right now is running ahead on the assumption that corporate AI monetisation will catch up with the spending. If the tech giants keep spending at this pace, data centre landlords in Singapore and North America keep commanding premium rents. If corporate clients start questioning their AI software budgets instead, hyperscaler spending slows down, and that tests the high occupancy and aggressive rental growth assumptions already priced into industrial real estate valuations.

4. Utilities: The Household Tariff Risk

Energy security is forcing major policy shifts across the Asia-Pacific region. S&P Global Ratings reports that several major economies are increasing coal generation to mitigate natural gas shortages.

The ratings agency flags Singapore and Taiwan as two highly vulnerable, gas-reliant markets. Because Singapore imports nearly all of its natural gas to fuel electricity generation, a prolonged Middle East conflict represents a direct operational threat. It could trigger supply disruptions, forcing utility providers to buy expensive spot-market fuel, which severely compresses corporate profit margins or drives up costs for end consumers

🟠Angela’s Observation

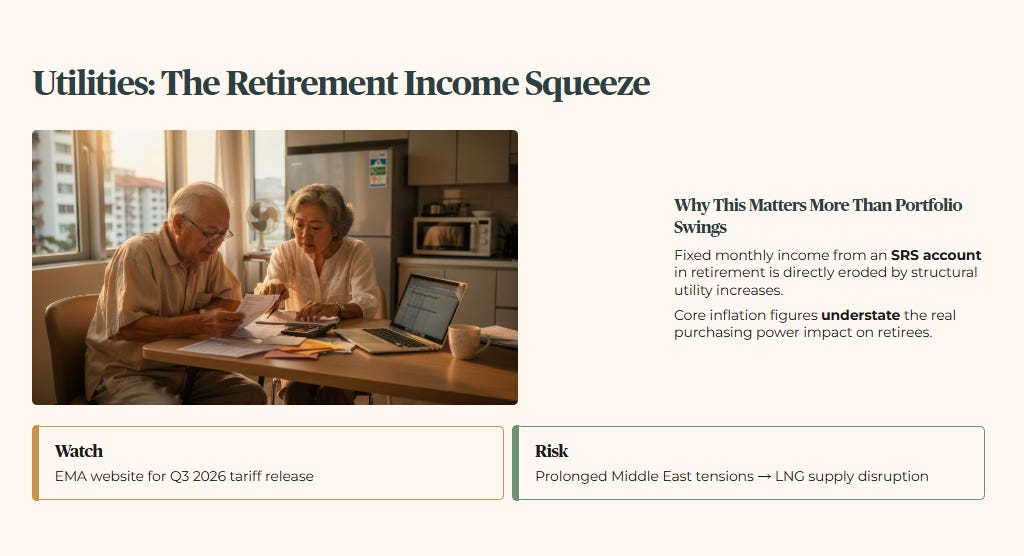

This is the one that hits household cash flow directly, more than any equity portfolio swing. Because our power system depends almost entirely on imported liquefied natural gas, the regulated electricity tariff every HDB household pays is tied straight to global energy volatility. The second-quarter 2026 tariff already moved up 2.1 percent to 27.27 cents per kilowatt-hour before tax. The third-quarter number has not been released yet, so I am watching the Energy Market Authority’s website for it. If you are drawing a fixed monthly income from an SRS account in retirement, this kind of structural utility increase eats into purchasing power faster than the core inflation number suggests.

Putting these four side by side, the pattern that jumps out at me isn’t really about any single sector doing well or badly. It’s that every one of them is a bet on something continuing that might not. Gaming is betting tourism keeps expanding fast enough to feed two newly upgraded resorts. REITs are betting that limited new supply keeps protecting rents even as individual buildings perform very differently underneath that average. Technology is betting that hyperscalers keep spending before anyone gets a clear answer on how AI actually pays for itself. And utilities are not really betting on anything, they are just exposed, because our gas dependency means the tariff risk shows up on your power bill whether you hold a single share or not.

That last point is really what ties the other three together for me. Gaming, REITs, and technology all carry a version of “this works as long as the current trend holds.” Utilities do not get that luxury. It is the one sector on this list where the consequence lands on every household in Singapore regardless of what is in your portfolio, which is part of why I keep coming back to it whenever I read these S&P Global Ratings sector calls.

The structural tariff risk and sector bets you have just seen set the scene, but the next section is where I translate those S&P credit metrics into a concrete SGX watchlist and the first-pass forensic filters I use before committing retirement capital.