S-REITs Report Card: Why Industrial REITs 🏭 Are Still Your “Boring But Good” Safe Haven

When everyone else is panicking about market volatility, smart money finds the assets that keep paying—quarter after quarter. Industrial S-REITs just proved (again) why boring wins.

The latest Q3 numbers are in. While retail REITs worry about consumer spending and office REITs battle work-from-home headwinds, Industrial S-REITs are doing what they do best: delivering stable occupancy, positive rental reversions, and steady income growth.

If you want excitement, go buy a volatile tech stock. If you want to sleep well at night and get paid while you do it, read on.

In This Article:

• 📊 The Numbers Don’t Lie: Industrial S-REITs Delivered

• 🌟 The 3 Key Takeaways (Deep Dive)

• 1. The “Growth Beast”: CapitaLand Ascendas REIT (CLAR)

• 2. The “Comeback Kid”: Mapletree Logistics Trust (MLT)

• 3. The “Small Cap Gem”: Alpha Integrated REIT

• 📈 Rental Reversion: The Metric That Matters

• 🛡️ Why Industrial is the “Defensive” Play

• 🇸🇬 The Singapore Context: Solving the “Supply” Paradox

• 💡 Iggy’s Take: Buy, Hold, or Sell?

• Final Thoughts

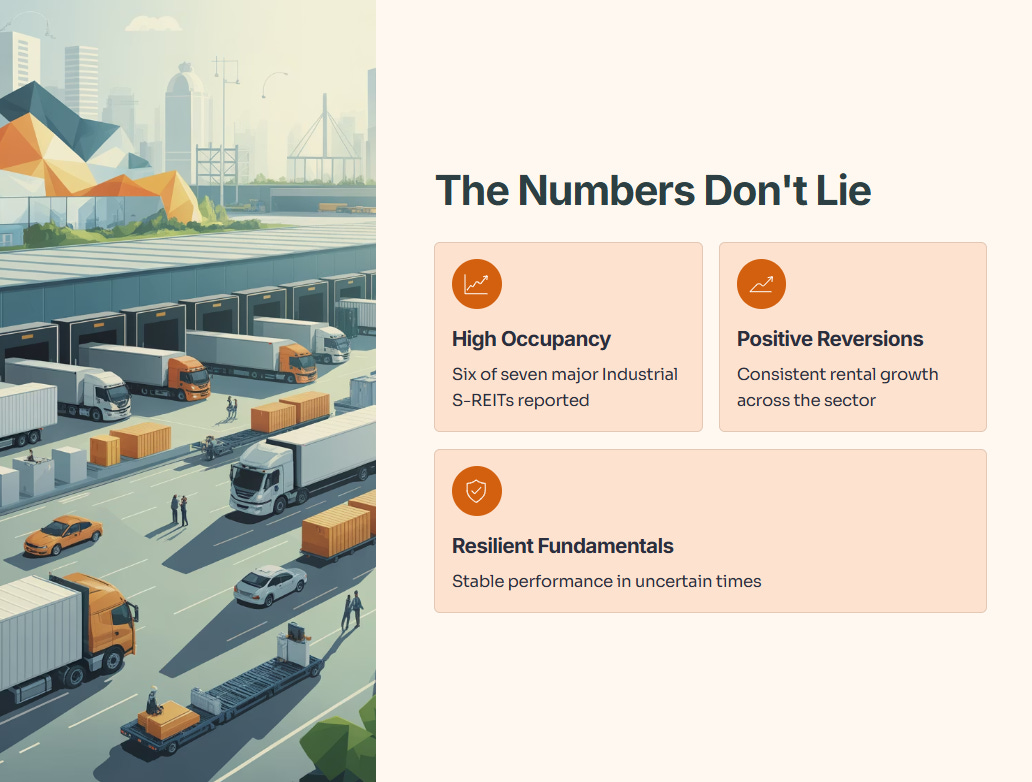

📊 The Numbers Don’t Lie: Industrial S-REITs Delivered

Six of the seven major Industrial S-REITs have reported their latest updates, and the story is remarkably consistent: high occupancy, positive rental reversions, and resilient fundamentals.

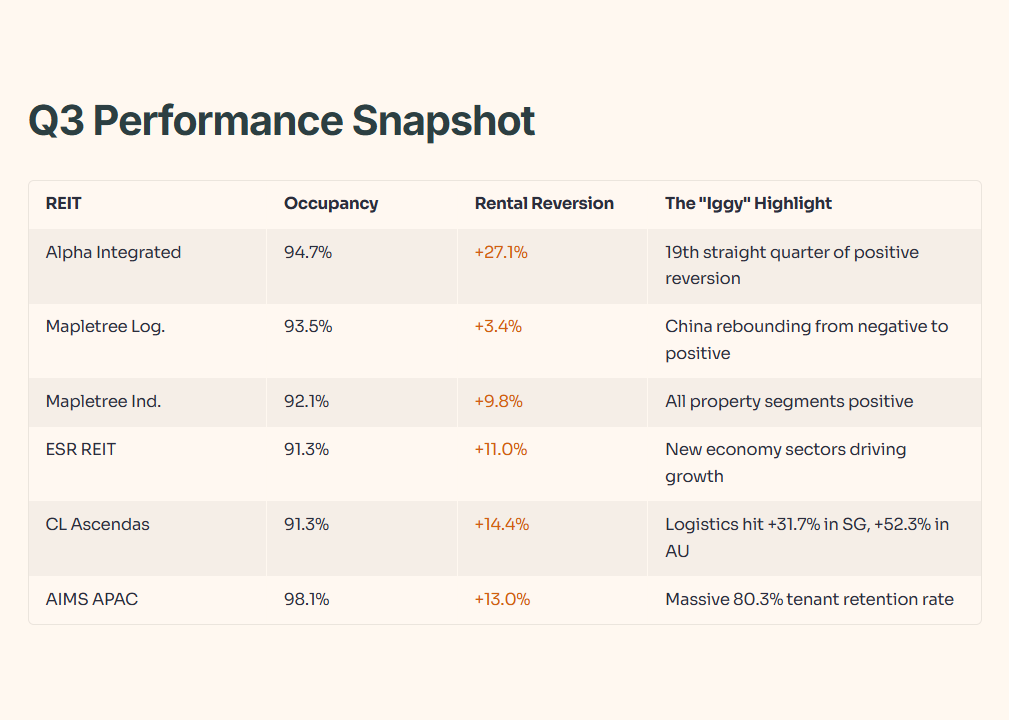

Here is the snapshot of how the sector performed in the latest quarter:

The 3 Key Takeaways (Deep Dive)

The table gives you the data, but here is the story behind the numbers.

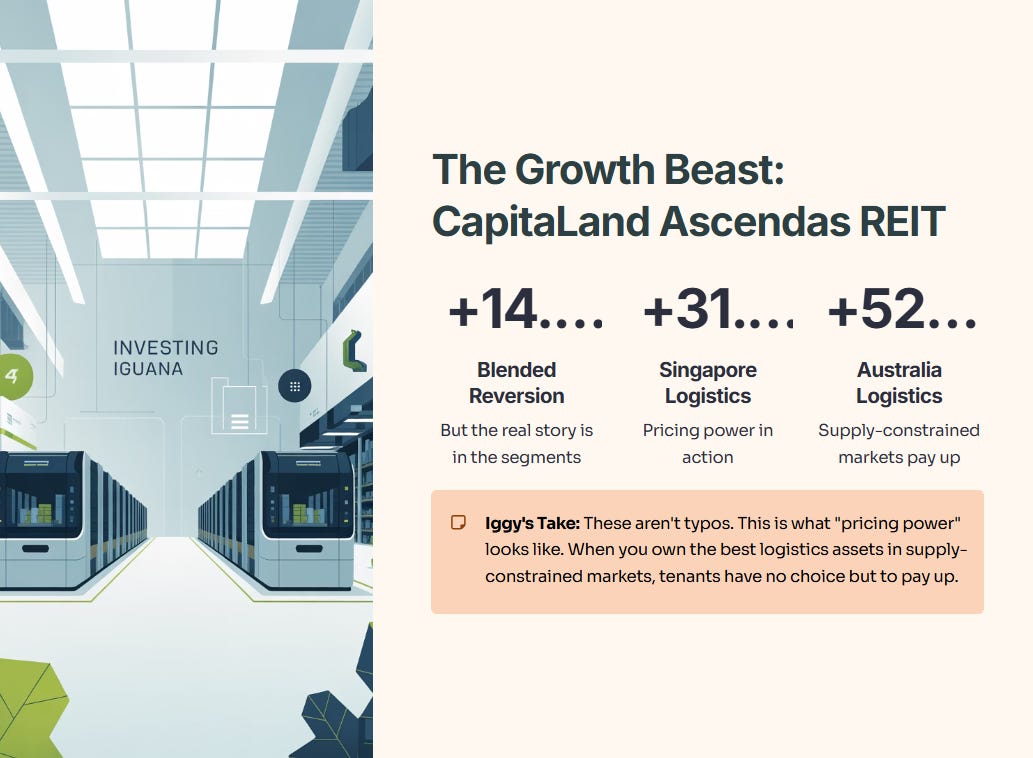

1. The “Growth Beast”: CapitaLand Ascendas REIT (CLAR)

CLAR achieved a blended +14.4% rental reversion, but the headline number hides the real story. Look at the specific segments:

Singapore Logistics: +31.7%

Australia Logistics: +52.3%

Iggy’s Take: These aren’t typos. This is what “pricing power” looks like. When you own the best logistics assets in supply-constrained markets, tenants have no choice but to pay up. CLAR is proving that size and quality act as a massive inflation shield.

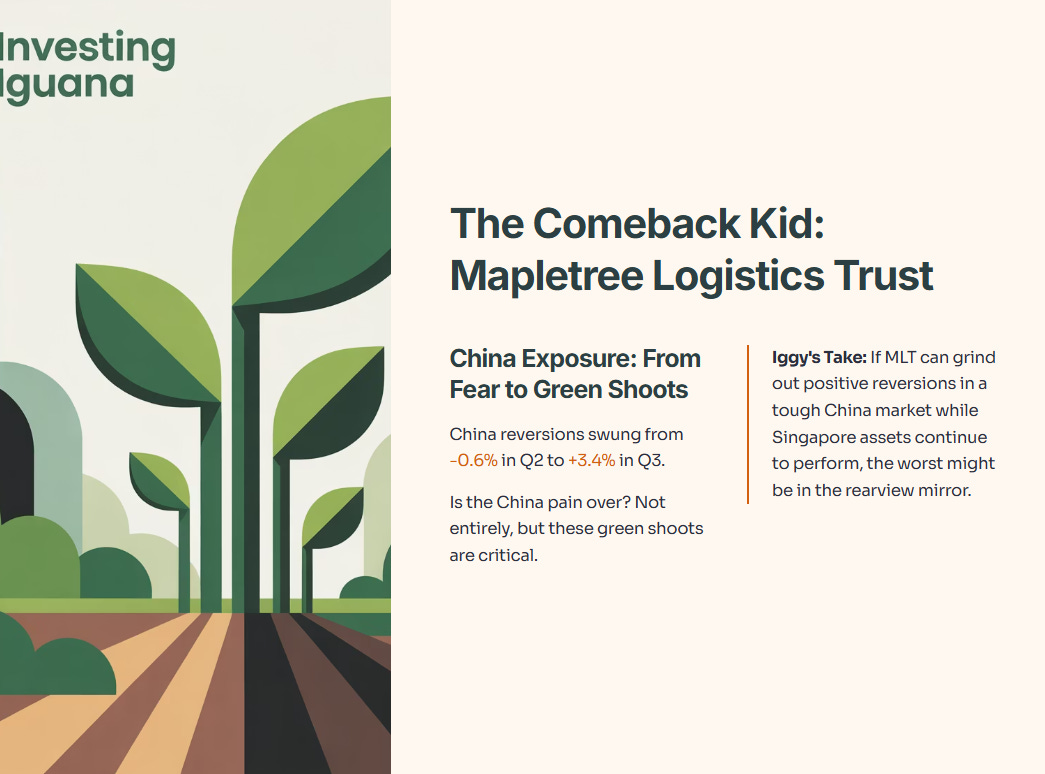

2. The “Comeback Kid”: Mapletree Logistics Trust (MLT)

For the last year, everyone has been terrified of MLT’s exposure to China. But look at the data: Reversions in China swung from -0.6% in Q2 to +3.4% in Q3.

Iggy’s Take: Is the China pain over? Not entirely, but these “green shoots” are critical. If MLT can grind out positive reversions in a tough China market while its Singapore assets continue to perform, the worst might be in the rearview mirror.

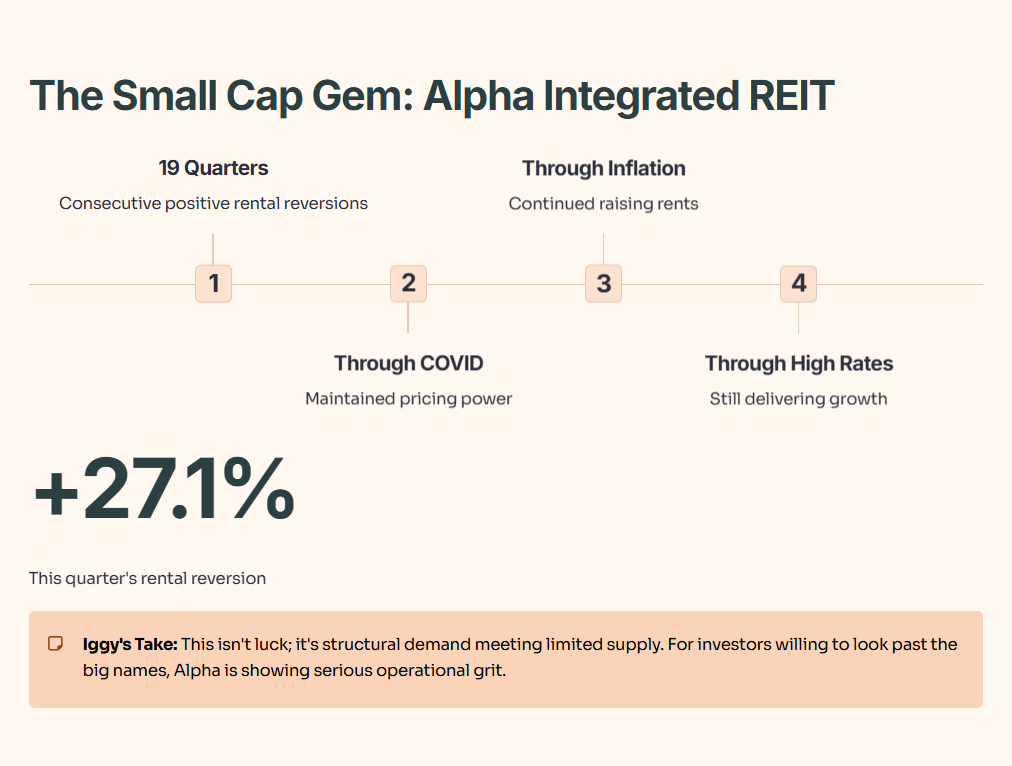

3. The “Small Cap Gem”: Alpha Integrated REIT

Formerly known as Sabana, this REIT just logged its 19th consecutive quarter of positive rental reversions (+27.1% this quarter!).

Iggy’s Take: Think about that consistency. Through Covid, through inflation, and through high interest rates, they have raised rents for nearly five years straight. This isn’t luck; it’s structural demand meeting limited supply. For investors willing to look past the big names, Alpha is showing serious operational grit.

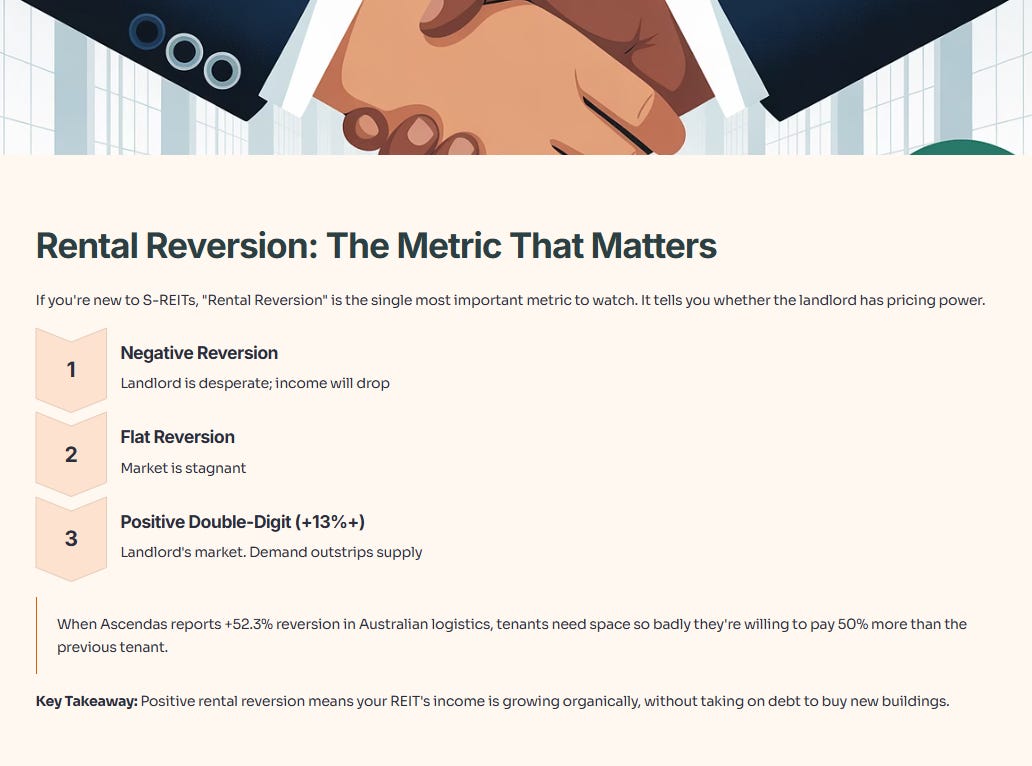

Rental Reversion: The Metric That Matters

If you are new to S-REITs, “Rental Reversion” is the single most important metric to watch. It tells you whether the landlord has pricing power.

Negative Reversion: The landlord is desperate; income will drop.

Flat Reversion: The market is stagnant.

Positive Double-Digit (+13%+): This is a landlord’s market. Demand is outstripping supply.

When Ascendas reports +52.3% reversion in Australian logistics, it means tenants need space so badly they are willing to pay 50% more than the previous tenant. That is what happens when e-commerce growth meets limited warehouse supply.

Key Takeaway: Positive rental reversion means your REIT’s income is growing organically, without the REIT needing to take on debt to buy new buildings. It means the business model is working.

🛡️ Why Industrial is the “Defensive” Play

Let’s compare Industrial S-REITs to their cousins in Office and Retail to see why “boring” beats “exciting” right now.

Office REITs are in trouble. US office occupancy plunged to 83.5% in 2024. The structural shift to hybrid work is not reversing.

Retail REITs are exposed. They rely on consumer spending, which is weakening as inflation bites.

Industrial REITs are essential. They benefit from e-commerce (which requires 3x the warehouse space of brick-and-mortar), supply chain resilience, and manufacturing.

The Bottom Line: You can delay buying a new laptop (Retail). You can work from your living room (Office). But you cannot delay storing food or shipping medicine. Industrial space is not discretionary; it is the backbone of the economy.

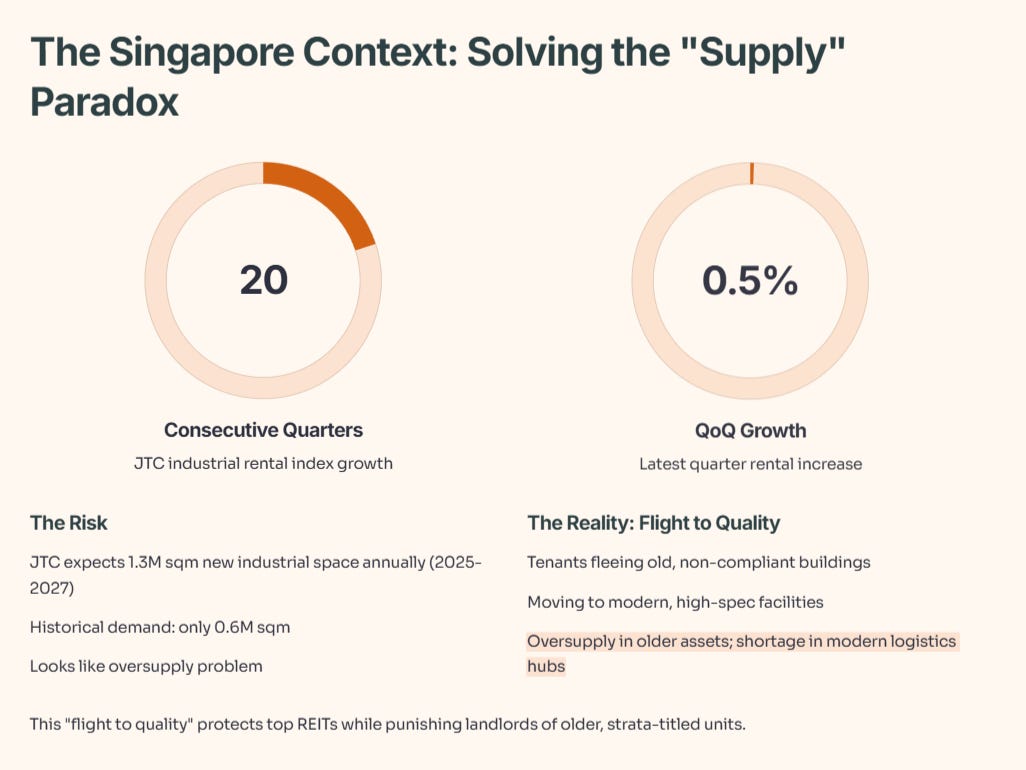

The Singapore Context: Solving the “Supply” Paradox

The broader Singapore industrial property market is showing sustained resilience. JTC data shows the industrial rental index rose 0.5% QoQ, marking the 20th consecutive quarter of rental growth.

The Risk: JTC expects 1.3 million sqm of new industrial space annually from 2025-2027. Historically, demand is only about 0.6 million sqm. On paper, this looks like an oversupply problem.

The Reality (Flight to Quality): So why are rents still rising? Because not all square footage is created equal.

Tenants are fleeing old, non-compliant buildings on the urban fringe and moving into modern, high-spec facilities with better connectivity (like the Punggol Digital District). The “oversupply” is largely in older assets, while the modern logistics hubs—where our top REITs operate—are seeing a shortage of space. This “flight to quality” protects the big REITs while punishing the landlords of older, strata-titled units.

💡 Iggy’s Take: Buy, Hold, or Sell?

Here is how I am positioning for the months ahead..