SGX (S68) 2.3% Yield vs 1.47% T-Bill Spread, SGX Digest — 10 April 2026

Don't let 'Adjusted Gearing' bluff you. Olam and CDL debt is real—refinancing math will eat your 2026 dividends alive.

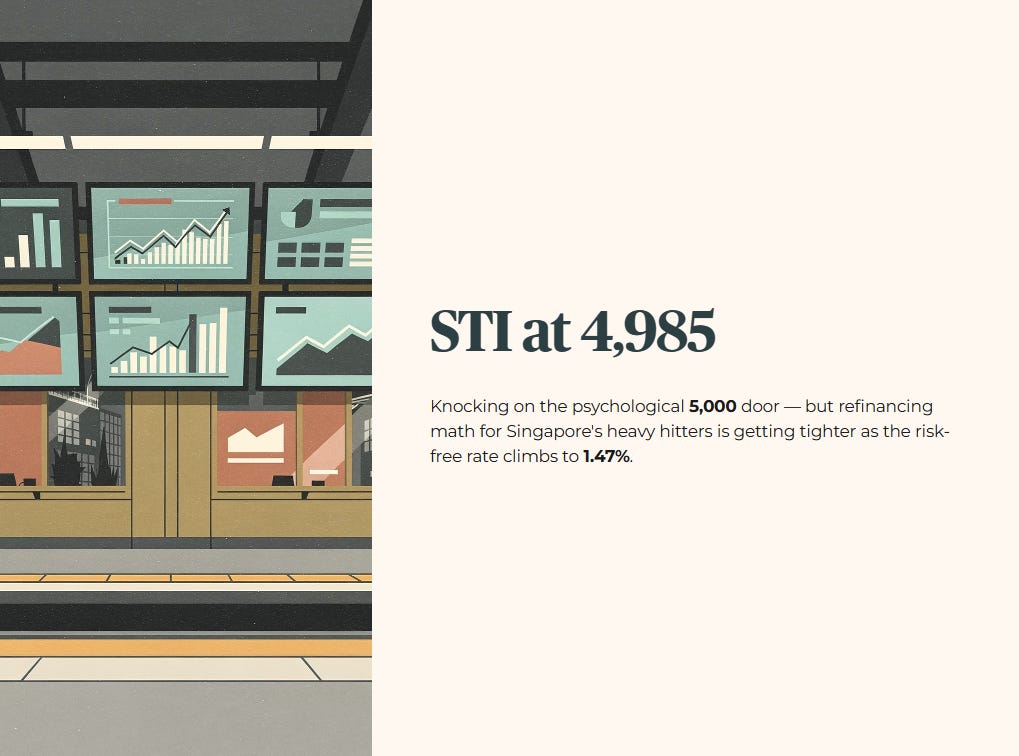

The STI closed near 4,985 yesterday, knocking on the psychological 5,000 door. Under the hood, however, the refinancing math for Singapore’s heavy hitters is getting tighter as the risk-free rate climbs to 1.47%.

In This Article:

Market Snapshot

The Audit City Developments C09 Gearing Alert

The Audit Singapore Exchange S68 Yield Trap Alert

The Audit Olam Group VC2 Gearing Alert

Analyst Chatter

Watchlist and Yield Spread

Iggys Take The Bottom Line

Disclaimer

About Iggy & the Elite Investors

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

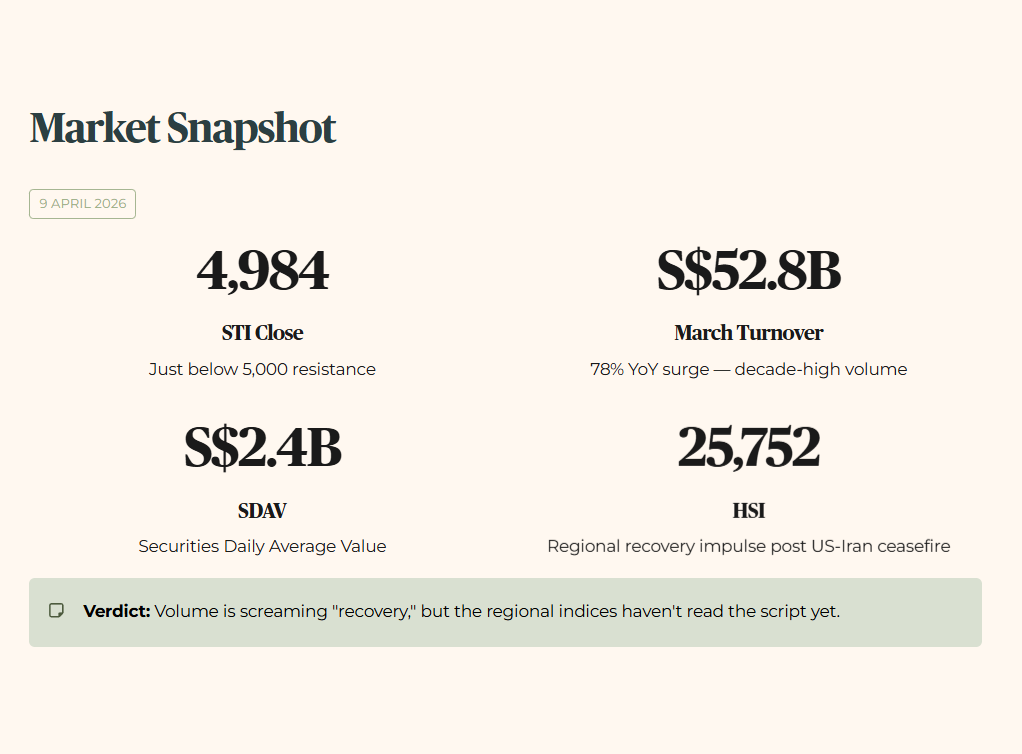

Market Snapshot

Verdict: Volume is screaming “recovery,” but the regional indices haven’t read the script yet.

The STI closed at 4,984.60 on 9 April, holding just below the 5,000 resistance level. Regional context is mixed: HSI confirmed at 25,752, while the SET and JCI are showing a region-wide recovery impulse following the US-Iran ceasefire rebound, though exact 9 April closes are pending final confirmation.

SGX March 2026 total turnover hit S$52.8 billion, a 78% YoY surge, with SDAV at S$2.4 billion. Trading volume is at a decade-high, but the indices are not keeping pace. Regional volatility remains the watchword.

The Audit

1. City Developments (C09): Gearing Alert

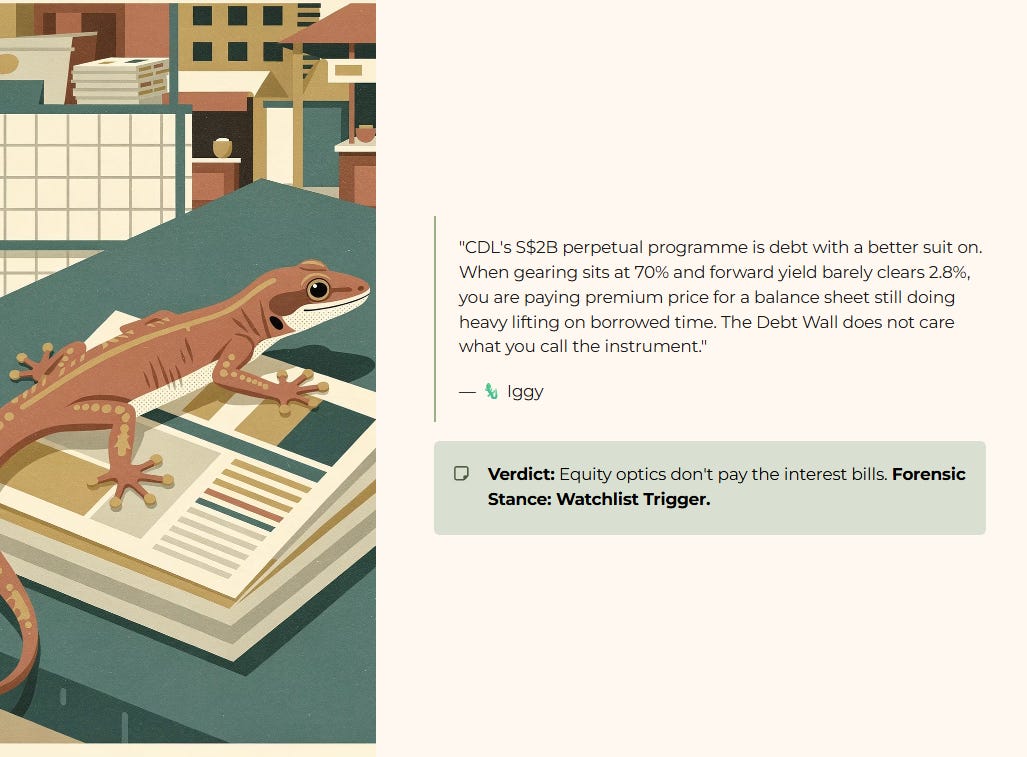

Verdict: A S$2 billion safety net made of paper won’t stop the gearing gravity.

Five-Layer Audit:

Layer 1: Raw Fact. CDL has launched a S$2 billion multicurrency perpetual securities programme for refinancing existing debt and working capital.

Layer 2: Benchmark. Net gearing of 70% is exactly double the Iggy 35% safety ceiling, sitting well above CDL’s own historical 60% comfort zone.

Layer 3: Peer Context. CapitaLand Investment continues to move toward an asset-light model with lower balance sheet intensity. CDL remains heavy on landbank and debt.

Layer 4: Forward Scenario. A 10% spike in interest costs on this S$2 billion pile would likely crush the ICR toward the 3.0x danger zone. Macro trigger: SORA volatility.

Layer 5: Wallet Impact. Location: Bedok. A 45-year-old HDB owner supplementing salary with dividends faces the MRT Door Paradox. The growth looks fast from the outside, but you are getting squeezed inside. Perpetual coupons must be paid before your common dividends. Forensic Stance: Watchlist Trigger.

🦎Iggy’s Take: “CDL’s S$2 billion perpetual programme is being sold as financial engineering. I call it debt with a better suit on. When your gearing sits at 70% and your forward yield barely clears 2.8%, you are paying premium price for a balance sheet that is still doing heavy lifting on borrowed time. The Debt Wall does not care what you call the instrument. My monitoring threshold has not been crossed for accumulation — it has been crossed as a caution flag.”

Verdict: Equity optics don’t pay the interest bills.

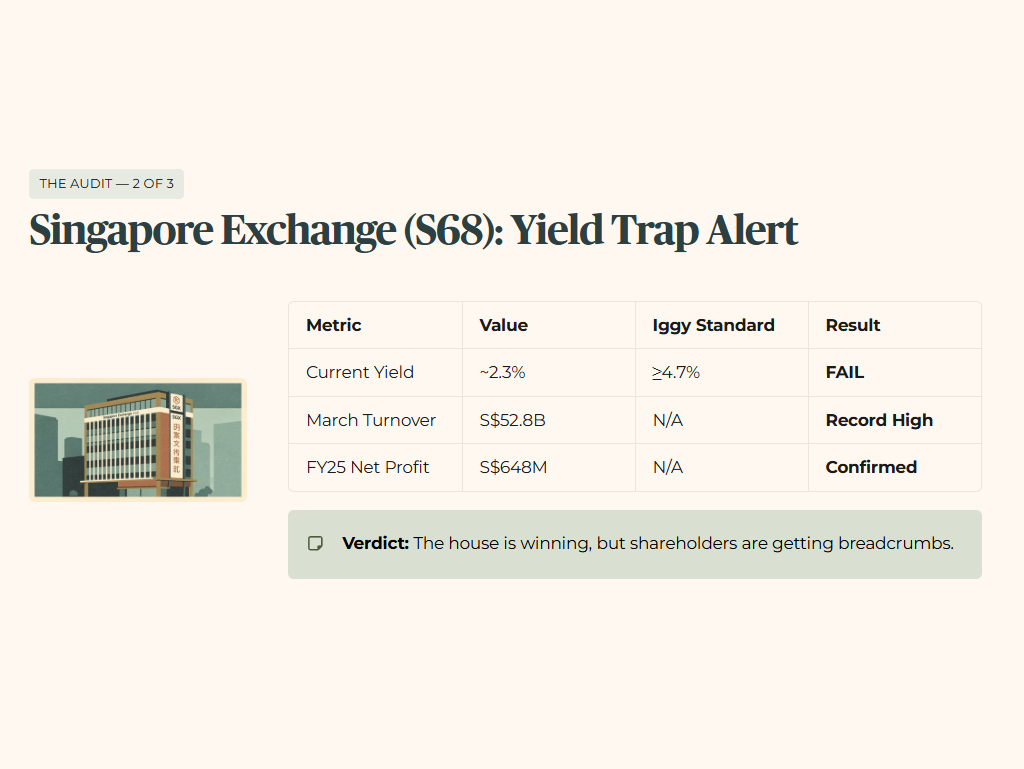

2. Singapore Exchange (S68): Yield Trap Alert

Verdict: The house is winning, but the shareholders are getting breadcrumbs.

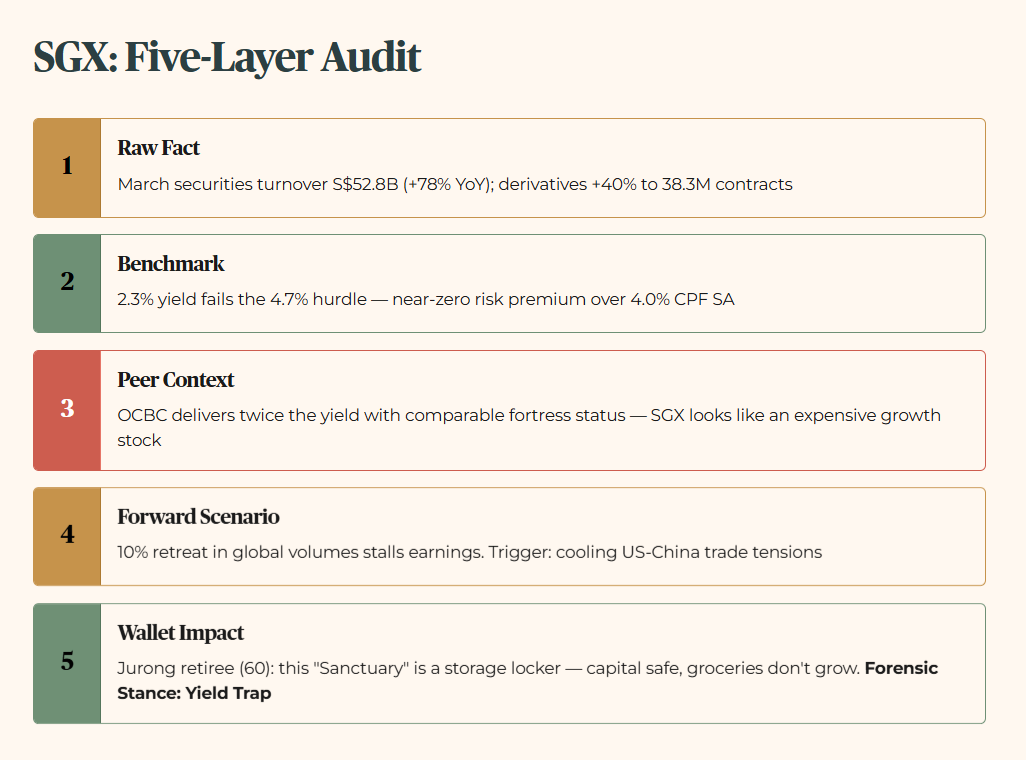

Five-Layer Audit:

Layer 1: Raw Fact. March securities turnover hit S$52.8 billion, a 78% YoY jump, while derivatives volume surged 40% to 38.3 million contracts.

Layer 2: Benchmark. A 2.3% yield is a flat-out failure against the 4.7% Iggy hurdle and offers almost zero risk premium over the 4.0% CPF SA benchmark.

Layer 3: Peer Context. Local banks like OCBC are providing twice the yield with comparable fortress status, making SGX look like a very expensive growth stock.

Layer 4: Forward Scenario. A 10% retreat in global trading volumes would stall the current earnings momentum, leaving that 2.3% yield as the only support. Macro trigger: cooling US-China trade tensions reducing hedging demand.

Layer 5: Wallet Impact. Location: Jurong. A 60-year-old retiree managing SRS drawdown finds this “Sanctuary” is actually a storage locker. It keeps the capital safe, but it does not grow the groceries. Forensic Stance: Yield Trap.

🦎Iggy’s Take: “SGX is one of Singapore’s most respected institutions, and that reputation is exactly what makes it a yield trap for the income investor who is not paying attention. A 2.3% yield against a 4.0% CPF SA benchmark means you are taking on equity volatility for a return that does not even beat your savings floor. The March volume surge is real and impressive. But volume is the exchange’s income, not yours. Track it. Do not anchor to it.”

Verdict: Growth is the story, but the income is a footnote.