Seatrium: 3 Good & 3 Red Flags At 1.24% Yield

A S$100,000 SRS position earns S$1,240 a year while 0.4x gearing and 7.4% margins carry integration risk that CPF SA avoids

This stock carries a massive S$17.8 billion order book and a microscopic 1.28% dividend yield. If you are deploying SRS funds into this turnaround narrative, your capital is absorbing immense engineering risk for a fraction of the guaranteed CPF baseline. This forensic audit dissects the underlying balance sheet to reveal whether the series-build margins justify holding this equity, or if it remains a yield trap masquerading as a growth play.

In This Article:

The Financial Snapshot

Dividend Trajectory

The 3 Good The Bull Case

The 3 Red Flags The Bear Case

Peer Comparison

The Singaporean Context The Stress Test

The Weighing Scale Forensic Synthesis

Outro and Disclaimer

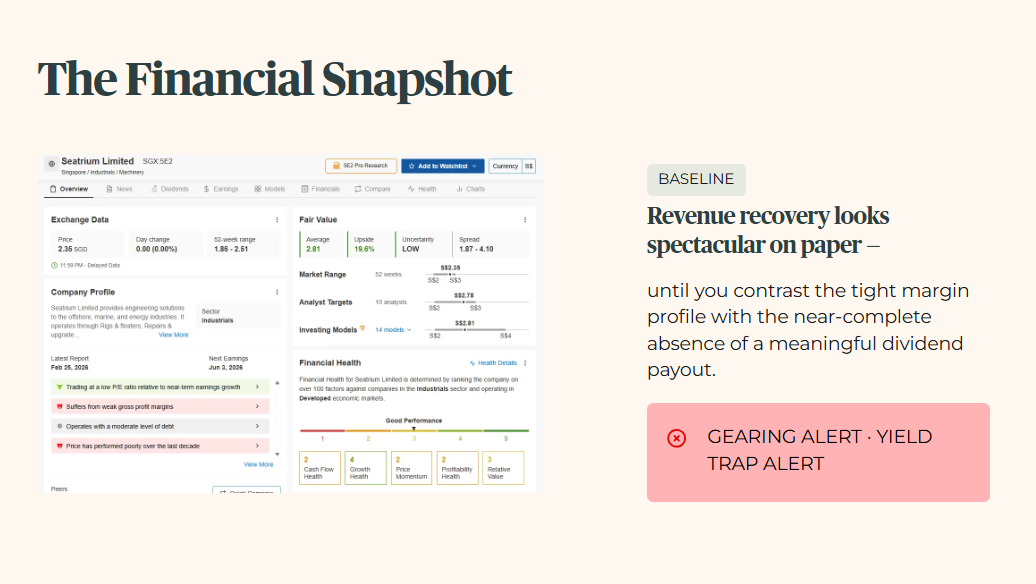

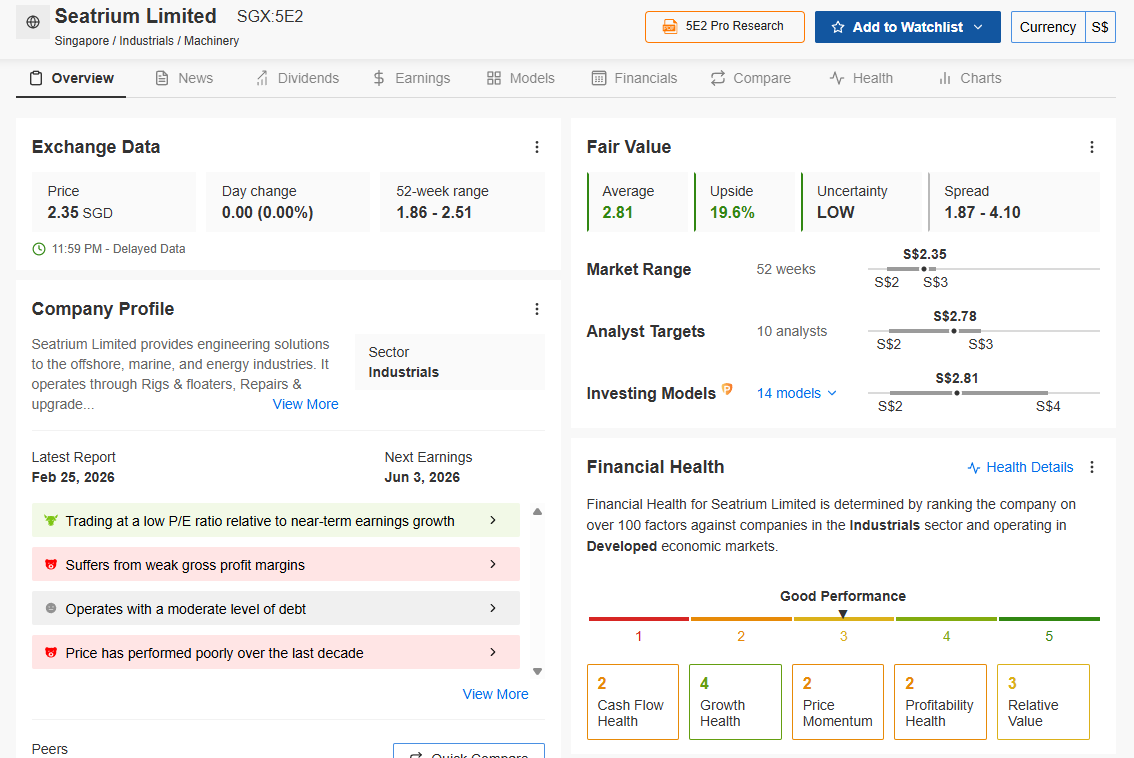

The Financial Snapshot (The Baseline)

GEARING ALERT YIELD TRAP ALERT

“I don’t just guess at valuations. I check the institutional models.” Source: InvestingPro Data. Unlock these institutional tools for your own portfolio: Use code INVESTINGIGUANA for an exclusive 50% Discount.

🏛️ [Claim Your 50% Discount Here]

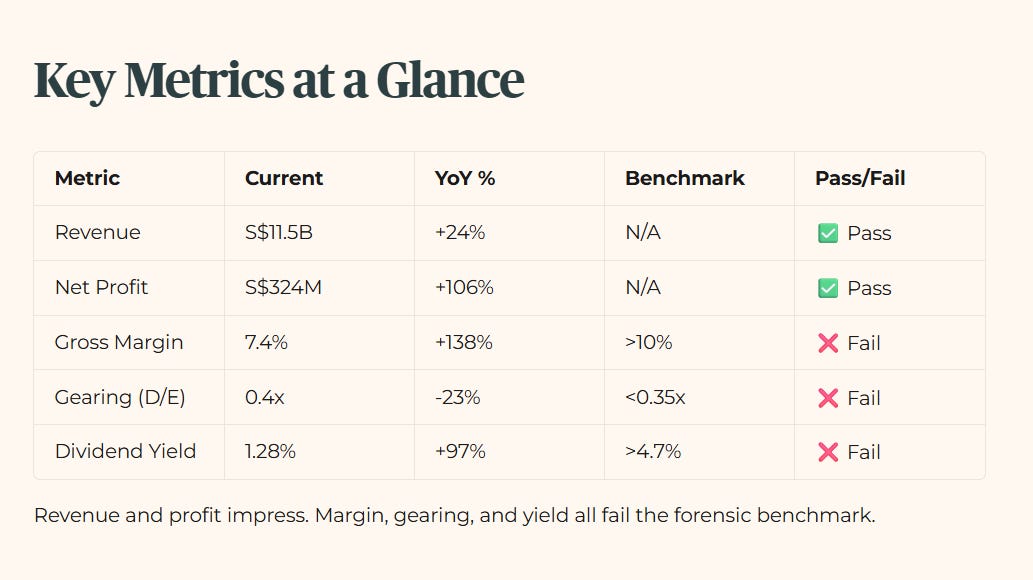

The topline revenue recovery looks spectacular on paper until you contrast the tight margin profile with the near-complete absence of a meaningful dividend payout.

Seatrium delivered revenue of S$11.5 billion, a solid increase from S$9.2 billion in the prior period, representing +24% year-on-year growth. Net profit tells a similar story, hitting S$324 million from S$157 million — a +106% jump. Then the forensic reality bites back. Gross margin sits at a tight 7.4%, up from 3.1%, a +138% improvement that still fails the greater than 10% sector benchmark. Gearing stands at 0.4x, down from 0.52x, but it still fails the less than 0.35x ceiling. The dividend yield of 1.28% is a genuine improvement from the near-zero payouts of the merger years, but it remains an absolute failure against the 4.7% minimum hurdle.

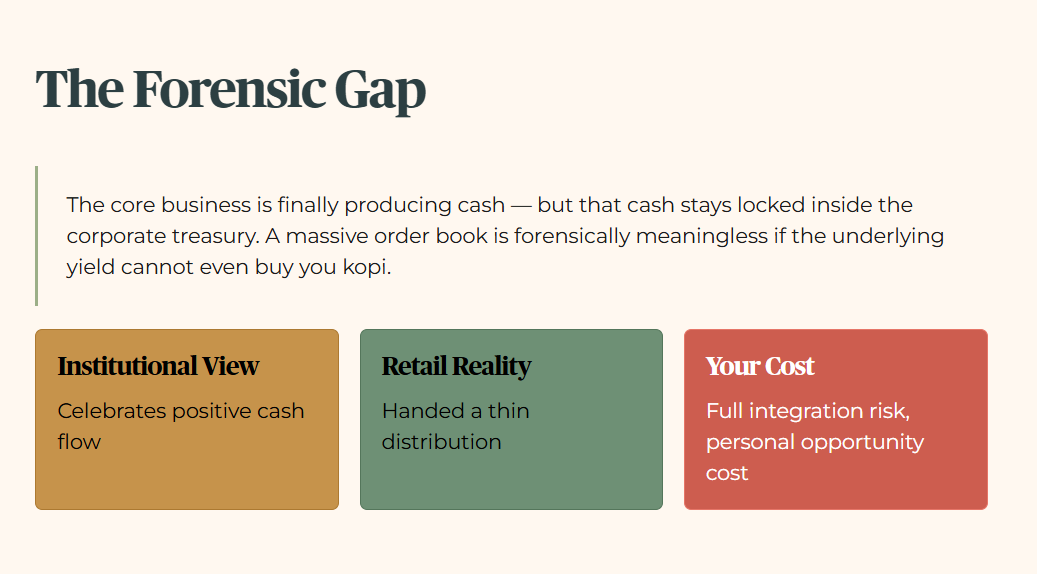

Iggy’s Insight Box 1: The Forensic Gap The market is pricing Seatrium based on a multi-billion dollar pipeline, but the current financials reveal a painful gap between expectations and reality. Institutional money celebrates positive cash flow, while retail investors are handed a thin distribution. Management is retaining capital to build an empire, ensuring that shareholders bear the full brunt of integration risks. You are funding their operational turnaround strictly with your personal opportunity cost. The core business is finally producing cash, but that cash stays largely locked inside the corporate treasury. A massive order book is forensically meaningless if the underlying yield cannot even buy you kopi.

Dividend Trajectory

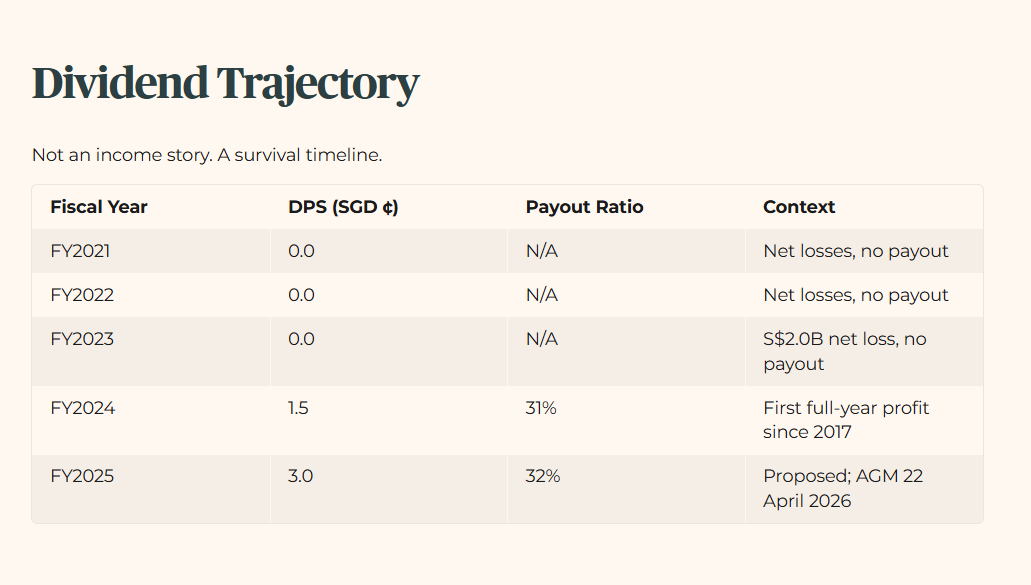

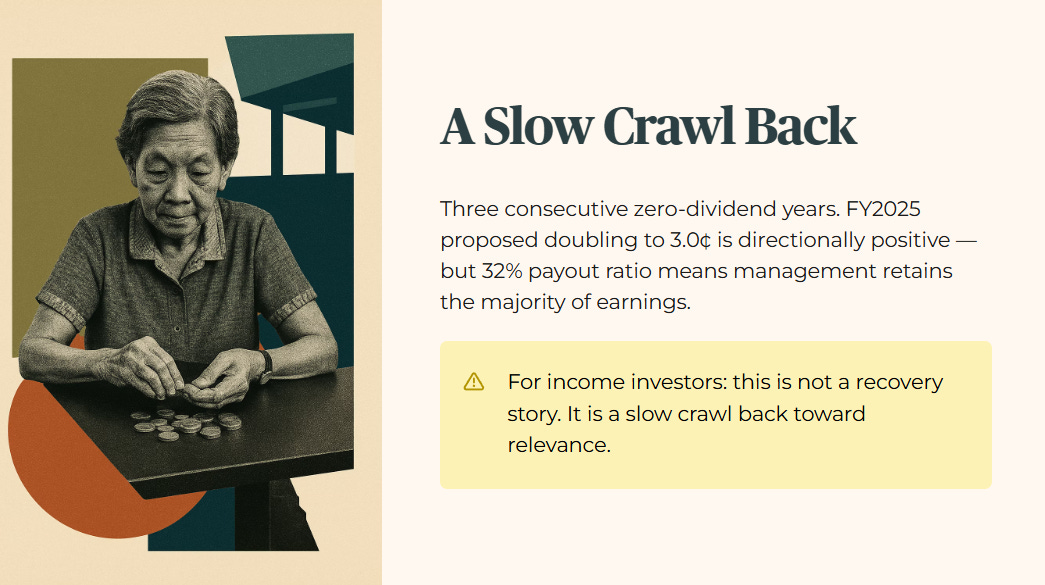

The dividend history here is not a story of income investing. It is a survival timeline.

Three consecutive zero-dividend years. The FY2024 resumption at 1.5 cents was the first payout since 2018. The FY2025 proposed doubling to 3.0 cents is directionally positive, but the payout ratio of approximately 32% reveals that management is still choosing to retain the majority of earnings inside the balance sheet. For an income investor, this trajectory is not a recovery story. It is a slow crawl back toward relevance.

The 3 Good (The Bull Case)

Good 1: The S$17.8 Billion Revenue Visibility

We begin with the primary defense of the valuation. Seatrium holds a S$17.8 billion net order book securing operations through 2033. This is a verifiable fact drawn directly from their latest corporate filings. When we apply our benchmark, this figure dramatically surpasses the 3 to 5 year historical average order book size for the previously separate entities. They have successfully aggregated global demand into a single pipeline.

In peer context, ST Engineering operates with a massive S$28 billion order book and passes the visibility test easily. Seatrium has now clawed its way into that same elite tier of institutional revenue certainty. They are no longer scrambling for quarterly survival. Stress-test a forward scenario: if global oil macro conditions see a +10% lift in the next twelve months, deepwater projects will accelerate. Seatrium will convert its pipeline faster, driving margins higher.

The wallet impact for the 55-year-old investor taking a pure capital appreciation stance is a pathway to greater than 15% total shareholder return, definitively beating the CPF SA floor through price action alone. Revenue certainty is the bedrock of the bullish argument. Without this backlog, the company would collapse under its own weight.

This bull case only holds if the S$32 billion forward pipeline converts at a rate of at least S$5 billion annually over the next 24 months.

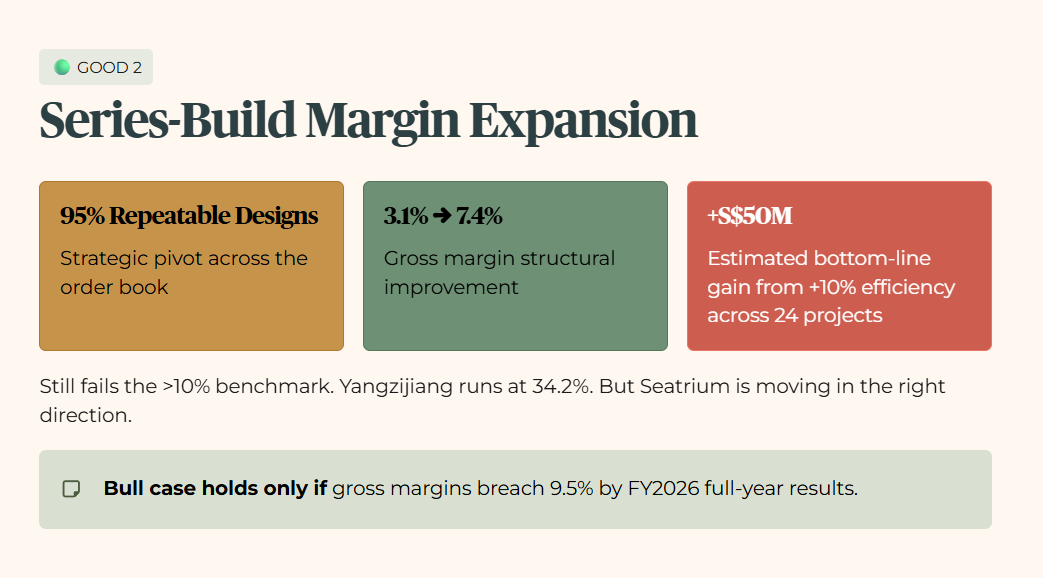

Good 2: The Series-Build Margin Expansion

The operational shift at the shipyards is highly significant. Seatrium now uses repeatable designs for 95% of its massive order book. This strategic pivot pushed gross margin from 3.1% to 7.4%. Against our benchmark, this is a massive structural improvement, but it still sits below the greater than 10% historical sponsor norms seen before the offshore industry crash.

In peer context, Yangzijiang Shipbuilding operates at a 34.2% gross margin in FY2025. Yangzijiang passes the efficiency threshold. Seatrium fails it. But Seatrium is moving in the right direction. A +10% operational efficiency gain across their current 24 projects adds an estimated S$50 million directly to the bottom line, with zero additional capital expenditure required.

The macro trigger here is the stabilisation of global steel prices. The wallet impact is a tangible share price rerate toward consensus targets. You are betting that the engineers can stop making expensive mistakes. The series-build model prevents bespoke errors from destroying project profitability. It is a factory line for the ocean.

This bull case only holds if gross margins breach 9.5% by the FY2026 full-year earnings report.

Good 3: Fortress Interest Coverage Resilience

The corporate balance sheet contains one undeniable bright spot. The interest coverage ratio stands at 8.7x. By our benchmark, this cleanly beats the 4.0x Iggy Fortress Balance Sheet threshold and completely eclipses the negative averages of its predecessor entities.

In peer context, ST Engineering operates at 5.7x ICR with a stable but debt-heavy balance sheet. Seatrium’s 8.7x offers superior debt servicing headroom. Stress-test a +10% spike in global borrowing costs. Even in that severe environment, the 8.7x buffer ensures zero threat to core operations. The wallet impact is purely defensive. The equity portfolio investor is protected from sudden emergency rights issues. Your capital base is preserved from massive, unexpected dilution. This resilience buys management the time to execute their turnaround without facing a liquidity crisis.

This bull case only holds if the interest coverage ratio remains strictly above 6.0x during the upcoming multicurrency debt issuance.

The 3 Red Flags (The Bear Case)

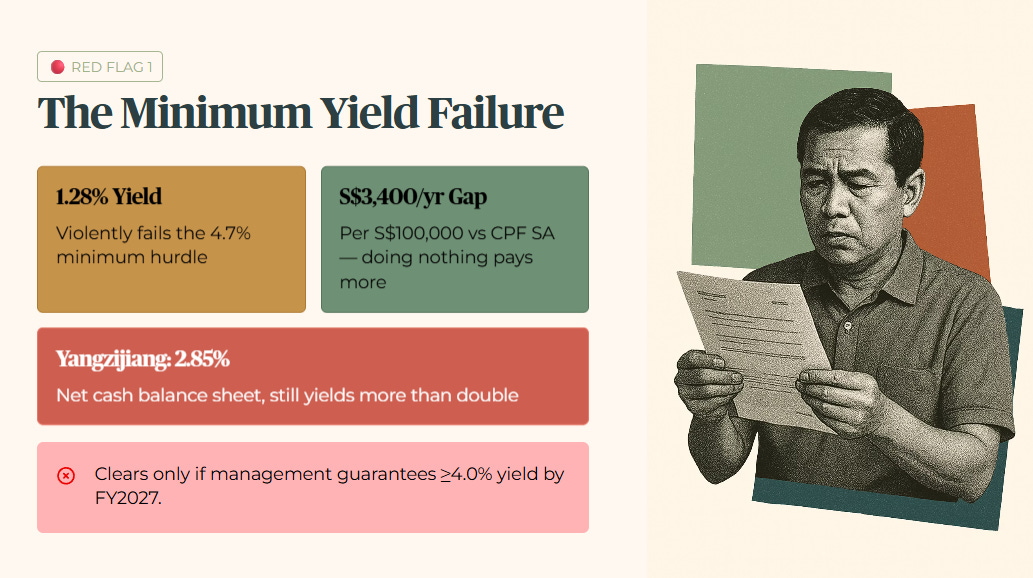

Red Flag 1: The Minimum Yield Failure

We must aggressively confront the primary failure. The forward dividend yield sits at 1.28% based on the proposed 3.0 cents FY2025 DPS against the current share price of S$2.35. This raw fact is mathematically hostile to any income-seeking investor. Apply the benchmark: it violently fails our 4.7% minimum yield hurdle. Shift to peer context.

Yangzijiang Shipbuilding currently yields 2.85% on a trailing basis, with a forward yield approaching 4.8% once the proposed FY2025 dividend is paid. Even Yangzijiang, which runs a net cash balance sheet with no interest expense burden, yields more than double what Seatrium offers today. You are taking severe maritime execution risk for less than a basic fixed deposit rate. Build the forward scenario. The stock must appreciate by over 3% annually just to match the CPF SA baseline.

The wallet impact is severe. For a S$100,000 deployment into Seatrium, you face a net yield gap of more than S$3,400 per year compared to doing absolutely nothing inside CPF SA. The 65-year-old retiree simply cannot afford to subsidise this corporate transition. You cannot eat an order book, and you cannot pay medical bills with gross margin expansions.

This red flag clears only if management implements a dividend policy guaranteeing a minimum 4.0% yield by FY2027.

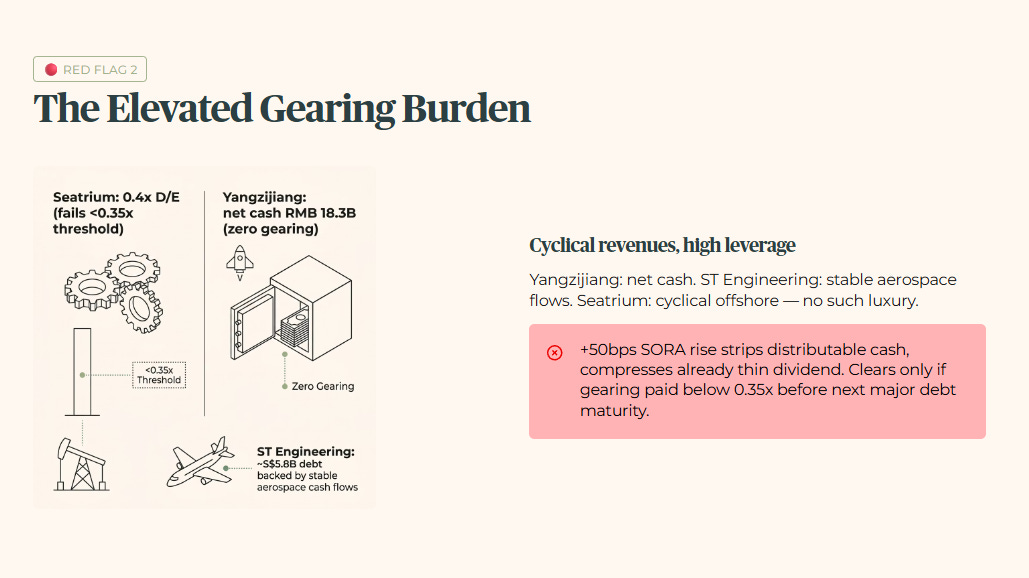

Red Flag 2: The Elevated Gearing Burden

The debt-to-equity ratio sits at 0.4x. By our benchmark, this breaches the strict 0.35x gearing ceiling required for a true Fortress Balance Sheet. They are carrying too much leverage for a notoriously low-margin business. In peer context, the contrast is stark. Yangzijiang carries a net cash position of RMB 18.3 billion. Zero net gearing. ST Engineering carries higher absolute debt at approximately S$5.8 billion, but defends it with highly stable aerospace and defence cash flows.

Seatrium’s highly cyclical offshore revenues do not afford them the same luxury. Look at the forward scenario. If SORA rises 50 basis points from its current level, the resulting interest expense strips away distributable cash and directly compresses the already thin dividend payout.

The wallet impact hurts deeply. The heartland retiree relying on payout stability sees their already minimal income stream erode further. A highly geared company in a volatile rate environment is a ticking time bomb for equity holders.

This red flag clears only if the gearing ratio is aggressively paid down below 0.35x before the next major debt maturity window.

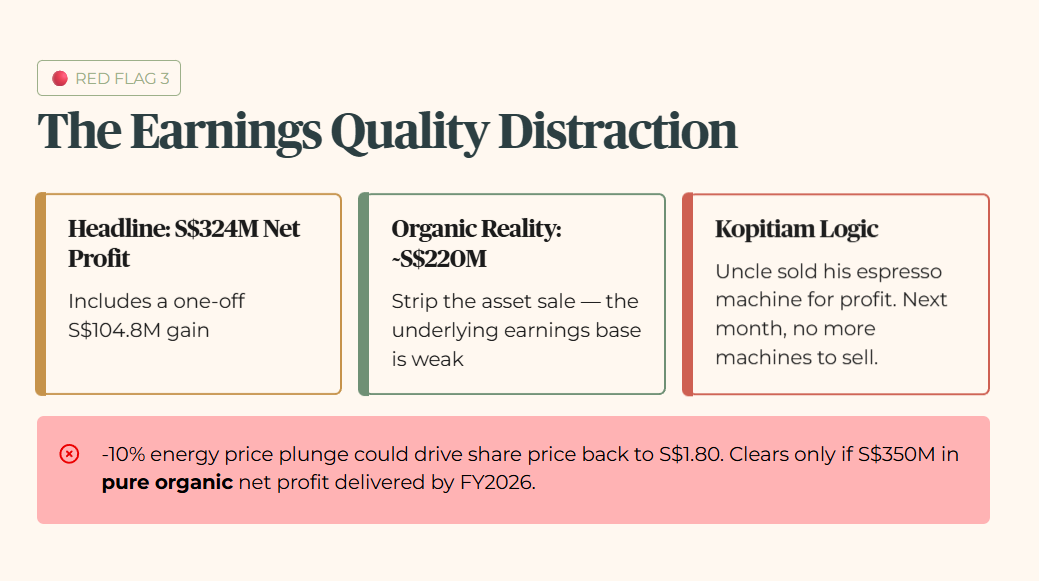

Red Flag 3: The Earnings Quality Distraction

The headline profit numbers tell a convenient lie. The S$324 million net profit was heavily inflated by a one-off S$104.8 million gain. Strip that out, and organic net profit falls to roughly S$220 million. Apply Kopitiam Logic: a drinks stall uncle claims he made a record profit this month. But when you check the ledger, he did not sell more coffee. He sold his second espresso machine for cash.

Next month, he has no more machines to sell. Seatrium is executing the exact same manoeuvre. In peer context, Yangzijiang’s record profit was driven purely by organic shipbuilding delivery at 34.2% gross margins. Yangzijiang passes the earnings quality test easily. Seatrium completely muddles it.

Under a forward scenario, a -10% plunge in global energy prices would rapidly expose the weak organic earnings base and could drive the share price straight back to the S$1.80 support level. The wallet impact is brutal. A retail investor entering at the current price faces meaningful per-share capital destruction.

This red flag clears only if Seatrium delivers S$350 million in pure, organic net profit without asset sale adjustments by FY2026.

And when you stack Seatrium’s 1.28% yield, 0.4x gearing, and 7.4% margin side by side against Yangzijiang, ST Engineering, and Sembcorp in the next table, the true scale of the risk–reward mismatch becomes painfully obvious