SGX 2023 - 2025 IPO Scorecard: -70% Crash vs +33% Gain (Revealed)

Real assets are back. Story stocks are dead. Here is the new mental model for Singaporean investors.

Many Singapore investors swore off IPOs after getting burned in 2023–2024. The disasters of 17LIVE and SAM Holdings left a mark on the collective wallet of the nation that is still healing.

But if you have been sitting on the sidelines in cash, you might have missed the quiet shift that happened in 2025. The market didn’t stop listing companies; it just changed what it rewards.

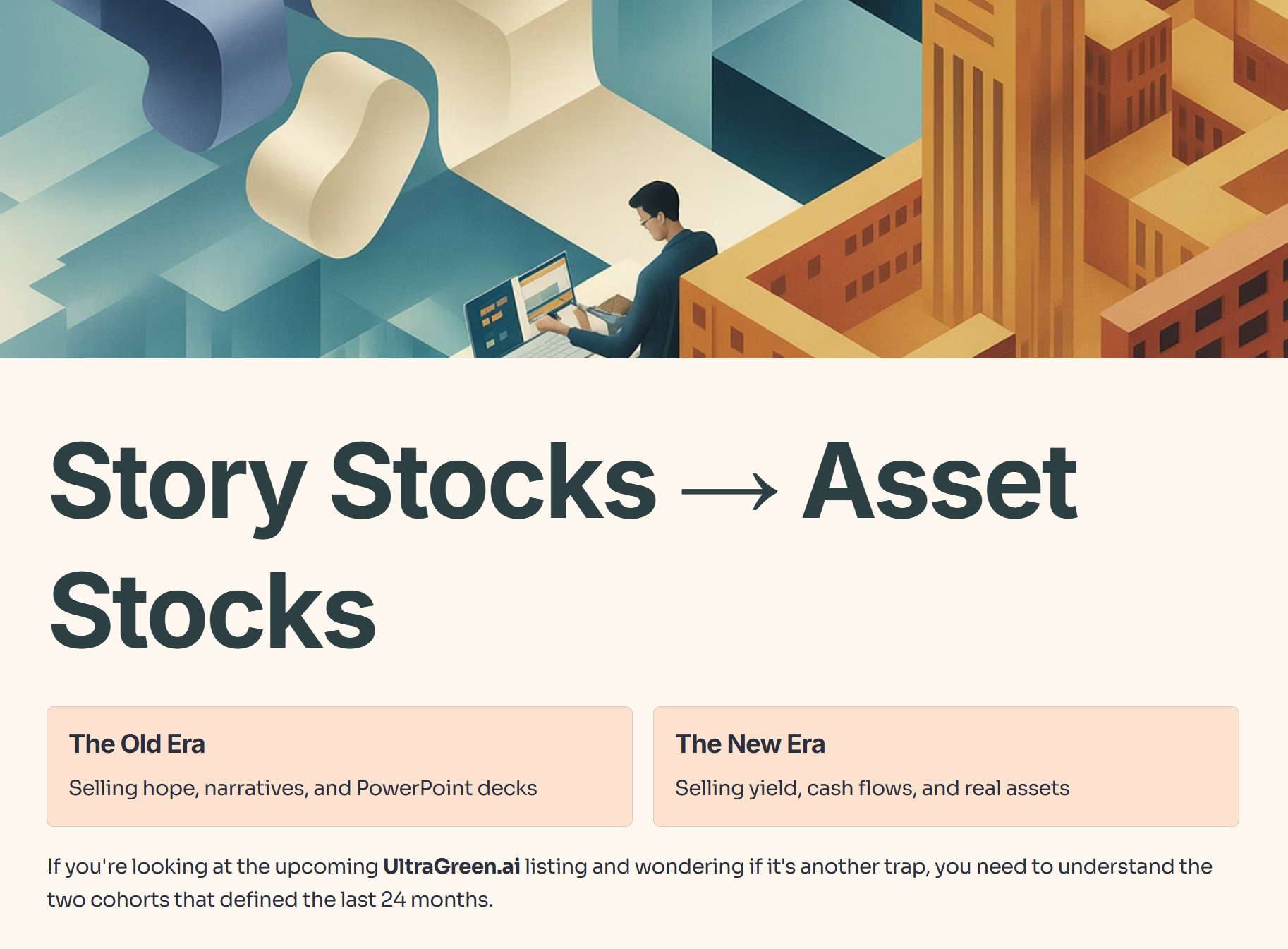

We have moved from an era of “Story Stocks” (selling hope) to “Asset Stocks” (selling yield).

If you are looking at the upcoming UltraGreen.ai listing and wondering if it’s another trap, you need to understand the two cohorts that defined the last 24 months.

• Phase 1: The Graveyard (The 2023/24 Winter)

• Iggy’s Insight: Why They Failed

• Phase 2: The Revival (The 2025 Spring)

• Iggy’s Insight: The “Boring” Premium

• The Upcoming Test: UltraGreen.ai

• Iggy’s Pre-IPO Filter

• Iggy’s Assessment & Portfolio Conclusion

• My final recommendation

Phase 1: The Graveyard (The 2023/24 Winter)

These companies sold narratives—Tech, Medical, Green Energy. They had great PowerPoint decks but weak cash flows.

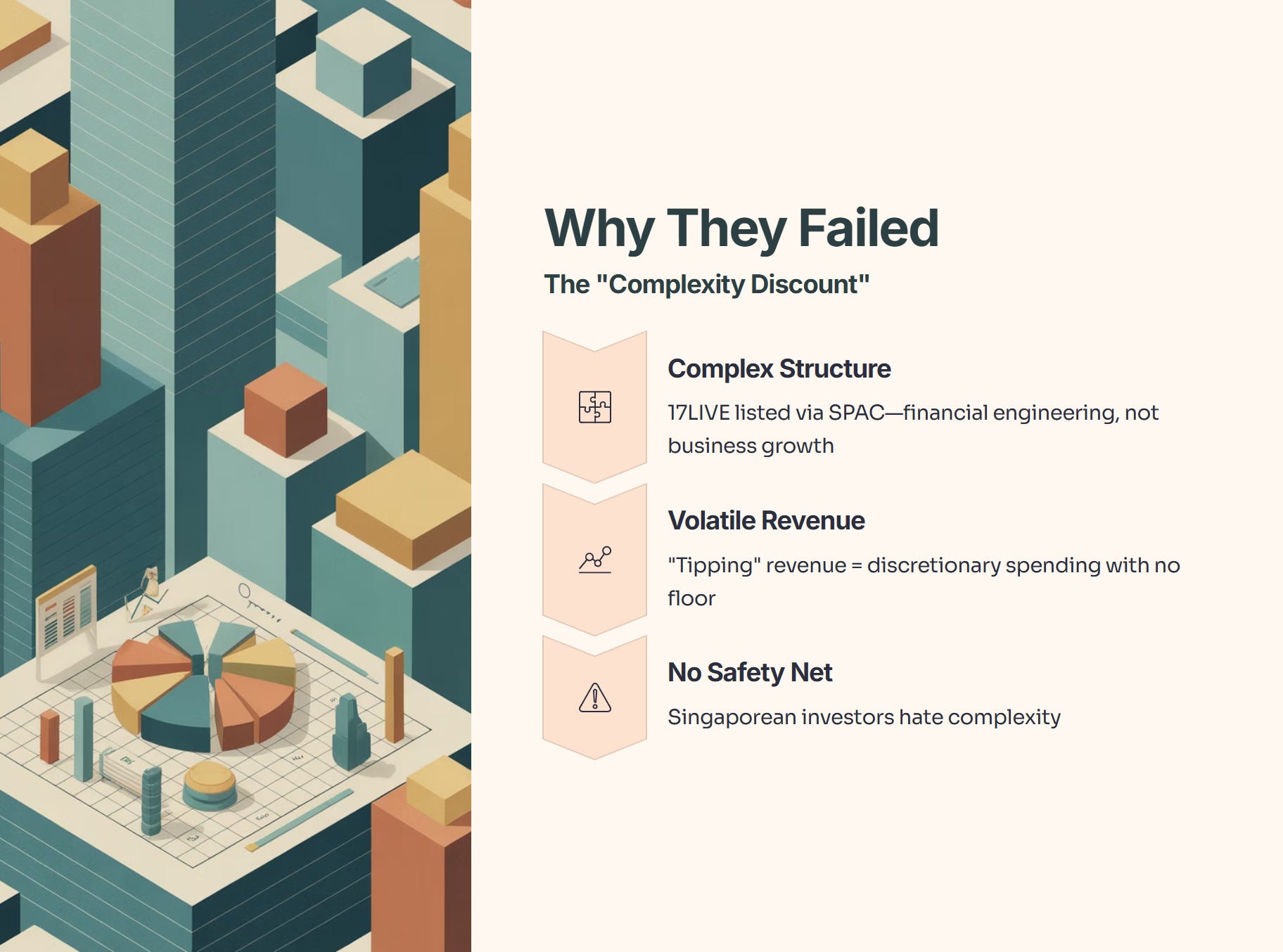

Iggy’s Insight: Why They Failed

The “Complexity Discount”

17LIVE didn’t fail just because of market conditions; it failed because Singaporean investors hate complexity. It listed via a SPAC (Special Purpose Acquisition Company)—a structure that screams “financial engineering” rather than “business growth.”

When you combine a complex structure with a business model that relies on volatile “tipping” revenue (which is essentially discretionary spending), you get a stock with no floor.

The Lesson: In Singapore, if you have to read the prospectus three times to understand how the company makes a dollar, do not buy it.

Note on Winking Studios: Why did they survive? Simple. They are a B2B service provider. They don’t rely on “hope”; they rely on contracts with giants like Ubisoft and Tencent. They sell shovels in a gold rush. That is a business model SGX understands.

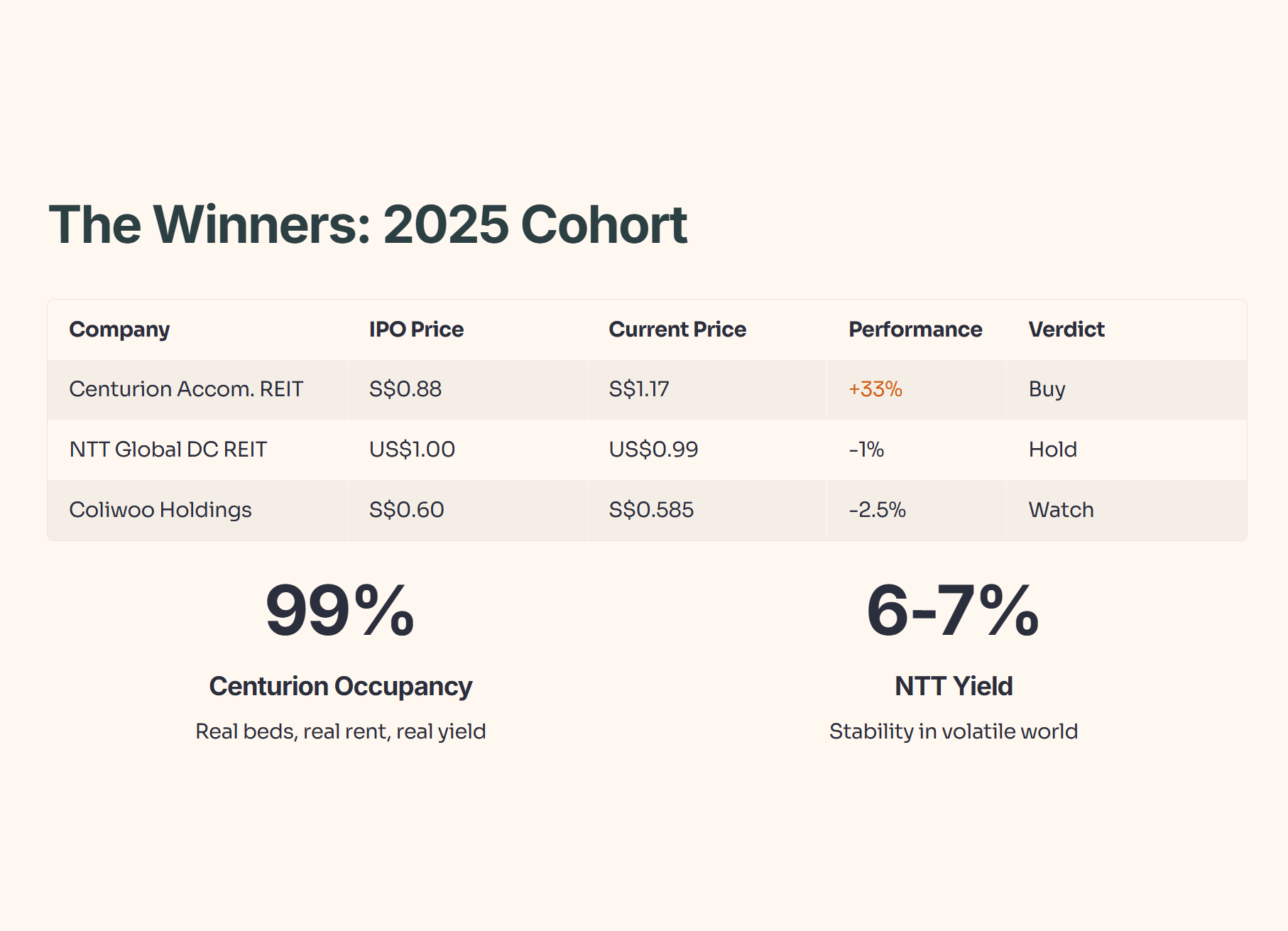

Phase 2: The Revival (The 2025 Spring)

The 2025 cohort is different. These companies aren’t trying to change the world; they are trying to pay rent. The market has rewarded them for it.

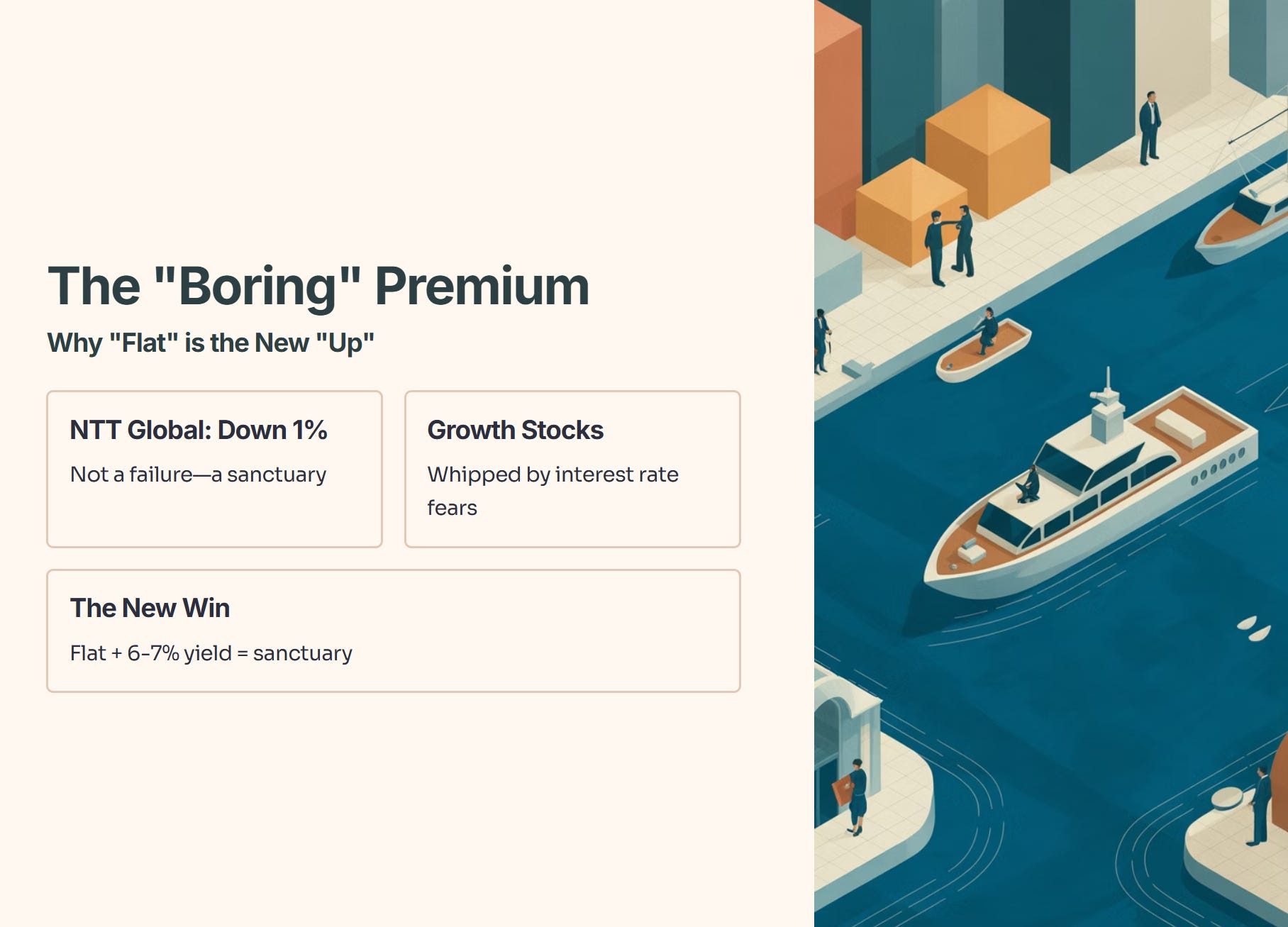

Iggy’s Insight: The “Boring” Premium

Why “Flat” is the New “Up”

Look at NTT Global Data Centers REIT. It’s down 1%. You might think that’s a failure. It’s not. In a year where growth stocks have been whipped around by interest rate fears, a stock that stays flat and pays you a 6-7% yield is a sanctuary.

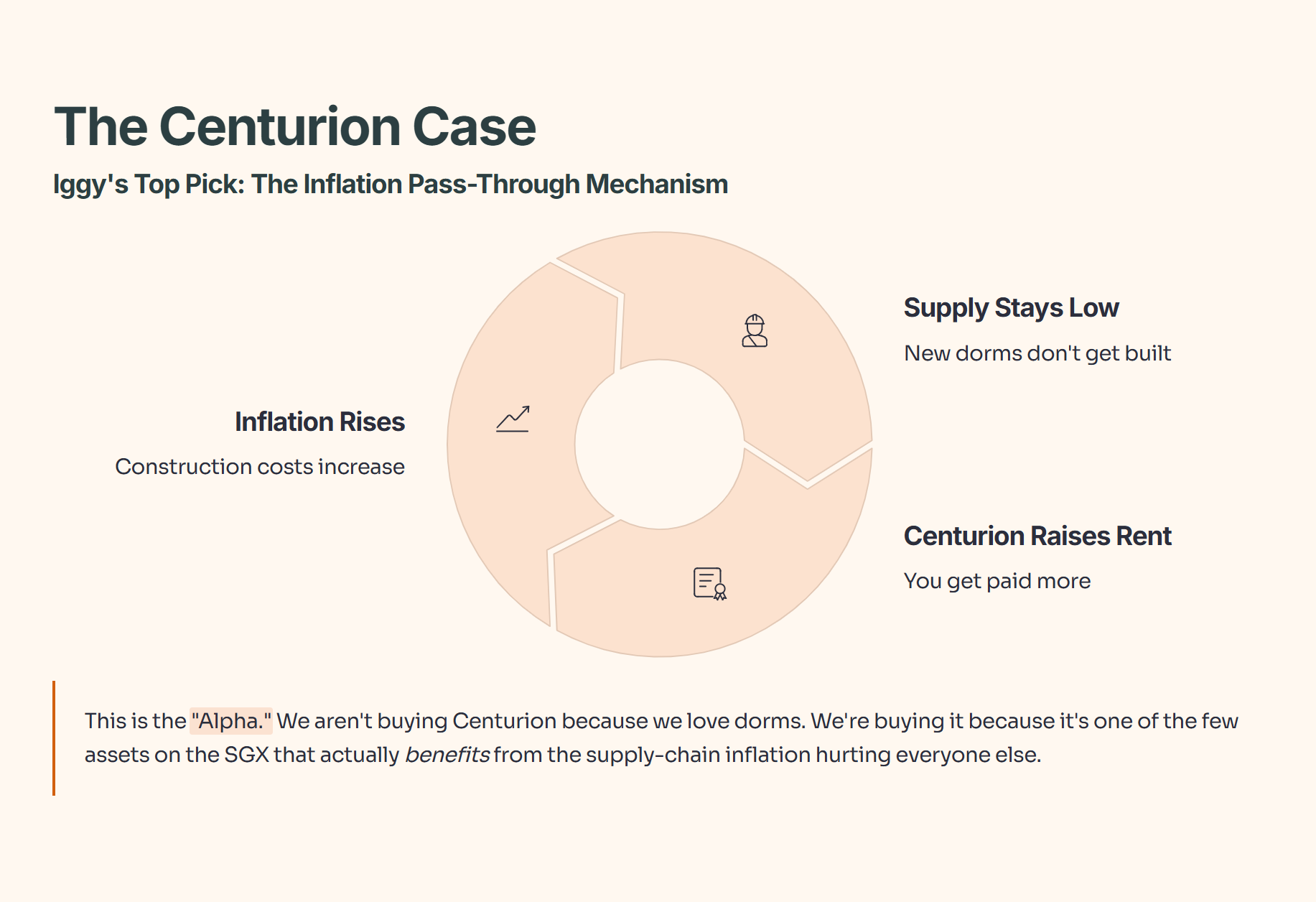

The Centurion Case:

This is my top pick for a reason. It is an Inflation Pass-Through Mechanism.

Inflation goes up? -> Construction costs rise -> New dorms don’t get built.

Supply stays low -> Centurion raises rent -> You get paid more.

This is the “Alpha.” We aren’t buying Centurion because we love dorms. We are buying it because it is one of the few assets on the SGX that actually benefits from the supply-chain inflation that is hurting everyone else.