Good evening. Iggy here — your forensic retail investor, ranked eighth among Singapore retail investors on Tiger Brokers, and permanently allergic to yield traps.

Every evening I run through the numbers so you do not have to guess. What clears my 4.7% minimum yield hurdle. What looks tempting but hides a cracked balance sheet underneath. What belongs in a CPF or SRS portfolio and what is pure speculation dressed up in a dividend.

Today’s pulse: four names on my radar, one macro read, and the usual forensic verdict with no suit-speak.

Let’s get into it.

In This Article:

The Market This Evening

Riverstone Holdings (AP4.SG) — The Yield That Demands a Second Look

Jumbo Group (42R.SG) — When the Numbers Tell You What the Menu Already Knows

SBS Transit (S61.SG) — Infrastructure Yield or Yield Illusion?

Geo Energy (RE4.SG) — Know What You Own

The Window Is Already Open

Evening Wrap

Iggy’s Forensic Disclaimer

The Market This Evening

STI closed at 4,942.77. Still circling below 5,000, which has been acting as a ceiling for weeks now. No catalyst broke through today. The market is not panicking — but it is not committing either.

Here is the context worth carrying into tonight’s reads. The six-month T-bill is yielding 1.40%. SSBs are sitting just above 2%. CPF OA at 2.5%. The only risk-free instrument clearing my 4.7% forensic minimum is CPF SA at 4.0% — and even that falls 70 basis points short. Inflation meanwhile has firmed to 1.7% year-on-year, electricity costs are up 2.1% quarter-on-quarter, and your household expenses are quietly rising while your cash savings earn almost nothing.

That is the environment every yield number tonight needs to be read against.

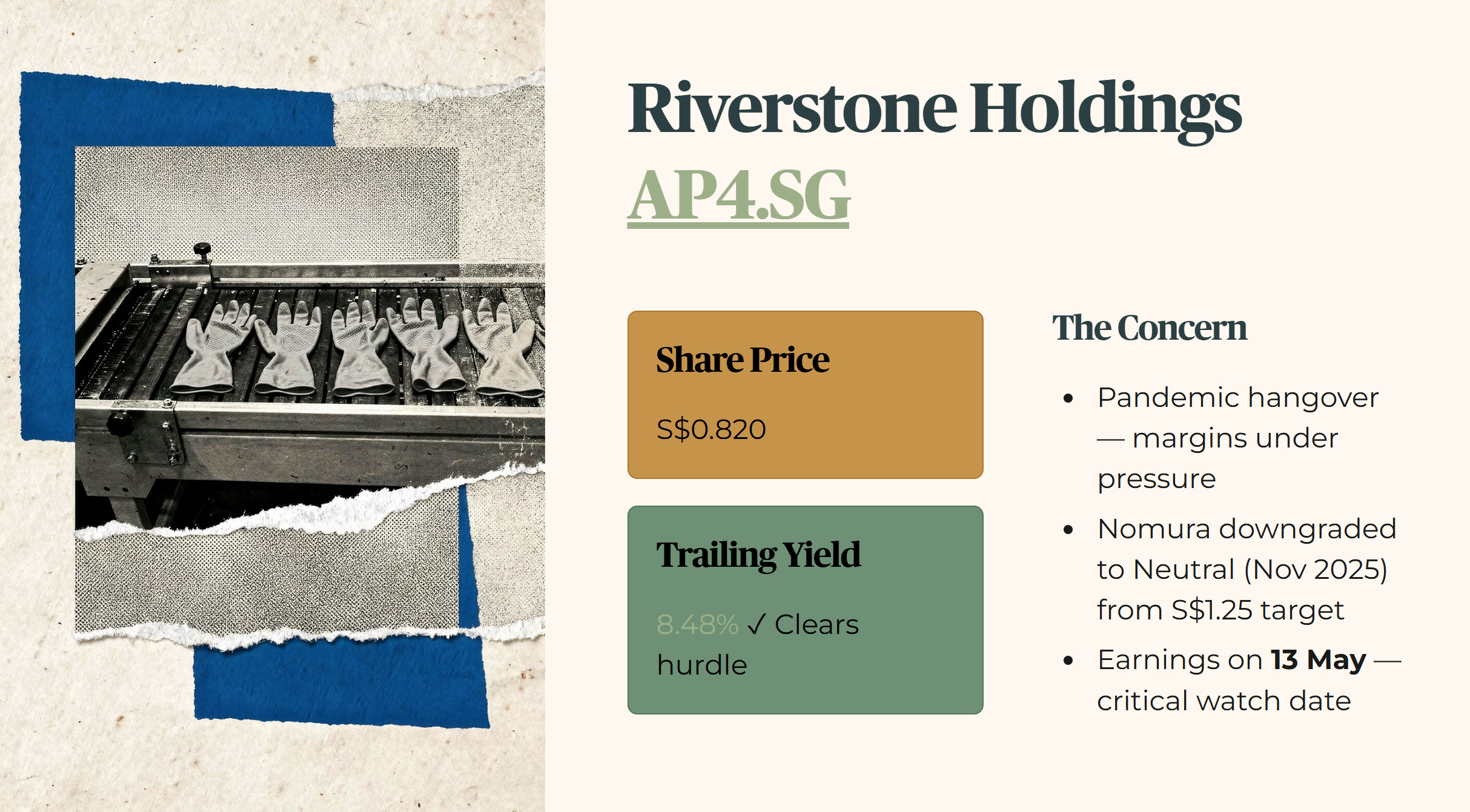

Riverstone Holdings (AP4.SG) — The Yield That Demands a Second Look

Share price: S$0.820. Trailing dividend yield: 8.48%.

That number clears my forensic floor by a wide margin. In a market where T-bills are paying 1.40% and the average heartland investor is watching their savings account do essentially nothing, 8.48% looks like the answer to every problem. That is precisely why it needs to be interrogated rather than celebrated.

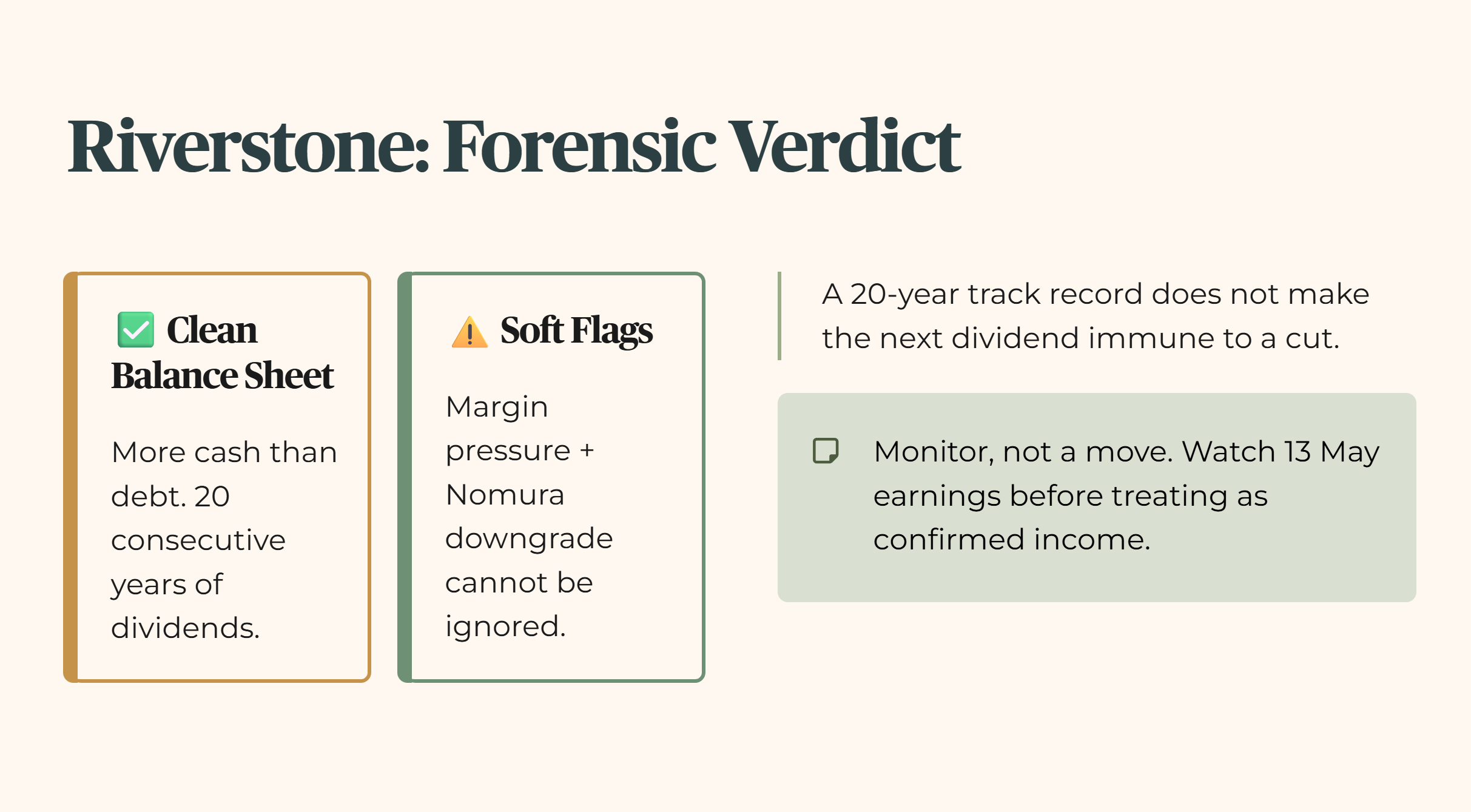

Riverstone manufactures cleanroom and healthcare gloves — a business that had its moment in the sun during the pandemic and has been navigating the hangover ever since. Margins have been under pressure. Revenue growth has slowed. Nomura, which had been a consistent bull on this name with price targets as high as S$1.25, downgraded to Neutral in November 2025 after weak nine-month results. That is not a minor signal. When the house that was calling S$1.25 pulls back to Neutral, something in the earnings trajectory gave them pause.

The balance sheet is genuinely clean — more cash than debt, 20 consecutive years of dividend payments. Those are real credentials. But a 20-year track record does not make the next dividend immune to a cut. High yields on glove manufacturers have a history of compressing sharply when margins deteriorate past a tipping point. The question is not whether 8.48% is real today. The question is whether it is still real after 13 May earnings.

Forensic read: Yield clears the hurdle. Balance sheet is sound. But margin pressure and a Nomura downgrade are soft flags that cannot be ignored. Watch the 13 May earnings closely before treating this as a confirmed income position. This is a monitor, not a move.

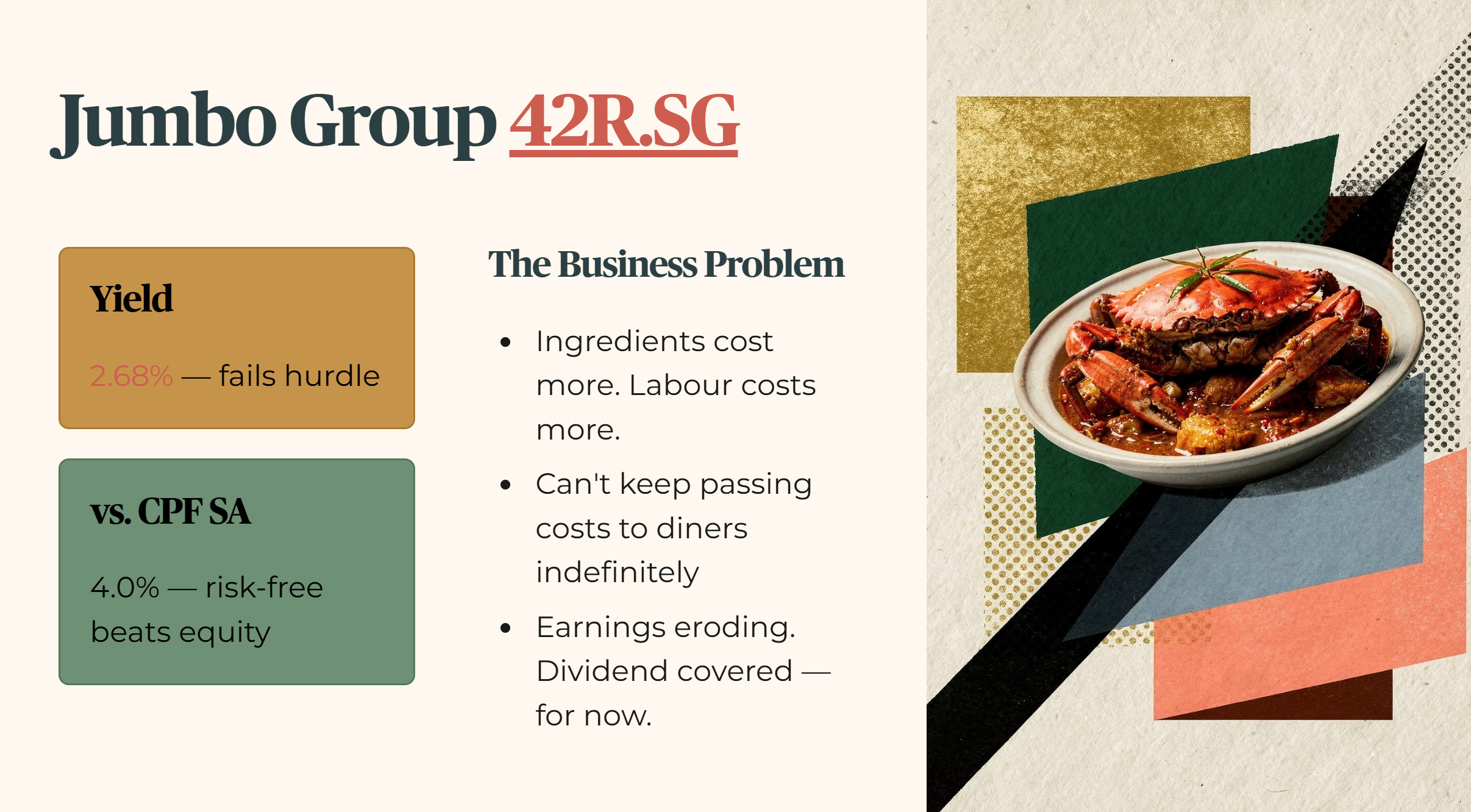

Jumbo Group (42R.SG) — When the Numbers Tell You What the Menu Already Knows

Yield: 2.68%.

Put that against CPF SA at 4.0%. Jumbo is asking you to take equity risk — the risk that earnings disappoint, that the dividend gets cut, that the share price falls — in exchange for a yield that does not even match what the government will pay you to do nothing. That is not a trade that makes forensic sense for a retirement portfolio.

The business problem is one every heartland Singaporean understands viscerally. Jumbo runs seafood restaurants. Ingredients cost more. Labour costs more. The price of a chilli crab dinner has limits — you cannot keep passing costs to the customer indefinitely before tables start going empty. Earnings are eroding. The dividend is covered for now, but covered-for-now is not the same as sustainable.

Forensic read: 2.68% fails my 4.7% minimum yield hurdle decisively. Below CPF SA. Below CPF OA. The operational trend is in the wrong direction. This does not belong in a retirement income portfolio at current yield levels. Full stop.

SBS Transit (S61.SG) — Infrastructure Yield or Yield Illusion?

Share price: S$3.59. Trailing dividend yield: 8.97%.

Four consecutive years of dividend increases. Net cash balance sheet. A business built on regulated public transport — the kind of essential service that does not disappear in a recession. On paper this is a strong income profile. But 8.97% on a regulated operator is the number that keeps a forensic investor up at night rather than sleeping soundly.

Here is the tension. Regulated revenue means stable income — but it also means capped upside. The government sets the framework. Fare increases go through the Public Transport Council. Cost pressures — and there are always cost pressures in a labour-intensive operation — cannot simply be passed on at will. When a regulated business is yielding nearly 9%, it usually means one of two things: either the market has mispriced a genuinely strong income stream, or the payout ratio is stretched and a normalisation is coming.

SBS Transit reports earnings today. That report will tell us whether the dividend trajectory is organic or whether the four consecutive increases have been running ahead of what the underlying cash flow can sustain.

Forensic read: Yield clears the hurdle comfortably. Balance sheet is clean. But the sustainability question is real and unanswered until today’s earnings. Do not size a position based on 8.97% before you have read the report.

Geo Energy (RE4.SG) — Know What You Own

Share price: S$0.63.

No yield figure to anchor. No forensic floor to test against. Geo Energy is a coal producer, which means the entire investment thesis lives and dies on commodity prices — and commodity prices are driven by factors entirely outside any management team’s control. Brent crude briefly touched above US$119 a barrel on 29 April on Iran and Strait of Hormuz tensions. Commodity sentiment is elevated right now. That can change in a week.

This is not a retirement income position. It is not a CPF or SRS candidate. If you own it, you are making a directional bet on coal prices and regional energy demand. That is a legitimate thing to do with speculative capital. It is not a legitimate thing to do with money you cannot afford to lose.

Forensic read: Outside forensic scope for income portfolios. Speculative only. Position size accordingly and do not let a short-term price move convince you it has become something it is not.

The Window Is Already Open

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

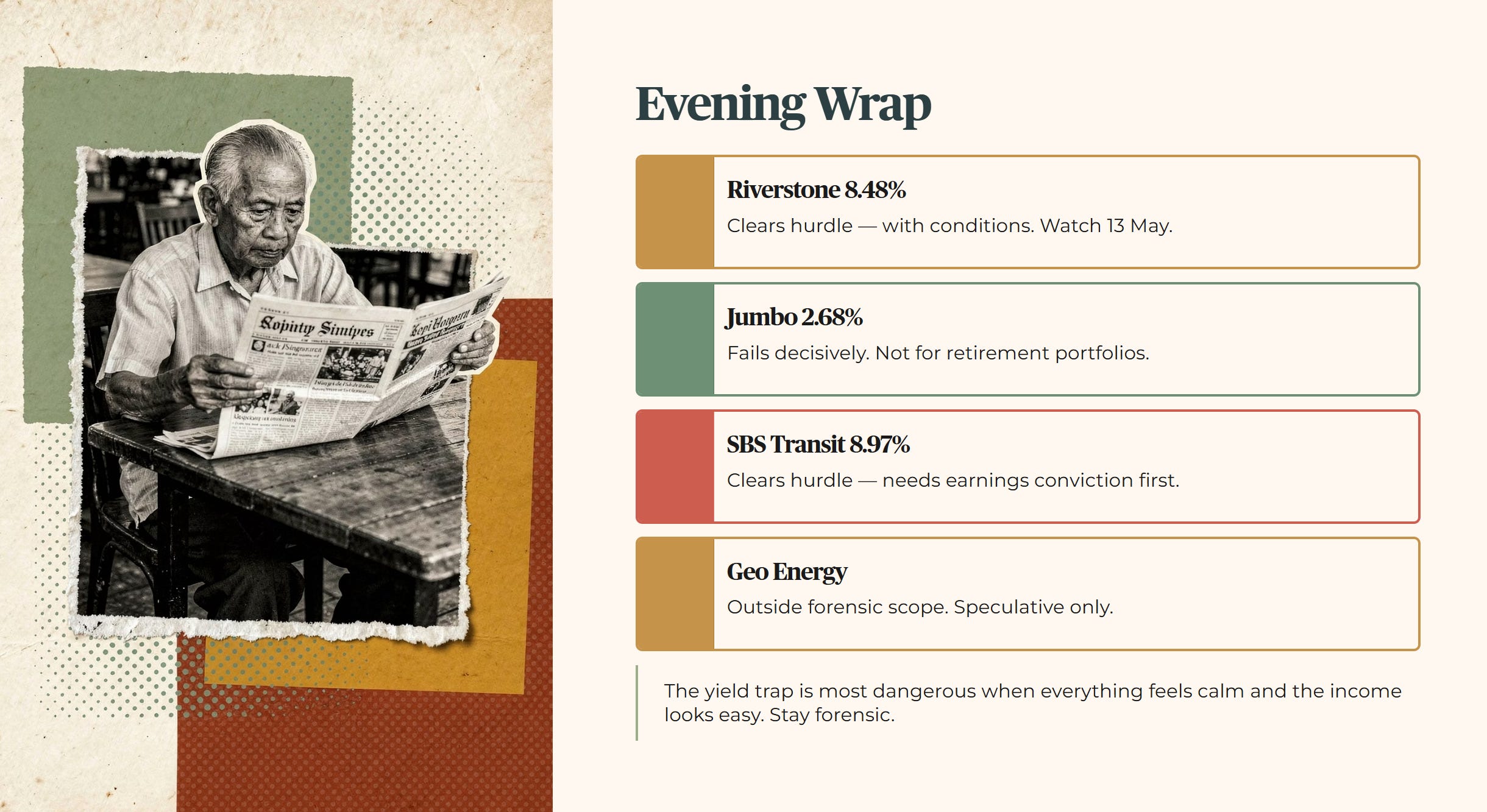

Evening Wrap

Four names tonight. One clears the hurdle with conditions attached. One fails it decisively. One clears it but needs an earnings report before it earns conviction. One sits outside the forensic framework entirely.

The common thread is the macro environment. With risk-free rates this low and inflation quietly climbing into your household expenses, every yield number looks more attractive than it should. That is exactly when forensic discipline matters most. The yield trap is not a concept for bear markets only. It is most dangerous when everything feels calm and the income looks easy.

Stay forensic.

Iggy’s Forensic Disclaimer

This content is produced for educational and informational purposes only. I am not a financial advisor — I am a retail investor who applies forensic analysis to my own portfolio and shares that process publicly. Nothing here constitutes a recommendation to buy, sell, or hold any security, and no specific target prices or personalised financial advice are offered. Stocks assessed under Iggy’s Forensic Yield Standard are benchmarked against a 4.7% minimum yield hurdle; stocks flagged as Growth Watch fall below this threshold but demonstrate clean balance sheet metrics and an identifiable growth catalyst — these carry a materially different risk profile and are not suitable as yield replacements for income-dependent investors. All data is sourced from public filings and verified sources; where data is unverified it is explicitly flagged. All investments carry risk, including the potential loss of principal, and past performance is not indicative of future results. If you are making investment decisions involving CPF, SRS, or personal capital, please conduct your own due diligence or consult a MAS-licensed financial adviser before committing funds.