SGX Dividend Payouts Jun to Aug 2026: The Forensic Breakdown | Which Ones Actually Clear the Bar?

The June to August 2026 Dividend Radar: One Passer, Ten Traps

The June to August 2026 Dividend Radar: One Passer, Ten Traps

Out of every Singapore stock declaring a dividend payout on the radar for the next three months, exactly one company clears my minimum threshold for retirement income. The rest of the list is a minefield of non-recurring distributions, foreign exchange leakage, and yields that fail to beat what you can get from a guaranteed government account. If you are holding these names thinking they will safely fund your retirement drawdown, the raw math on these upcoming distributions says otherwise.

If you are chasing short-term price momentum or trading capital gains, a lower-quality dividend layout might clear your hurdle. But if you are a retiree focused on capital preservation and dependable lifestyle income, my forensic standard is built to protect that money. This quarter, looking at the crop of payouts landing between June and August 2026, we need to talk about why the headline numbers do not match the cash that actually hits your bank account.

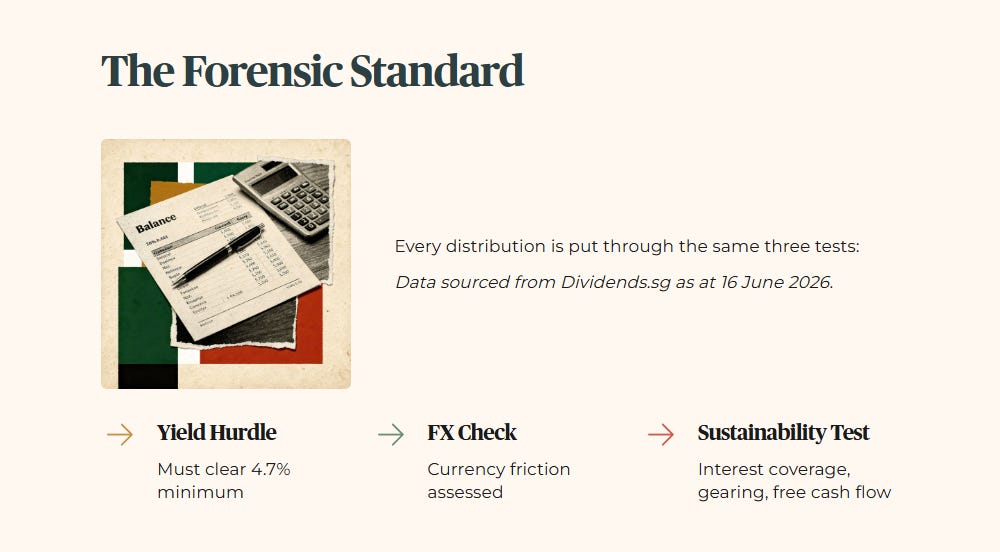

Every few months, Iggy runs a forensic sweep of the upcoming dividend calendar, not to chase the highest headline number, but to separate the payouts that genuinely work for a retirement portfolio from the ones that look generous until you read the fine print. This is that segment. If you have been following along, you know the forensic standard: every distribution gets put through the same yield hurdle, the same FX check, and the same sustainability test that I apply to my own retirement capital. Today we are looking at the June to August 2026 payout window, and the results are more sobering than the headline yields suggest.

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips, the interest coverage, the gearing, the free cash flow sustainability, so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

Upcoming Dividend Radar: June to August 2026

Trap 1: The Special Dividend Illusion

Iggy’s Insight

Trap 2: The FX Friction Problem

Trap 3: Yield Below the CPF SA Floor

You Shouldn’t Be Reading This Alone

The One Name That Clears the Hurdle

Iggy’s Insight

The Bottom Line

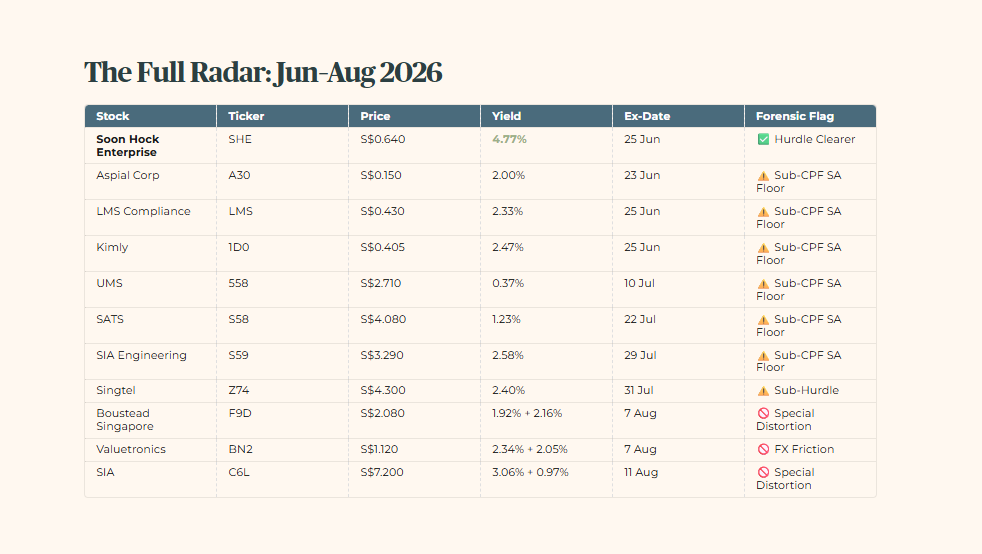

Here is the master checklist of the upcoming dividend radar entries. Every figure is sourced directly from Dividends.sg as at 16 June 2026.

This is where the dividend math breaks for the vast majority of retail favourites.

Upcoming Dividend Radar: June to August 2026

Trap 1: The Special Dividend Illusion

The biggest danger to a retiree’s cash flow is an accounting spike passed off as regular income. Look at Boustead Singapore (F9D) and Singapore Airlines (C6L) on this calendar cycle. Both are distributing across two separate tranches, and neither tranche clears the 4.7% minimum yield hurdle (the income threshold I require before any stock qualifies for a retirement portfolio) on its own or in combination.

A special dividend is a non-recurring payment made by a company to its shareholders from one-time events like asset sales or windfall profits. It does not reflect sustainable core business earnings. When you build a retirement drawdown plan around a special dividend, you are making a structural mistake. You are treating a temporary capital distribution as permanent cash flow.

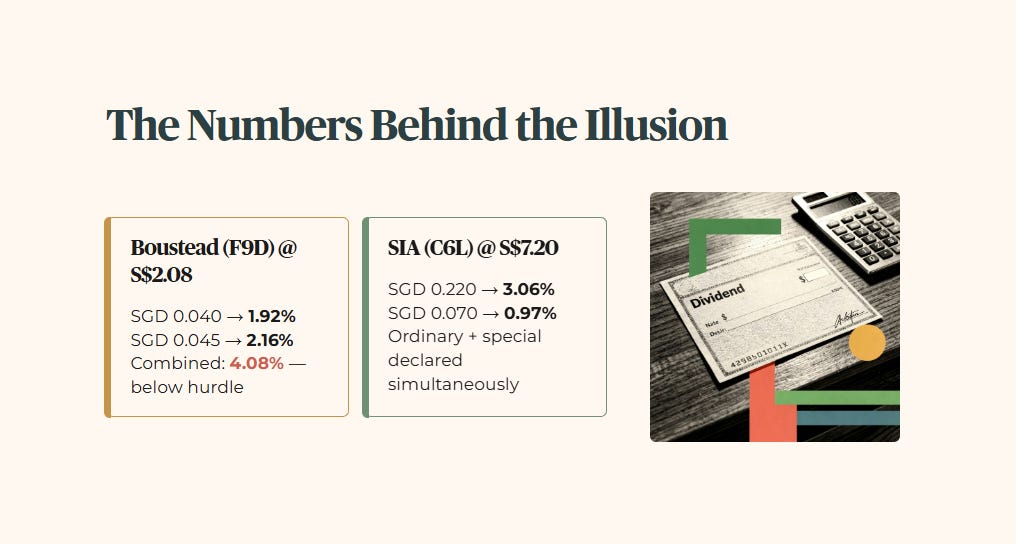

Boustead is paying SGD 0.040 and SGD 0.045 separately, yielding 1.92% and 2.16% on each tranche at the current price of S$2.08. Even combined at 4.08%, the total falls below the hurdle. SIA is distributing SGD 0.220 as its larger tranche and SGD 0.070 as a secondary payment, producing 3.06% and 0.97% respectively at S$7.20. The ordinary payout and the special component are being declared simultaneously, which makes the headline figure look more attractive than the repeatable income actually is.

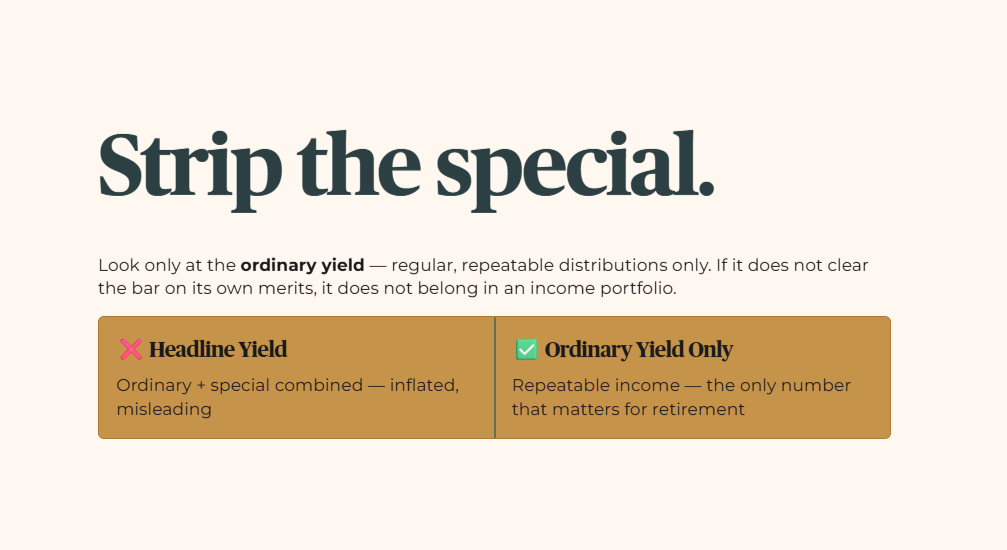

To protect your wallet, strip out the special components completely. Look only at the ordinary yield, the dividend yield calculated using only regular, repeatable distributions. If the ordinary yield does not clear the bar on its own merits, the stock does not belong in an income portfolio.

Iggy’s Insight

Special dividends are the corporate equivalent of selling the family car to pay the electricity bill. It feels great when the cash lands, but you cannot repeat the trick next year. Boustead and SIA are distributing cash from specific operational peaks that are already rolling over as global capacity normalises. If your monthly expenses depend on these payouts remaining flat, you are positioning your portfolio for a sudden drop in income. Always run your retirement math on the ordinary distributions alone. One-off cash bursts are a bonus for capital preservation, never a foundation for sustainable drawdown.

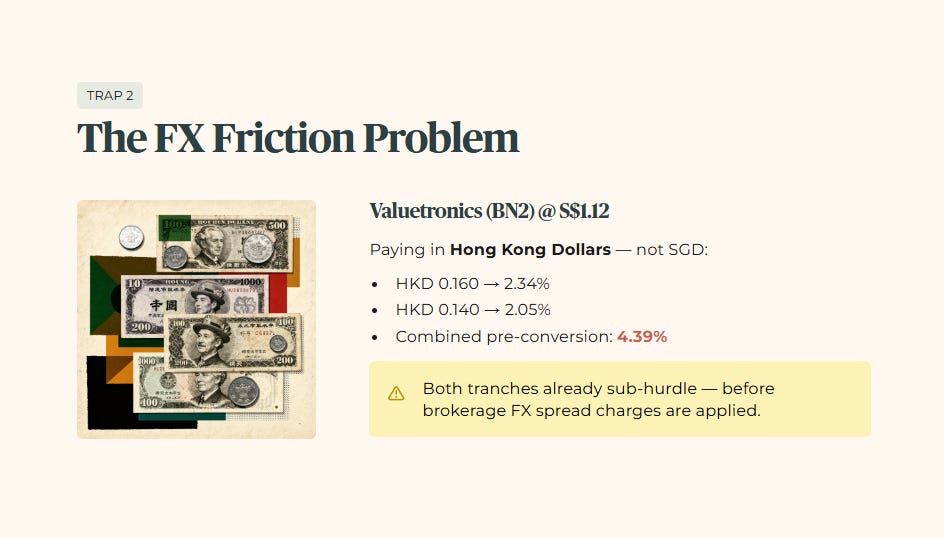

Trap 2: The FX Friction Problem

Valuetronics (BN2) carries a different kind of hidden cost. The stock is paying out two separate tranches denominated in Hong Kong Dollars, not Singapore Dollars: HKD 0.160 and HKD 0.140, yielding 2.34% and 2.05% respectively at the current price of S$1.12. Even before accounting for currency conversion, both tranches sit well below the 4.7% hurdle.

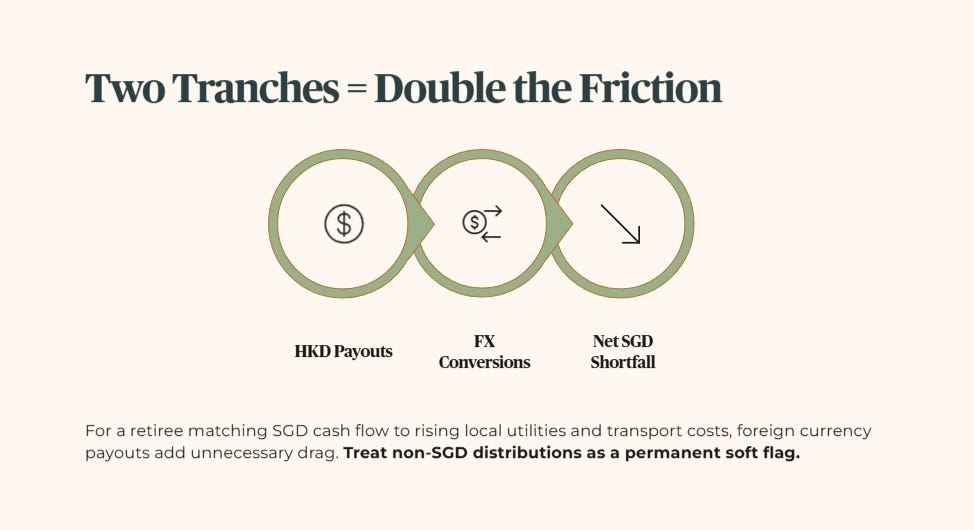

The more important issue for a Singapore retirement portfolio is what I call FX friction: the losses an investor incurs from foreign currency conversion fees and unfavourable exchange rates applied by brokerages. When a foreign currency payout drops into a local brokerage account, the bank does not convert it out of charity. They charge a spread, and for a retail investor holding a modest position, those fixed conversion fees and currency movements quietly reduce an already sub-hurdle yield further.

The split-tranche structure compounds this. Two separate HKD payouts mean two separate conversion events, two separate spread charges, and two separate exposures to short-term SGD/HKD rate movement. A combined pre-conversion yield of 4.39% on paper becomes a materially lower net cash return in your bank account by the time both tranches clear. For an investor relying on clean SGD cash flow to match rising local utilities and transport costs, foreign currency payouts add unnecessary friction to a retirement budget. Treat non-SGD distributions as a permanent soft flag for an income portfolio.

The combined 4.39% headline yield is already eroding under FX friction at the pre-conversion level — and once we stack it against the CPF SA sanctuary floor and my 4.7% forensic hurdle in the next section, the gap between “looks acceptable” and “fails the retirement math” becomes uncomfortably clear.