Weekly SGX Gainers & Losers (4 April 2026) **Heartland Retiree Yield Trap |🦖EP1525

The Investing Iguana | Week Ending 2 April 2026

Weekly Gainers & Losers — Forensic Audit

The Investing Iguana | Week Ending 4 April 2026

Three of SGX’s top movers this week are parading five-year historical average yields that mask severe current-day income compression and massive structural debt. If you are holding these momentum names for your retirement cash flow, you are underwriting their leverage with your own capital while fighting a losing battle against inflation.

In This Article:

The Macro Pulse

This Weeks Forensic Movers The Gainers

This Weeks Forensic Warnings The Losers

Financial Health Checklist

Dividend Trajectory Current vs Historical Average

Peer Comparison SGX Forensic Benchmarks

The Forensic Yield Spread Monitor

The Macro Connector

Iggys Weekly Verdict

Iggys Forensic Compliance Standards Standard Disclaimer

About Iggy & the Elite Investors

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

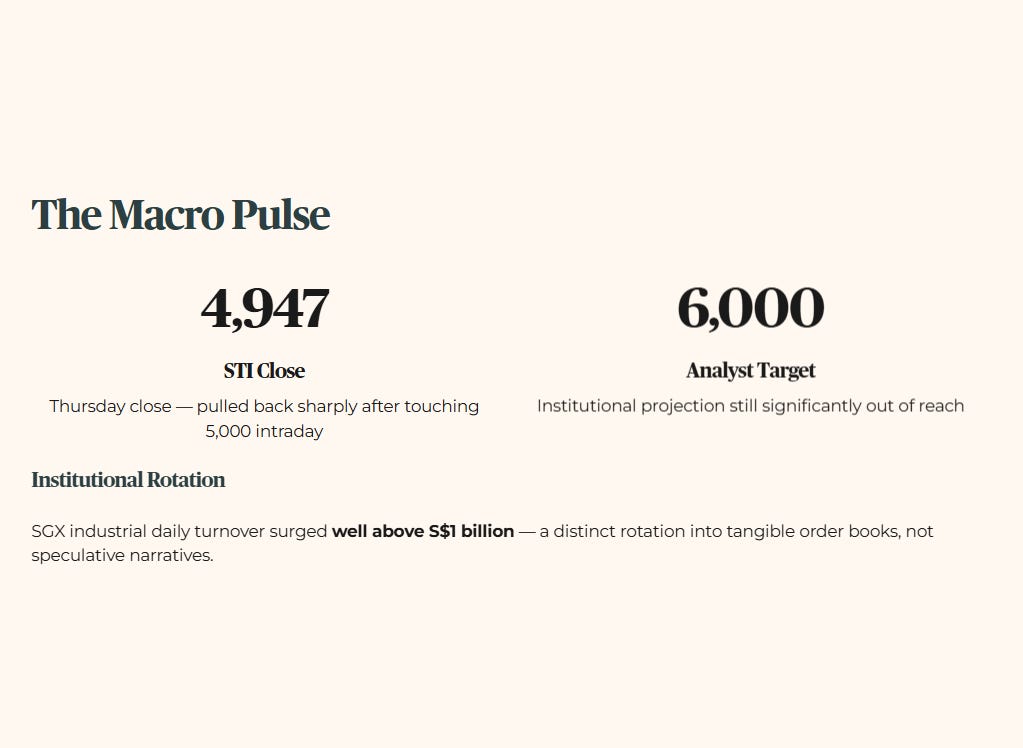

The Macro Pulse

The Straits Times Index closed Thursday at 4,947.50 — touching 5,000 intraday before pulling back sharply, ending the week below that psychological barrier and still significantly adrift from the 6,000-point milestone projected by institutional analysts. Meanwhile, SGX industrial daily turnover has surged well above the S$1 billion mark, signalling a distinct institutional rotation into tangible order books rather than speculative narratives.

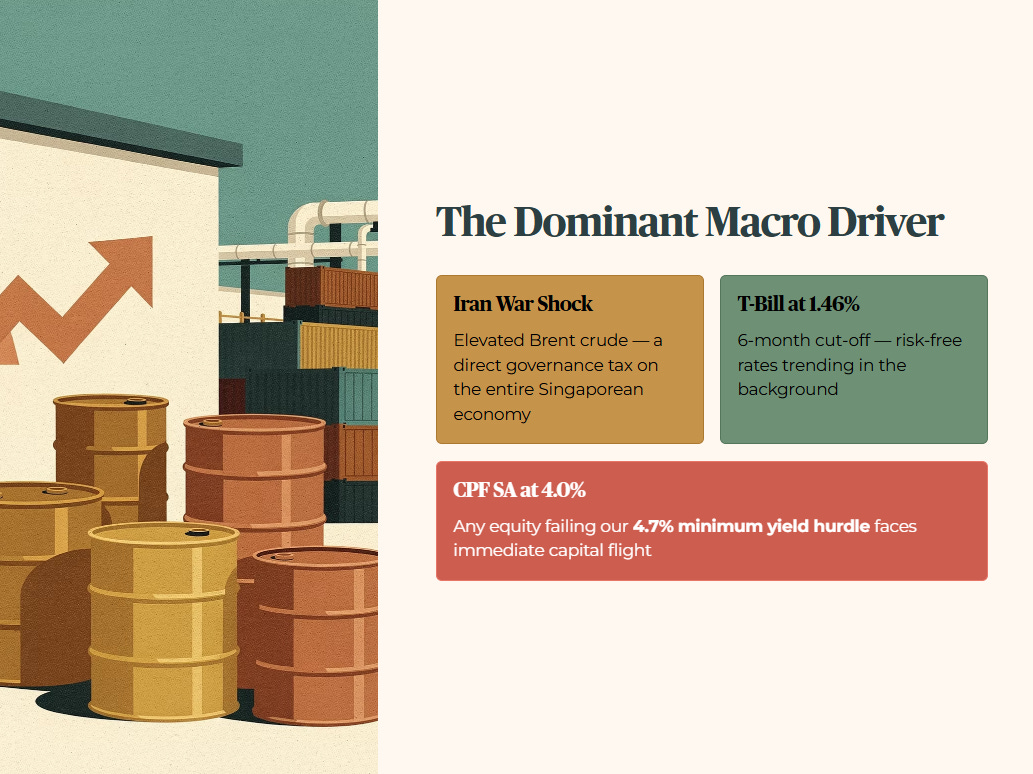

The single macro driver dominating this week’s tape is the escalating Iran War Shock, which has elevated Brent crude prices and functions as a direct, unavoidable governance tax on the entire Singaporean economy. The latest 6-month T-Bill auction cut-off locked at 1.46% — a sobering reminder that risk-free rates continue trending in the background. With the CPF Special Account sanctuary benchmark holding firm at 4.0%, any equity asset failing to clear our 4.7% minimum yield hurdle faces immediate capital flight as the market enforces strict financial discipline.

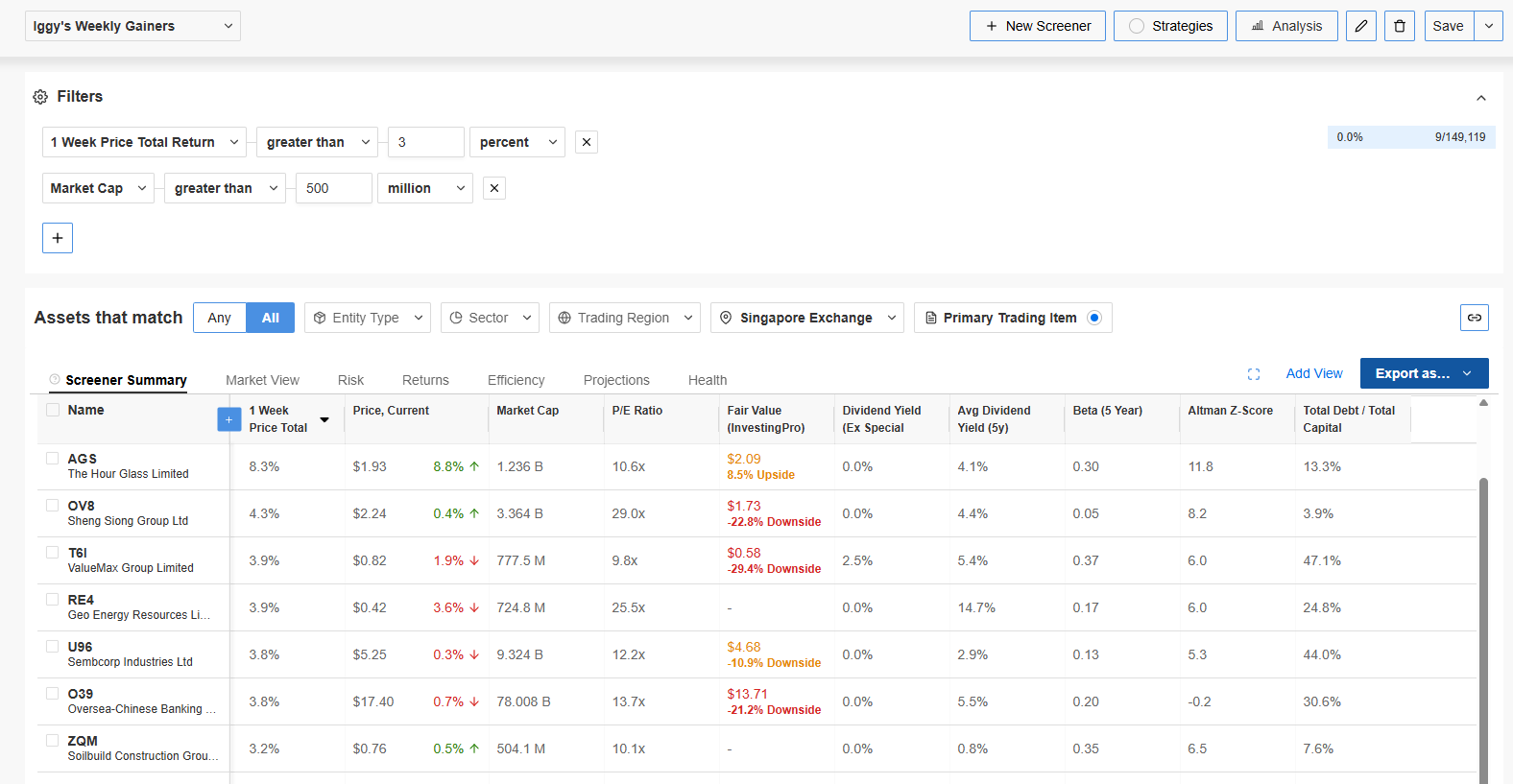

This Week’s Forensic Movers — The Gainers

(Note: Prices are in USD)

— GEARING ALERT

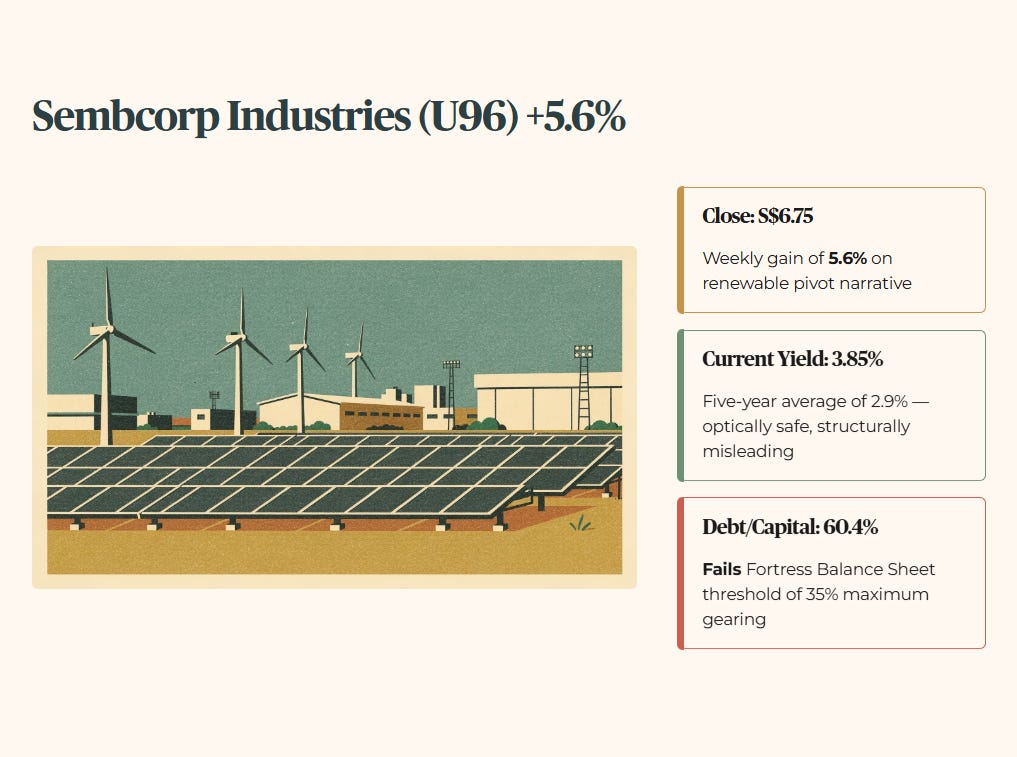

Sembcorp Industries (U96)

Raw Fact: Sembcorp Industries (U96) gained 5.6% to close at S$6.75, carrying a financial debt-to-capital ratio of 60.4% while offering a trailing current yield of just 3.85%.

Historical Benchmark: The screener presents an optically safe five-year average yield of 2.9%, but the current leverage profile is dramatically heavier than historical norms prior to the renewable transition.

Peer Context: Compared to SGX peers like ST Engineering, which maintains disciplined capital recycling, Sembcorp explicitly fails the Fortress Balance Sheet threshold of 35% maximum gearing.

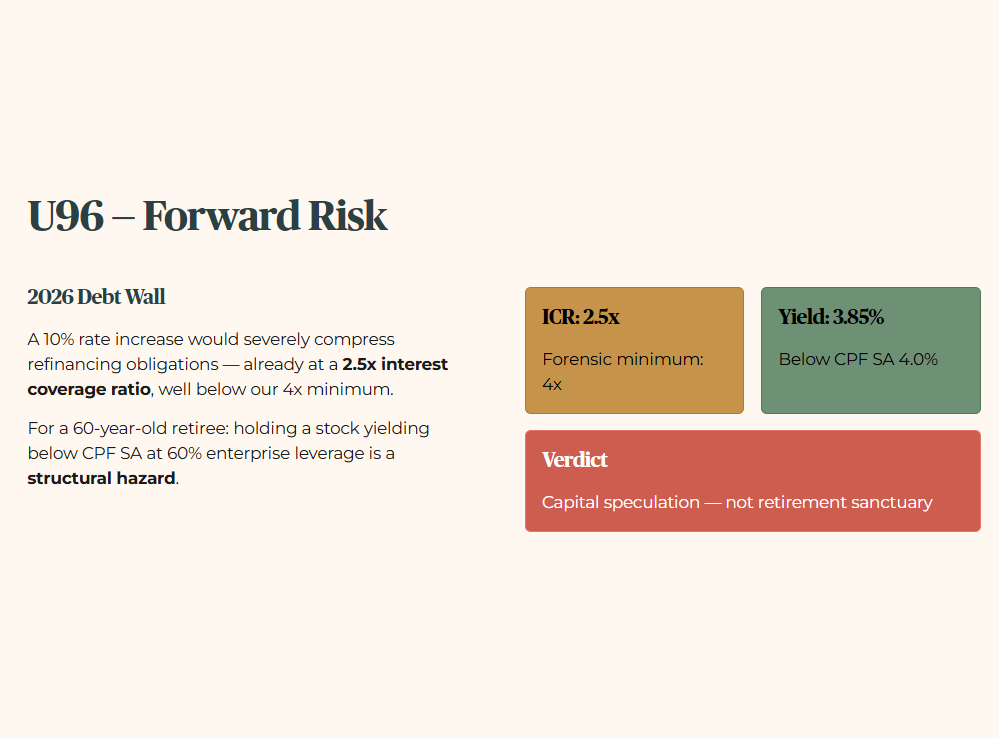

Forward Scenario: In a scenario where regional rates increase by 10% heading into the 2026 debt wall, Sembcorp’s refinancing obligations will severely compress its 2.5x interest coverage ratio — a figure that already sits well below our 4x minimum — delaying capital returns further.

Wallet Impact: For a 60-year-old retail investor relying on dividends to cover rising utility bills, holding a stock yielding below the CPF SA benchmark while carrying sixty percent enterprise leverage is a structural hazard. My forensic stance is that this is a capital appreciation speculation, not a retirement sanctuary.

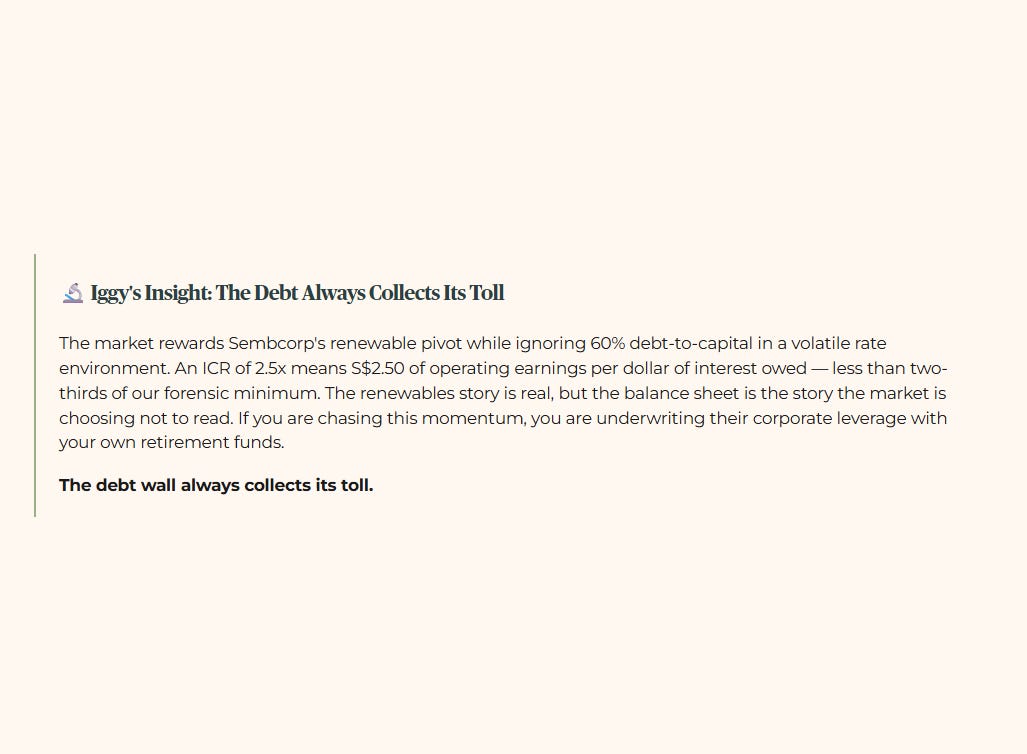

🔬 Iggy’s Insight: The Debt Always Collects Its Toll

The market is currently rewarding Sembcorp for its renewable pivot while ignoring the structural danger of carrying sixty percent debt-to-capital in a volatile rate environment. An interest coverage ratio of 2.5x means the business is generating just S$2.50 of operating earnings for every dollar of interest it owes — less than two-thirds of our forensic minimum of 4x. You cannot outrun borrowing costs with capital expenditure narratives forever. The renewables story is real, but the balance sheet is the story the market is choosing not to read. If you are chasing this momentum, you are effectively underwriting their corporate leverage with your own retirement funds. The debt wall always collects its toll.

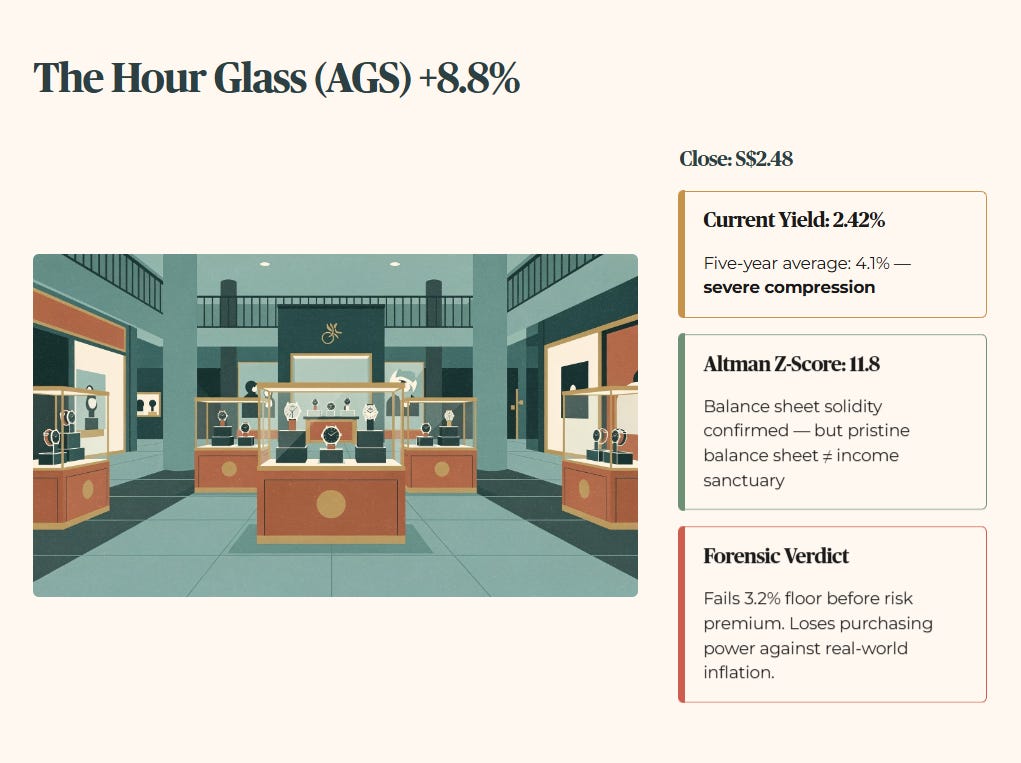

The Hour Glass (AGS)

Raw Fact: The Hour Glass (AGS) delivered an 8.8% return to S$2.48, masking a current trailing yield of just 2.42% beneath an attractive five-year historical average payout of 4.1%.

Forensic Verdict: This severe compression in current yield indicates the stock is trading purely on luxury technical momentum rather than income fundamentals. A 2.42% yield falls below our 3.2% Forensic Floor before we even apply the 150-basis-point risk premium. It protects capital on paper but functionally loses purchasing power against real-world inflation for a mature income portfolio.

Altman Z-Score of 11.8 per InvestingPro confirms balance sheet solidity — but a pristine balance sheet generating sub-floor income does not constitute a sanctuary.

Sheng Siong (OV8)

Raw Fact: Sheng Siong (OV8) rose 5.9% to S$2.88, backed by a bank-debt ratio that expands to 22.8% when fully accounting for lease liabilities. The current yield has compressed to 2.22% — the five-year average of 4.4% tells a very different story than the current reality.

Forensic Verdict: At 2.22%, OV8 fails the forensic floor by a full percentage point. Its Altman Z-Score of 8.2 per InvestingPro signals genuine operational resilience, and the balance sheet is clean on financial debt. But a defensive parking spot that does not generate the required income is not a retirement asset — it is a capital preservation placeholder while you wait for something better.

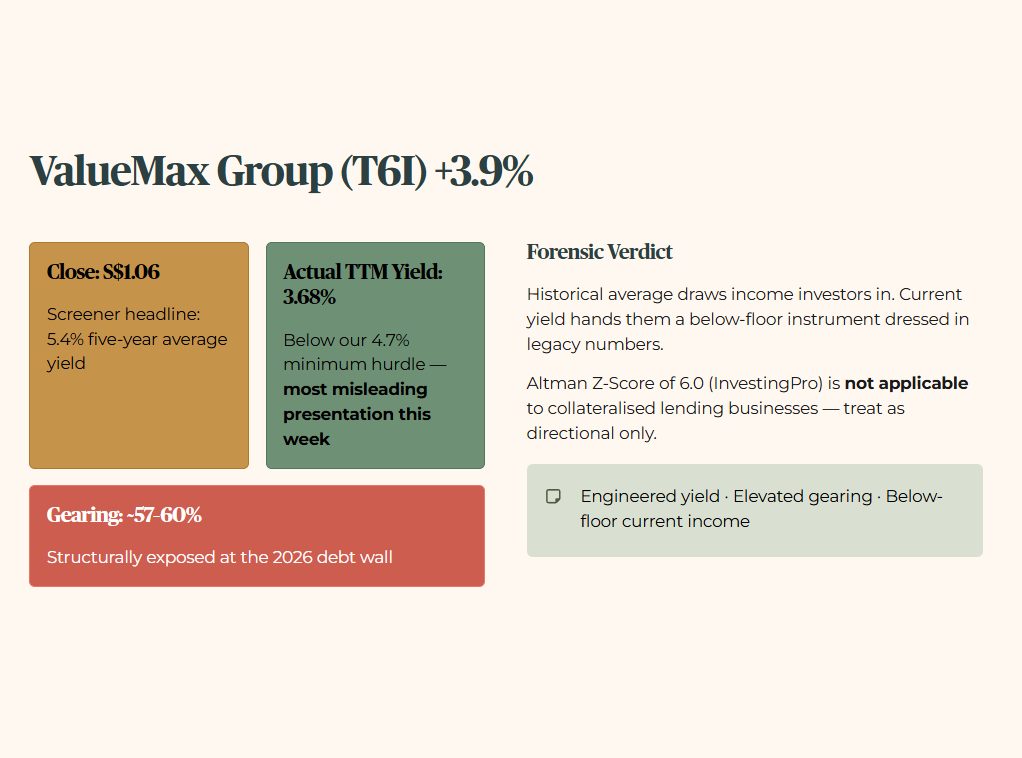

ValueMax Group (T6I)

Raw Fact: ValueMax Group (T6I) gained 3.9% to close at S$1.06. The five-year average yield from the screener reads 5.4%, but the confirmed TTM trailing yield at current price is 3.68% — sitting below our 4.7% minimum hurdle.

Forensic Verdict: This is the most misleading presentation in this week’s tape. The historical average yield headline of 5.4% draws income investors in; the actual current yield of 3.68% hands them a below-floor instrument dressed in legacy numbers. Layer a gearing ratio of approximately 57–60% (per cross-verified external sources) on top of that, and this pawnbroker’s balance sheet is structurally exposed at the 2026 debt wall.

Note: Altman Z-Score is not designed for collateralised lending businesses — the InvestingPro figure of 6.0 should not be interpreted the same way it would for a manufacturer or retailer. The forensic read stands regardless: engineered yield, elevated gearing, below-floor current income.

Gainers Summary Table

Note: U96 Altman Z-Score sourced from InvestingPro screener. Primary balance sheet computation places U96 in the grey zone (Z’ ~1.94). T6I Z-Score model is structurally unsuited to collateralised lending businesses — treat as directional only.

This Week’s Forensic Warnings — The Losers

The yield spread calculation above clears the floor for no counter — but the unambiguous disqualification pattern in the next section changes the entire week's verdict.