SGX Weekly Gainers & Movers 3 May 2026: Debt Ceiling Breached | 🦖EP1589

No real yield means your 100,000 dollar portfolio cannot cover one month of utilities in Singapore

Three of the five biggest SGX gainers this week are carrying gearing above the ceiling and the market has not priced that in yet. If you are holding any of them for income, the forensic picture is more complicated than the price chart suggests.

Iggy’s Different Kind of Content: Retirement-Grade Investing

Most financial content is built around excitement — what is surging, what is breaking out, what you might be missing. I am deliberately building something different. Retirement-grade investing is not exciting. It is disciplined, forensic, and it is designed to still be working when you need it most.

In This Article:

Iggy’s Different Kind of Content: Retirement-Grade Investing

The Macro Pulse

This Weeks Forensic Movers The Gainers

Featured Gainer AEM Holdings Ltd AWX YIELD TRAP ALERT

Remaining Gainers

This Weeks Forensic Warnings The Losers

Featured Loser Mapletree Pan Asia Commercial Trust N2IU MULTI THRESHOLD ALERT

Remaining Losers

The Forensic Yield Spread Monitor

The Macro Connector

The Window Is Already Open

Iggys Weekly Verdict

Iggys Forensic Disclaimer

The Macro Pulse

The Straits Times Index (STI) continues to flirt with the 4,912.69 level, placing it within a 104-point strike distance of the 5,000-point milestone. This psychological level remains the terminal target for several institutional analysts for the 2026 fiscal year. Regionally, sentiment is bolstered by stabilised factory activity data in China, yet the local narrative is overshadowed by a rising Private Credit Gating Crisis documented in the Iggy Operational Log.

The primary macro driver this week is the widening Forensic Gap between high-growth technology proxies and the deteriorating balance sheets of commercial property assets. The 6-month T-Bill yield has slipped to 1.40%, sitting a full 180 basis points below my conservative 3.2% forensic floor. This collapse in risk-free rates is forcing capital into riskier equity tranches without a corresponding increase in forensic quality.

This Week’s Forensic Movers — The Gainers

The market is currently rewarding revenue momentum in the semiconductor space while ignoring the massive yield deficit compared to historical sanctuary assets.

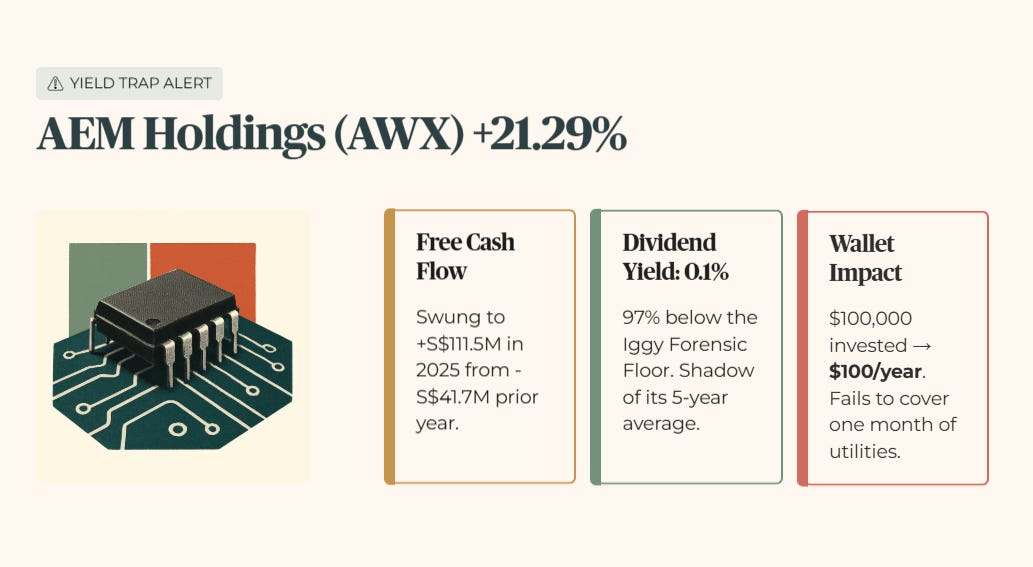

Featured Gainer: AEM Holdings Ltd (AWX) — YIELD TRAP ALERT

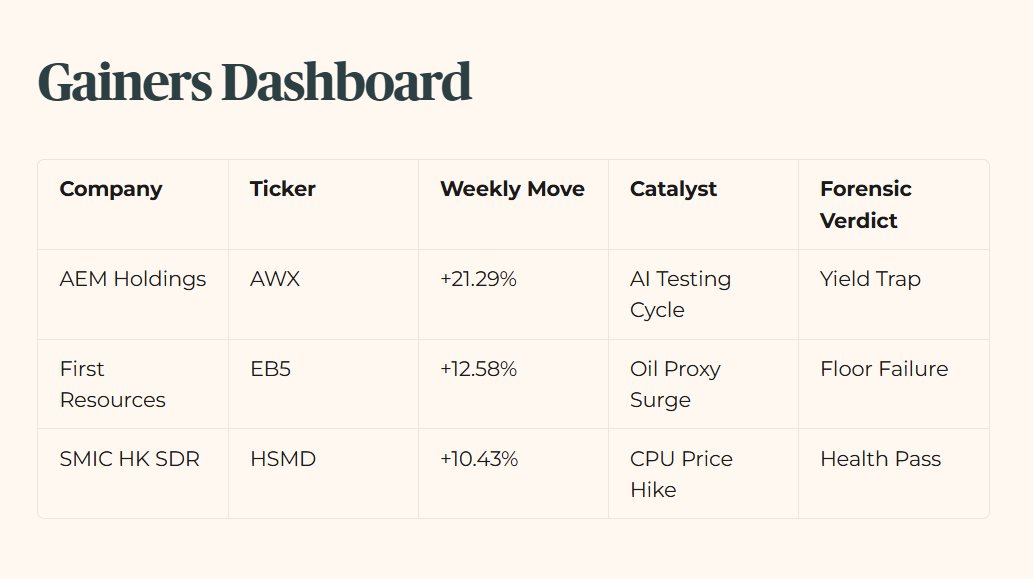

Raw Fact: AEM Holdings reported a return to positive free cash flow of S$111.5 million in 2025, swinging from negative S$41.7 million in the prior year, alongside a 21.29% weekly price surge.

Historical Benchmark: The current dividend yield of 0.1% is a shadow of its five-year average when the stock was a staple for growth-income hybrid portfolios. Even with the reinstatement of dividends, the payout remains 97% below the Iggy Forensic Floor.

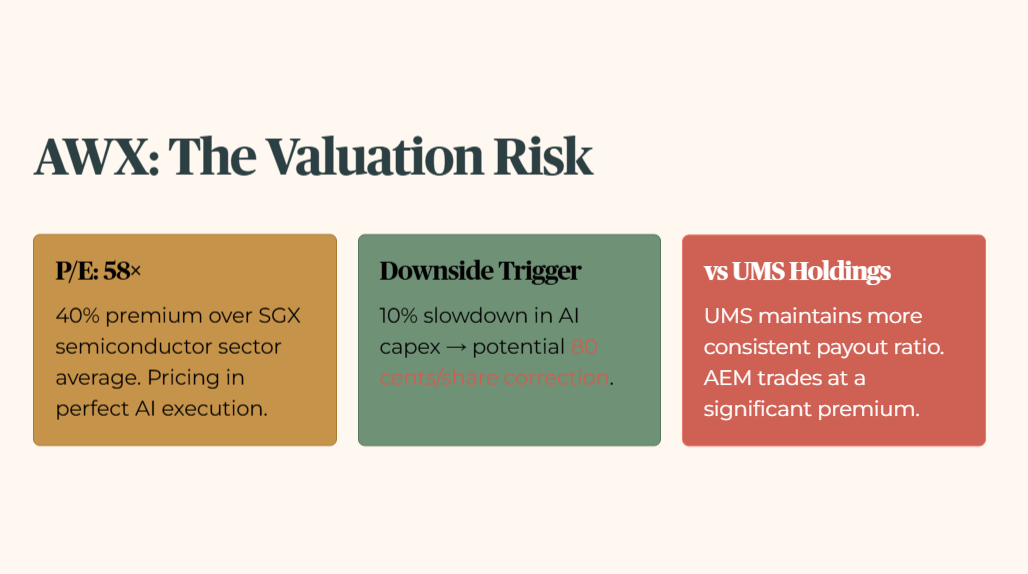

Peer Context: Compared to UMS Holdings, which maintains a more consistent payout ratio, AEM is trading at a price-to-earnings multiple of 58 times. This is a 40% premium over the semiconductor sector average on the SGX, suggesting the market is pricing in perfect execution of the AI testing cycle.

Forward Scenario: A 10% slowdown in global AI capital expenditure spending by major chipmakers would likely trigger a sharp contraction in AEM’s forward multiple, potentially resulting in a 80 cents per share price correction. This macro trigger is the primary risk to the current momentum.

Wallet Impact: For the tech-curious retiree who bought into the AI hype, a 21% price gain feels like a win. A 100,000 dollar investment at the current 0.1% yield generates just 100 dollars in annual income. That fails to cover even a single month of basic utility bills in the current inflationary environment.

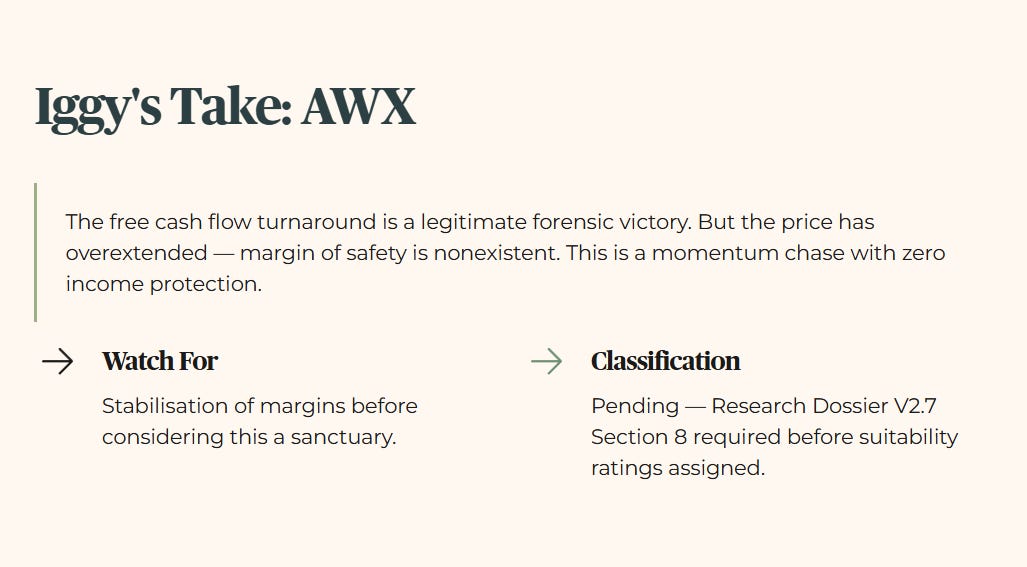

Iggy’s Take

The free cash flow turnaround is a legitimate forensic victory for the balance sheet. However, the price has overextended into a zone where the margin of safety is nonexistent. This is a classic momentum chase where investors ignore the yield floor in hopes of capital gains. I am watching for a stabilisation of margins before considering this a sanctuary for long-term capital. The AI Infrastructure Trade is currently a growth play with zero income protection.

Remaining Gainers

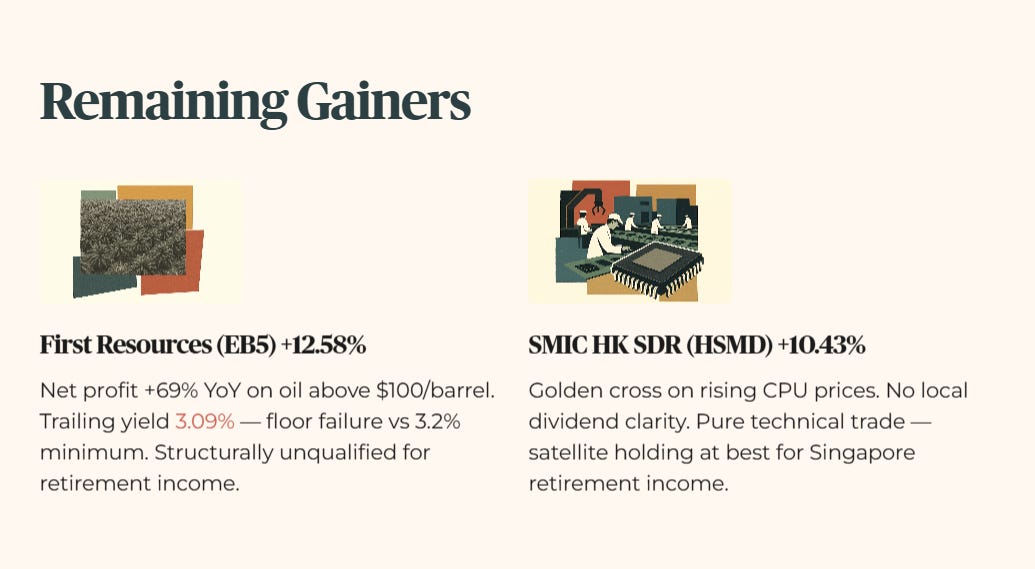

First Resources Ltd (EB5): Net profit increased 69% year on year as global oil benchmarks spiked past 100 US dollars per barrel. This is a commodity-driven windfall that masks the underlying volatility of palm oil pricing. The trailing yield has compressed to 3.09% at the current price — a floor failure against my 3.2% minimum standard, not merely a hurdle shortfall. Investors should treat the income profile here as structurally unqualified for a retirement dividend portfolio at current prices.

SMIC HK SDR (HSMD): The stock triggered a technical golden cross following a 10% weekly gain driven by rising global CPU prices. The lack of local dividend clarity makes this a pure technical trade. This is a satellite holding at best for anyone focused on Singaporean retirement income.

Gainers Dashboard

This Week’s Forensic Warnings — The Losers

The bleeding in the REIT sector is no longer about interest rates alone. It is now a forensic assessment of which managers can survive a debt wall without diluting shareholders.

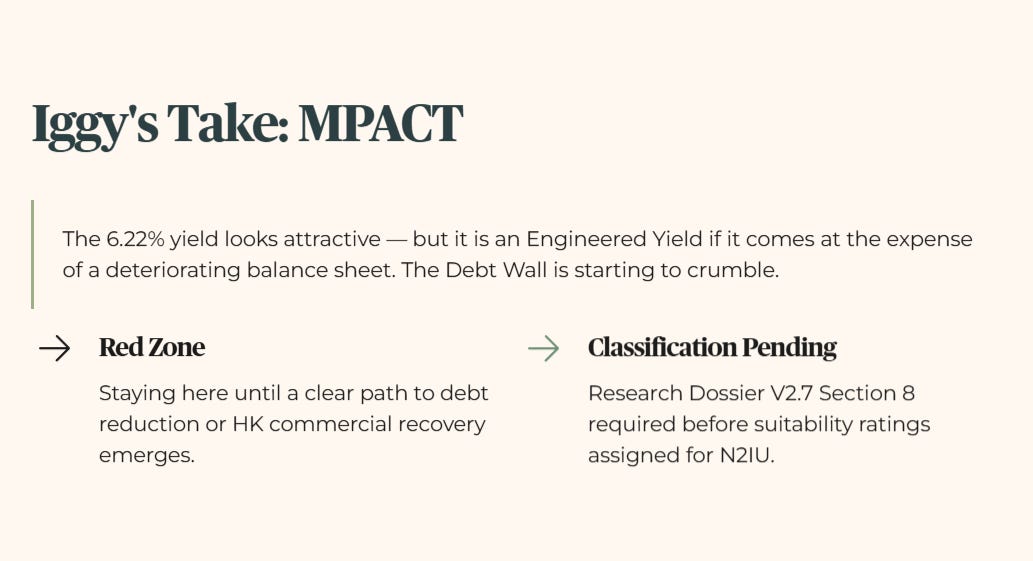

Featured Loser: Mapletree Pan Asia Commercial Trust (N2IU) — MULTI-THRESHOLD ALERT

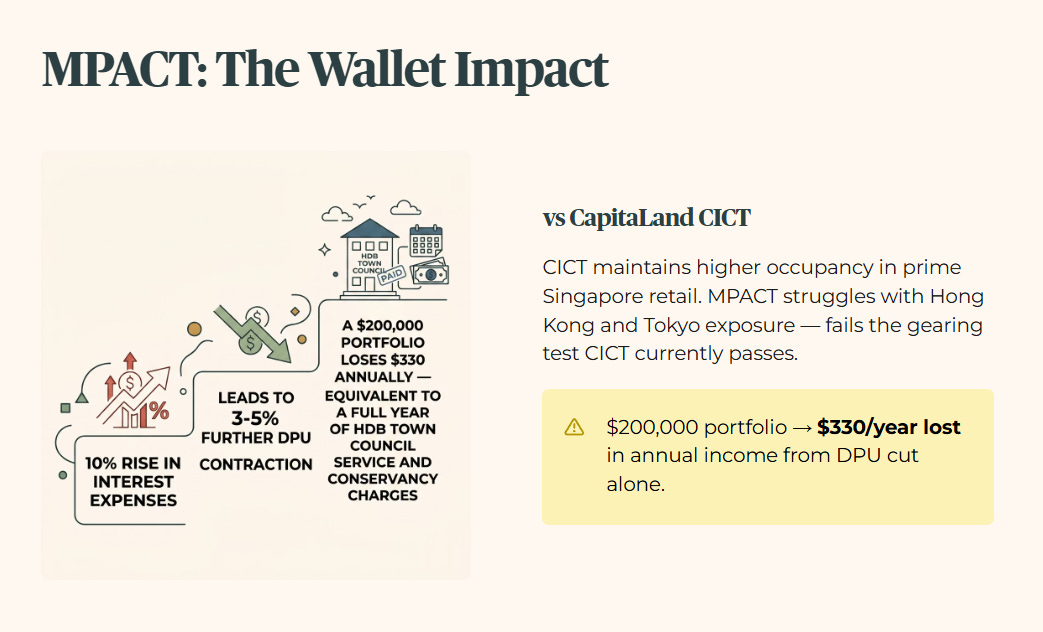

Raw Fact: MPACT reported a 2.6% fall in Distribution per Unit to 1.9 Singapore cents for the fourth quarter, while verified gearing has reached 36.02% against total assets of 15.424 billion Singapore dollars.

Historical Benchmark: The gearing ratio has now climbed above the 35% fortress line, a significant departure from its historical range of 30% to 33%. This reduces the debt headroom for future acquisitions to just 3.2 billion Singapore dollars before hitting regulatory caps.

Peer Context: Compared to CapitaLand Integrated Commercial Trust, which has managed to maintain higher occupancy in prime Singapore retail, MPACT is struggling with its Hong Kong and Tokyo commercial exposure. It fails the gearing test that CICT currently passes.

Forward Scenario: A 10% increase in interest expenses across its unhedged debt portion would likely lead to a further 3% to 5% contraction in distribution per unit. This is the higher-for-longer macro trigger that the market is beginning to price in.

Wallet Impact: For the dividend seeker relying on MPACT for monthly expenses, the 2.6% distribution per unit drop is a direct pay cut. On a 200,000 dollar portfolio, that represents a loss of roughly 330 dollars in annual income. That is equivalent to a full year of standard HDB town council service and conservancy charges.

Iggy’s Take

The breach of the 35% gearing ceiling is the primary forensic red flag here. While the 6.22% yield looks attractive, it is an Engineered Yield if it comes at the expense of a deteriorating balance sheet. I am keeping this in the Red Zone until we see a clear path to debt reduction or a recovery in the Hong Kong commercial segment. The Debt Wall is starting to crumble for over-leveraged commercial assets.

Remaining Losers

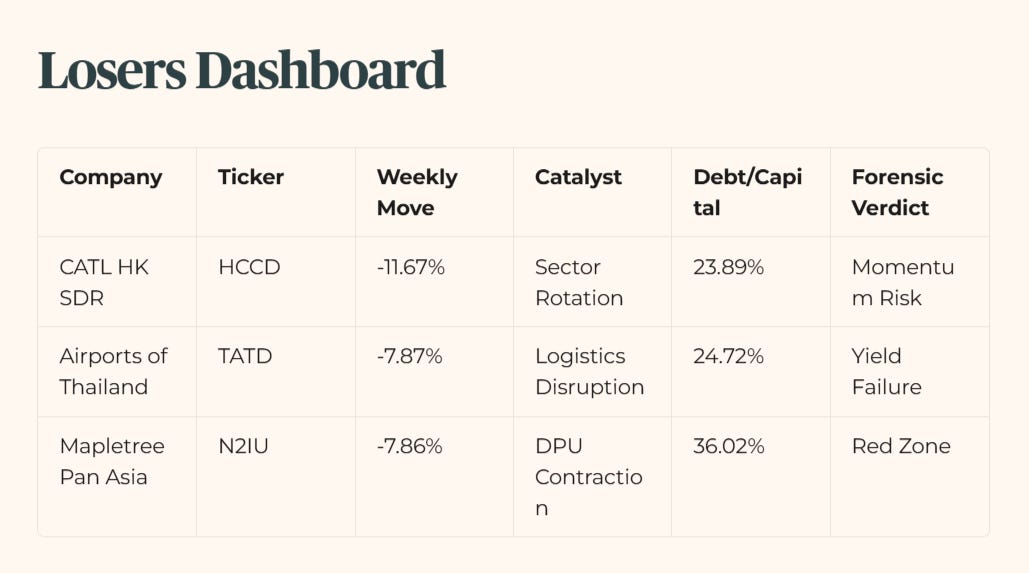

CATL HK SDR (HCCD): Price fell 11.67% as the market pivoted away from the green transition trade and into AI infrastructure. This is a liquidity drain rather than a fundamental failure of the battery business model. For the heartland investor, this volatility confirms that SDRs are not sanctuary assets.

Airports of Thailand SDR (TATD): Travel disruptions and rising jet fuel costs led to a 7.87% decline this week. While the long-term recovery thesis remains, the current yield profile fails to meet the 4.7% mandatory hurdle. This makes it an unattractive option for those prioritising immediate cash flow.

Losers Dashboard

The Forensic Yield Spread Monitor

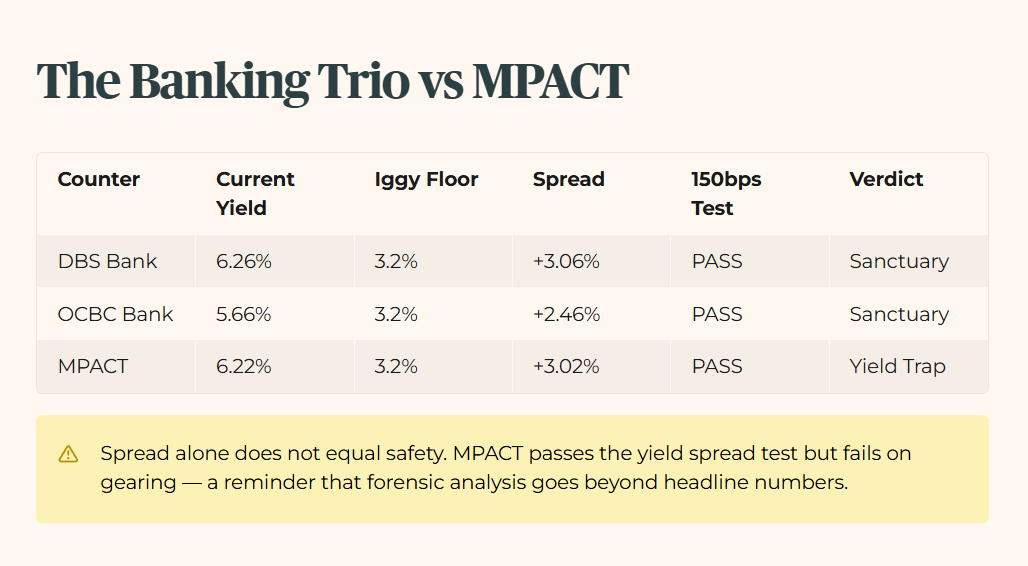

The local banks continue to act as the banking sanctuary while the rest of the market struggles to find a floor.

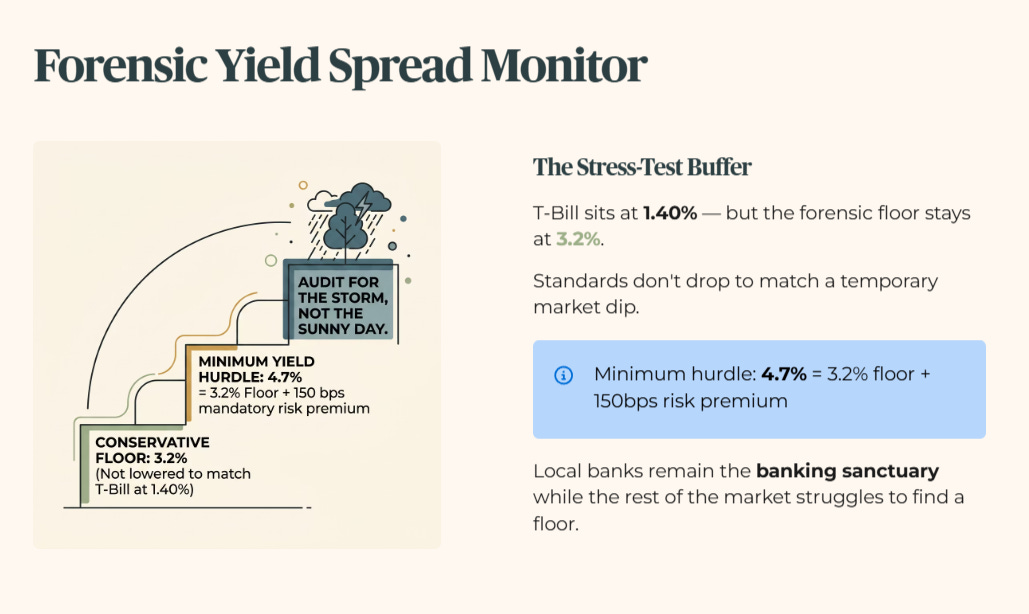

Note on the Stress-Test Buffer: For this audit, I apply a conservative floor of 3.2%. We audit for the storm, not just the sunny day. The 6-month T-Bill sits at 1.40%, but I do not lower my standards to match a temporary market dip. My floor remains at 3.2% to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle is 4.7% — that is the 3.2% floor plus 150 basis points of mandatory risk premium.

The spread between the Banking Trio and the crumbling REIT sector is widening, signalling a regime shift where balance sheet strength is valued over headline yield.

The Macro Connector

The connecting theme this week is the Great Yield Decoupling. We are seeing investors abandon traditionally safe REITs in favour of high-growth tech stocks that offer no income protection. This shift is happening just as the Private Credit Gating Crisis begins to tighten liquidity in the wealth management space. The pattern implies a looming credit squeeze where the only surviving assets will be those with fortress balance sheets and organic income growth.

The Window Is Already Open

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

Iggy’s Weekly Verdict

The most important takeaway for a heartland investor is that the STI at 5,000 is a facade. While the index looks healthy, the Debt Wall for commercial property is becoming a critical failure point. This aligns explicitly with my Private Credit Gating Crisis thesis in the Iggy Operational Log. If liquidity in private funds continues to dry up, the slow-motion bank run will eventually hit the public markets. For my own portfolio construction, I am tracking the interest coverage ratios of the S-REIT sector. This is a personal forensic boundary, not a recommendation.

Iggy’s Forensic Disclaimer

This content is produced for educational and informational purposes only. I am not a financial advisor — I am a retail investor who applies forensic analysis to my own portfolio and shares that process publicly. Nothing here constitutes a recommendation to buy, sell, or hold any security, and no specific target prices or personalised financial advice are offered. Stocks assessed under Iggy’s Forensic Yield Standard are benchmarked against a 4.7% minimum yield hurdle; stocks flagged as Growth Watch fall below this threshold but demonstrate clean balance sheet metrics and an identifiable growth catalyst — these carry a materially different risk profile and are not suitable as yield replacements for income-dependent investors. All data is sourced from public filings and verified sources; where data is unverified it is explicitly flagged. All investments carry risk, including the potential loss of principal, and past performance is not indicative of future results. If you are making investment decisions involving CPF, SRS, or personal capital, please conduct your own due diligence or consult a MAS-licensed financial adviser before committing funds.