SGX Weekly: 8C8U REIT Yield Fails The Stress Test |🦖EP1511

Chasing 0.3% yield is like queuing 2 hours for free tissue paper. Brother, the bus fare also more expensive!

Sunday is the day most retail investors do their worst thinking. The market is closed, the weekend papers are full of analyst upgrades, and without live prices to anchor them, people talk themselves into positions they will regret on Monday. This week gave us plenty of material to work with. Let us run the forensic lens over the tape before the week gets away from you. Welcome back. Let us audit the tape.

In This Article:

The Macro Pulse

This Week’s Forensic Movers — The Gainers

This Week’s Forensic Warnings — The Losers

The Forensic Yield Spread Monitor

The Macro Connector

Iggy’s Weekly Verdict

About Iggy & the Elite Investors

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

The Macro Pulse

We keep our forensic focus firmly locked on the 6,000-point STI milestone. The index formally breached its 5,000-point resistance back in February, but has since retraced to 4,898.18 as at 27 Mar close. On the rates front, the latest 6-Month MAS T-Bill cut-off for BS26106T sits at 1.46% (Mar26 auction). Meanwhile, the 1-Month Compounded SORA remains stubbornly elevated near 1.13-1.15% (Mar data).

The macro driver this week is glaringly obvious: retail capital is executing a speculative rotation away from yield and straight into cyclical growth. Investors across the region are willingly bypassing the sanctuary of yield to chase high-beta momentum, aggressively discarding niche assets regardless of their underlying balance sheet health. We are seeing a complete disregard for defensive positioning.

This Week’s Forensic Movers — The Gainers

“Is your yield a trap? Check the Health Score before you buy.” Stop trading on gut feelings. Get the same data the banks keep for themselves. Use code INVESTINGIGUANA to lock in your edge at half price. 💎

📈 [Verify Your Portfolio Safety Here]

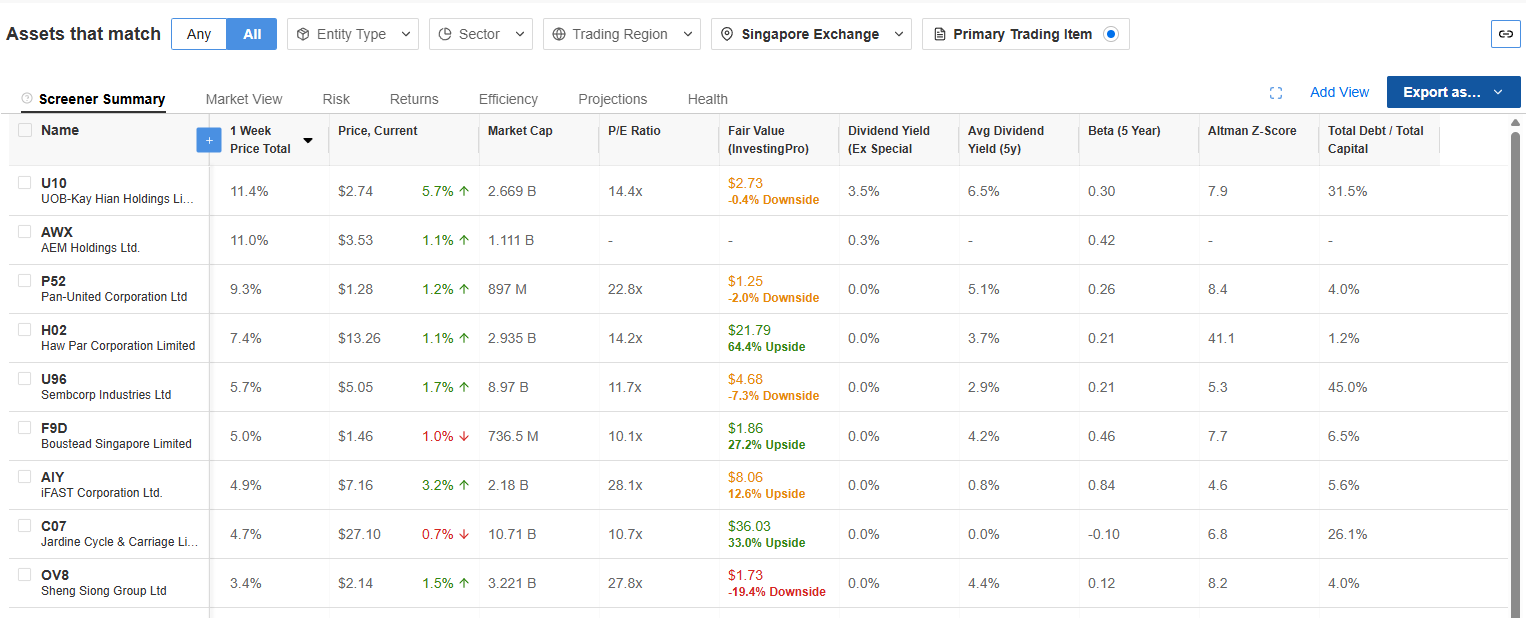

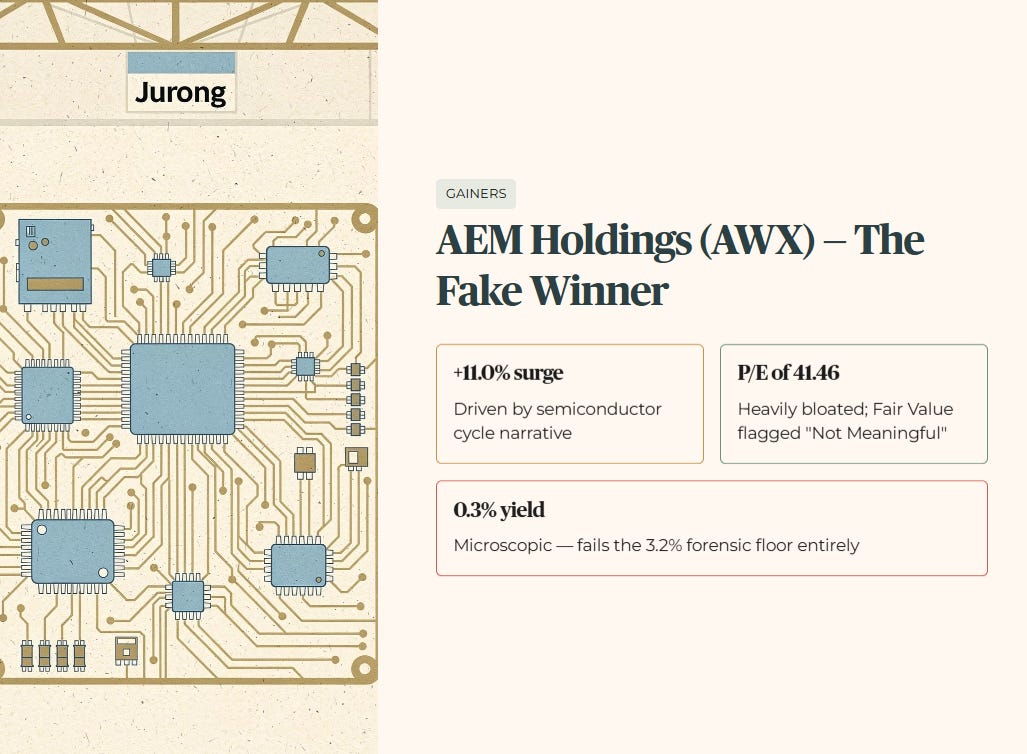

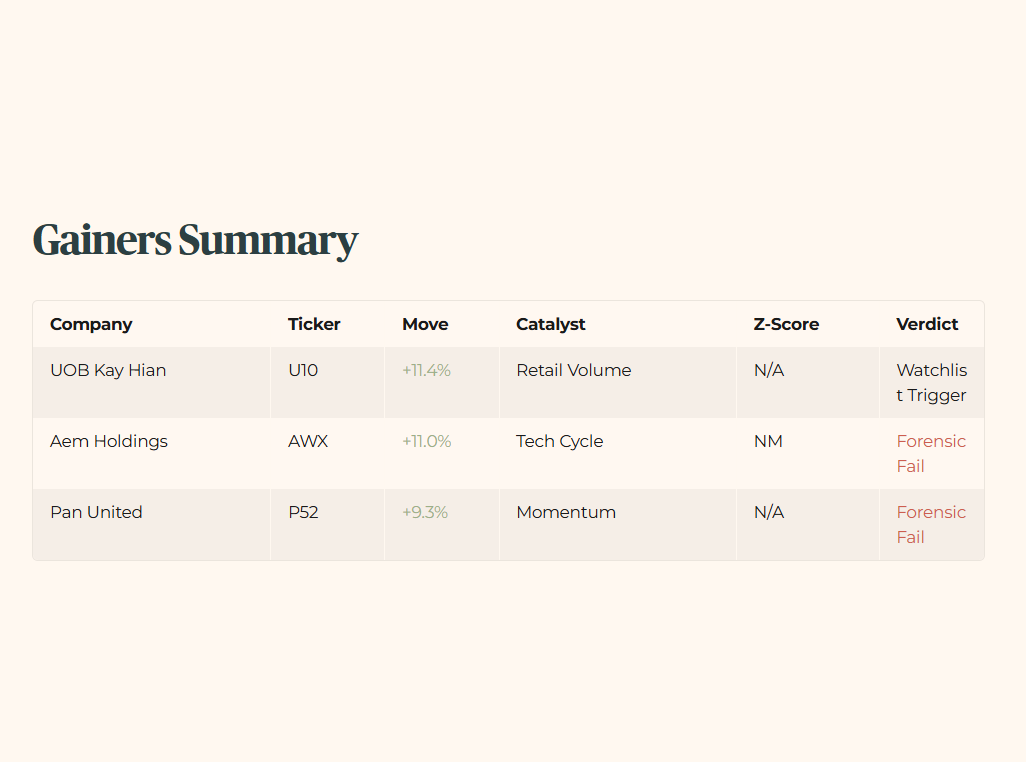

Aem Holdings Ltd (SGX:AWX) [as-of Mar27 close]

The Fake Winner

Raw Fact: AWX surged an impressive 11.0% this week, driven primarily by a narrative celebrating a resurgence in the global semiconductor cycle.

Benchmark: Historically, this counter relies on tech upswings, but its current P/E of 41.46 is heavily bloated, and its InvestingPro Fair Value is flagged as “Not Meaningful.”

Peer Context: Compared to broader manufacturing peers on the SGX, AWX is priced for flawless execution while offering a microscopic 0.3% dividend yield.

Forward Scenario: If the macro environment shifts against tech demand, this high-beta play offers zero sanctuary, failing our baseline 3.2% forensic floor.

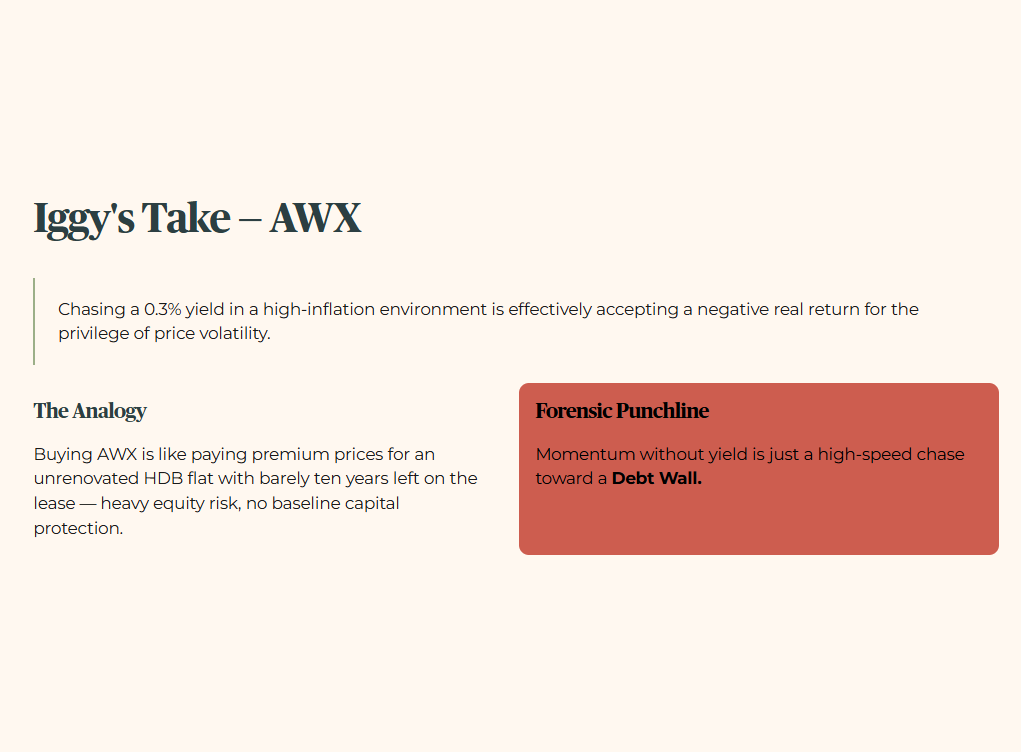

Wallet Impact: Buying AWX right now is like paying premium prices for an unrenovated HDB flat with barely ten years left on the lease; it represents heavy equity risk with no baseline capital protection.

Iggy’s Take: > While the momentum is visible, the forensic reality is stark. Chasing a 0.3% yield in a high-inflation environment is effectively accepting a negative real return for the privilege of price volatility. For the retail investor, this counter bypasses every safety pillar in our framework, offering neither the safety of the 3.2% floor nor the 4.7% minimum hurdle. You are gambling on the “greater fool” theory rather than underlying cash flows.

Forensic Punchline: Momentum without yield is just a high-speed chase toward a Debt Wall.

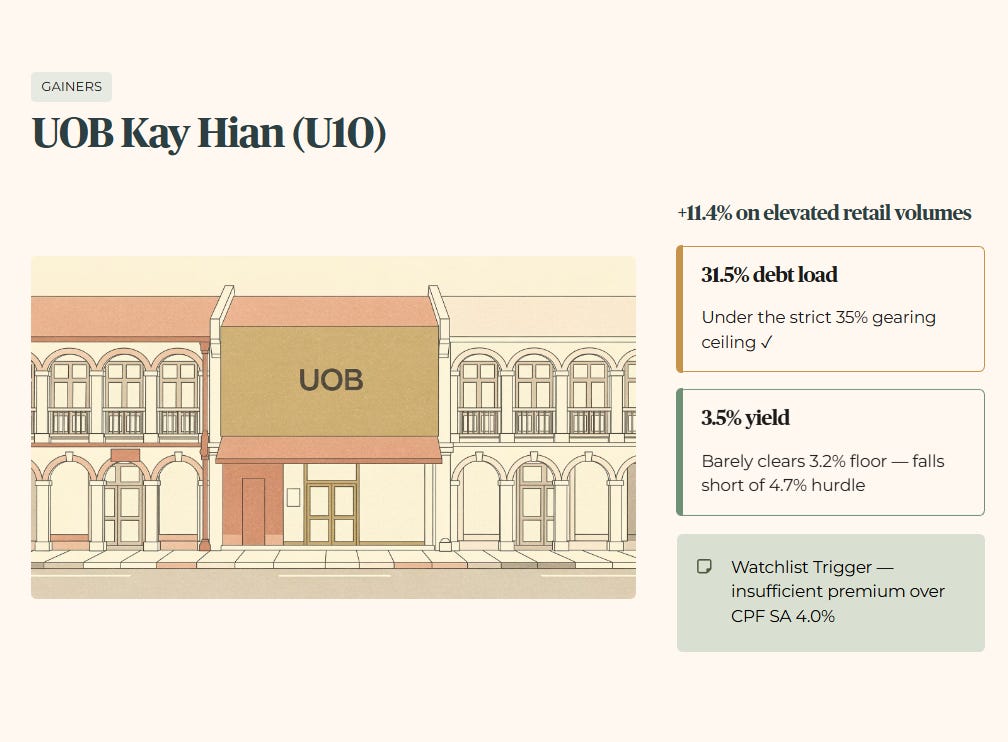

UOB Kay Hian Holdings Ltd (SGX:U10) [as-of Mar27 close]

U10 jumped 11.4% on elevated retail volumes, carrying a 31.5% debt load that stays under our strict 35% gearing ceiling. However, its 3.5% yield barely clears the 3.2% floor and falls short of the 4.7% absolute minimum yield hurdle. It lacks a true margin of safety. This represents a Watchlist Trigger for market participation, but it does not provide enough premium yield to justify aggressive allocation over risk-free alternatives like the CPF SA 4.0% benchmark.

Pan United Corporation Ltd (SGX:P52) [as-of Mar27 close]

P52 rode a 9.3% speculative wave driven by sector momentum, with a 0.0% dividend yield. Forensically, this is pure high-beta momentum chasing that bypasses sanctuary logic. Having no yield means you have zero downside protection when the market music stops, turning hard-earned capital into a high-wire speculative bet.

While most investors fixate on this week’s “winners”, the top 1% quietly harvest their biggest gains from the bloodied “losers” — and the next section shows you exactly which forensic gaps I am stalking.