Should Singaporean Investors Buy AMD Stock Now? The AI Chip Revolution Meets Market Reality

Balancing Hype and Fundamentals in AMD’s Global Growth Story for Singaporean Investors

The semiconductor world changed dramatically in 2024. Advanced Micro Devices emerged as both a winner and a warning sign within the artificial intelligence boom. The company’s partnership with OpenAI, announced just days ago, sent shares soaring over 25% in a single week. But beneath this excitement lies a more complex investment story that demands careful analysis, especially for Singaporean investors trading US stocks through their brokerage accounts.

AMD delivered record annual revenue of US$25.8 billion in 2024, representing 14% year-over-year growth. This surge came primarily from explosive demand in its Data Center segment, which nearly doubled to contribute almost half of total revenue. The company successfully launched a multi-billion-dollar Data Center AI initiative that generated over US$5 billion in revenue. This positions AMD as a legitimate challenger to Nvidia’s dominance in the AI accelerator market. However, this impressive top-line growth masks underlying challenges that complicate the investment thesis for investors in Singapore looking to add US tech stocks to their portfolios.

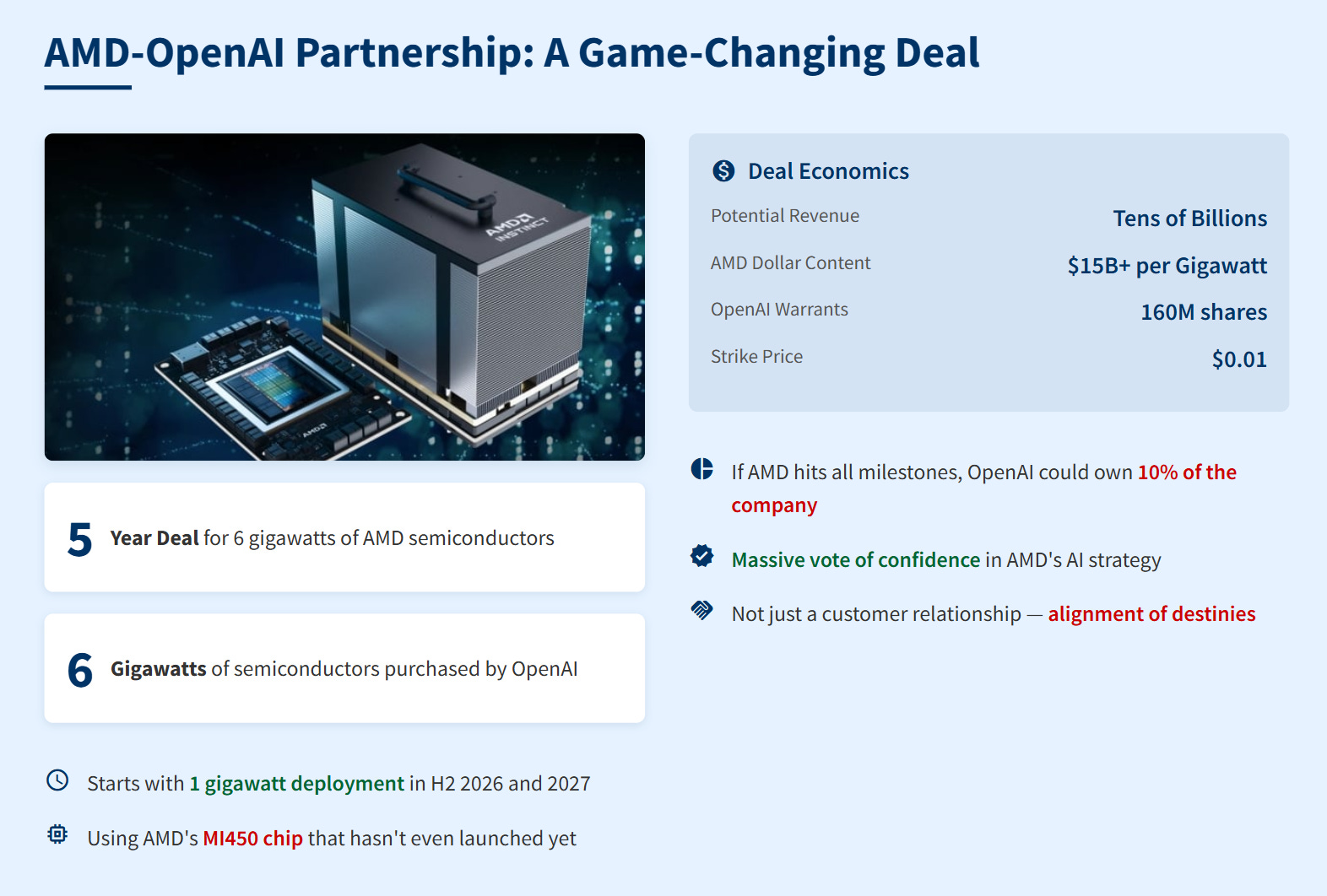

The OpenAI Partnership: Game-Changer or Market Mirage?

The recent OpenAI announcement represents the most significant validation of AMD’s AI strategy to date. Under the five-year agreement, OpenAI will purchase 6 gigawatts of AMD’s semiconductors. Deployment begins with the MI450 chip launching in 2026. This partnership could generate tens of billions of dollars in additional revenue for AMD over the next five years. Analysts estimate AMD’s dollar content at more than US$15 billion per gigawatt.

The deal structure includes performance-based warrants for up to 160 million AMD shares at a US$0.01 strike price. This effectively gives OpenAI a potential 10% stake in AMD if deployment milestones are met. Think of it like a major customer getting skin in the game, similar to how a Singapore REITs sponsor commits to units to align interests. This arrangement demonstrates OpenAI’s confidence in AMD’s technology while aligning incentives for successful execution.

For Singaporean investors accessing US markets through platforms like Moomoo or Tiger Brokers, this validation matters. Singapore investors increasingly allocate up to 75% of their portfolios to US markets, seeking higher growth potential than what SGX can offer. AMD now represents one of the key AI infrastructure plays alongside Nvidia in this global technology transformation.

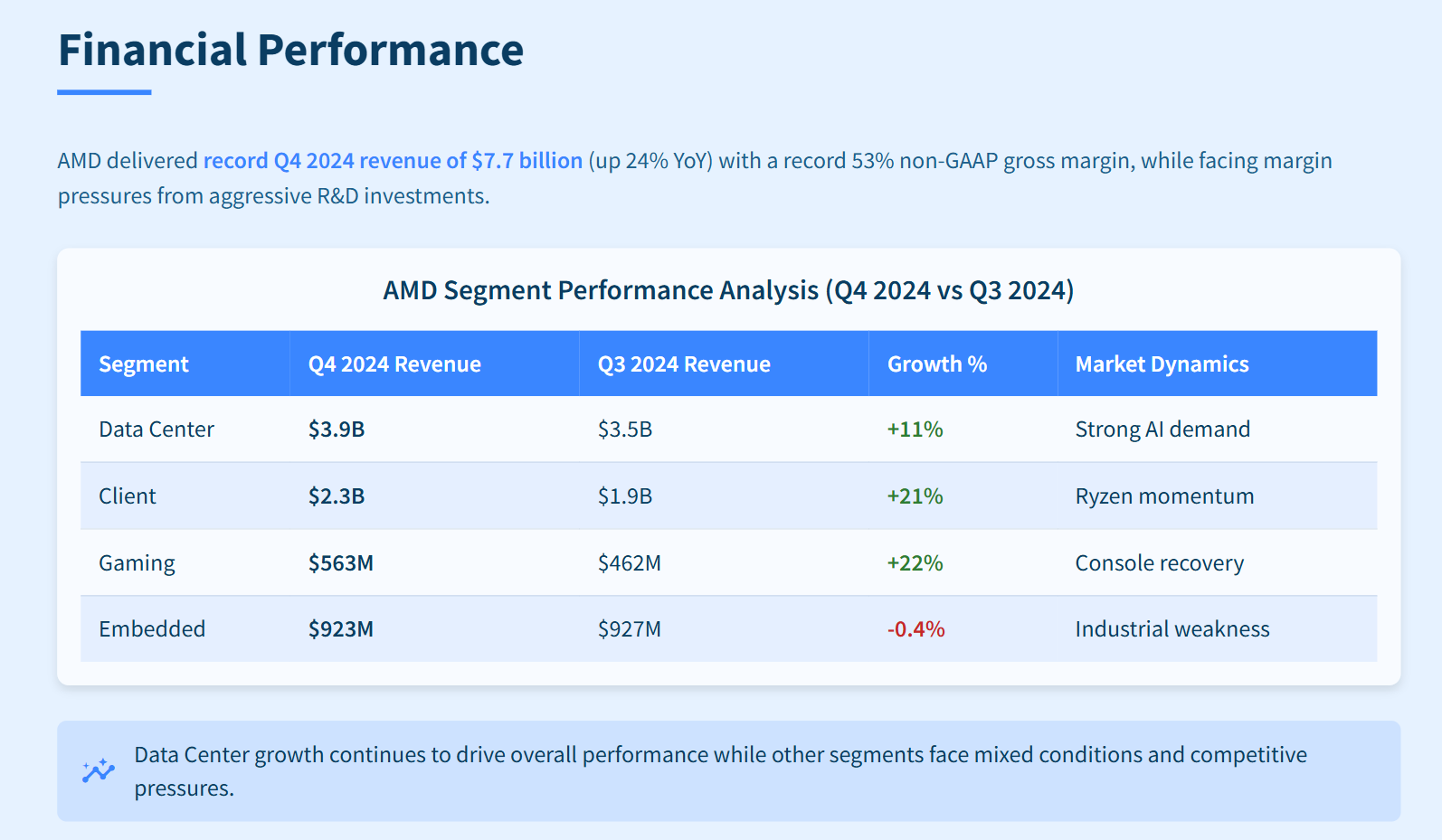

Financial Performance: Strong Growth Amid Margin Pressures

AMD’s recent financial performance reveals both opportunities and challenges facing the company. Fourth-quarter 2024 revenue reached a record US$7.7 billion, up 24% year-over-year. Full-year gross margin hit a record 53% on a non-GAAP basis. The Data Center segment’s remarkable 94% growth to US$3.9 billion highlighted AMD’s success in capturing AI infrastructure demand.

Yet beneath these impressive headlines, margin pressures and competitive dynamics create concern. The company’s fourth-quarter net income declined to US$482 million from US$667 million the previous year. This drop primarily came from a 17% increase in operating expenses driven by aggressive research and development investments in AI. This investment is necessary for long-term competitiveness but pressures near-term profitability. For Singaporean investors watching their portfolio returns in Singapore dollars, currency fluctuations add another layer of consideration when evaluating these earnings.

Think of it like this: AMD is spending heavily to compete, similar to how Grab had to invest aggressively to dominate Southeast Asia’s ride-hailing market. The question is whether these investments will pay off before the company burns through too much cash or loses competitive positioning. For investors in Singapore used to evaluating SGX stocks like Sea Limited or Grab Holdings that also prioritized growth over near-term profitability, this dynamic should feel familiar.

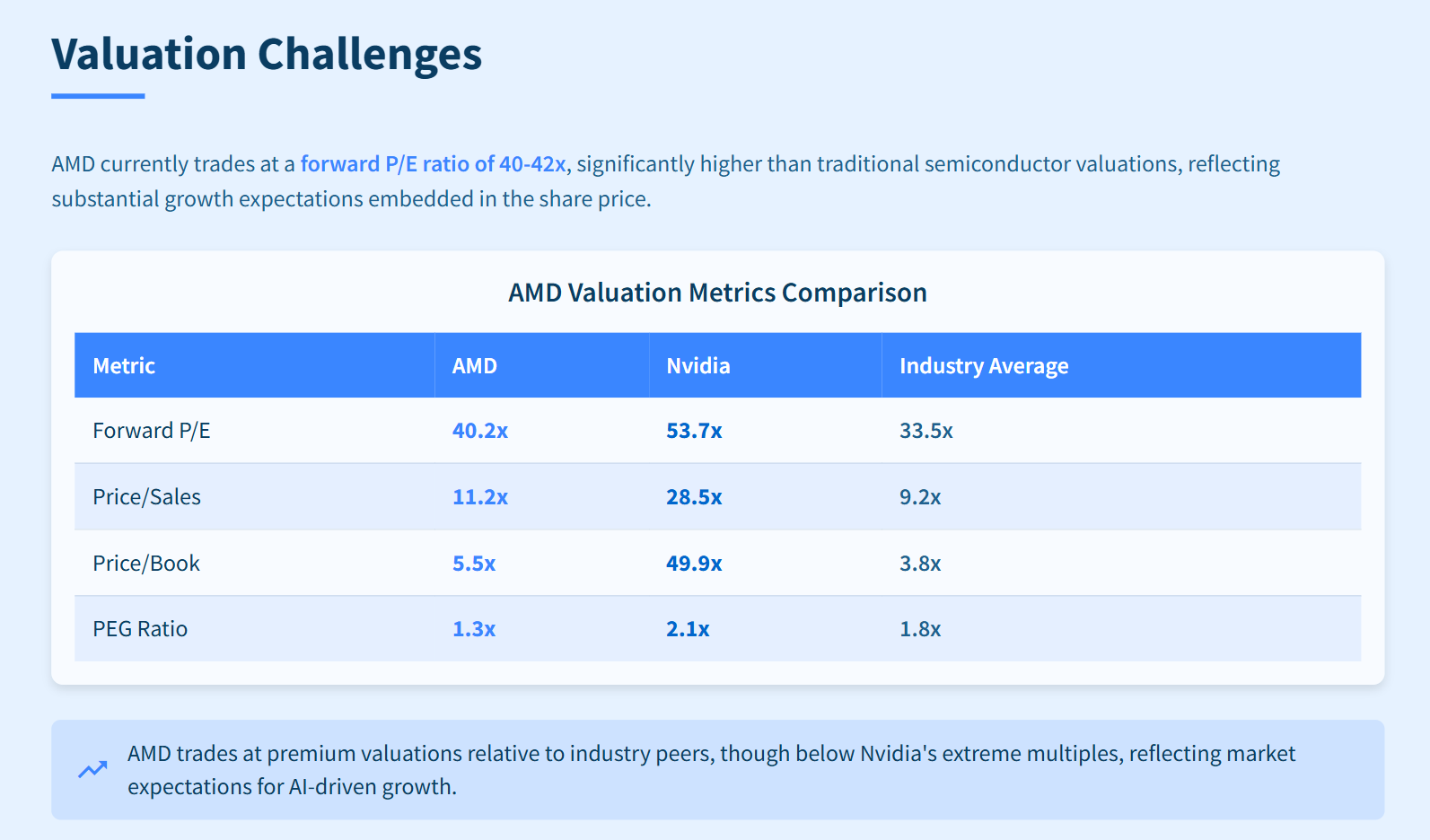

Valuation Challenges: Premium Pricing Meets Execution Risk

AMD currently trades at a forward price-to-earnings ratio of approximately 40-42 times. This is significantly higher than traditional semiconductor valuations. It reflects substantial growth expectations embedded in the share price. This premium valuation demands flawless execution across multiple business segments and successful market share capture from Nvidia.

The company’s current market capitalization of approximately US$330 billion represents a significant premium to historical metrics. Analysts’ price targets range from US$140 to US$300. This wide dispersion reflects uncertainty about AMD’s ability to capitalize on AI opportunities while defending existing market positions. For Singaporean investors converting Singapore dollars to US dollars for investment, the exchange rate currently sits around 1.36 SGD per USD, making this a roughly S$450 billion company in local currency terms.

To put this in perspective, AMD’s market cap exceeds the entire market capitalization of several major Singapore-listed companies combined. The Singapore Exchange’s total market cap was approximately US$650 billion, meaning AMD alone represents half the value of Singapore’s entire stock market. This scale illustrates why Singapore investors increasingly look beyond SGX for growth opportunities.

Competitive Landscape: The Nvidia Challenge

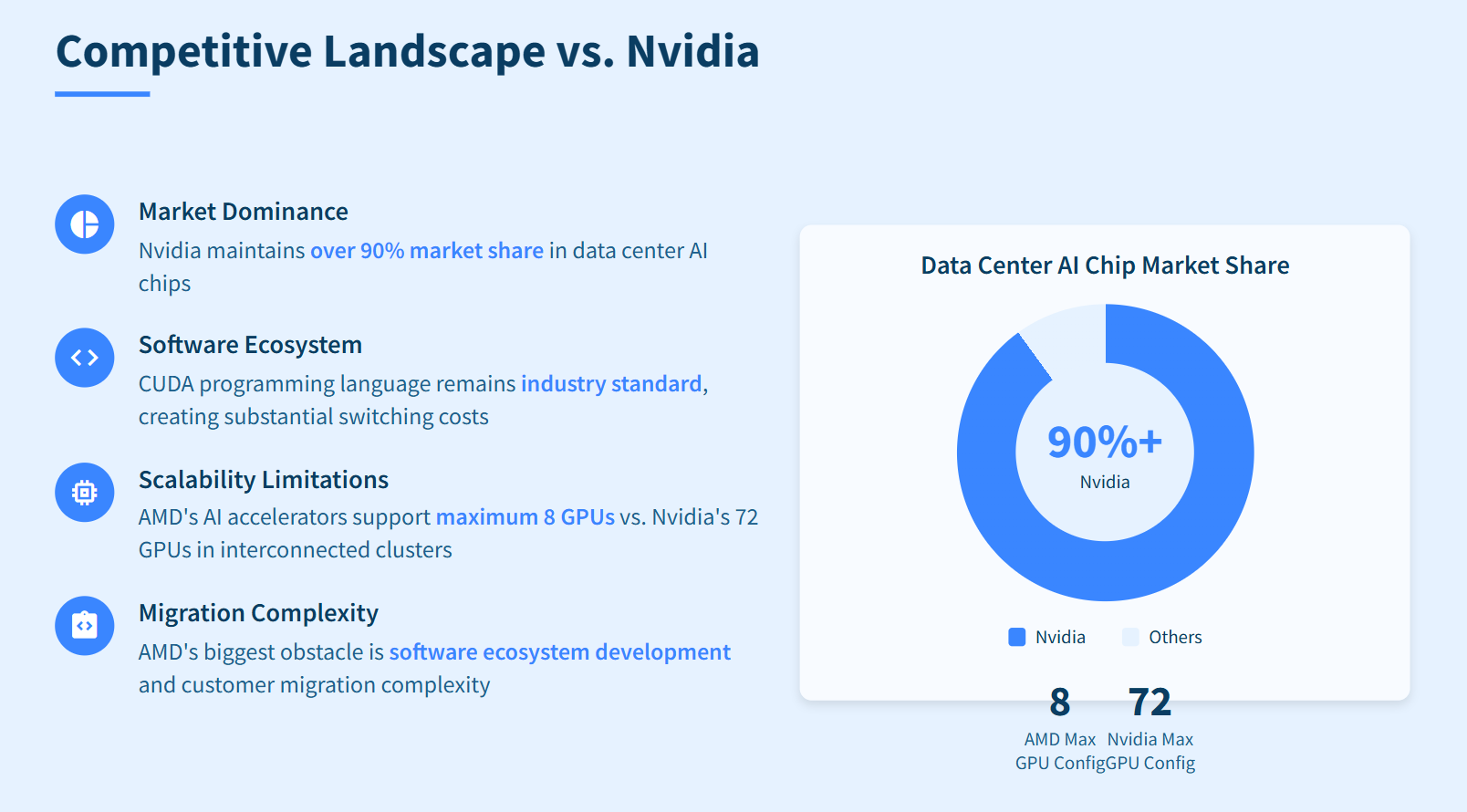

While AMD has made significant strides in AI accelerators, Nvidia maintains overwhelming market dominance with over 90% market share in data center AI chips. Nvidia’s CUDA programming language remains the industry standard. This creates substantial switching costs for customers considering AMD alternatives. AMD’s biggest obstacle lies not in hardware performance but in software ecosystem development and customer migration complexity.

Recent product launches, including the MI325X accelerator, demonstrate AMD’s technical capabilities but face scalability limitations. Industry analysts note that AMD’s current AI accelerators support maximum configurations of eight GPUs. In contrast, Nvidia’s ability scales to 72 GPUs in interconnected clusters. This limitation constrains AMD’s addressable market for large-scale AI training applications.

For context, Singapore itself has emerged as an AI powerhouse in Southeast Asia, with the government committing over S$1.6 billion in AI funding. Singapore generates 15% of Nvidia’s global revenue, making it Nvidia’s fourth-largest market worldwide despite having just 5.9 million residents. This remarkable concentration of AI infrastructure spending in Singapore translates to S$600 per capita on Nvidia chips alone. Understanding this local context helps Singaporean investors appreciate why Nvidia’s ecosystem advantage matters so much in the competitive landscape.

Investment Risks and Opportunities

The investment case for AMD centers on the company’s ability to capture meaningful market share in the expanding AI accelerator market. At the same time, it must defend positions in traditional CPU markets. The OpenAI partnership provides unprecedented validation and revenue visibility. Yet execution risks remain substantial, particularly for Singaporean investors who must also consider currency risk when holding US stocks.

Export restrictions targeting China represent another significant risk. AMD potentially faces US$1.5 billion in revenue losses during 2025 due to limitations on advanced chip sales to Chinese customers. This regulatory overhang creates additional uncertainty around growth projections and market access. For Singapore investors who understand geopolitical tensions given our position between major powers, this risk should resonate as very real and material.

The AI accelerator market could reach US$500 billion by 2028, creating massive opportunity. However, Nvidia’s entrenched software advantage, scalability limitations in current AMD products, and margin pressure from R&D investments all present challenges. For Singaporean investors, these factors must be weighed against the potential rewards of gaining exposure to the AI revolution through AMD’s stock.

The Verdict: Cautious Optimism Amid Premium Pricing