Singapore Airlines FY25/26: The Profit Collapse Behind the Record Revenue

A full forensic audit of SIA's 57.4% net profit drop, the Air India accounting drag, and what the lagged jet fuel cost means for your dividend in FY26/27.

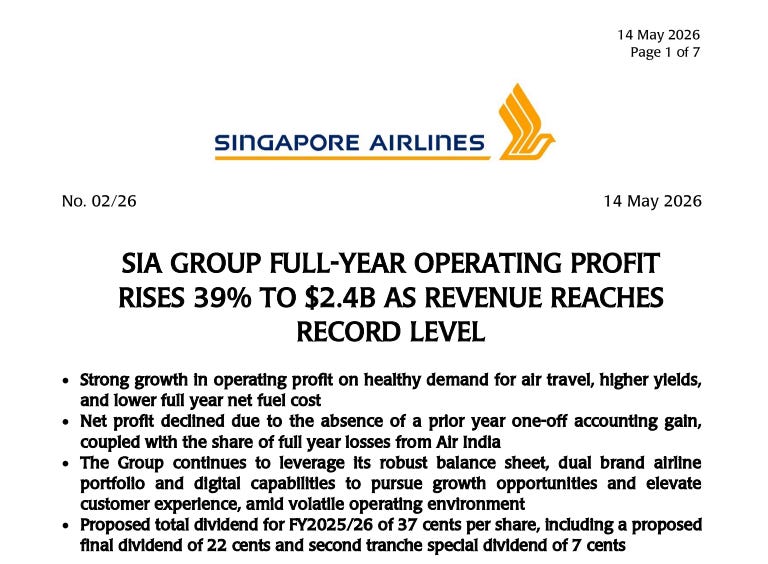

Net profit plunged 57.4 percent year-on-year to SGD 1,184 million. Yet the earnings presentation headlines shouted about record revenue and a 39 percent rise in operating profit. For a Singaporean retiree relying on these dividends, that profit collapse translates to a painful 22.9 percent income cut — wiping out nearly S$877 annually on a S$50,000 holding.

Before we get into the numbers, a quick word for anyone joining us for the first time. In Episode 1600 — our pre-earnings Iggy Answers session — we flagged Singapore Airlines as a Watchlist name, not a conviction buy. We said wait for May 14 before deciding. The results are now in, and today we do what we promised: the full forensic audit.

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips — the interest coverage, the gearing, the free cash flow sustainability — so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

Here is the rigorous forensic audit exposing the hidden lag in jet fuel costs and the structural drag of Air India. The glossy management slide deck attempted to contextualise these away.

In This Article:

The Slide-by-Slide Audit

The Reality Check

The Scorecard and Yield Spread

How Iggy Rates Every Stock

The Forward Outlook

Forensic Verdict

Iggy’s Forensic Disclaimer

2. The Slide-by-Slide Audit

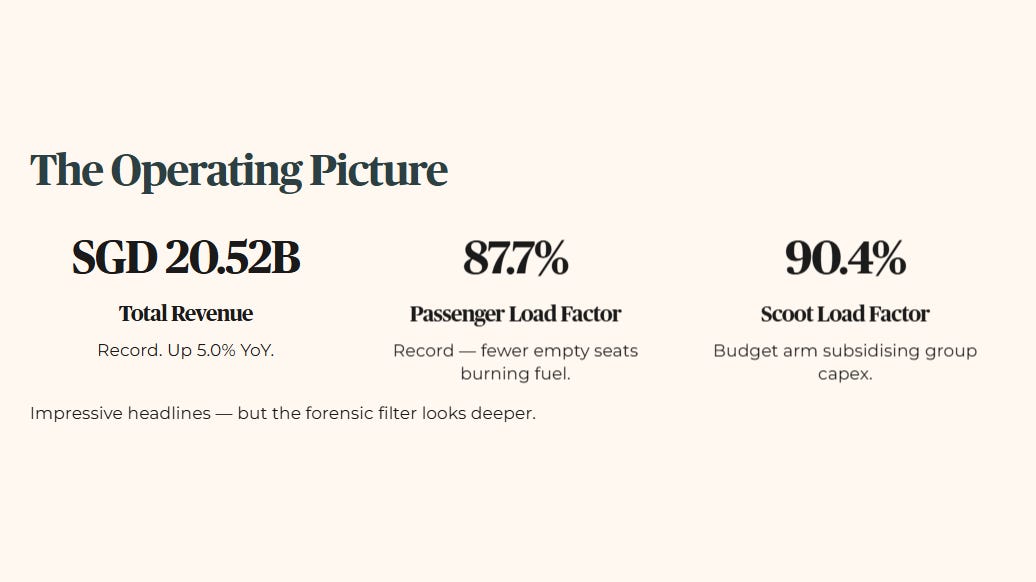

When evaluating an airline like Singapore Airlines, the heartland investor must separate the operating illusion from the statutory reality. Management led their presentation with a record total revenue of SGD 20.52 billion and an operating profit of SGD 2.4 billion. These are impressive headline figures. However, my forensic filter prioritises the metrics most directly linked to distribution sustainability. For industrial and passenger airline assets, we lead with revenue and operating margin.

Total revenue reached SGD 20.52 billion, a 5.0 percent increase year-on-year. For a 55-year-old investor holding this counter for dividend stability, this top-line growth provides a temporary cushion against inflationary pressures on household expenses.

Group Passenger Load Factor — the percentage of available seating capacity actually filled with paying passengers — hit a record 87.7 percent. High utilisation means fewer empty seats burning expensive jet fuel. That directly supports the cash flow needed to fund your semi-annual dividend payouts. Scoot’s Passenger Load Factor came in at an even higher 90.4 percent. This budget airline performance helps subsidise the broader group capital expenditure, protecting the parent company dividend pool from being entirely drained by fleet renewal costs.

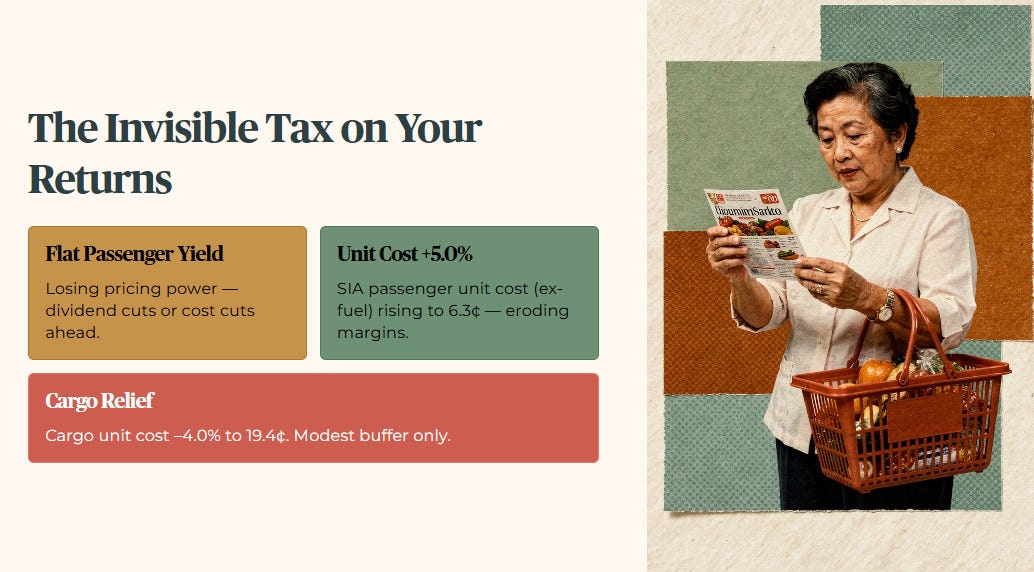

Passenger yield — the average revenue earned per passenger flown one kilometre — was relatively flat. Flat yields mean the airline is losing pricing power. That will eventually force management to cut costs or reduce dividend payouts to maintain their cash buffer.

SIA Passenger Unit Cost excluding fuel rose by 5.0 percent to 6.3 cents. This creeping operational cost acts like an invisible tax on your investment returns, steadily eroding the profit margins that support your passive income. Cargo Unit Cost decreased by 4.0 percent to 19.4 cents, providing slight margin relief and modestly improving the defensive posture of the stock during periods of volatile passenger demand.

Value Added per Employee dropped 15.1 percent to SGD 290,561. This sharp drop in productivity efficiency warns us that headcount costs are rising faster than actual value creation — a threat to the long-term sustainability of the 37-cent dividend.

On balance sheet housekeeping: all SGD 850 million of convertible bonds issued in December 2020 were fully converted by November 2025. This permanent alteration of the dilution profile means your share of the earnings pie will not be unexpectedly shrunk by sudden bond conversions, offering clearer visibility for retirement income planning.

🦎 Iggy’s Insight: The metric management spent the least time on

Management briefly noted that jet fuel is typically priced on a lagged basis, practically whispering that the higher fuel price environment arising from Middle Eastern conflicts was only partially reflected in the March 2026 net fuel cost. This silence is deafening. It means the current profit margins are artificially inflated by outdated, cheaper fuel hedges. When the full impact of geopolitical fuel spikes feeds into the FY2026/27 accounts, the operating margin will compress violently. Ignoring this lag is a luxury forensic investors cannot afford. The headline operating profit is not the operating profit of the year ahead — it is the operating profit of the fuel contracts signed eighteen months ago.

3. The Reality Check

The narrative pushed by management paints a picture of unstoppable travel demand and record operational efficiency. The InvestingPro fair value model tells a more textured story.

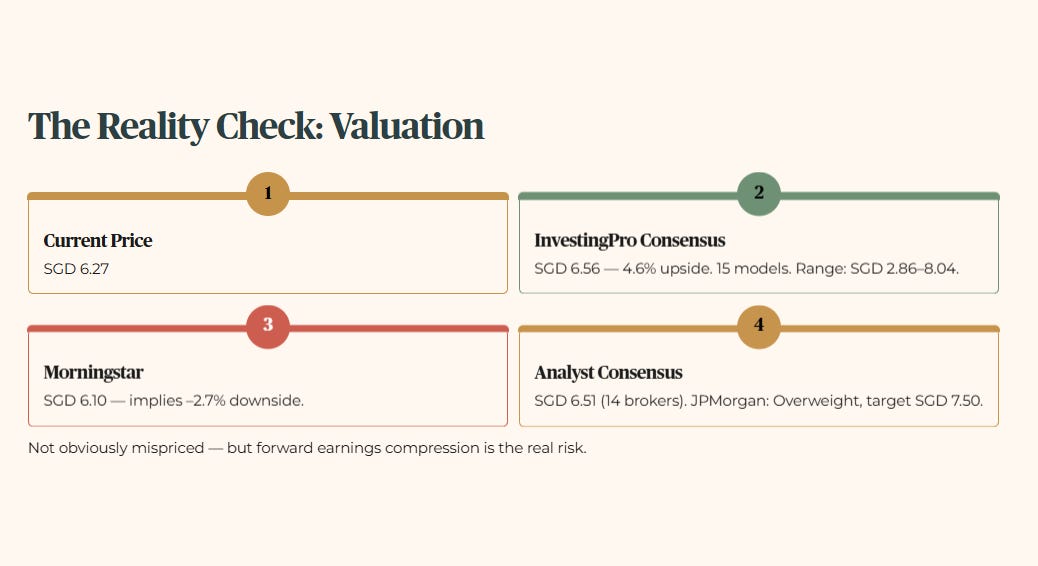

The stock currently trades at SGD 6.27. InvestingPro’s consensus model — spanning fifteen independent valuation models — arrives at an average fair value of SGD 6.56, implying 4.6 percent upside from here with low uncertainty. On that basis, the stock is modestly undervalued, not expensive.

But here is the forensic discipline that matters. The InvestingPro consensus represents the central estimate across a wide range — the full spread runs from SGD 2.86 to SGD 8.04. At the more conservative end, Morningstar’s independent model sets a fair value of SGD 6.10, implying a small downside of 2.7 percent from current price. The analyst consensus of fourteen brokers sits at SGD 6.51, with JPMorgan maintaining an Overweight rating and a SGD 7.50 target as of May 14.

The forensic read is this: the stock is not obviously mispriced in either direction. The upside is real but modest. The downside scenario is equally real and driven by something concrete — forward earnings compression.

Here is the five-layer breakdown.

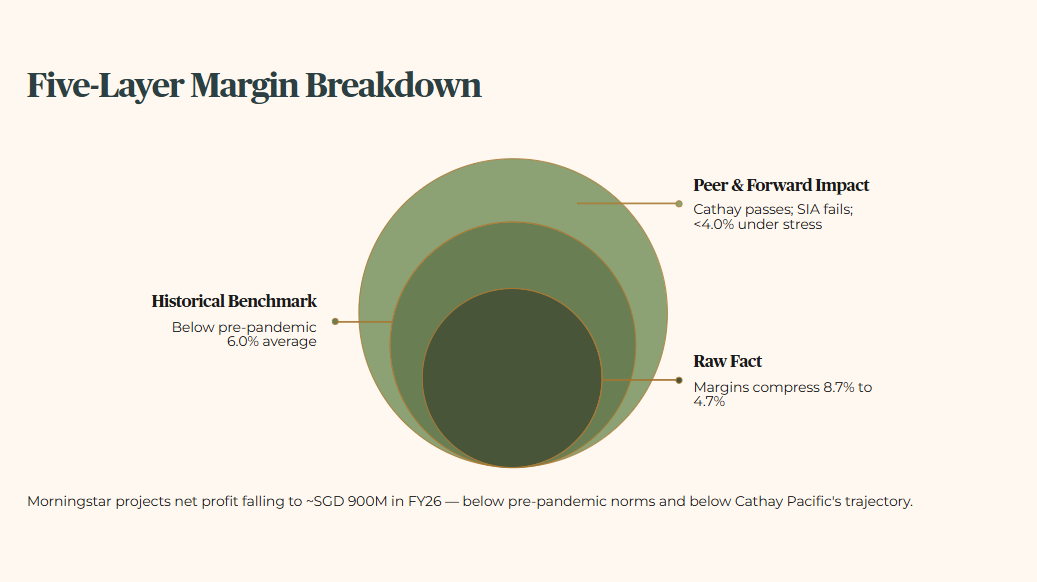

First, the raw fact. Morningstar projects operating margins to compress from 8.7 percent in FY25 to 4.7 percent in FY26, with net profit falling to approximately SGD 900 million.

Second, the historical benchmark. Over the past five years, Singapore Airlines has occasionally enjoyed double-digit margins during capacity crunches. A return to 4.7 percent falls below their pre-pandemic historical average of around 6.0 percent.

Third, peer context. Cathay Pacific is currently expanding its attributable profit to HKD 10.8 billion and managing operating margins without the 57.4 percent statutory net profit contraction we see here. Cathay Pacific passes the margin sustainability test. Singapore Airlines is failing it on a forward basis.

Fourth, the forward scenario. A negative 10 percent stress applied to current passenger yields — driven by aggressive regional capacity dumping from Chinese carriers — would compress operating margins below 4.0 percent, restricting free cash flow and likely forcing a reduction in the absolute dividend payout by at least 150 basis points.

Fifth, the wallet impact. Think of it like buying a resale HDB flat. You might pay a premium because the flat has fresh paint and looks beautiful today. But if you know the lift requires a major upgrade next year that you will have to co-fund, the true value is lower than the asking price. The market is paying for the fresh paint of FY2025/26 record revenue. The forensic investor is pricing in the upcoming lift upgrade of FY2026/27 fuel costs and margin compression.

The forensic gap here is not price versus value. It is earnings quality versus headline yield. The yield looks safe today. The question is whether the cash flow can sustain it when the lagged fuel costs arrive in full.

4. The Scorecard and Yield Spread

We do not accept raw yields at face value. We calculate the true risk premium to confirm the investor is being adequately compensated for holding equity risk.

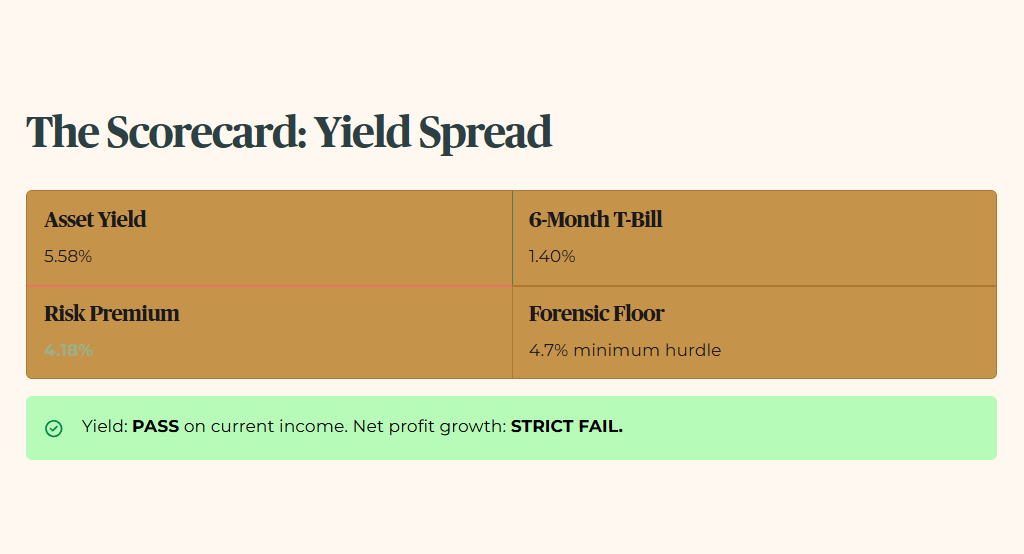

Asset Yield: 5.58 percent (LB verified, May 2026, replacing original 5.90 percent). Singapore 6-Month T-Bill cut-off rate: 1.40 percent. Risk Premium: 4.18 percent.

A note on the Stress-Test Buffer: I apply a conservative floor of 3.2 percent regardless of where the T-Bill sits. The minimum yield hurdle — my 3.2 percent forensic floor plus 150 basis points of mandatory risk premium — is 4.7 percent. While the T-Bill sits at 1.40 percent today, I do not lower my standards to match a temporary market dip. I audit for the storm, not just the sunny day.

The forensic verdict on income sustainability: pass on current yield, strict fail on net profit growth. The asset clears the 4.7 percent minimum yield hurdle comfortably.

Table 1 — Income Sustainability

Source: InvestingPro, with LongBridge verification, May 2026.

How Iggy Rates Every Stock

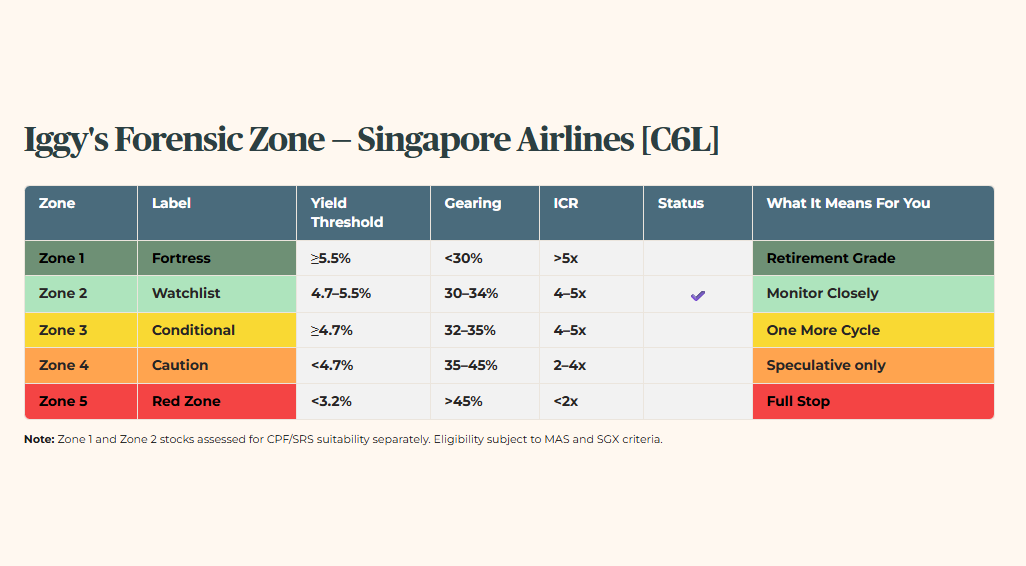

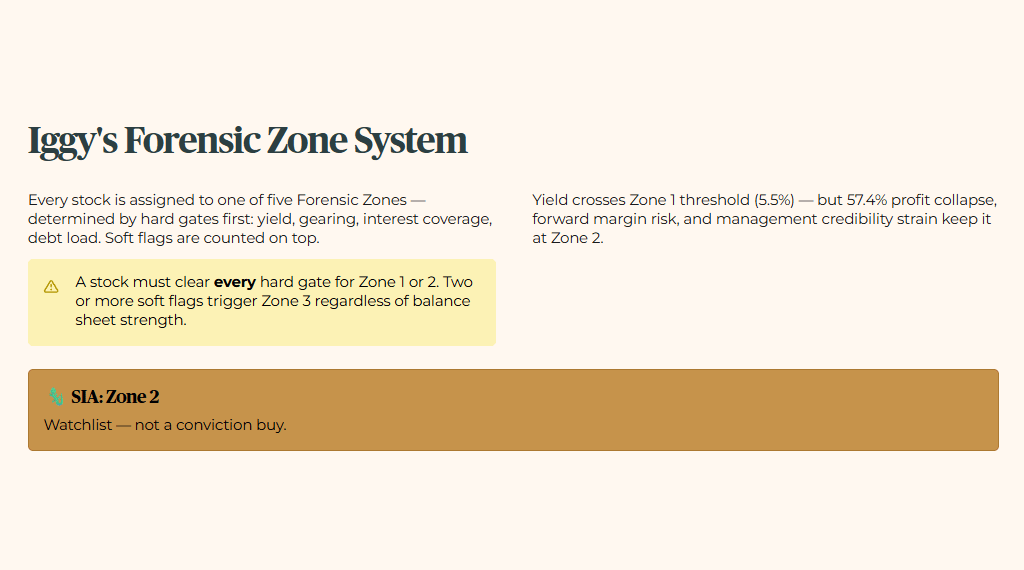

Every stock I cover is assigned to one of five Forensic Zones. The zones are determined by hard gates — yield, gearing (the proportion of assets funded by debt), interest coverage, and debt load — assessed first. Soft flags are then counted on top. A stock must clear every hard gate to qualify for Zone 1 or Zone 2. Two or more soft flags trigger Zone 3 regardless of how strong the balance sheet looks. The full rationale for Singapore Airlines’ zone assignment is available to Iggy’s Elite Investors below.

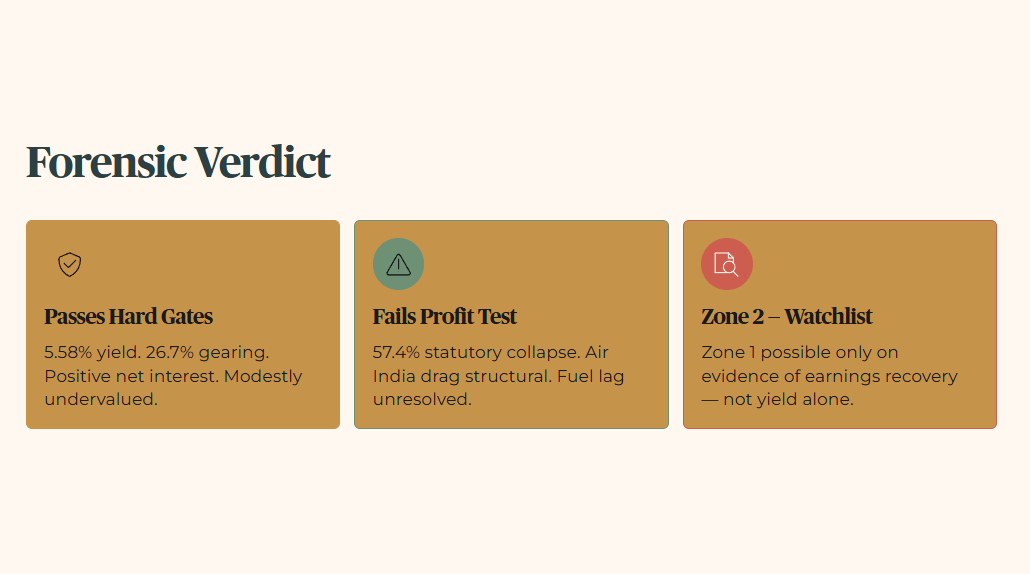

Iggy’s Forensic Zone: Zone 2 — Watchlist.

Note: At 5.58 percent, Singapore Airlines’ yield technically crosses the Zone 1 yield threshold of 5.5 percent. The Zone 2 conservative hold is deliberate, driven by the 57.4 percent statutory net profit collapse, forward margin compression risk, and management credibility strain documented in this audit. Zone 1 remains possible — but only on evidence of earnings recovery, not on yield alone.

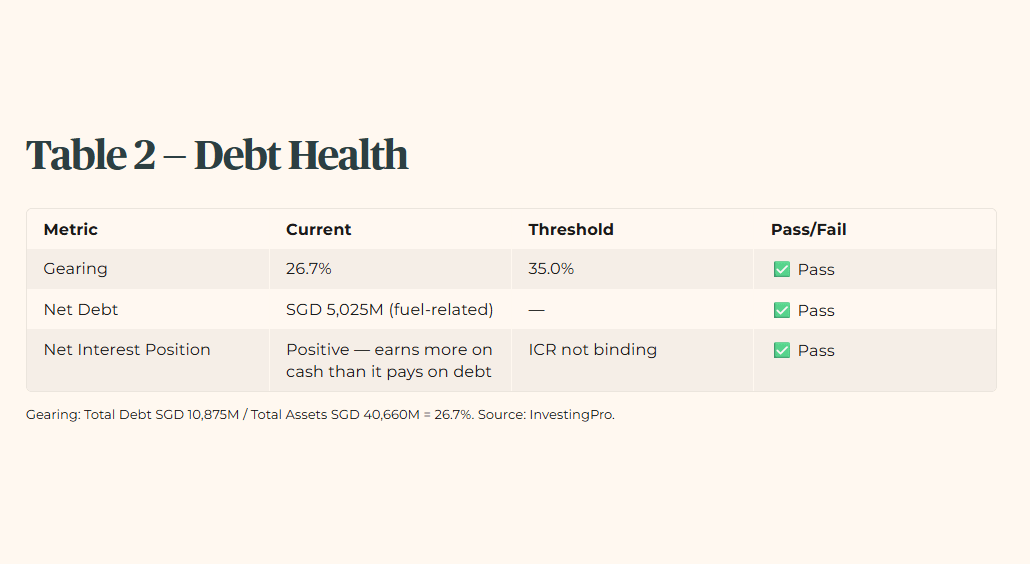

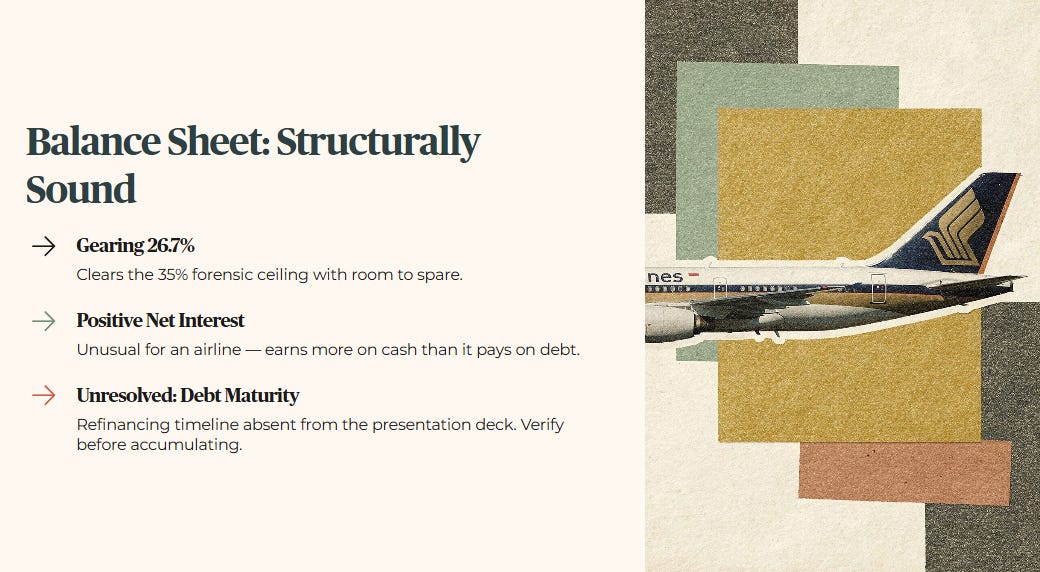

The forensic verdict on debt health is that the company operates from a position of financial strength on leverage.

Table 2 — Debt Health

Gearing calculated from InvestingPro balance sheet: Total Debt SGD 10,875M / Total Assets SGD 40,660M = 26.7%. Net interest position confirmed positive per InvestingPro income statement. Debt maturity and refinancing schedules absent from presentation deck.

The gearing ratio of 26.7 percent clears the 35 percent forensic ceiling with room to spare. The net interest position is positive — Singapore Airlines earns more on its substantial cash holdings than it pays on its debt obligations. This is an unusual and structurally sound position for an airline. The interest coverage ratio as a conventional constraint does not apply here.

What remains genuinely unresolved is the debt maturity schedule. The exact refinancing timeline was absent from the presentation deck and warrants verification ahead of any accumulation decision.

You Shouldn’t Be Reading This Alone

One Community. One Forensic Lens. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. While free subscribers are reading yesterday’s story, Iggy’s Elite Investors are already cross-checking the next setup — together, in real time.

Iggy’s Elite Investors don’t just get the report earlier. They get the full forensic picture the moment it’s finalised — zero-day breakdowns, the complete “Red Zone” watchlist, and institutional-grade cheatsheets built around the same Five-Layer Audit you see here. The difference is they get it before the market opens, not after it has already moved.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

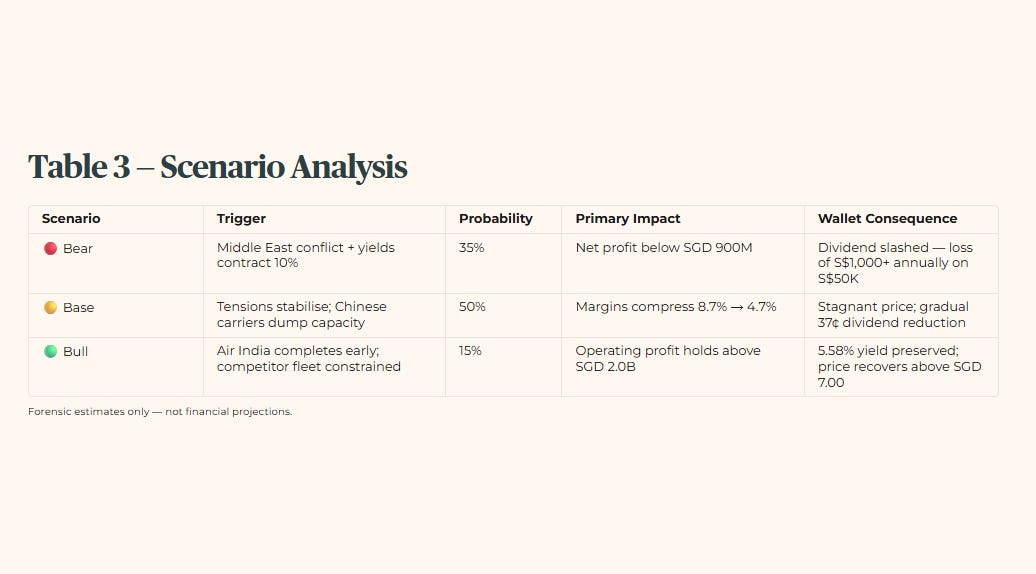

5. The Forward Outlook

Table 3 — Scenario Analysis

Scenario probabilities are forensic estimates, not financial projections. Verify against live market conditions before any investment decision.

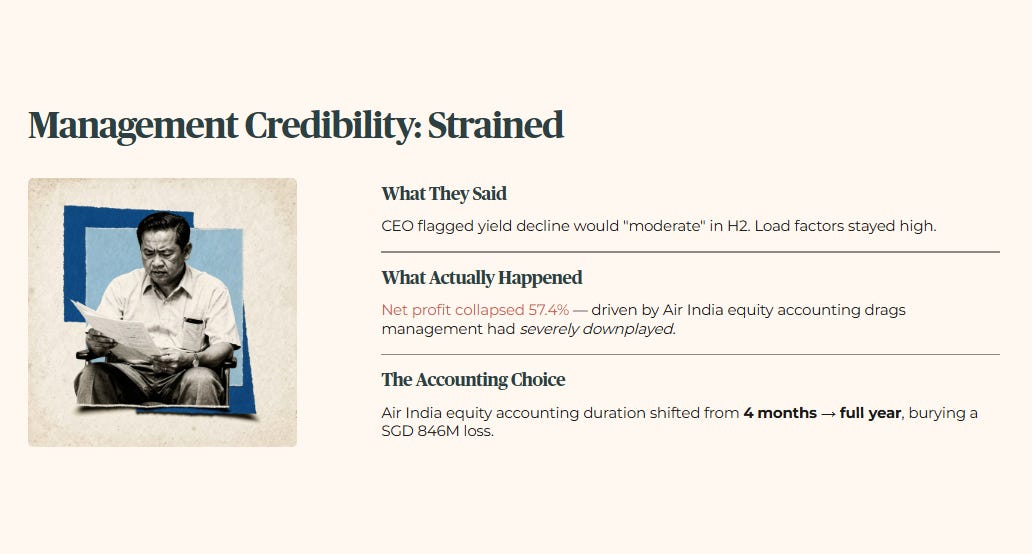

On management’s historical guidance accuracy: historically, management has been optimistic about capacity absorption. In a prior quarter, when queried about a sharp decline in Scoot yields, CEO Leslie Thng stated that the outlook for yield in the second half was good and they expected the rate of decline to moderate. The actual outcome shows that while passenger load factors remained high, statutory net profit collapsed due to structural equity accounting drags from Air India — drags management had severely downplayed in prior quarters.

Management’s shift of the Air India equity accounting duration from four months to a full year buried a SGD 846 million loss in structural integration costs. That accounting choice is documented. The forensic credibility of forward guidance has taken a hit.

🦎 Iggy’s Insight: When management changes the goalposts

The forensic verdict on management credibility is strained. Tone and optimism do not pay your grocery bills. The specific gap between what they projected regarding regional yield stability and what the FY2025/26 numbers actually show is troubling. They shifted the equity accounting duration for Air India from four months to a full year — burying a massive SGD 846 million loss in structural integration costs. This is not a one-off shock. It is an accounting choice that distorts the bottom line and compounds across reporting periods. When management changes the goalposts to explain away a 57.4 percent profit collapse, the forensic auditor stops listening to the narrative and starts aggressively discounting the fair value of forward earnings guidance.

6. Forensic Verdict

Iggy’s Forensic Zone: Zone 2 — Watchlist.

Forensic Stance: Watchlist Trigger.

The absolute yield of 5.58 percent passes the hard gates. The balance sheet is fundamentally robust — 26.7 percent gearing, net positive interest position, no near-term debt covenant pressure. On InvestingPro’s consensus valuation, the stock is modestly undervalued. These are not trivial positives.