Is SIA a 5.9% Yield Trap? The Truth Behind the $417M “Anchor” Loss 🦖 EP1269

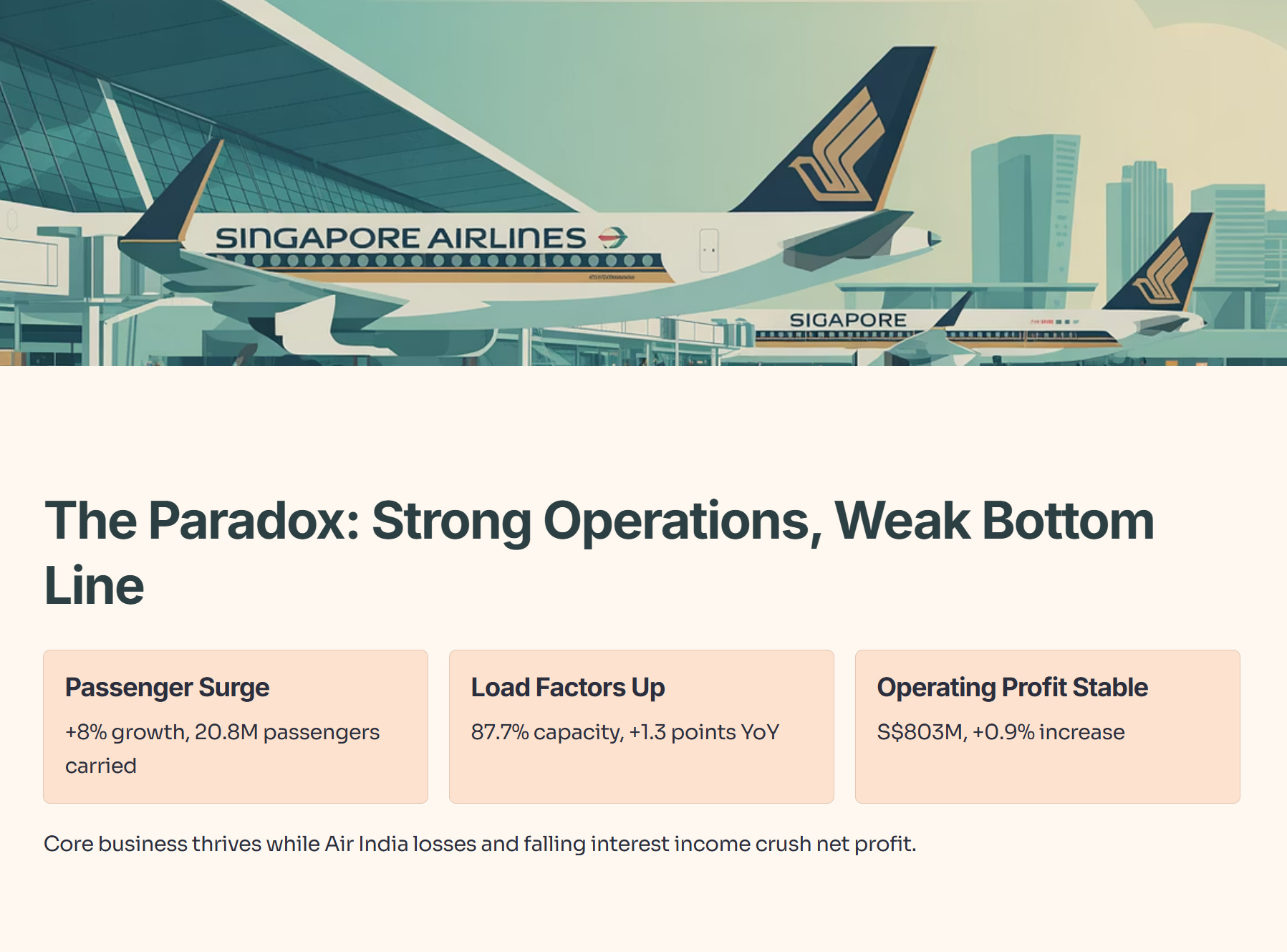

Singapore Airlines just released their half-year results for FY2025/26, and the headline is stark: Net profit has fallen off a cliff—down 68% to S$239 million.

While operating profit held steady at S$803 million, a massive S$417 million swing in losses from associated companies (primarily Air India) and falling interest income crushed the bottom line. Yet, beneath that ugly net profit number, the core business shows resilience: passenger numbers surged 8%, load factors climbed, and the company even announced a S$0.9 billion special dividend plan.

The big question for Singaporean investors: Is this a temporary blip or a structural problem? Should you hold for the 5.9% projected yield, or sell before the “Air India anchor” drags the stock lower?

This deep dive unpacks the official financial report to tell you exactly where SIA stands and whether it deserves a spot in your CPF or SRS portfolio.

Iggy: As always, I’ve not inserted screenshots of the results here. You can cross reference it by downloading it below. I hope this helps.

In This Article:

• The Tale of Two Airlines: Operational Strength vs. Bottom-Line Pain

• The S$417 Million Anchor: The Air India Problem

• The Income Angle: Is the 5.9% Yield Safe?

• Beneath the Wing: Yields are Dropping, Costs are Rising

• Balance Sheet & Outlook

• Iggy’s Assessment: Hold for Income, Watch the “Anchor”

1. The Tale of Two Airlines: Operational Strength vs. Bottom-Line Pain

If you only look at the top line, SIA looks like a champion. The Group reported record half-year revenue of S$9,675 million, up 1.9% year-on-year [Page 1].

Traffic is booming: The Group carried 20.8 million passengers (+8.0%) [Page 2].

Planes are full: Load factors jumped 1.3 percentage points to a very healthy 87.7% [Page 2].

Core business is stable: Operating profit (money made from actually flying planes) rose marginally by 0.9% to S$803 million [Page 1].

But here is the problem: While the “shop” is busy, the bank account is taking a hit. Net profit collapsed 67.8% to S$239 million [Page 1].

Iggy’s Take: Think of this like a hawker stall that has a queue every day (strong revenue/operations) but the owner is paying off a massive debt for a second failed stall next door (Air India/Associates). The main business is fine, but the side investment is dragging down the whole company.

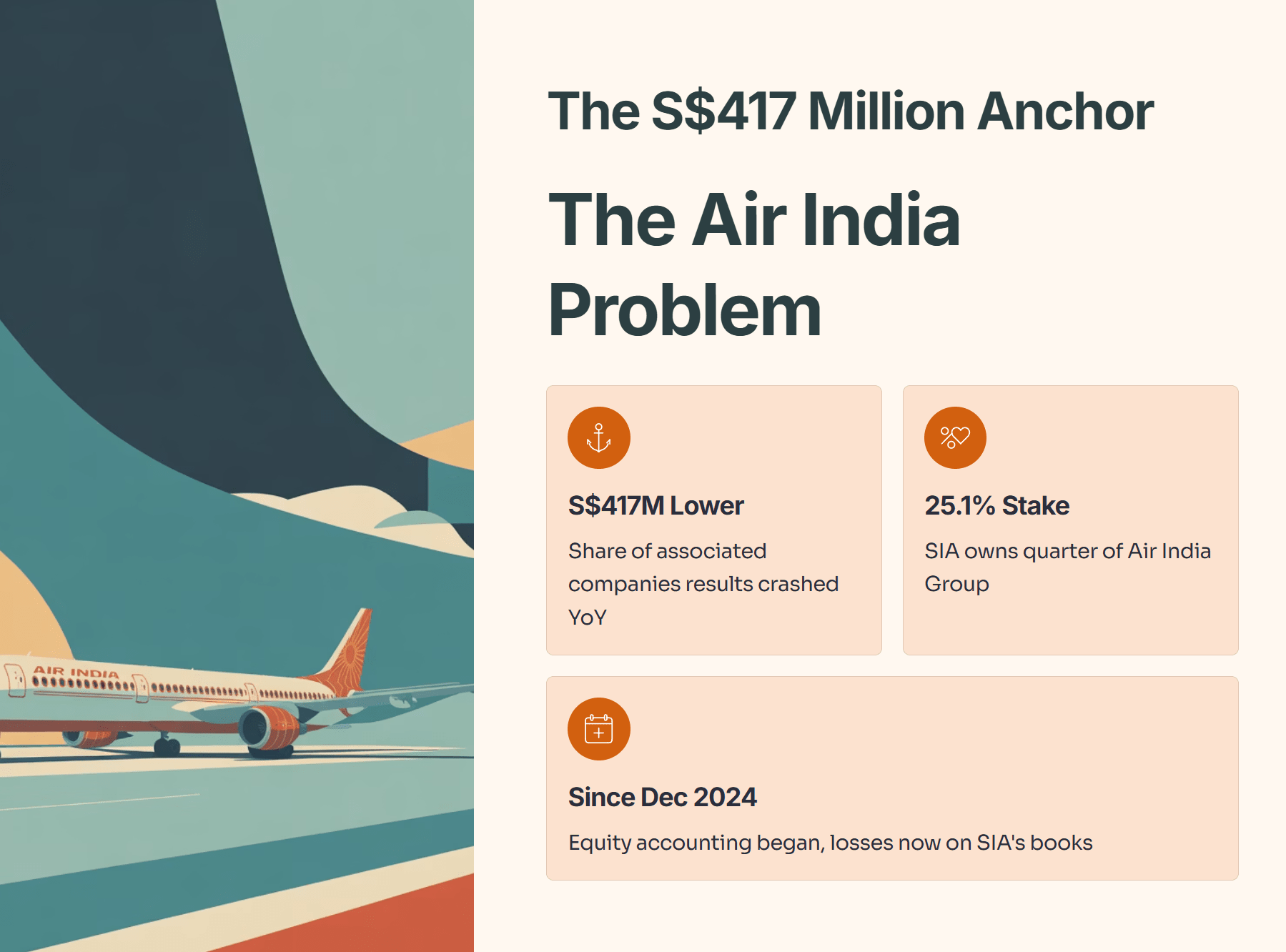

2. The S$417 Million Anchor: The Air India Problem

Here is the elephant in the cabin. The Group’s “share of results of associated companies” was S$417 million lower year-on-year [Page 2].

Why? Because SIA owns a 25.1% stake in the Air India Group [Page 4]. This was a strategic move to tap into the massive Indian aviation market, but right now, it is bleeding cash.

SIA began equity accounting for Air India’s performance starting December 2024 [Page 2].

This means 25.1% of Air India’s losses now sit directly on SIA’s books.

The “Fixer-Upper” Risk:

Investing in Air India is like buying a fixer-upper house in a prime district. The location (India) is incredible, and the potential is huge. But right now, the renovation costs are bleeding SIA dry. The report explicitly states SIA is committed to supporting Air India’s “comprehensive multi-year transformation programme” [Page 4]. “Multi-year” is code for “expect losses to continue.”

3. The Income Angle: Is the 5.9% Yield Safe?

Here is the good news for income investors. Despite the profit crash, SIA is aggressively returning cash to shareholders.

The Payout Details [Page 5]:

Interim Dividend: 5 cents per share.

Interim Special Dividend: 3 cents per share.

Pay Date: Both will be paid on 23 December 2025.

The Forward Plan:

SIA has announced a plan to pay a 10 cent special dividend annually for the next three financial years (subject to AGM approval) [Page 5].

The Yield Calculation:

At a share price of ~S$6.64:

Total Interim Payout (8 cents) = ~1.2% yield (half-year).

Annualized Potential: If the final dividend matches the interim, plus the locked-in special dividends, you are looking at a total forward yield of roughly 5.9%.

Iggy’s Warning (Capital Recycling):

Is SIA generating excess cash, or are they just giving you your money back? Note that cash and bank balances declined by S$1.8 billion to S$6.4 billion in the first half [Page 3]. This was partly due to paying out previous dividends and repaying debt.

While the 5.9% yield beats the CPF OA 2.5% rate, it is not “risk-free.” You are effectively getting paid a high yield to hold a stock with significant execution risk in India.

4. Beneath the Wing: Yields are Dropping, Costs are Rising

Even within the profitable core business, there are warning signs in the metrics:

Pricing Power is Weakening: Passenger yields fell 2.9% to 9.9 cents/pkm [Page 2]. This means SIA is making less money for every kilometer flown because competition is forcing them to lower ticket prices.

Inflation is Biting: Non-fuel expenditure surged 5.9% (S$353 million) [Page 2]. Inflation is hitting everything from staff costs to airport fees.

Fuel Hedging Misfire: While fuel prices dropped 12.7%, SIA didn’t capture all the savings. They swung from a fuel hedging gain last year to a loss this year [Page 2].

Cargo is Soft: Cargo revenue fell 2.8% and yields dropped 4.1% [Page 2]. The pandemic-era cargo gold rush is officially over.

5. Balance Sheet & Outlook

The balance sheet remains a fortress, but the walls are slightly lower than before.

Deleveraging: Total debt fell by S$2.0 billion, improving the debt-equity ratio to a very healthy 0.70x (down from 0.82x) [Page 3].

Convertible Bonds: Watch out for November 24, 2025. Convertible bonds are exercisable until this date. S$714 million have already been converted, diluting shareholders, with S$136 million outstanding [Page 3].

The Outlook [Page 6]:

Management expects demand to remain “resilient” for the year-end peak. However, they explicitly flag “geopolitical tensions, macroeconomic headwinds, and inflationary cost pressures” as ongoing challenges.