Why CPF Outperforms Property in 2026: Understanding the -0.71% Rental Yield Gap

A 13,500-unit MOP wave is about to flood the heartlands, and the math proves your rental yield is losing to the CPF Board. Stop falling in love with your bricks.

1. The Global Headline (The Storm)

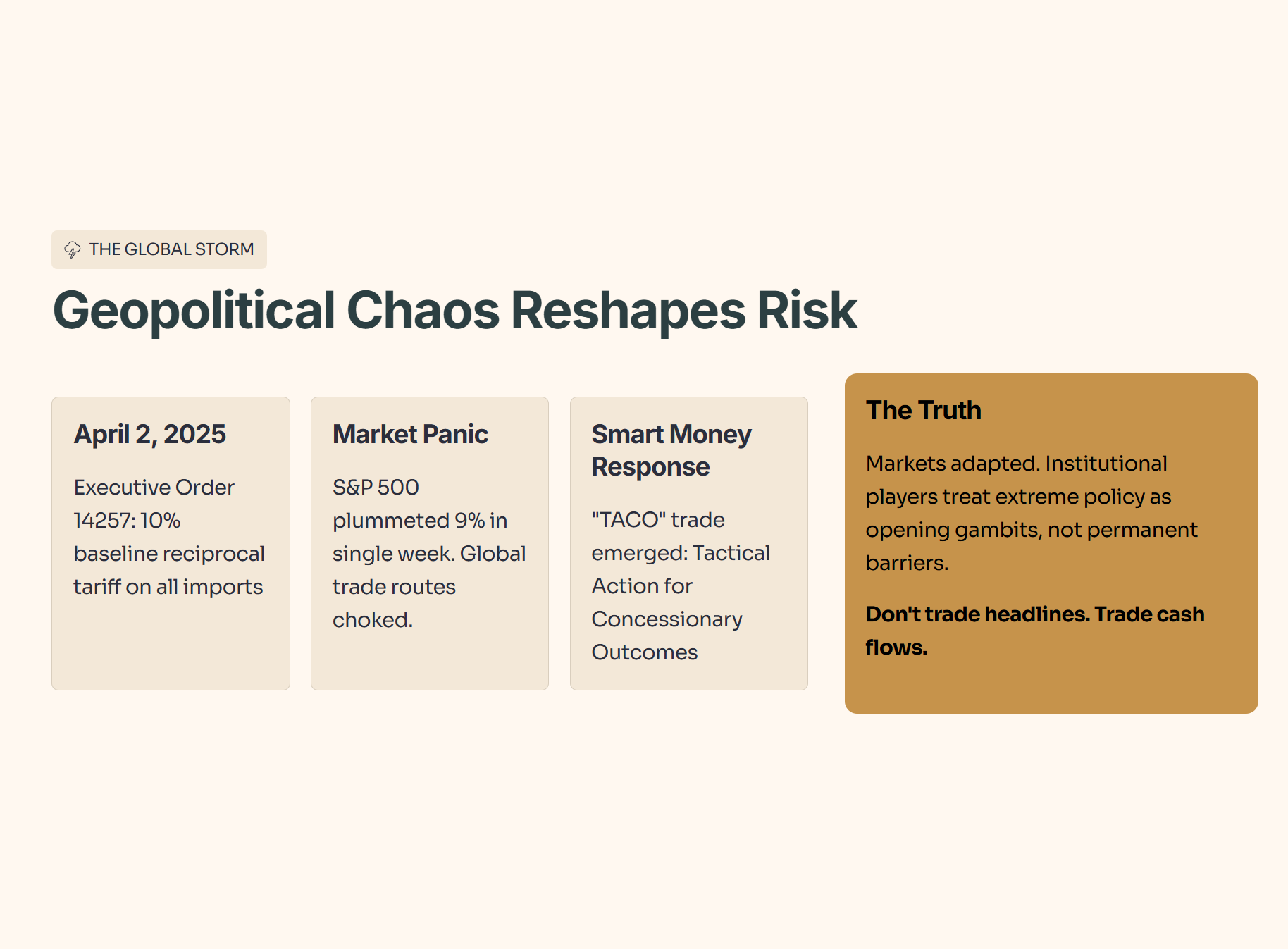

You can feel the anxiety radiating off the screens. The global economic landscape of 2025 has been defined by an unprecedented shift in the geopolitical order, fundamentally altering the risk-reward calculus for every Singaporean investor holding assets today. The 47th administration of the United States introduced a brutal “new normal” characterized by dramatic economic nationalism. We saw this peak on April 2, 2025, when Executive Order 14257 slapped a 10% baseline reciprocal tariff on nearly all imports. The immediate reaction was violent. The S&P 500 plummeted 9% in a single week. Global trade routes choked. The financial media screamed that globalization was dead.

And look, on the surface that panic makes complete sense. But here is the uncomfortable truth: the markets demonstrated a remarkable capacity for adaptation. Smart money gave rise to the “TACO” trade—Tactical Action for Concessionary Outcomes. Institutional players learned to interpret these extreme policy positions as opening gambits in transactional deal-making, rather than permanent structural barriers. To the 170 Elite Members of our community, this is why we do not trade the headlines. We trade the underlying cash flows. If you are sitting in your HDB flat watching American political theater, you are missing the actual wealth transfer happening right under your nose in the Singaporean residential market.

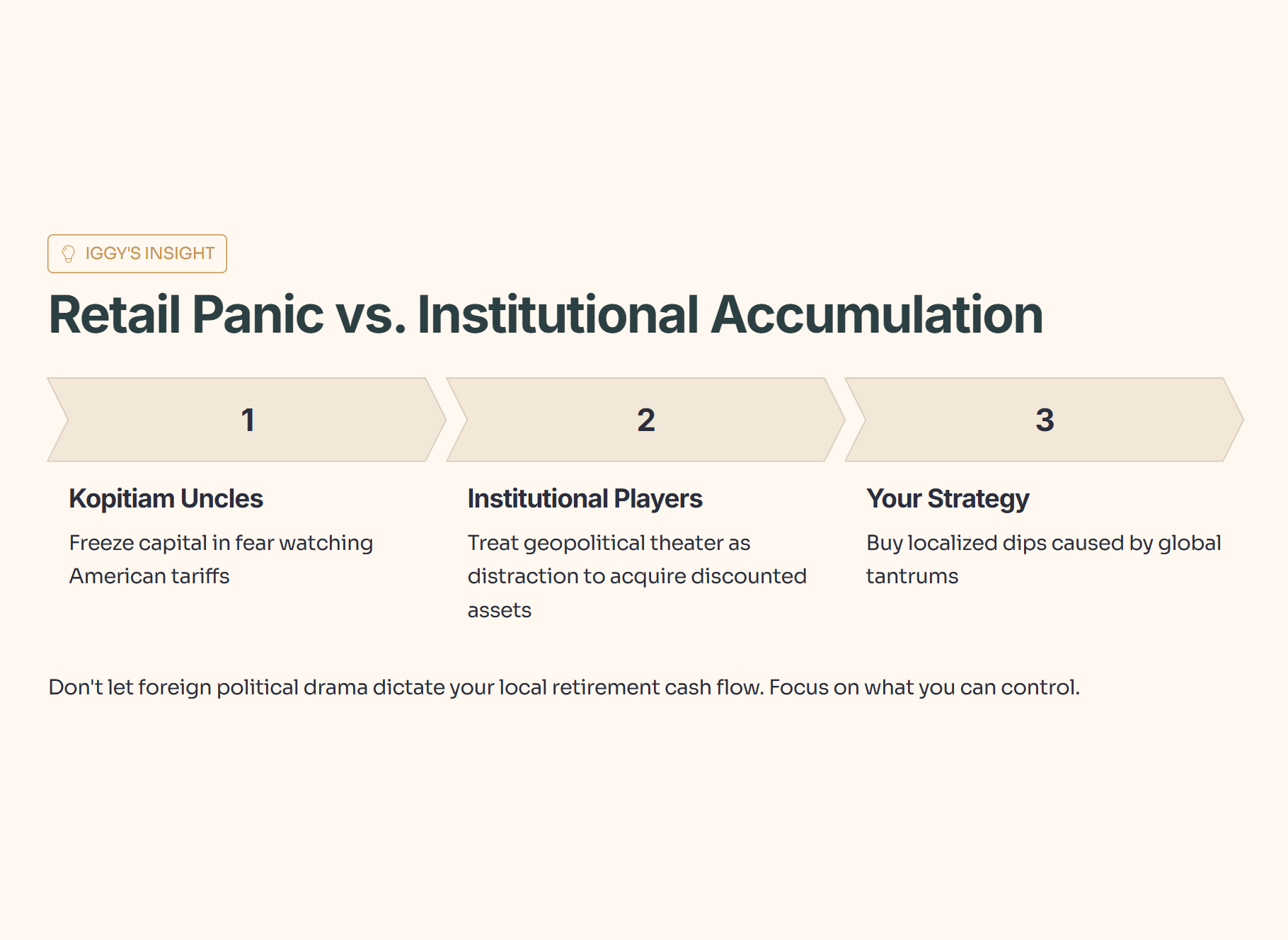

🦎 Iggy’s Insight: When the kopitiam uncles stare at the TV screaming about American tariffs, they freeze their capital in fear. Institutional players do the opposite. They treat geopolitical theater as a distraction to quietly acquire discounted assets. This is the psychological gap between retail panic and institutional accumulation. Your job is not to predict the next political tweet. Your job is to understand how that noise forces weaker hands to liquidate prime Singaporean assets. The smart money buys the localized dips caused by global tantrums. Do not let foreign political drama dictate the future of your local retirement cash flow. Focus on what you can control.

In This Article:

The Local Impact (The Wallet)

The Data Proof (The Evidence)

The Strategic Landscape (Scenario Matrix)

The Singapore Investor Playbook

InvestingPro Reality Check

The Verdict2. The Local Impact (The Wallet)

This global volatility does not exist in a vacuum. It directly impacts your wallet, your job security, and your ability to generate retirement income. Let us examine the job and income impact first. Despite the international chaos, the Singaporean economy demonstrated exceptional resilience, recording a GDP growth rate of 5% in 2025. This heavily outperformed the official forecasts of 1–3%. Historically, a 5% GDP print places us well above our 3-year post-pandemic average.

Compared to ASEAN peers like Malaysia or Thailand, Singapore has absorbed the tariff shocks by pivoting hard into tech-related AI services and a flourishing financial sector. If this macro resilience intensifies by 10%, we will see massive wage inflation in specialized sectors. If it reverses 10% due to a sudden global recession, wage stagnation will hit the middle class hard. So what does this mean for you? It means the domestic “wealth effect” is real, providing the exact liquidity needed to prop up local property prices even when global equities tremble.

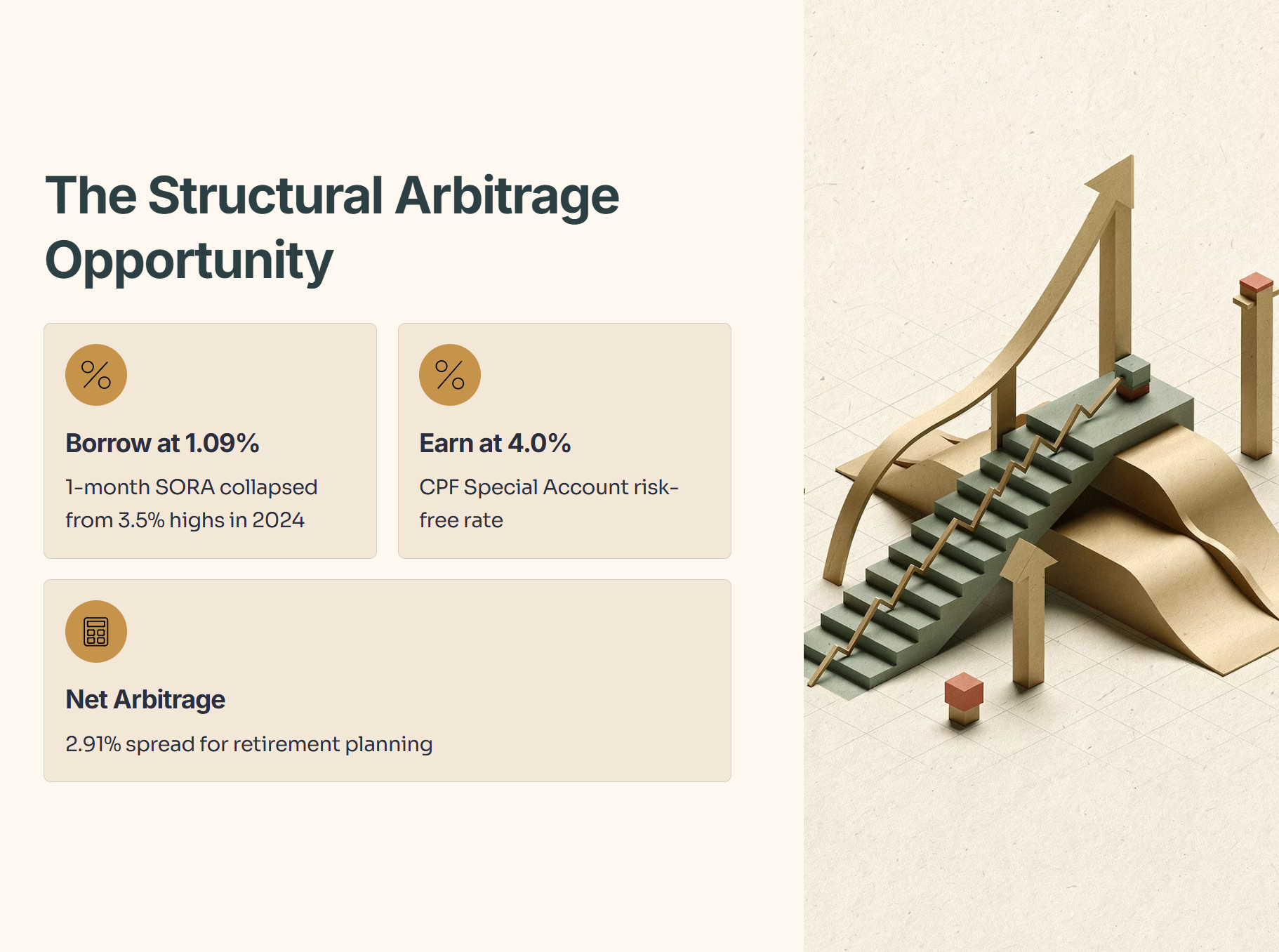

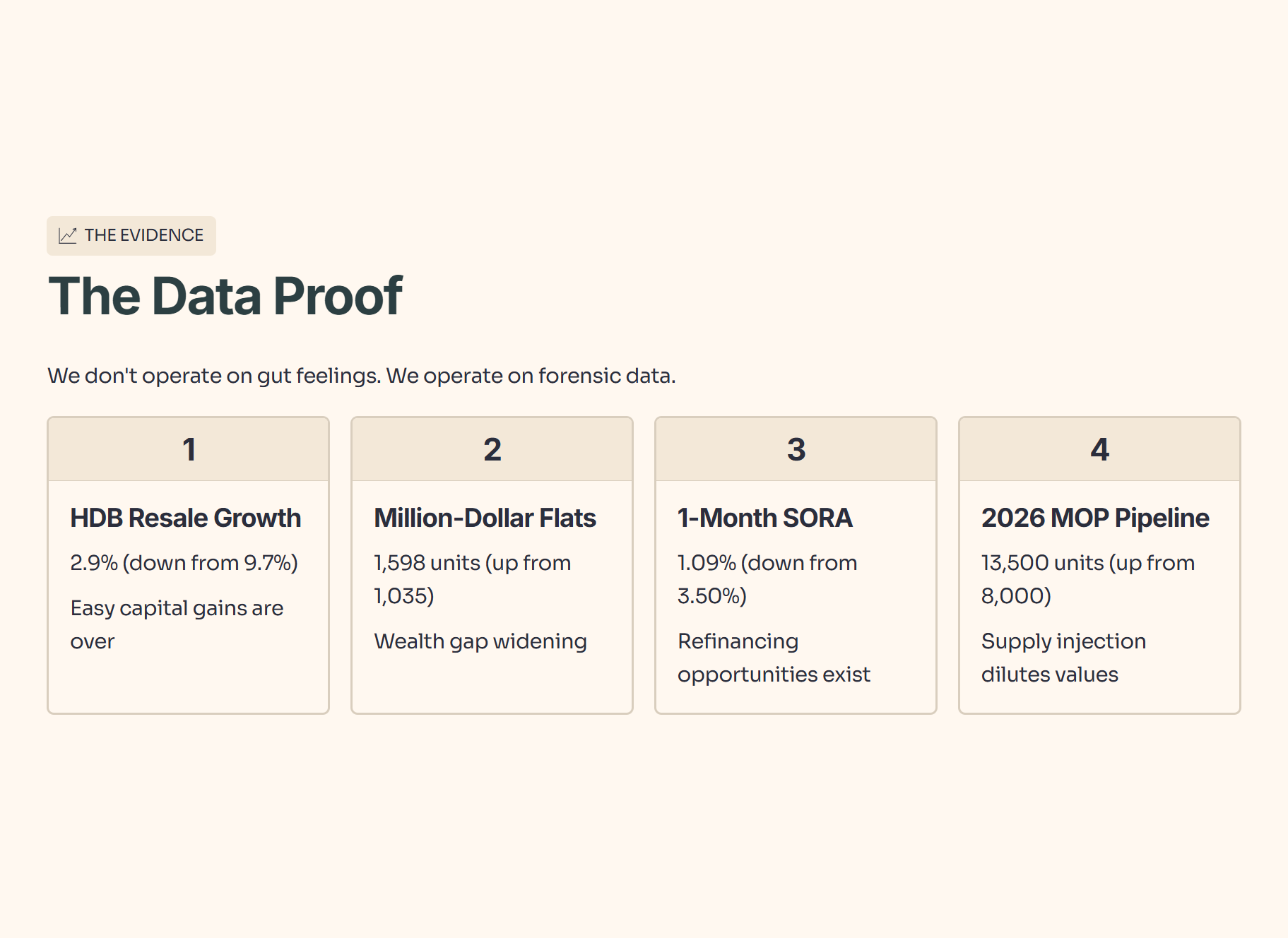

Next, we must look at the CPF and SRS impact. A defining feature of this current cycle is the stabilization of interest rates at relatively lower levels. The Singapore Overnight Rate Average (SORA) has collapsed from its 2024 highs. The 1-month SORA floating mortgage rate is now sitting at roughly 1.09%. Historically, this is a massive reversion from the 3.5% pain we felt two years ago. Compared to the US Federal Reserve’s hesitation, the local cost of borrowing has provided massive relief. If this rate trajectory continues downward by another 10%, cash-out refinancing will become a primary strategy for retirees. If rates spike 10%, over-leveraged buyers will be crushed. So what does this mean for you? It means your CPF Special Account paying a risk-free 4.0% is vastly outperforming the cost of capital. You can borrow at 1.09% and earn 4.0% risk-free. That is a structural arbitrage opportunity for your retirement planning.

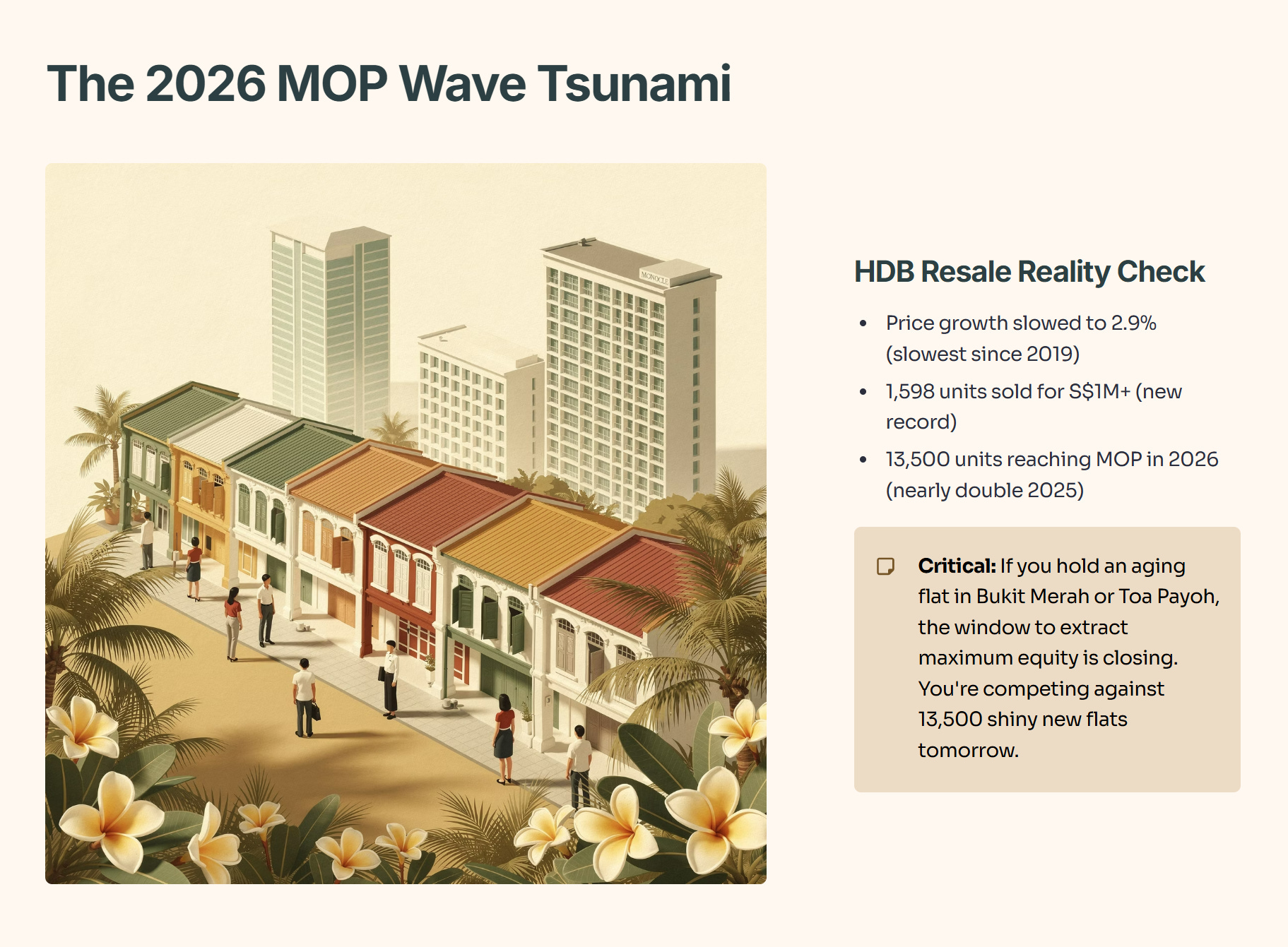

Finally, we have to audit the SGX portfolio and physical real estate impact. The HDB resale market has experienced a stabilization of price growth, easing to 2.9% for the full year. This is the slowest annual growth since 2019. However, the segment for high-value transactions reached new heights, with 1,598 units sold for at least S$1 million. We are looking down the barrel of a massive 2026 “MOP Wave.”

Approximately 13,500 units will reach their 5-year Minimum Occupation Period—nearly double the 8,000 units seen in 2025. If this supply shock hits 10% harder than expected, heartland resale prices will correct sharply. If demand outstrips it by 10%, million-dollar flats will become the new baseline in mature estates. So what does this mean for you? If you hold an aging flat in Bukit Merah or Toa Payoh, the window to extract maximum equity is closing. You are competing against 13,500 shiny new flats hitting the market tomorrow.

🦎 Iggy’s Insight:

The 2026 MOP wave is the silent killer of older HDB valuations. It is the classic supply shock most Singaporeans ignore until their neighbor sells for fifty thousand less than expected. Think about the wet market when a new stall opens selling the exact same fish for cheaper. The old stalls must adapt or bleed customers. If you are sitting on an aging flat hoping for a million-dollar payout, you are playing a dangerous game of musical chairs. The music is slowing down. You must extract your equity before the new supply forces a structural price correction in your specific precinct.

3. The Data Proof (The Evidence)

We do not operate on gut feelings here. We operate on forensic data. The narrative tells you the property market is always going up, but the data reveals a dangerous dual-track evolution that you must navigate carefully.

The number that matters most here is the 13,500 units in the forward 2026 MOP pipeline, because this represents a massive supply injection that will fundamentally alter pricing power in the heartlands. You cannot expect 2023 price appreciation when the market is suddenly flooded with nearly double the supply of newly MOP-ed units.

Furthermore, the private resale market tells a highly localized story. The Outside Central Region (OCR) saw prices increase by 5.6%. In sharp contrast, the Core Central Region (CCR) saw a contraction of -0.2%. The median transacted unit price gap between new non-landed homes in the CCR and the RCR narrowed to just 10%—the smallest on record since 1995.

So what does this mean for you? It means the heartlands are becoming historically expensive relative to prime districts. The risk-reward ratio is shifting.

🦎 Iggy’s Insight:

A 10% price gap between the CCR and the OCR is a mathematical anomaly. It means you are paying nearly Orchard Road prices for a condo in Sengkang. This is the equivalent of paying premium wagyu prices for a standard hawker steak. The market has temporarily mispriced convenience over prime land value. For the shrewd investor, this is the clearest signal to rotate. Sell the overvalued heartland asset to the desperate buyer, and use those funds to acquire prime central real estate while foreign buyers are locked out by the 60% ABSD.

4. The Strategic Landscape (Scenario Matrix)

To survive 2026, you cannot rely on a single forecast. You must build a portfolio that survives multiple distinct futures. We run scenarios because hope is a terrible financial strategy.

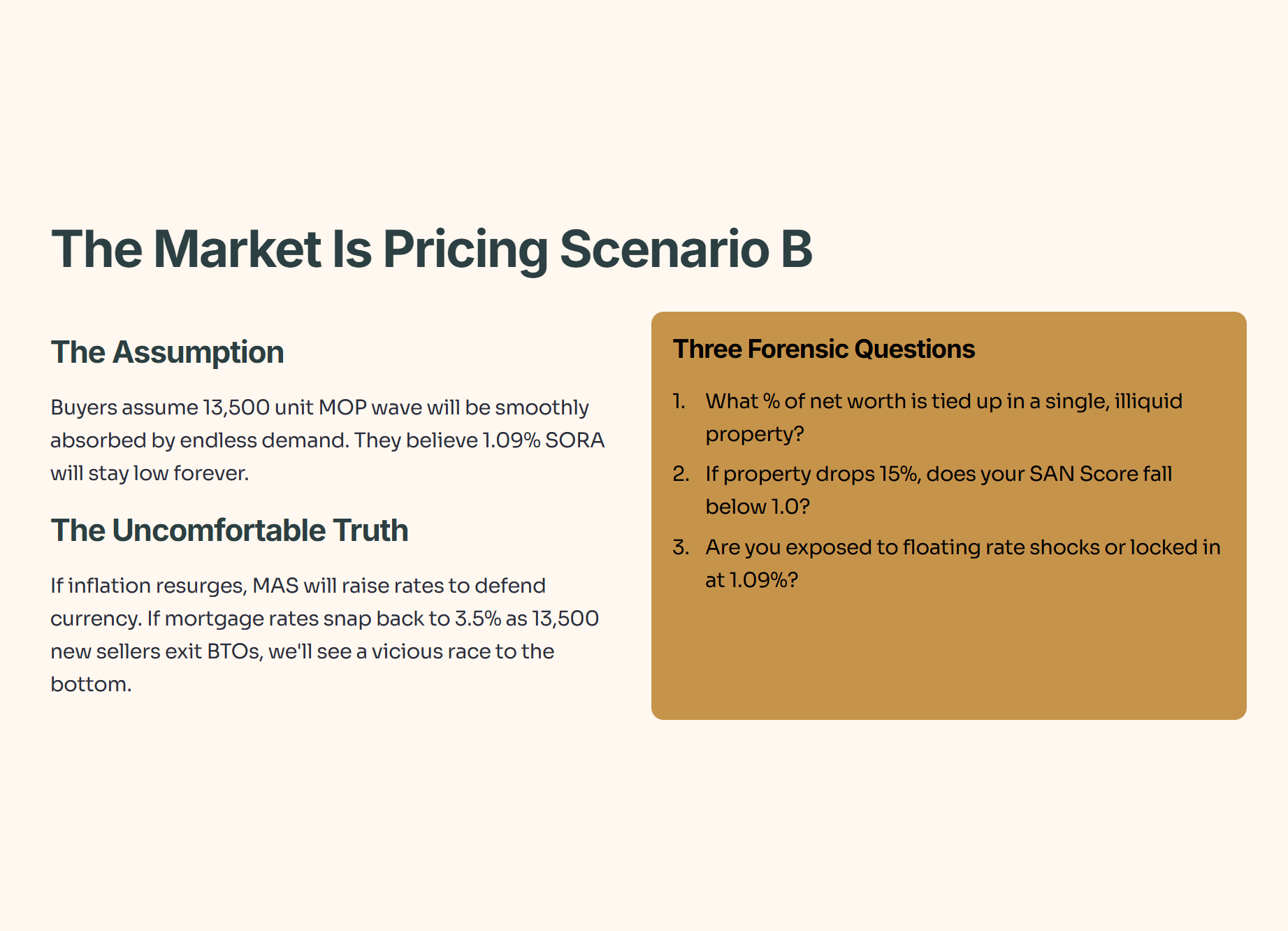

Currently, the market is pricing in Scenario B. Buyers assume the massive 13,500 unit MOP wave will be smoothly absorbed by endless demand, and that the 1.09% SORA rate will stay low forever.

And look, on the surface that makes sense given the 5% GDP growth we just witnessed. But here is the uncomfortable truth: if inflation resurges due to aggressive US tariffs, local rates will be forced up by the MAS to defend the currency. If mortgage rates snap back to 3.5% precisely as 13,500 new sellers try to exit their BTOs, we will see a vicious race to the bottom in HDB resale prices.

You need to run your own portfolio through the wringer tonight. Ask yourself these three forensic questions before the market opens tomorrow:

What is the exact percentage of your net worth tied up in a single, illiquid residential property right now?

If your property value drops 15% tomorrow, does your SAN Score drop below 1.0, forcing you to alter your retirement lifestyle?

Are you holding a mortgage package that exposes you to floating rate shocks, or have you locked in the current 1.09% anomaly?

🦎 Iggy’s Insight:

Running scenarios is like keeping an umbrella in your car trunk. You do not carry it because you want it to rain; you carry it so you are not the fool getting soaked when the weather unexpectedly turns. We always plan for Scenario C because the market always punishes the unprepared. If you only plan for a sunny housing market, a minor supply shock will wipe out your paper wealth. By stress-testing your mortgage against a sudden rate spike, you ensure your family’s roof is never dependent on the mercy of a central banker.

5. The Singapore Investor Playbook

“Next, I’ll show you the exact ‘property vs CPF vs dividends’ decision rule (with the yield-spread math) that tells you whether to hold, rent, or rotate—based on your own numbers.”