Q3 Tariff Hike: The $1B Warning For Industrial REITs

Government give $1B shield for your HDB light bill, but your industrial REIT landlord is still paying full price.

The $1B Warning: Why Singapore’s Energy Shield Exposes Your REIT Dividends

Singapore just triggered a one billion dollar emergency shield to suppress utility costs, and if you hold local industrial real estate investment trusts, this is the exact moment your dividend yield comes under structural threat. The payout is not a windfall. It is the pre-funding of a severe utility shock that has not yet appeared on a single balance sheet in the SGX industrial sector.

The central question for your portfolio is not whether global energy prices are rising or falling today. The question is which of your assets will survive the margin squeeze that is already mathematically locked into the system — and will only become visible two quarters from now.

In This Article:

The Storm That Has Already Happened — You Just Cannot See It Yet

Iggy’s Insight

The Wallet Consequence

Iggy’s Insight

The Data Proof

The Strategic Picture

The Singapore Investor Playbook

The Forensic Verdict

About Iggy & the Elite Investors

A Quick Note Before the Verdict. You aren’t here for the kopi tips or the hype. You’re here because you want the forensic truth before you commit a single dollar of your capital. That tells me something about the kind of investor you are.

But here’s the uncomfortable truth about how independent publishing works. The algorithm doesn’t know you read every word. It doesn’t know you checked the gearing ratio twice. It only sees one signal — whether you’ve hit that subscribe button. Every forensic investor who reads without subscribing is invisible to the machine.

If this analysis has ever helped you identify a risk or calculate a margin of safety — subscribe for free now and share this with one person who needs to hear it. Not for me. To tell the algorithm that data-driven SGX analysis deserves a seat at the table alongside the noise.

Section 1: The Storm That Has Already Happened — You Just Cannot See It Yet

The Middle East conflict systematically squeezed the Strait of Hormuz, and physical dated Brent reached near $150 per barrel at the peak of the crisis on April 7. By April 8, a two-week ceasefire announcement had pulled spot Brent back sharply to approximately $93–$94 per barrel — a drop of over fourteen percent in a single session. Most retail investors watching that headline number will conclude the energy crisis is over. That conclusion is the most dangerous misread of the current macro cycle.

Here is the mechanism that makes the spot price movement almost irrelevant to your dividend stream.

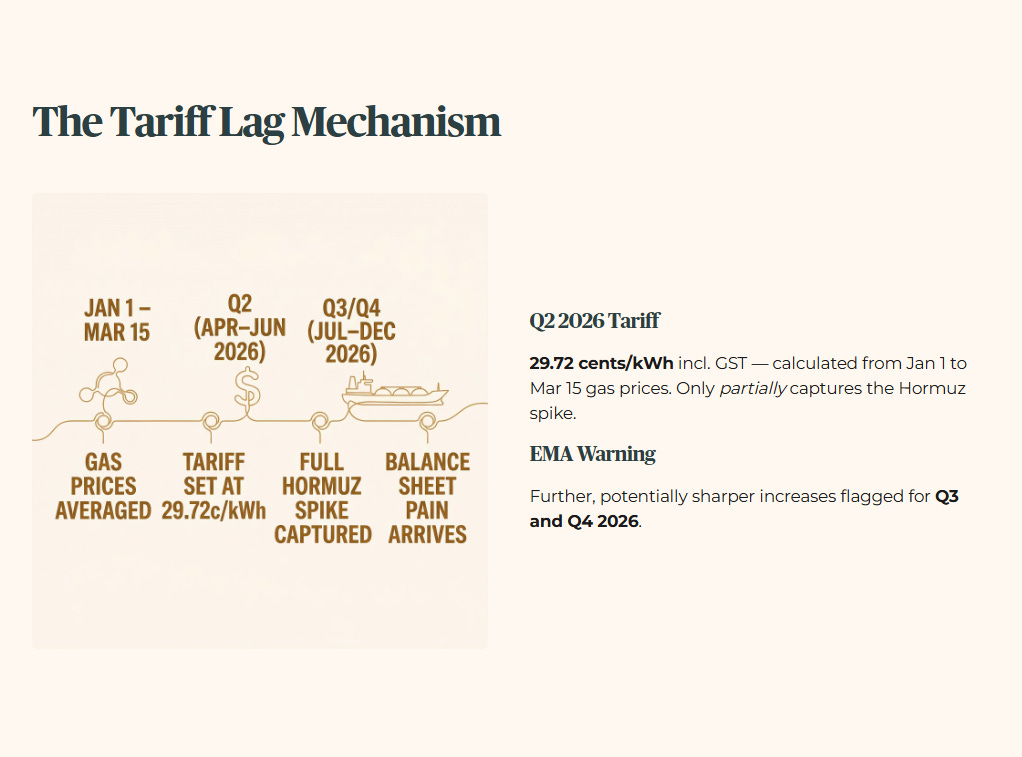

SP Group does not set the Singapore electricity tariff based on where Brent crude is trading today. The tariff is calculated using a backward-looking average of natural gas procurement costs over a defined preceding window. The Q2 2026 tariff — effective April 1 to June 30 — was set at 27.27 cents per kWh before GST, or 29.72 cents per kWh including GST. That figure was calculated using natural gas prices from January 1 to March 15, 2026. It only partially captures the Hormuz-driven price spike. The EMA has explicitly flagged that further and potentially sharper increases are expected in Q3 and Q4 2026 as the full effect of elevated gas prices flows through the calculation.

Read that again. The ceasefire happened on April 8. The Q3 tariff calculation window has already begun. Whatever damage the Hormuz crisis inflicted on wholesale natural gas pricing between January and March is now locked into the forward tariff — regardless of where spot crude closes this week. The relief you are reading about in the headlines is a household consumption subsidy. It protects the HDB flat. It offers zero protection to the commercial landlord paying the utility bill on a logistics warehouse in Jurong or a flatted factory complex in Tuas.

The six-month lag in the SP Group tariff adjustment mechanism is the quietest and most dangerous part of this cycle. The pain of the geopolitical tension that peaked in early April will only appear on corporate balance sheets in Q3 and Q4. That is the forensic gap the retail market has not priced.

🦎 Iggy’s Insight

The psychological gap between what institutional money is pricing and what the retail market feels is currently at its widest point this year. Retail investors are looking at the ceasefire headline and concluding the energy threat has passed. Institutional capital is looking at the same headline and calculating exactly how much cash flow will be erased from commercial real estate earnings when the Q3 and Q4 SP Group tariffs arrive — tariffs that were set using gas prices from before the ceasefire existed.

The state has ring-fenced the consumer. It has left the commercial landlord fully exposed. The dividend you rely on is standing directly in the path of a cost wave that was locked in months ago and cannot be recalled by any diplomatic announcement.

Section 2: The Wallet Consequence

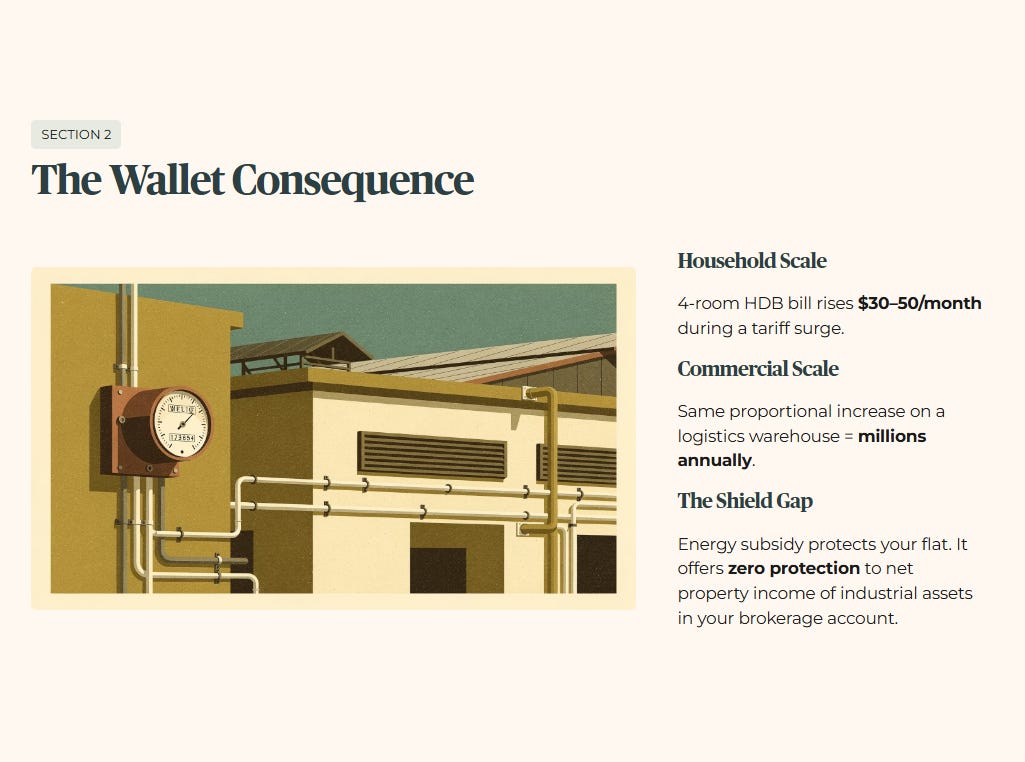

To understand how a tariff lag translates into a localised margin collapse, you have to measure the cost impact in terms a household in Bedok or Toa Payoh would recognise. When the underlying energy tariff surges, the monthly utility bill for a four-room HDB flat might shift upward by thirty to fifty dollars. That proportional increase applies to a logistics warehouse or a sprawling business park on a commercial scale that runs into the millions of dollars annually. The energy shield temporarily protects your personal flat. It offers zero protection to the net property income of the industrial facilities you own through your brokerage account.

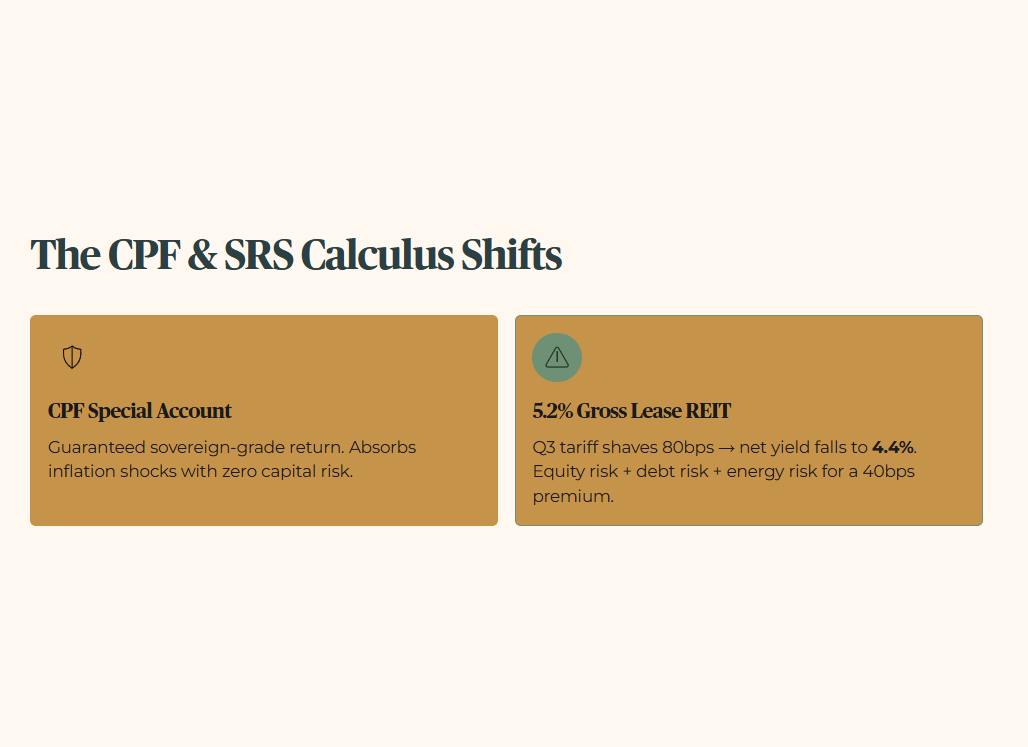

This macro reality forces a completely different CPF and SRS calculus for the next twenty-four months. When utility overheads threaten to erase corporate profit margins, the risk-free environment becomes drastically more attractive relative to standard equity exposure. The CPF Special Account offers a guaranteed return that acts as a true sanctuary — a sovereign-grade fortress that absorbs global inflation shocks without capital risk. Chasing a five percent yield in an energy-vulnerable asset right now carries a specific structural risk that is not visible in today’s unit price. If the incoming Q3 tariff shaves eighty basis points off a distribution that was already yielding five point two percent, your net return falls to four point four percent. You are taking on equity risk, debt refinancing risk, and geopolitical energy risk for a forty basis point premium over a guaranteed sanctuary rate.

The most direct wallet consequence lies within the industrial real estate sector, and it depends entirely on how lease agreements are structured. When an asset operates on a gross lease, the landlord pays the utilities. As SP Group bills spike in Q3 and Q4 in response to the energy shock, net property income collapses because the trust absorbs the extra cost to keep the facility operational. Conversely, assets operating on triple net leases are structurally fortified. The tenant pays the utilities directly. The distribution is shielded from the energy shock because the cost passes entirely to the occupier. Understanding this mechanical difference is the only forensic tool that protects your retirement cash flow from the incoming grid adjustments.

🦎 Iggy’s Insight

The second-order effect that retail investors are completely missing is the debt servicing cascade. When utility bills compress net property income, the overall valuation of the asset takes a hit at the next appraisal cycle. That valuation drop pushes the gearing ratio higher without the trust taking on a single dollar of new debt. A trust operating near the four times interest coverage threshold will see that buffer erode the moment the Q3 tariff takes effect. If utility costs jump twenty percent, a trust with an ICR of two point five times faces a binary choice: slash the distribution or risk a technical covenant breach. You are not just losing a slice of your quarterly income to the power grid. You are watching the fortress walls of the balance sheet weaken in real time — before the earnings report confirms it.

Section 3: The Data Proof

The forensic conclusion here is that the structural delay in local price adjustments has created a temporary and dangerous illusion of safety.

Table 1 — Macro Evidence Dashboard

The single number that makes the rest of the noise irrelevant is not the spot crude price. It is the Q3 tariff calculation window, which opened on April 1 and is running right now. Every day of elevated wholesale natural gas pricing between now and the close of that window gets averaged into the Q3 tariff that will hit commercial balance sheets in July. The ceasefire buys diplomatic time. It does not rewind the averaging mechanism.

The single number that makes the rest of the noise irrelevant is not the spot crude price. It is the Q3 tariff calculation window, which opened on April 1 and is running right now. Every day of elevated wholesale natural gas pricing between now and the close of that window gets averaged into the Q3 tariff that will hit commercial balance sheets in July — and that is the moment your industrial REIT either clears its dividend floor or quietly fails it.