Singapore Space Ambitions vs. Valuation: Can a $32.6B Order Book Justify the 11x P/B?

ST Engineering (S63): Does a S$32.6B Order Book Justify a 16.7% Valuation Premium?" -- A Deep Dive into the S$10 ST Engineering Question.

The News & Context

On April 1, 2026, Singapore is set to launch the National Space Agency of Singapore (NSAS). This isn’t just a vanity project; it is a calculated move to capture a slice of a US$1.8 trillion global space economy. For the average investor, this announcement centers on one specific national champion: ST Engineering (S63).

With the government committing over S$210 million to space initiatives and ST Engineering unveiling a “next phase” constellation of satellites (NeuSAR-2) and laser-comms (NEBULA), the narrative is intoxicating. The headlines suggest we are witnessing the birth of a regional space powerhouse.

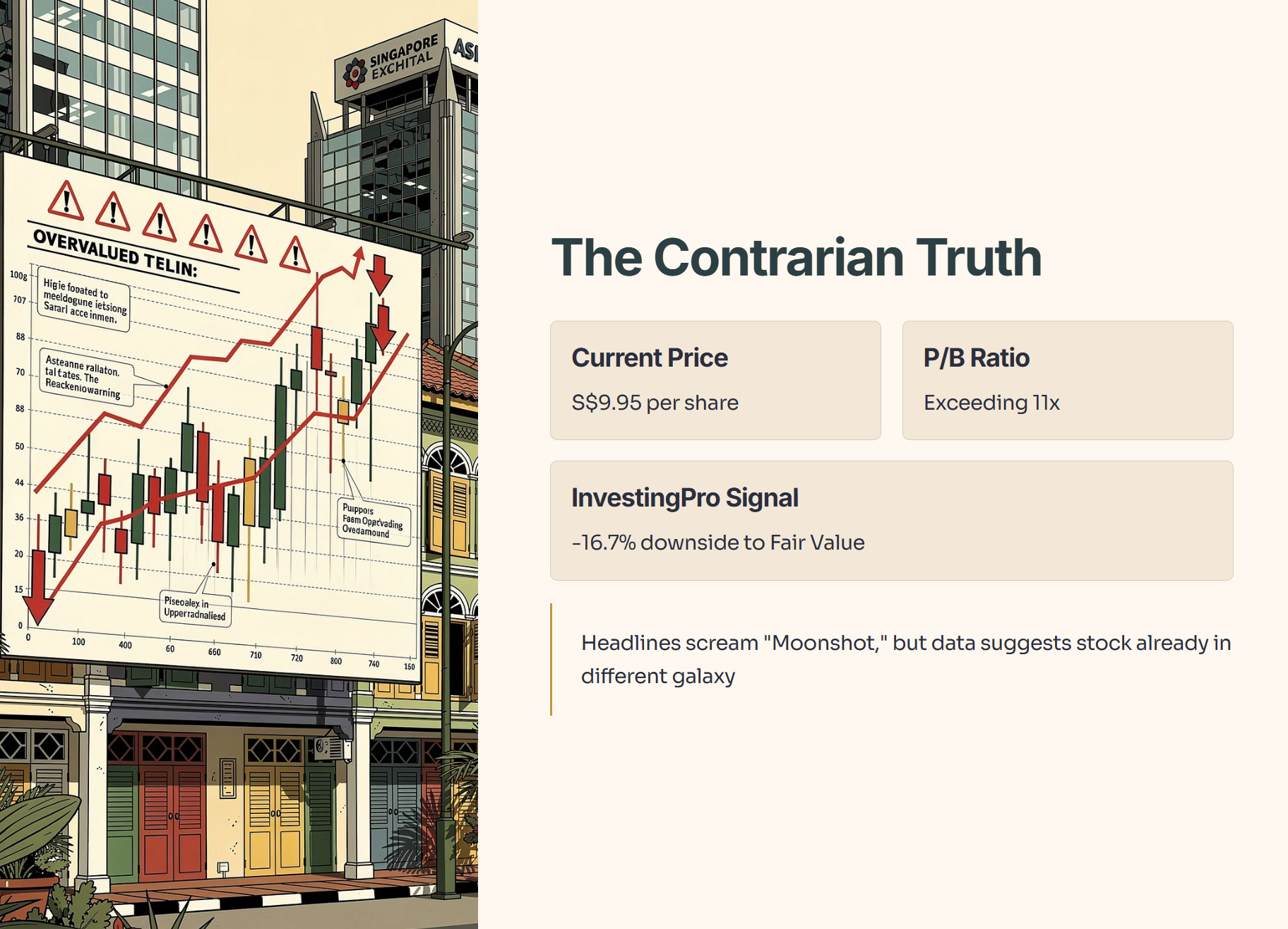

The Contrarian Truth

The headlines scream “Moonshot,” but the InvestingPro data suggests the stock is already in a different galaxy. While the news of NSAS reinforces ST Engineering’s status as a strategic pillar, the retail investor’s reality is grounded by a sobering set of numbers. We are looking at a stock trading at S$9.95, with a Price-to-Book (P/B) ratio exceeding 11x.

Is this a fundamental re-rating, or are we overpaying for “cool factor” satellites? InvestingPro currently flags the stock in overbought territory with a -16.7% downside to its Fair Value.

In This Article:

The Masterclass: The Incremental Dividend Payout Model

Step 1: The Health Check (Balance Sheet & Net Debt)

The Narrative: “Before we look at the dividend, can they pay their bills?”

The Data: Analyze Solvency

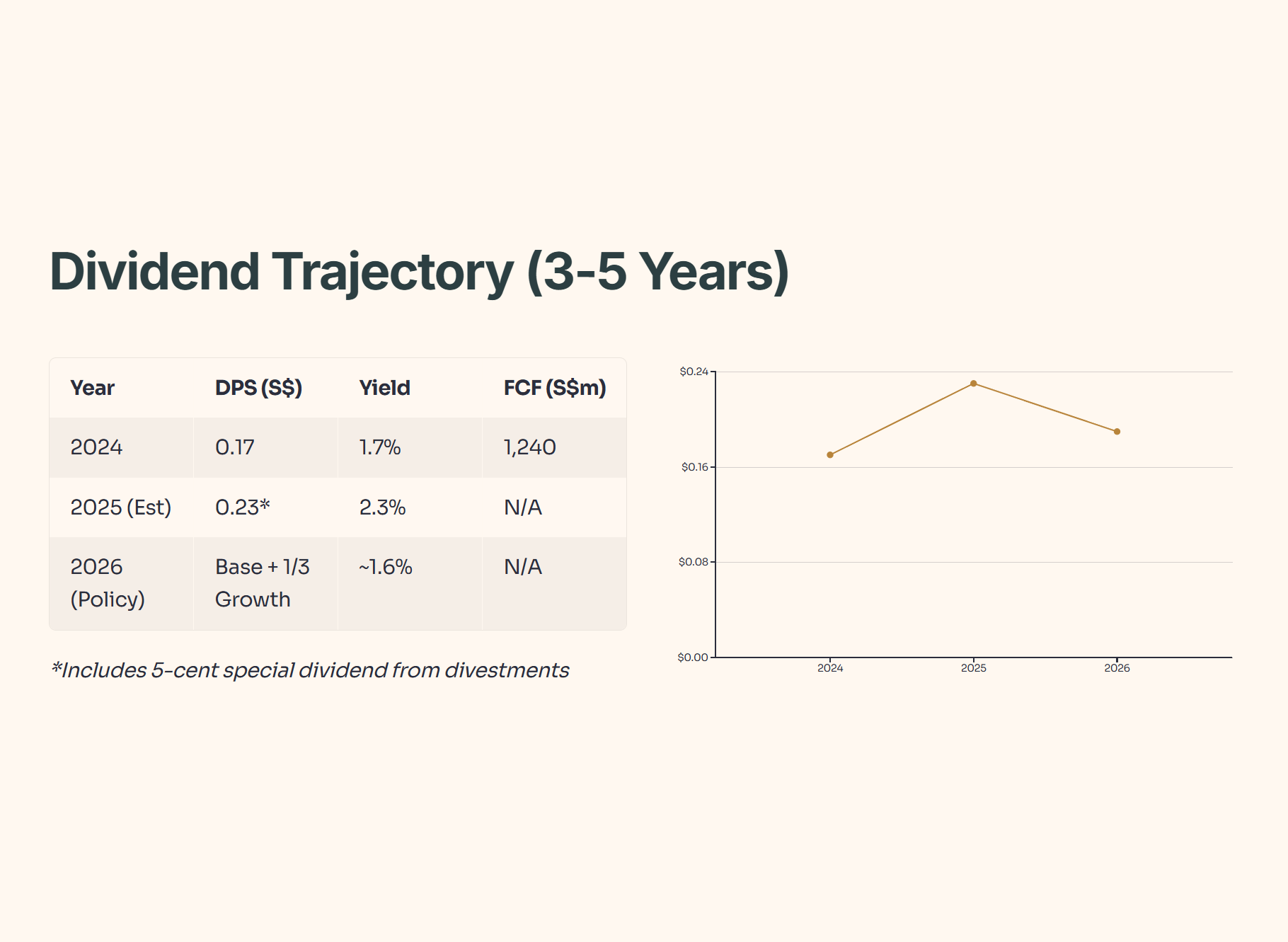

Step 2: The Wealth Check (Dividends & Cash Flow)

The Narrative: “Are they paying us from profit or debt?”

The Data: Payout & FCF

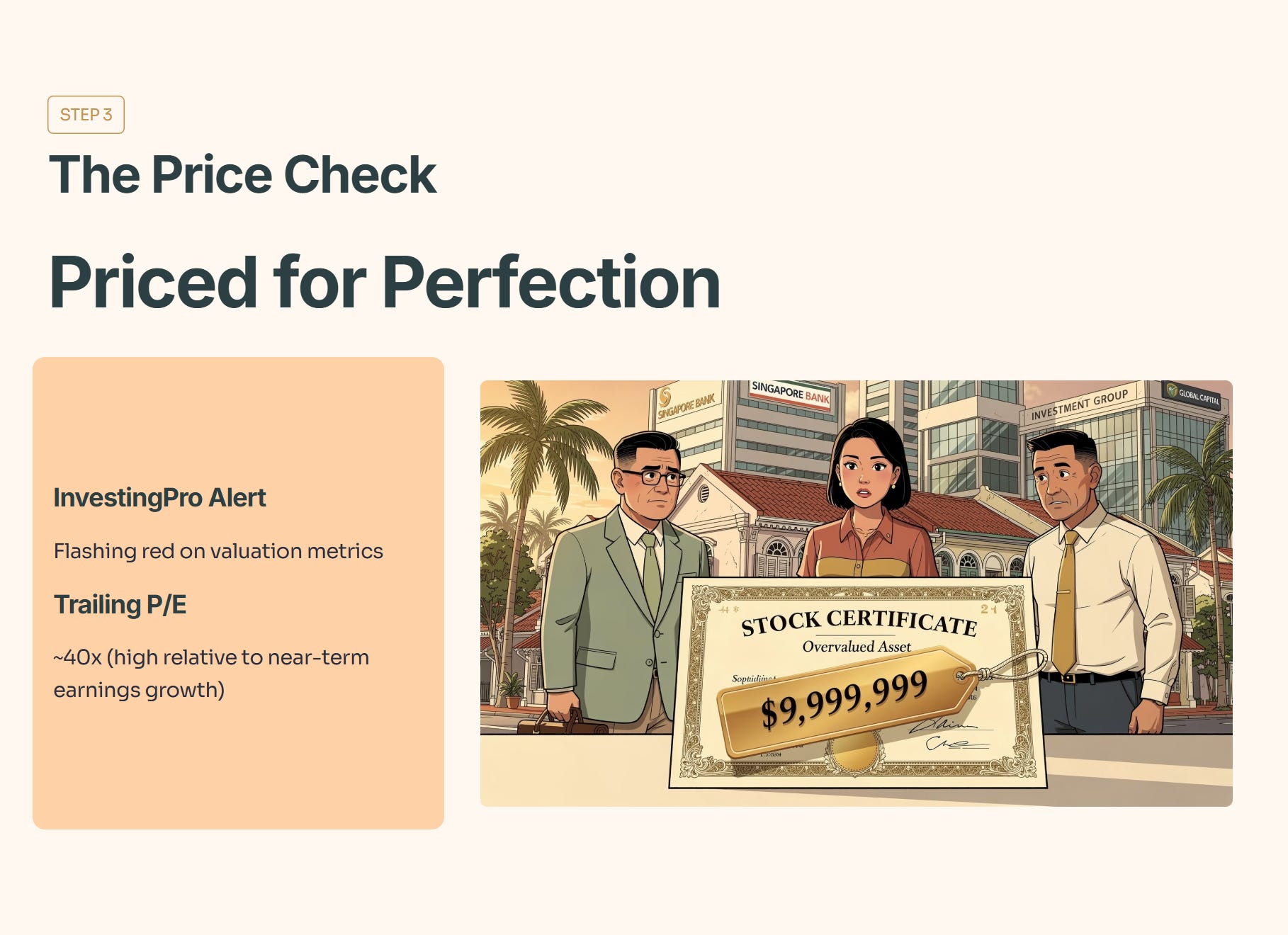

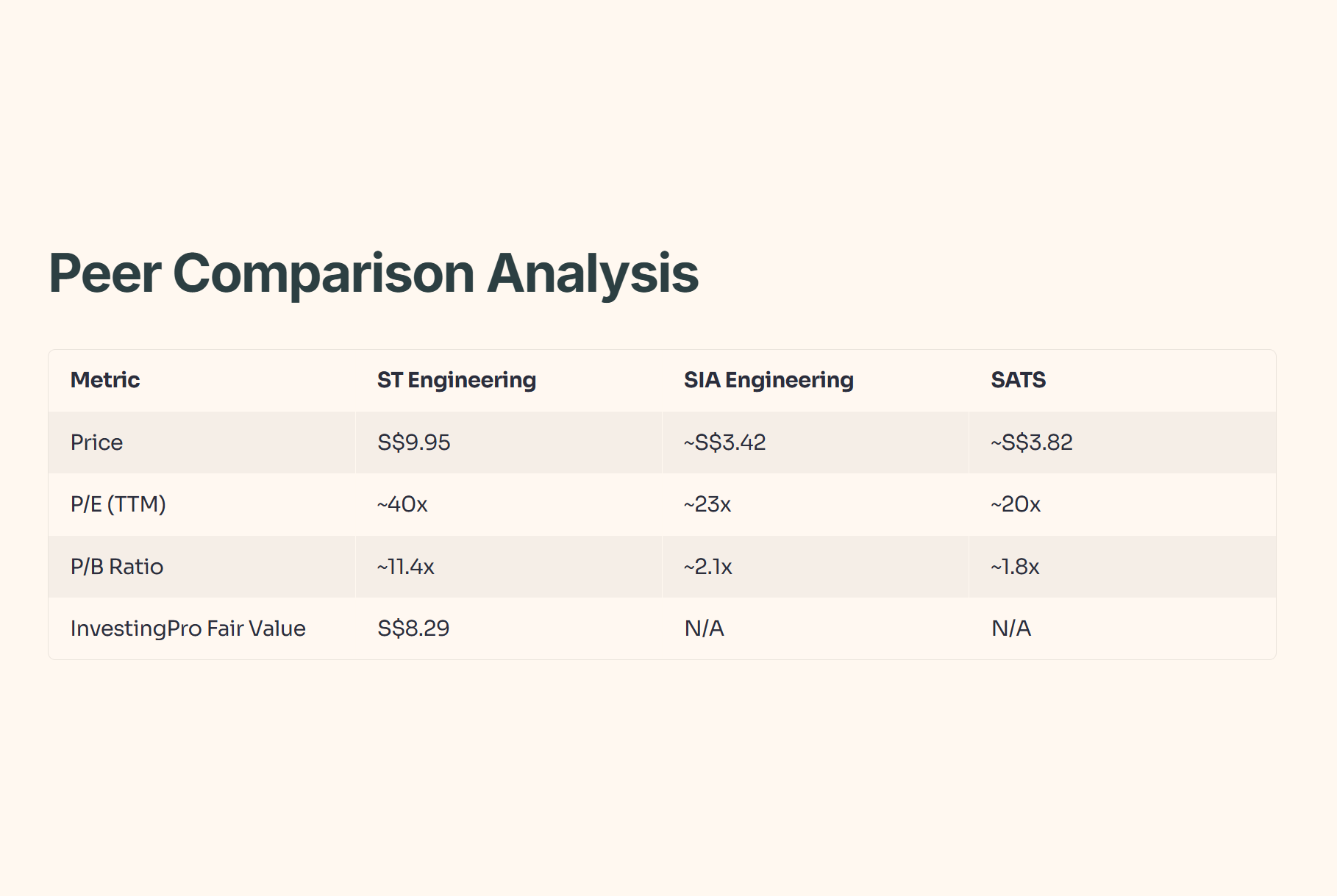

Step 3: The Price Check (Valuation & Peers)

The Narrative: “Is it cheap, or is it just ‘cheap’ for a reason?”

The Data: P/E, P/B vs Peers

Step 4: The Future Check (Scenarios & Fair Value)

The Focus: The InvestingPro Model

The Bottom Line (Strategic Conclusion)

InvestingPro Reality Check

Iggy's Verdict🦎 About Iggy & The “Elite 150”

Welcome to the Pit! I’m Iggy, your guide through the Singapore market jungle. We are 5,800+ subscribers strong, hunting the alpha that mainstream media misses.

🚨 Stop Waiting 14 Days for “Old News” Free subscribers wait 2 weeks to see my videos. By then, the trade is often gone.

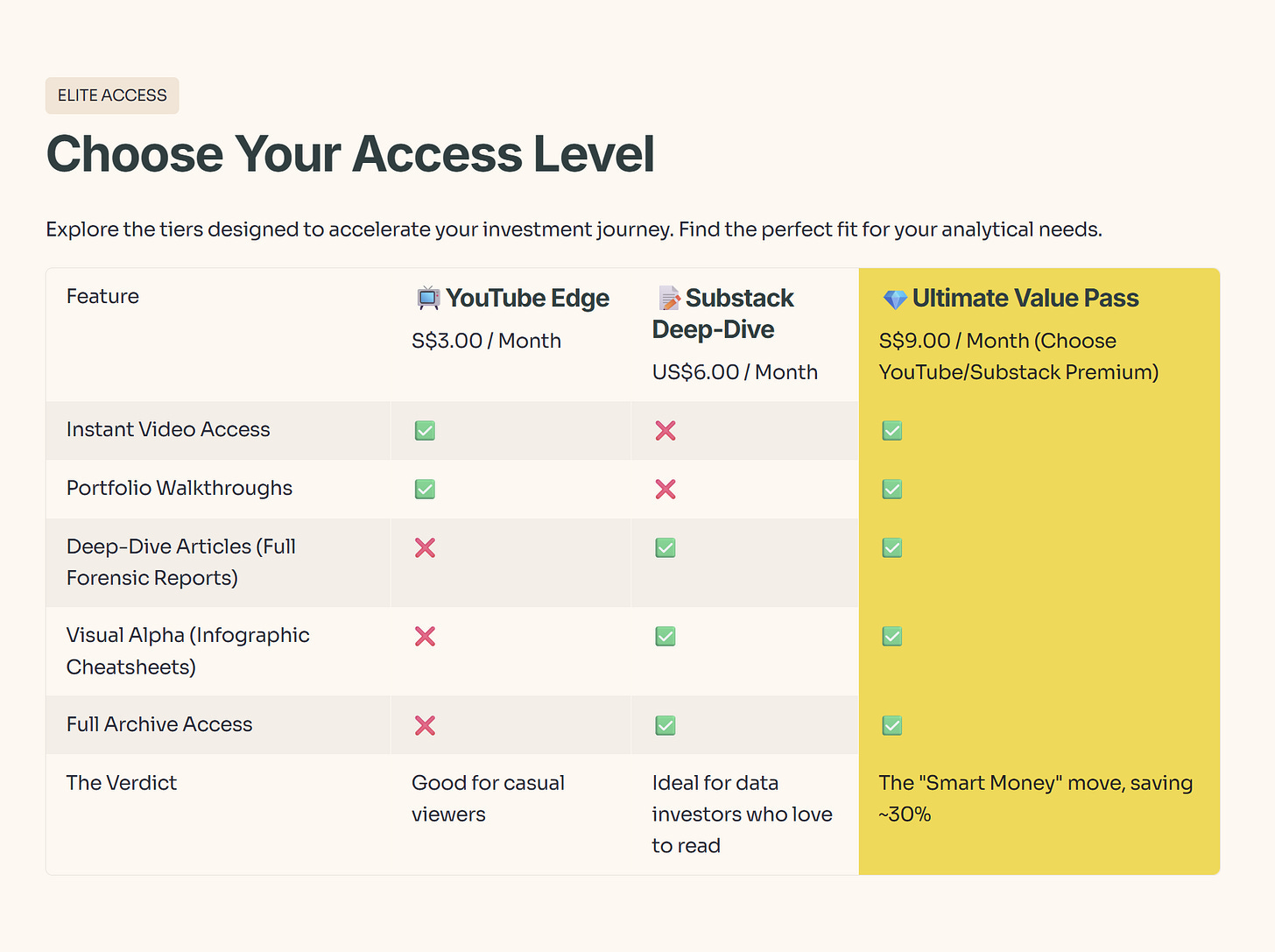

Join the 150+ Members in the Inner Circle:

⚡ Instant Access: Watch videos the moment they drop.

📝 The Full Vault: Unlock deep-dive articles & infographics.

💎 The “Smart Money” Move: Get the S$9/mo Bundle (YouTube + Substack) and save ~30%.

Get the data while it’s fresh. 👉 Join the Inner Circle Here

The Masterclass: The Incremental Dividend Payout Model

Most investors understand a standard “Payout Ratio”—the percentage of earnings paid as dividends. However, ST Engineering has introduced a more focused framework for 2026: the Incremental Payout.

Under this policy, the company commits to paying out one-third of its year-on-year net profit increase as additional dividends. This shifts the focus from “What is the current yield?” to “How fast can they grow profit?” If profits stagnate, the dividend growth follows.

🎓 Educational Note: Total Shareholder Return (TSR)

TSR is the total gain an investor receives, combining share price appreciation and dividends. For high-valuation stocks like STE, the “Yield” (dividends) becomes a smaller part of the TSR equation compared to “Capital Gains.”

Step 1: The Health Check (Balance Sheet & Net Debt)

The Narrative: “Before we look at the dividend, can they pay their bills?”

Space exploration is expensive. Building a “constellation” of satellites requires heavy capex. ST Engineering carries significant borrowings, but it has been deleveraging, with total borrowings reducing to roughly S$5.8b in 2024.

The Data: Analyze Solvency

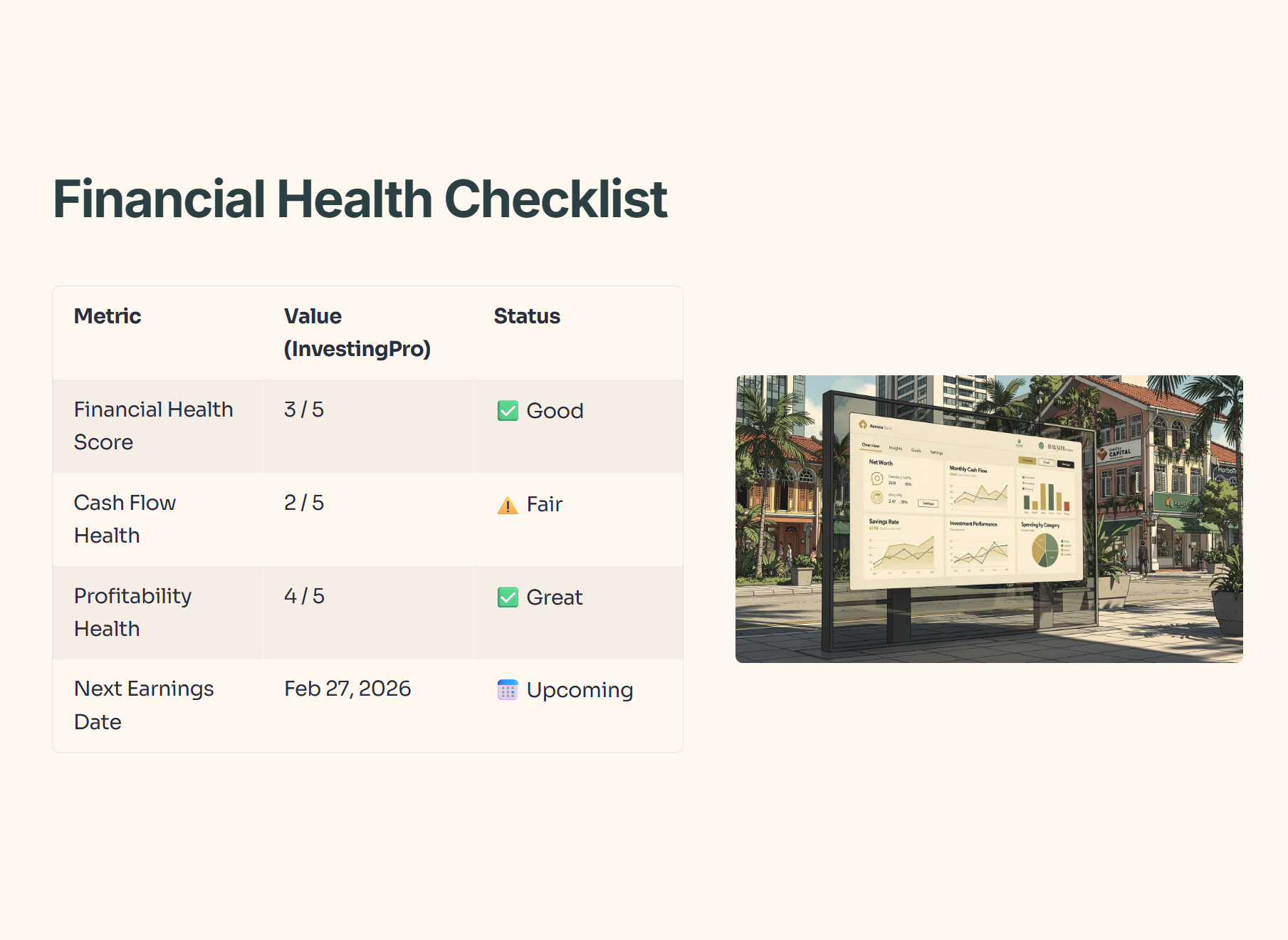

According to InvestingPro, the company maintains a Financial Health score of 3/5, labeled as “Good Performance”. However, its Cash Flow Health sits at a 2/5, indicating that while they are stable, cash conversion needs to remain tight to fund their ambitious space roadmap.

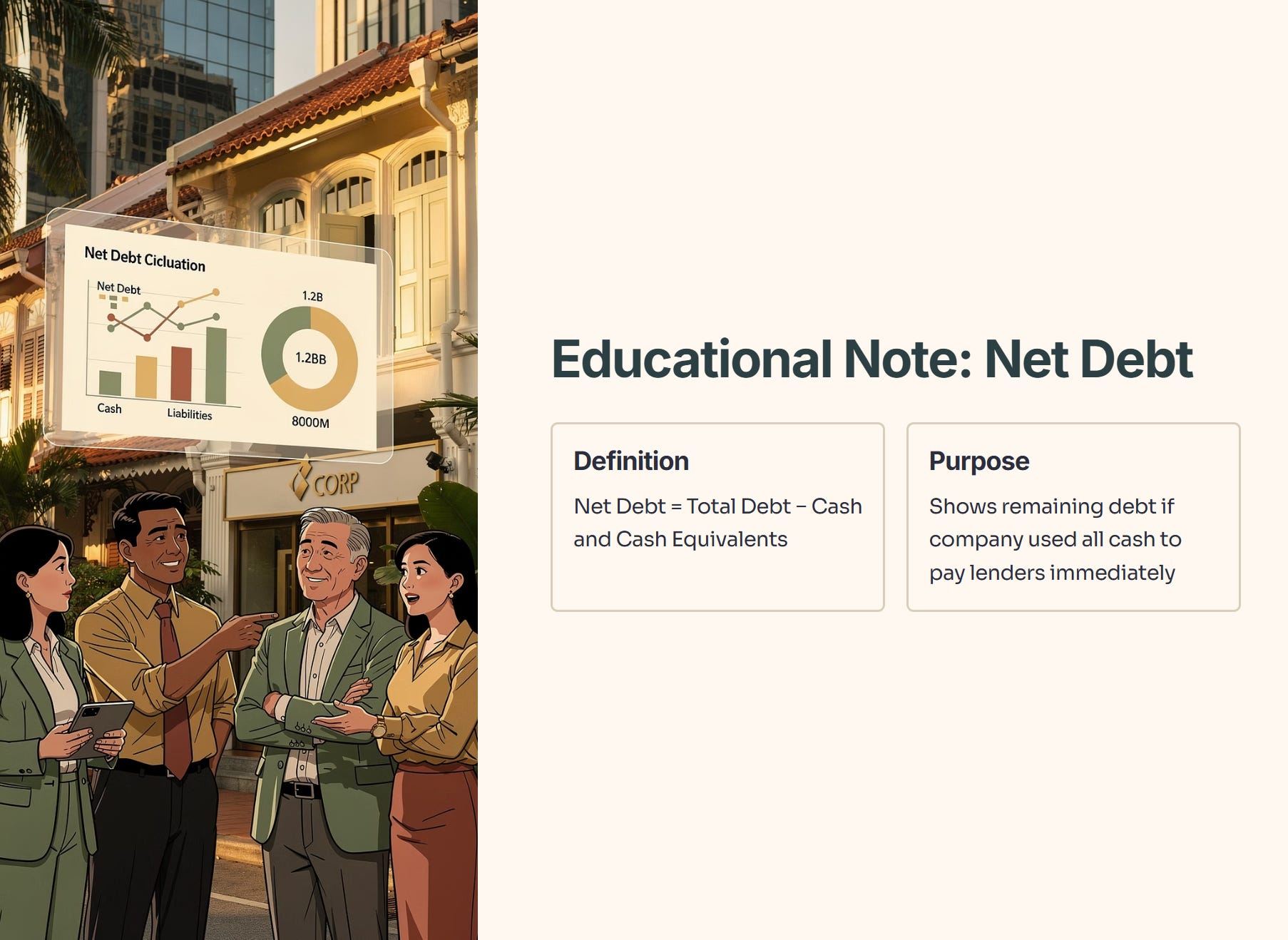

🎓 Educational Note: Net Debt

Net Debt is calculated as:

Net Debt=(Total Debt−Cash and Cash Equivalents)

It shows how much debt would remain if the company used all its available cash to pay off lenders immediately.

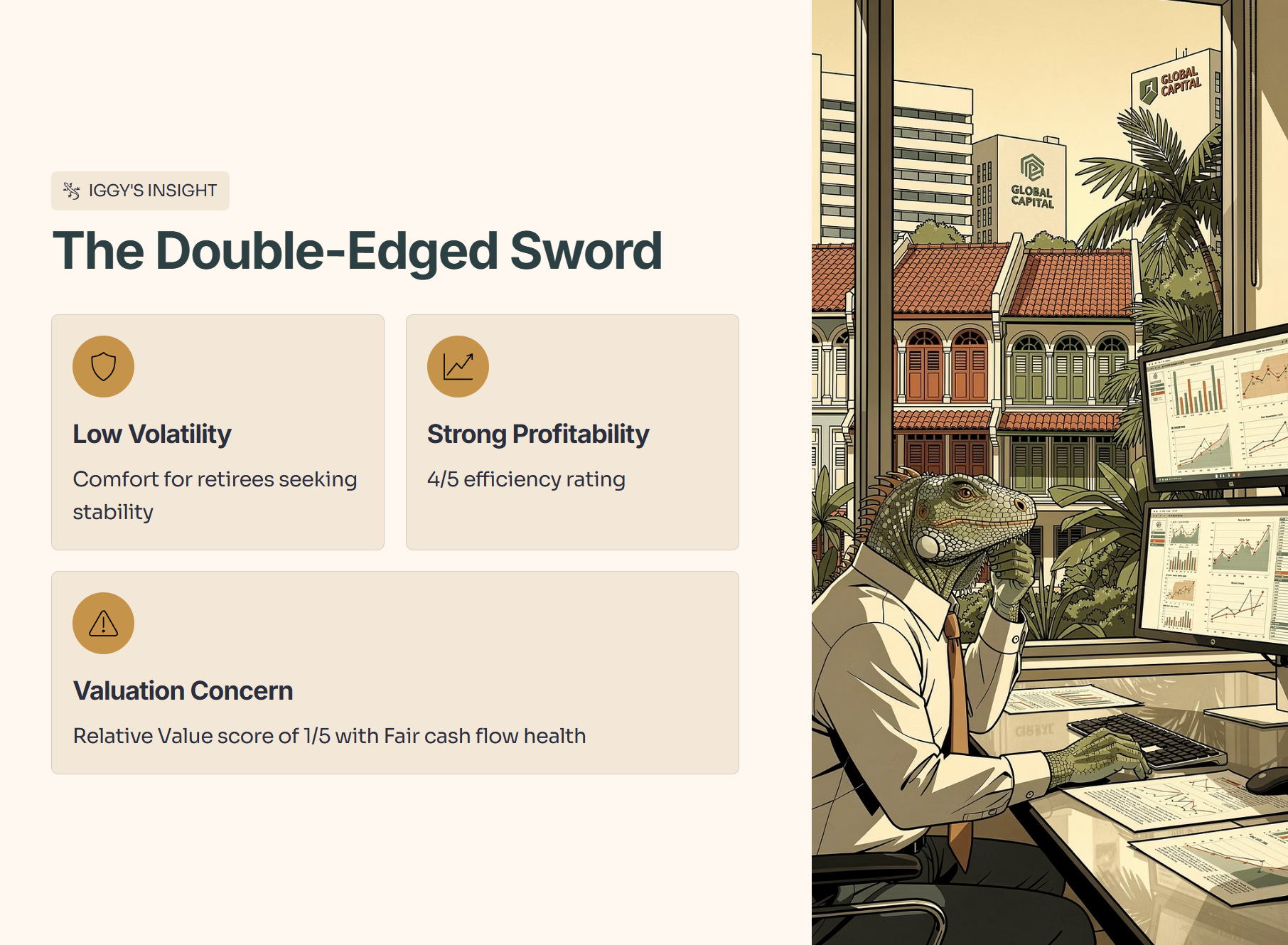

🦎 Iggy’s Insight:

Leverage is a double-edged sword. InvestingPro notes the stock generally trades with low price volatility, which is a comfort for retirees. But at a 4/5 for Profitability, they are efficient. The real worry for a capital-preservation investor is that Relative Value score of 1/5. You are paying top-shelf prices for a company with “Fair” cash flow health.

Step 2: The Wealth Check (Dividends & Cash Flow)

The Narrative: “Are they paying us from profit or debt?”

ST Engineering’s Free Cash Flow (FCF) staged a massive recovery in 2024, jumping to S$1.24 billion. This supports their current dividend, even as the share price run-up has compressed the yield.

The Data: Payout & FCF

The current forward dividend yield is ~1.63%. While lower than historical norms, it is now better covered by earnings than in previous years.

🦎 Iggy’s Insight:

InvestingPro flags that the stock is trading at a high earnings multiple. For a retiree, the yield is currently underwhelming compared to a plain-vanilla T-Bill. The bullish thesis rests on the assumption that the “Space Agency” catalyst will drive profits high enough to force that “Incremental Dividend” policy to pay out significantly more in 2027 and beyond.

Step 3: The Price Check (Valuation & Peers)

The Narrative: “Is it cheap, or is it just ‘cheap’ for a reason?”

By every standard metric, ST Engineering is currently priced for perfection. InvestingPro is flashing red on its valuation metrics.

The Data: P/E, P/B vs Peers

The stock trades at a trailing P/E of ~40x, which InvestingPro highlights as high relative to near-term earnings growth.

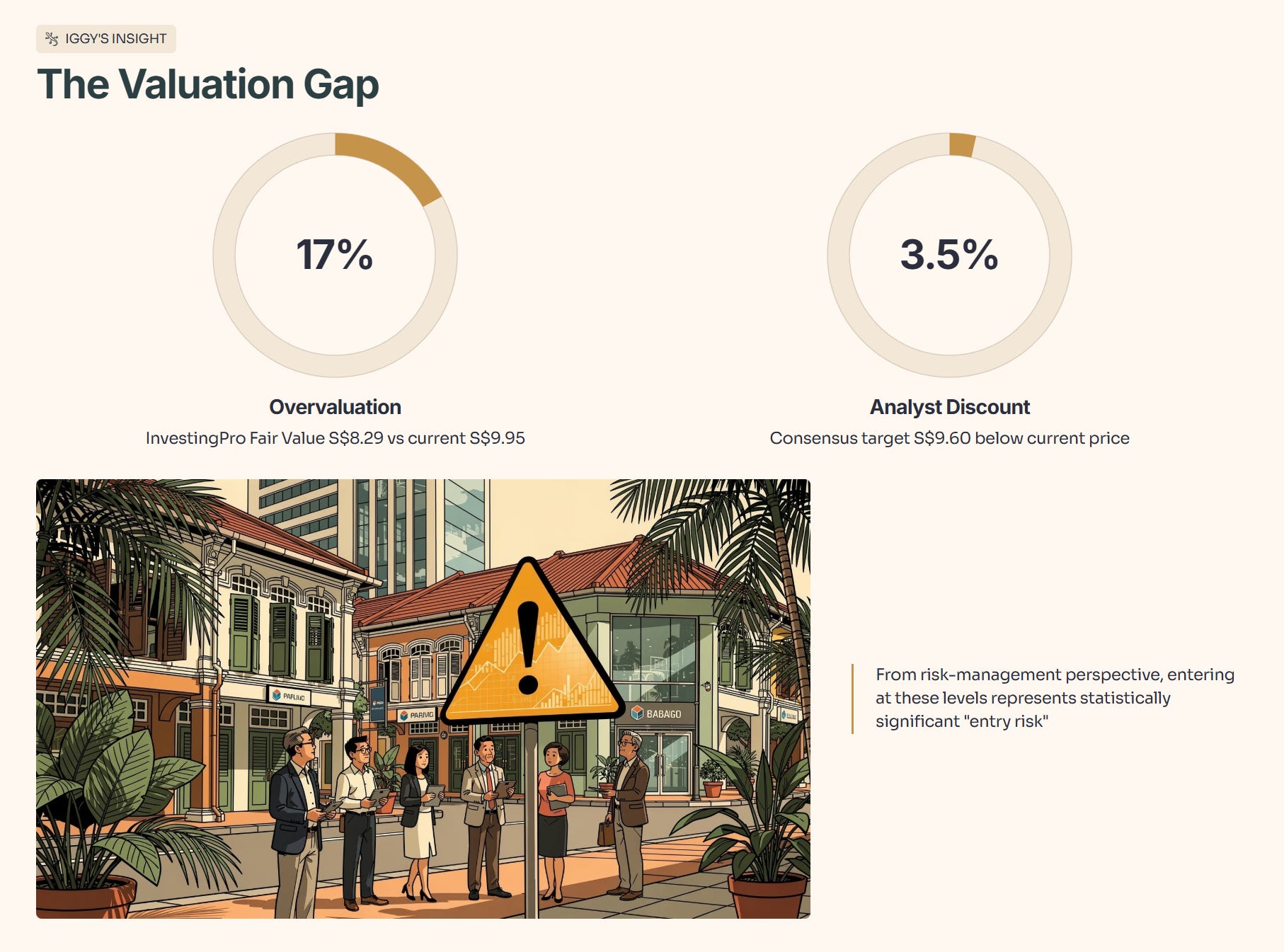

🦎 Iggy’s Insight:

InvestingPro’s Fair Value of S$8.29 suggests the stock is currently overvalued by nearly 17%. Even the consensus analyst target of S$9.60 sits below today’s price of S$9.95. From a risk-management perspective, entering at these levels represents an “entry risk” that is statistically significant.

Step 4: The Future Check (Scenarios & Fair Value)

The Focus: The InvestingPro Model

Here’s the playbook I’d use for ST Engineering at today’s price if I were protecting a retiree’s nest egg.