No Market Maker = No Exit Liquidity on SGX AAPL, NVDA | EP1595🦖

And it’s not SGD bridge access paying you. It’s the 4.0% CPF SA you’re giving up for 0.02%

SGX-Nasdaq Bridge: AAPL, NVDA Analysis

The Bridge Is Open — But Read the Fine Print

Under the shadows of the skyscrapers at Shenton Way, where the humidity of the Singapore River meets the refrigerated air of institutional trading floors, a quiet regulatory tectonic shift is reaching its final alignment. The formal activation of the SGX-Nasdaq dual-listing bridge in June 2026 marks a moment where the architectural redesign of the Singapore equity market moves from a policy white paper to a live digital corridor.

This strategic initiative, codified through the Securities and Futures (Amendment) Bill 2026, is not just a technical update for the back-office systems of the exchange. It represents a sophisticated repositioning of Singapore’s capital markets to bridge the liquidity gap between the growth enterprises of Asia and the deep institutional pools of the United States.

In This Article:

The Bridge Is Open — But Read the Fine Print

The Hidden Toll: FX Drag and the Secondary Listing Trap

The Yield Verdict: What the Numbers Actually Say

Macro Evidence, Sector Watch, Scenario Matrix

The Forensic Stress Test: Who Should Cross the Bridge?

The Secondary Listing Trap — and the Only Sanctuary That Matters

Most financial content is built around excitement — what is surging, what is breaking out, what you might be missing. I am deliberately building something different. Retirement-grade investing is not exciting. It is disciplined, forensic, and it is designed to still be working when you need it most. For the heartland investor in Singapore, typically anchored to the stability of local banks and the distributions of REITs, this bridge offers something long desired but historically expensive: a direct pathway to Magnificent Seven constituents like Apple (AAPL) and Nvidia (NVDA) via Singapore Dollar (SGD) denominated accounts.

The stakes for the Singaporean retirement portfolio are high because this bridge introduces complex forensic considerations that go far beyond the convenience of a local ticker symbol. We are looking at a total cost of ownership problem that includes currency-pegged price volatility and the potential for a secondary listing trap where local liquidity fails to match the primary exchange depth in New York or London.

On the surface, the idea of buying Apple shares as easily as one buys DBS or SingTel makes perfect sense for a modern portfolio. But here is the uncomfortable truth that the data from the Global Listing Board (GLB) reveals: the convenience of the bridge may actually be a high-priced luxury for those who do not account for the synthetic nature of local pricing and the hidden friction of the secondary market.

The Forensic Gap here is the distance between the institutional optimism surrounding the bridge launch and the operational reality for an investor managing Central Provident Fund (CPF) or Supplementary Retirement Scheme (SRS) capital. While the Ministry of Trade and Industry and the Monetary Authority of Singapore (MAS) emphasize the S$3.95 billion deployed through the Equity Market Development Programme (EQDP) to support liquidity, the forensic data suggests that the SGD-denominated shares on the SGX still face a risk of shallow order books compared to their primary USD counterparts. For the individual investor, the excitement of owning the future must be weighed against the structural mechanics of a regulatory safe harbor that protects the issuer more than the retail subscriber.

Iggy’s Insight

The psychological gap in the market right now is the belief that dual listing automatically confers the same quality of execution found on the Nasdaq. Institutional voices focus on the harmonised prospectus and regulatory alignment, but they rarely mention that for a retail investor, the best price is often a function of high-frequency market makers who may not see enough volume in the Singapore tranche to narrow the spreads. The reframing we need is simple: a bridge is only as good as the traffic it carries. If the local traffic is thin, the toll you pay in bid-ask spreads will eventually consume the very capital gains you crossed the bridge to find.

The Hidden Toll: FX Drag and the Secondary Listing Trap

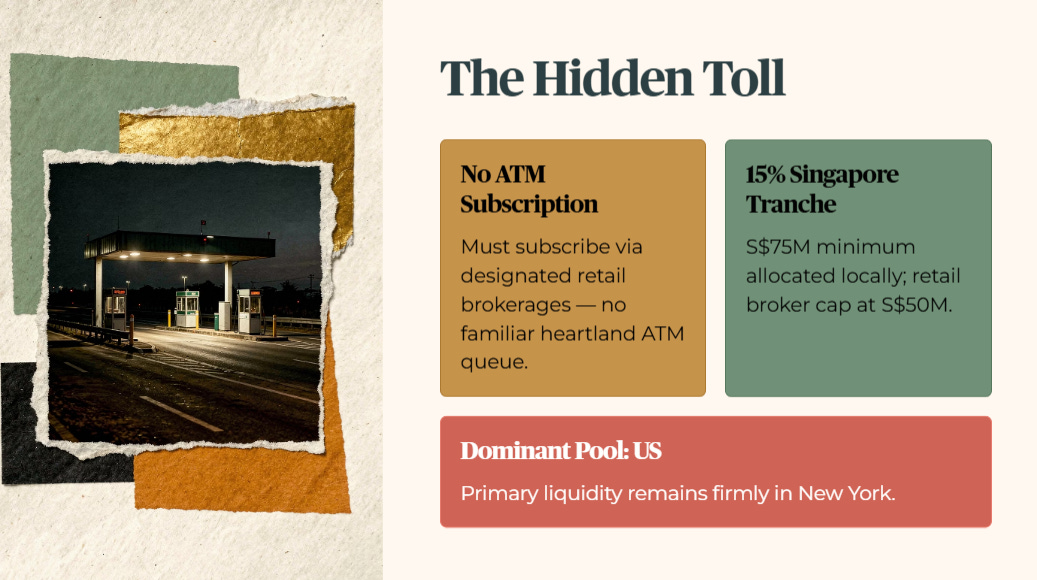

The shift into the 2026 regulatory landscape has introduced several novel mechanics for retail participation that change the traditional calculus of the Singapore wallet. In a departure from the traditional Initial Public Offerings (IPOs) heartland investors are used to, there is no separate Automated Teller Machine (ATM) subscription for the Global Listing Board. Instead, anyone in Toa Payoh or Jurong looking to participate must subscribe through designated retail brokerages. The framework mandates that 15% of the IPO value or S$75 million, whichever is higher, must be allocated to the Singapore tranche. But this comes with a specific reservation for retail brokers capped at S$50 million. This ensures a baseline of local availability, but it also acknowledges that the dominant liquidity pool remains firmly in the United States.

The cost of living impact of this bridge launch manifests most clearly through the FX spread, which acts as a hidden tax on heartland wealth. For an investor buying Apple or Nvidia through a traditional bank’s multi-currency account, the exchange rate spread often carries a markup of 0.5% to 1.0%. On a S$20,000 investment, that represents an immediate loss of S$150 before the trade is even executed. While the GLB allows trades in SGD to eliminate this upfront friction, the price remains a synthetic derivative of the Nasdaq quote. If the Singapore Dollar strengthens by 5% against the US Dollar, the local price of Apple will drop by that same 5% even if the stock price in New York remains flat. This currency drag is a direct hit to the purchasing power of an SRS account that is intended for long-term domestic use.

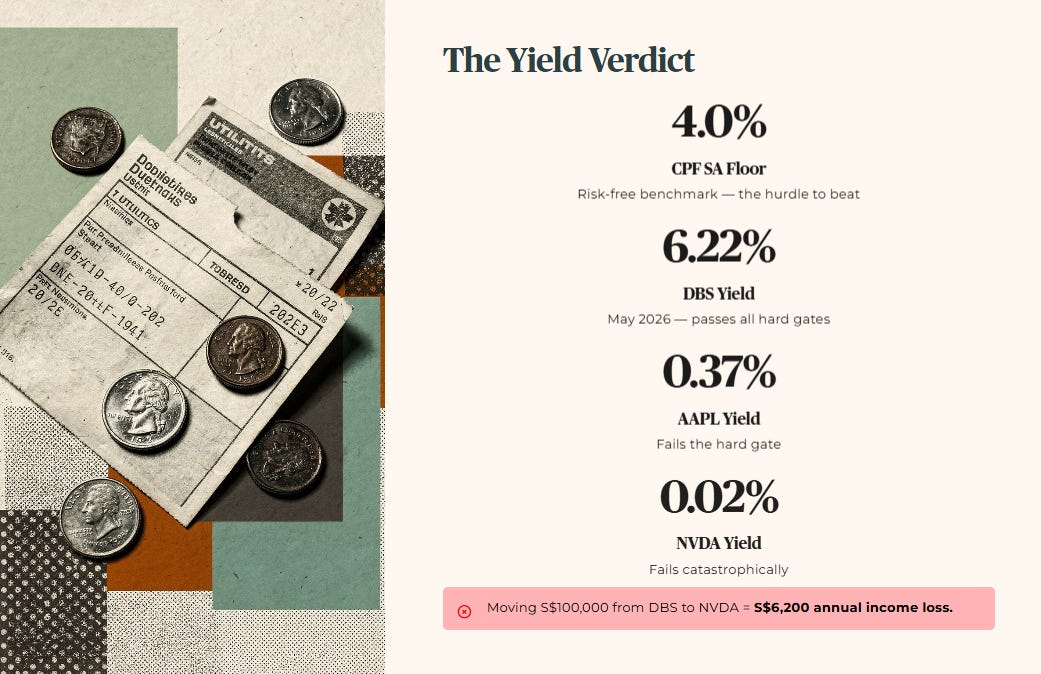

The Yield Verdict: What the Numbers Actually Say

When we look at the CPF and SRS calculus, the macro environment of 2026 makes the risk-free benchmark of the CPF Special Account (SA) at 4.0% an incredibly high hurdle for tech giants to clear. Neither Apple, with a yield of 0.37%, nor Nvidia, at 0.02%, comes close to the Sanctuary returns available in the Singaporean domestic market.

For a heartland retiree, moving S$100,000 from a local bank like DBS, which currently yields 6.22% in May 2026, into Nvidia results in an immediate income loss of S$6,200 per year. This is the heartland paradox of the 2026 bridge: you can own the most innovative companies in the world while simultaneously struggling to pay your monthly utility bills because of a catastrophic failure in income yield.

Iggy’s Insight

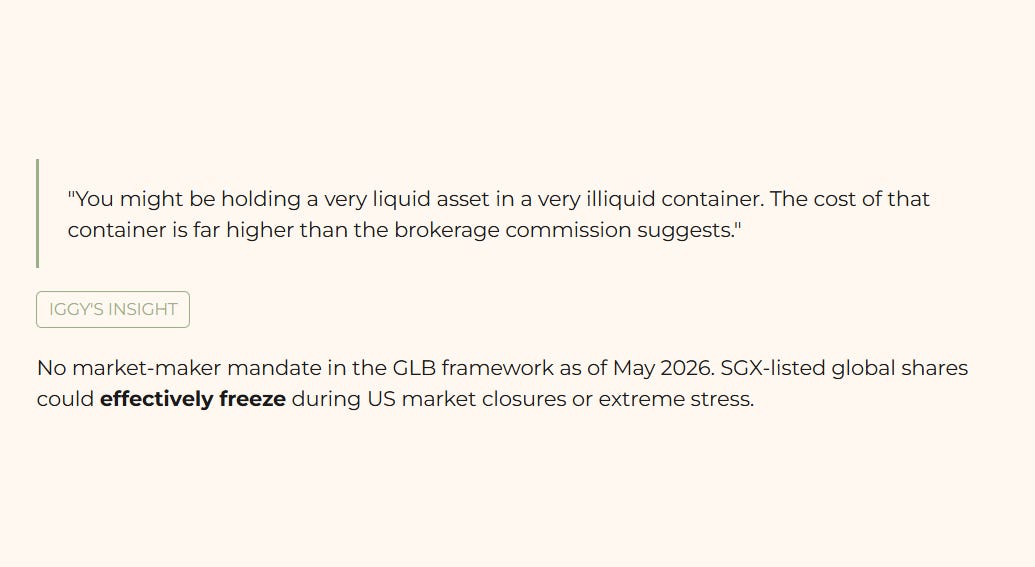

The second-order effect that most retail investors are missing is the absence of a market-maker mandate within the GLB framework as of May 2026. While the EQDP provides institutional support, there is no guarantee of continuous quoting during local market hours. This creates a structural liquidity risk where the SGX-listed shares of a global giant could effectively freeze during US market closures or periods of extreme global stress. The forensic reality is that you might be holding a very liquid asset in a very illiquid container. The cost of that container is far higher than the brokerage commission suggests.

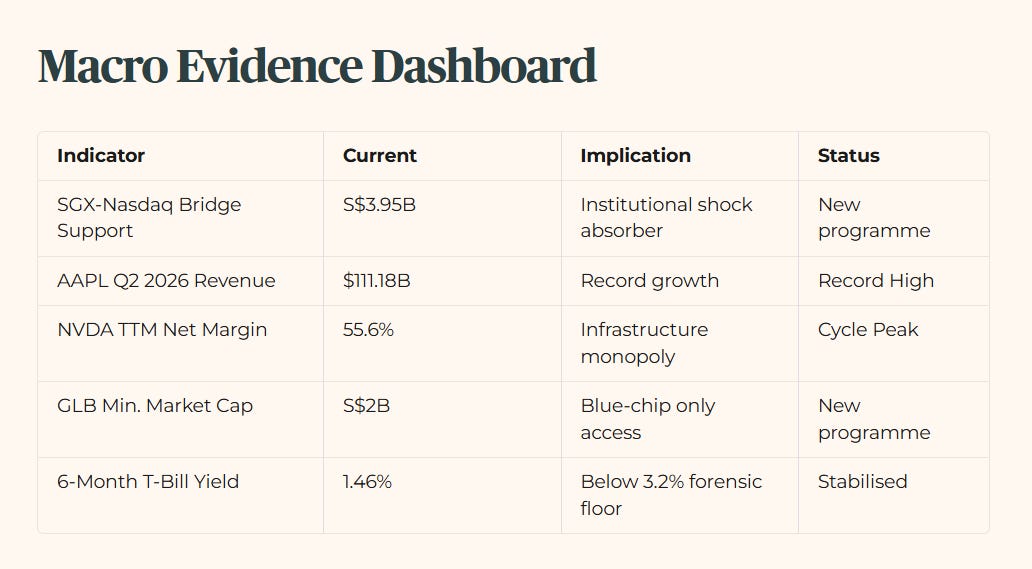

Macro Evidence, Sector Watch, Scenario Matrix

The analytical conclusion for the June 2026 bridge launch is that while it democratises access to global tech, it does so at the cost of a significant yield sacrifice and a hidden liquidity premium.

Table 1: Macro Evidence Dashboard

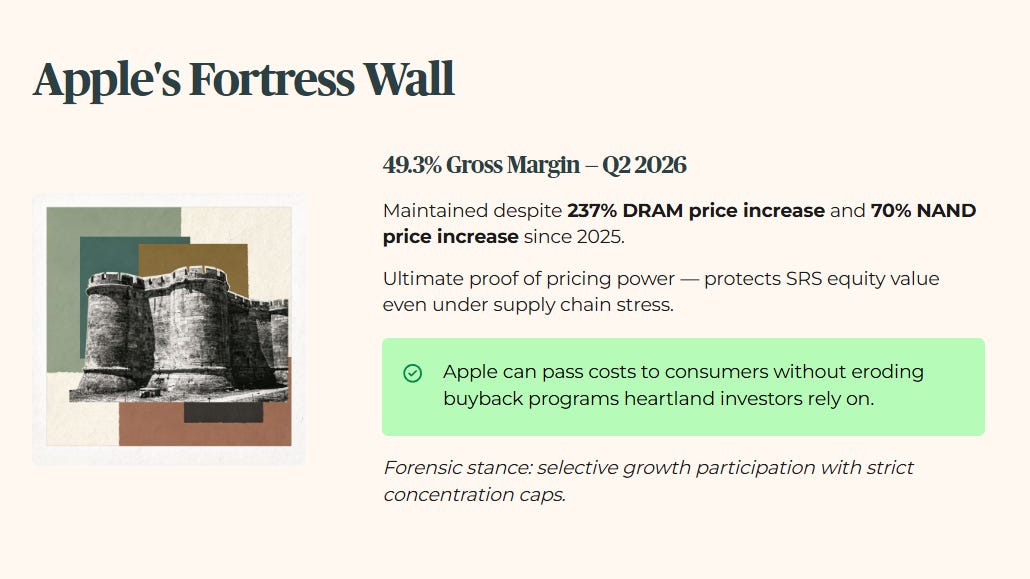

The forensic linchpin of this entire dossier is the 49.3% gross margin maintained by Apple in Q2 2026 despite a 237% increase in DRAM prices and a 70% increase in NAND prices since 2025. This number is the ultimate proof of pricing power. For a 55-year-old investor in Tampines managing an SRS account, this margin is the Fortress wall that protects their equity value even when global supply chains are under immense stress. It means that Apple can pass on costs to the consumer without eroding the capital that supports the buyback programs heartland investors are relying on for growth, even if the dividend yield remains negligible.

The overarching forensic stance across the SGX tech and global listing universe is one of selective growth participation with a strict cap on concentration to protect retirement-grade income.

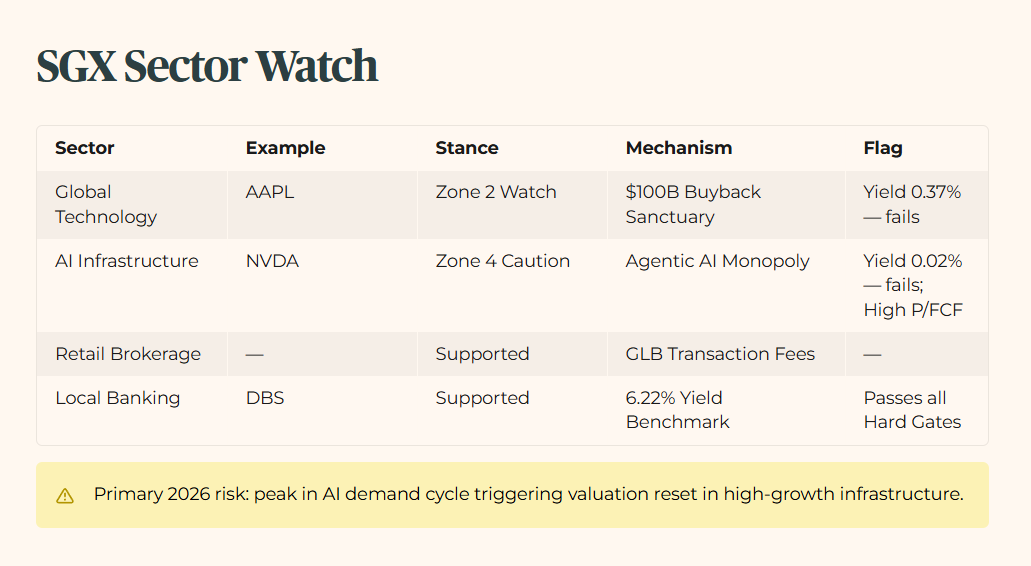

Table 2: SGX Sector Watch

The primary risk for 2026 is a potential peak in the AI demand cycle that could trigger a reset in the valuation of high-growth infrastructure plays.

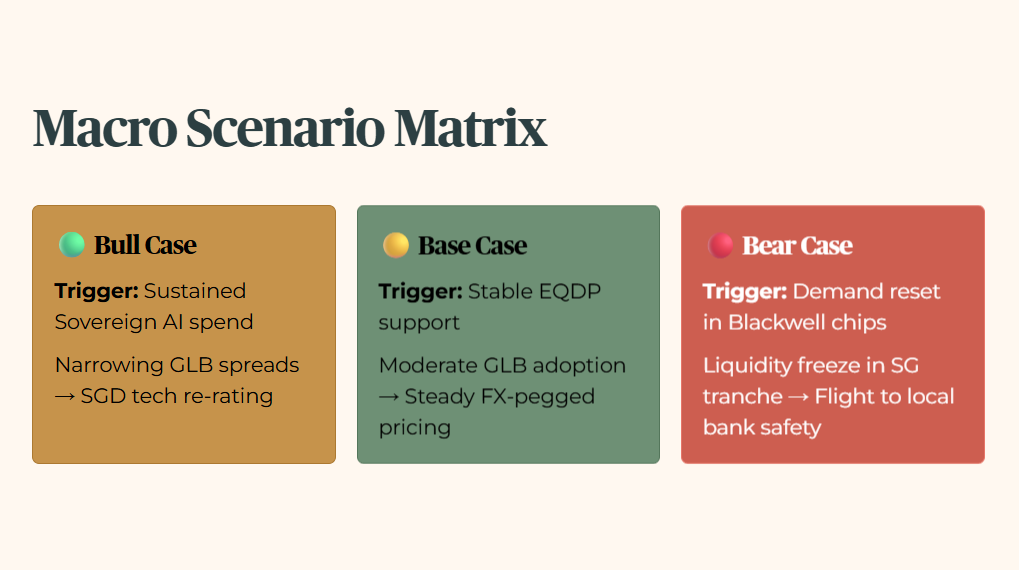

Table 3: Macro Scenario Matrix

Given the scenario matrix above, every heartland investor should be asking three forensic stress-test questions.

First, if you hold a tech-heavy position in your SRS, can your portfolio survive a 5% currency drag if the SGD strengthens significantly against the USD?

Second, for your blue-chip local bank holdings, does the diversification benefit of the SGX-Nasdaq bridge outweigh the 6,200 basis point yield loss you accept when switching from DBS to Nvidia?

Third, if you are using the CPF Investment Scheme to access these global names, do you have the cash buffer to cover your monthly obligations if the secondary market liquidity on the SGX thins out during a US market correction?

Because once you layer those three stress-test questions on top of the 3.2% forensic floor in the next section, the age-band verdict on who should actually cross this bridge — and who should stay anchored in DBS — looks very different from the headline story.