Singapore Stocks Q4 2025: Winners, Losers & My Portfolio Moves

Are your October winners setting you up for Q4 gains—or a painful correction?

You watched Singapore stocks hit record highs in October 2025. The STI crossed 4,400 points. Your portfolio looked pretty good. But here’s what most investors miss: October’s winners don’t automatically become November’s champions. Some are just getting started. Others are running on fumes. The difference between the two will determine whether you end Q4 celebrating or cursing your decisions. Let me show you exactly who deserves your money going into the final quarter and who you should avoid like the plague.

The Singapore market hit new all-time highs in October 2025, with the STI touching 4,474 points. This marks a remarkable 22.65% gain over the past 12 months. But not all stocks participated equally in this rally. Some surged on real fundamentals. Others rode momentum that’s already fading. The key question isn’t what worked in October—it’s what will work in Q4.

In This Article:

• The Winners Circle: October’s Top Performers

• The Performance Comparison Table

• The Losers: October’s Underperformers

• Sector-by-Sector Q4 Buy/Hold/Sell Guide

• The Fed Factor: How Rate Cuts Shape Q4

• Risk Factors: What Could Derail the Q4 Rally

• Action Plan: Concrete Steps for Q4

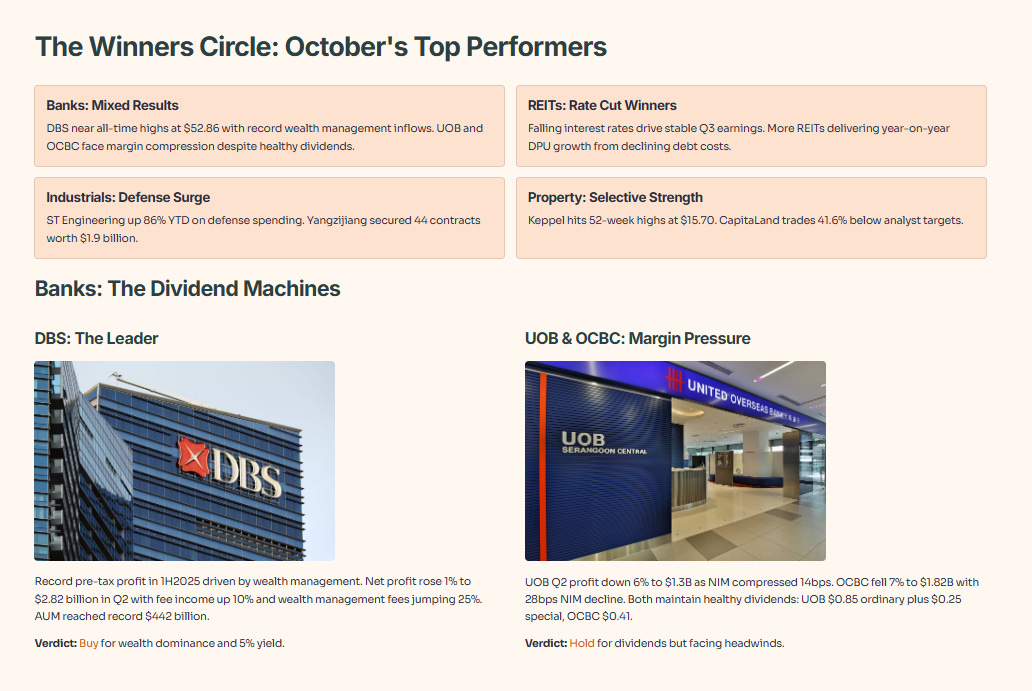

• The Bottom LineThe Winners Circle: October’s Top Performers

October delivered distinct winners across multiple sectors. Banks showed mixed performance despite record earnings. REITs benefited from falling interest rates. Industrial stocks rode defense spending and shipbuilding momentum. Property counters saw selective strength.

Banks: The Dividend Machines Keep Churning

DBS led the banking sector with its share price near all-time highs at $52.86. The bank posted record pre-tax profit in the first half of 2025, driven primarily by massive inflows into its wealth management business. Net profit rose 1% year-on-year to $2.82 billion in Q2 2025, with fee income surging 10% and wealth management fees jumping 25%.

UOB and OCBC faced more headwinds. UOB reported Q2 2025 net profit of $1.3 billion, down 6% year-on-year due to net interest margin compression of 14 basis points. OCBC’s net profit fell 7% to $1.82 billion as NIM declined by 28 basis points. Despite lower profits, both banks maintained healthy dividends. UOB declared $0.85 in ordinary dividends for 1H2025 plus a special dividend of $0.25. OCBC proposed $0.41 per share.

The key driver separating DBS from its peers: wealth management dominance. DBS gained market share as wealth management assets under management reached a record $442 billion. All three banks are pivoting from rate-driven profits to fee-based growth built on wealth management, cross-border connectivity, and sustainable finance.

For Q4, banks face continued NIM compression but should benefit from lower funding costs as deposit interest rate cuts implemented in Q2 take effect. Credit costs remain manageable with stable non-performing loan ratios.

Buy, Hold, or Sell? DBS remains a Buy for its wealth management dominance and 5% dividend yield. UOB and OCBC are Holds—solid dividend plays but facing margin pressure. All three benefit from capital return programs including share buybacks.

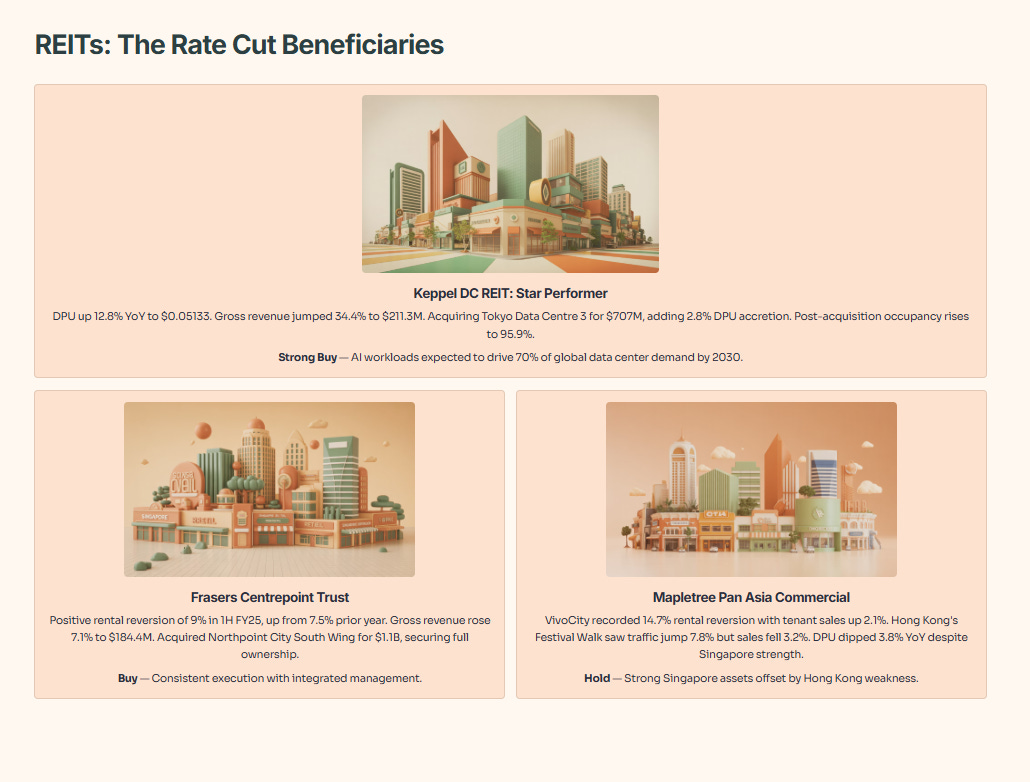

REITs: The Rate Cut Beneficiaries

Singapore REITs emerged as clear winners from falling interest rates. The sector is expected to deliver stable Q3 earnings driven by easing debt costs and resilient operating metrics. More REITs are now delivering year-on-year distribution per unit growth helped by declining average interest expenses.

Keppel DC REIT stands out as the star performer. The data center REIT reported outstanding results for 1H2025 with DPU increasing 12.8% year-on-year to $0.05133. Gross revenue jumped 34.4% to $211.3 million and net property income climbed 37.8% to $182.8 million. The REIT is acquiring a 98.47% stake in Tokyo Data Centre 3 for approximately $707 million, which is DPU-accretive by 2.8%. Post-acquisition, portfolio occupancy will rise to 95.9% with weighted average lease expiry of 7.2 years.

Frasers Centrepoint Trust delivered solid retail REIT performance. The REIT achieved positive rental reversion of 9% for 1H FY25, higher than the 7.5% logged a year ago. Gross revenue rose 7.1% year-on-year to $184.4 million with net property income up 7.3%. The REIT successfully acquired Northpoint City South Wing for around $1.1 billion, giving it full ownership of Northpoint City.

Mapletree Pan Asia Commercial Trust showed divergent performance between its Singapore and Hong Kong assets. VivoCity recorded rental reversion of 14.7% with tenant sales rising 2.1% year-on-year. However, Hong Kong’s Festival Walk experienced opposite trends—shopper traffic jumped 7.8% but tenant sales fell 3.2%. DPU dipped 3.8% year-on-year for the latest quarter despite strong Singapore performance.

Buy, Hold, or Sell? Keppel DC REIT is a Strong Buy. Data center demand driven by AI workloads is expected to account for 70% of global data center demand by 2030. Frasers Centrepoint Trust is a Buy for its consistent execution and full Northpoint ownership. Mapletree Pan Asia Commercial Trust is a Hold—strong Singapore assets offset by Hong Kong weakness.

Industrials: Defense and Shipbuilding Shine

Singapore Technologies Engineering delivered a turnaround performance after being among August’s worst performers. The defense and aerospace conglomerate posted robust 1H2025 results with revenue rising 7.2% year-on-year to $5.9 billion, with all three business segments contributing. The stock delivered approximately 86% year-to-date returns as of late September, riding global defense spending increases and aerospace recovery.

Yangzijiang Shipbuilding emerged as a top gainer, rising 1.9% on October 16 to $3.26. The shipbuilder secured 44 effective contracts in 2025 with a combined value of $1.9 billion. First-half 2025 net profit attributable to shareholders rose 37% year-on-year to RMB 4.2 billion with gross margin improving by 7.8 percentage points to 34.5%. The orderbook stood at 258 vessels as of early September: 125 container ships, 64 tankers, 41 bulk carriers, and 28 LNG/LPG carriers.

Buy, Hold, or Sell? ST Engineering is a Buy for long-term defense spending trends and aerospace recovery. Yangzijiang Shipbuilding is a Hold—strong fundamentals but recent momentum may have priced in near-term gains.

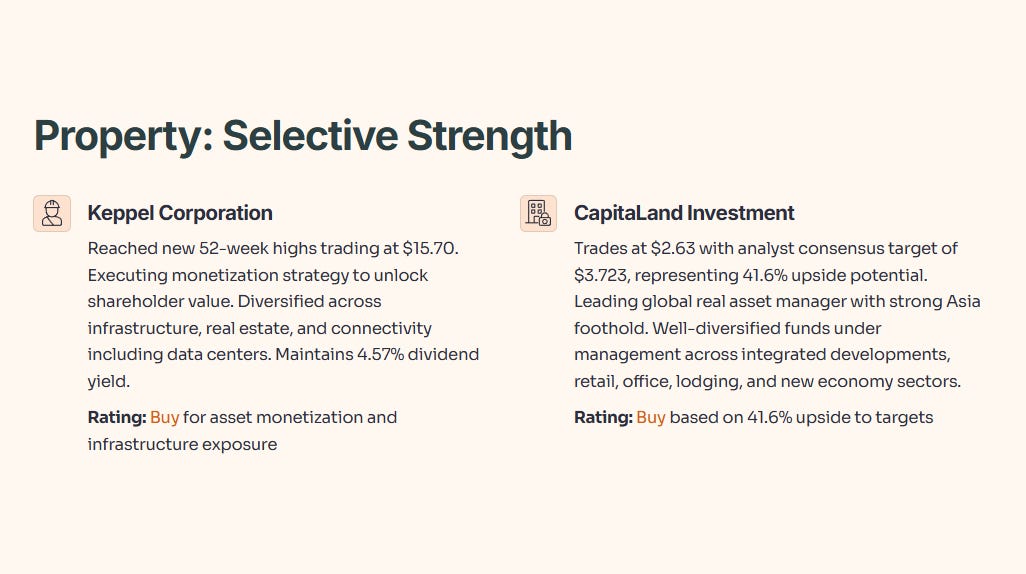

Property: Selective Strength

Keppel Corporation reached new 52-week highs in October, trading as high as $15.70. The conglomerate is executing its monetization strategy to unlock shareholder value. The company’s diversified business model spans infrastructure, real estate, and connectivity including data centers. Keppel maintains a 4.57% dividend yield.

CapitaLand Investment trades at $2.63 with analyst consensus price target of $3.723, representing 41.6% upside potential. The company is a leading global real asset manager with strong Asia foothold and well-diversified funds under management across integrated developments, retail, office, lodging, and new economy sectors.

Buy, Hold, or Sell? Keppel is a Buy for its asset monetization strategy and infrastructure exposure. CapitaLand Investment is a Buy based on the 41.6% upside to analyst targets and diversified real estate exposure.

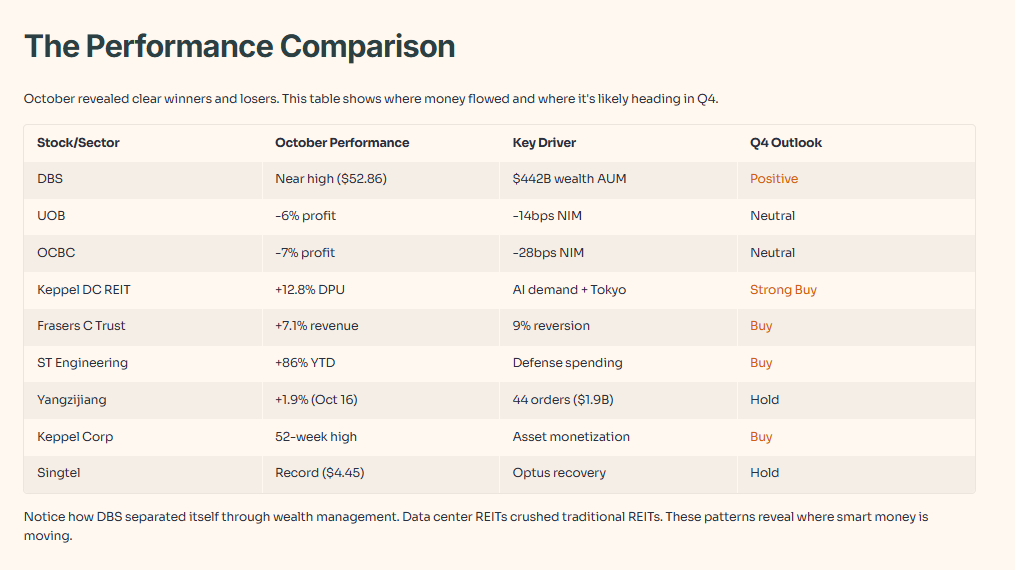

The Performance Comparison Table

This table shows you exactly where the money flowed in October and where it’s likely to flow in Q4. Notice how DBS separated itself from UOB and OCBC through wealth management. Notice how data center REITs crushed traditional REITs. These patterns tell you what the smart money is doing.

The Losers: October’s Underperformers

Not every stock participated in October’s rally. Several blue-chips struggled or faced sector-specific headwinds that could persist into Q4.

Singtel: The Rally That Ran Too Far

Singtel hit an all-time high of $4.45 in October after a strong 35.6% year-to-date rally. The telco delivered strong Q1 FY2025/26 results with underlying net profit up 14% to $686 million. Optus revenue rose 4% year-on-year with EBIT surging 36% on higher mobile customer base and improved average revenue per user.

But the rally may have run ahead of fundamentals. Singapore’s core business revenue remained flat with mobile service revenue dropping 11% year-on-year as roaming and voice services weakened. Lingering Optus risks from recent outages remain a concern. The recent run-up provides a lower margin of safety for new investors.

Hold—But Don’t Add The stock remains a fairly resilient dividend play with potential growth in data centers and associates. However, the recent rally has reduced the margin of safety. Current holders should hold for the 2.89% dividend yield. New investors should wait for a pullback.

Property Stocks with China Exposure

Hongkong Land trades at a price-to-book of just 0.45, making it Singapore’s most undervalued blue-chip property stock. Most of its portfolio is concentrated in Hong Kong (57%). The company struggled with poor performance and a declining share price due to exposure to Hong Kong and China properties. Despite a 5% dividend yield, investors lost 5.58% after holding for the past ten years through 2024.

The company announced a strategic pivot in October 2024 to focus on property investment over development, aiming to generate more recurring income. However, execution risk remains high given China’s ongoing property sector challenges.

Avoid The 0.45 price-to-book ratio looks tempting, but China property exposure remains toxic. The strategic pivot will take years to execute. Better opportunities exist elsewhere in Singapore’s market.

S-Chips: The Governance Risk Premium

There are currently 103 Chinese firms listed on SGX (known as S-Chips) as of May 2025, representing 14% of all listed companies. These companies face persistent concerns over corporate governance and transparency despite SGX’s efforts to attract more Chinese listings. Several accounting scandals between 2007 and 2012 led many S-Chip firms to fail SGX listing requirements.

While some S-Chips trade at depressed valuations, the governance risk premium remains justified. Foreign investors continue to express caution regarding China’s tightly regulated financial landscape and capital controls.

Avoid Unless you have deep expertise in Chinese company analysis and accept the governance risks, avoid S-Chips. Singapore offers plenty of high-quality alternatives without the governance uncertainty.

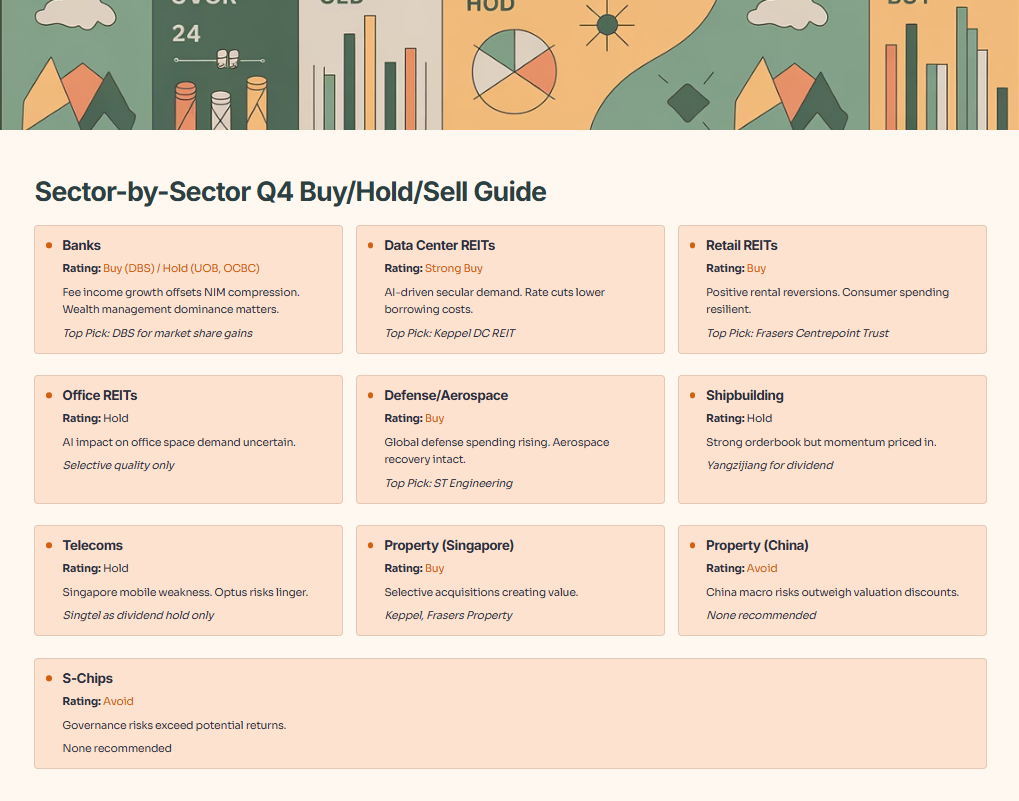

Sector-by-Sector Q4 Buy/Hold/Sell Guide

Use this table as your decision-making framework. Don’t get distracted by noise. Stick to sectors with strong fundamentals and clear catalysts. Avoid sectors where cheap valuations mask serious structural problems.

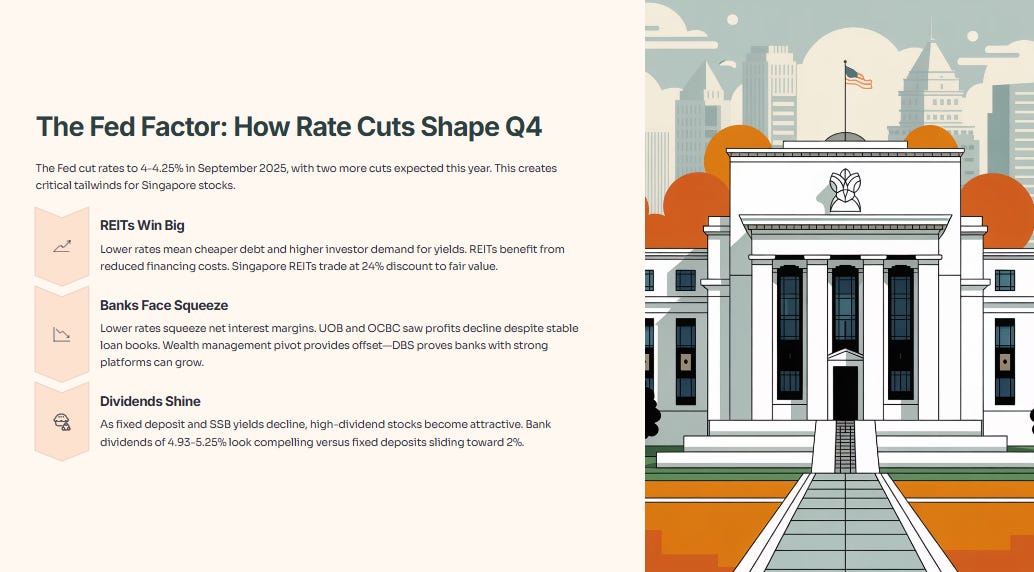

The Fed Factor: How Rate Cuts Shape Q4

The US Federal Reserve’s rate cutting cycle provides critical tailwinds for Singapore stocks. The Fed cut rates to a range of 4% to 4.25% in September 2025, with two more cuts expected this year. This creates several important effects for Singapore investors.

REITs Are the Biggest Winners

Lower rates mean cheaper debt and higher investor demand for yields. REITs benefit directly from reduced financing costs. Singapore REITs are trading at a 24% discount to fair value, creating an attractive entry point as borrowing costs fall.

Data center REITs particularly benefit. These assets have long-term leases with built-in rent escalations and are positioned to capture AI-driven demand growth. As rates fall, the present value of these future cash flows increases, supporting higher valuations.

Banks Face Margin Squeeze

Lower interest rates typically squeeze net interest margins—the key profitability metric for banks. This explains why UOB and OCBC saw profits decline even as loan books remained stable. However, the pivot to fee-based wealth management revenue provides an offset. DBS demonstrates that banks with strong wealth platforms can grow earnings even as lending margins compress.

High-Dividend Stocks Become More Attractive

As fixed deposit rates and Singapore Savings Bond yields decline, high-dividend stocks become attractive alternatives. Singapore bank dividends ranging from 4.93% to 5.25% look compelling compared to fixed deposits sliding toward 2%.

Risk Factors: What Could Derail the Q4 Rally

Several risks could interrupt Singapore’s market momentum heading into Q4.