Singapore's High-Yield REIT Trap: Why Double-Digit Yields Demand Your Caution

Chasing 8–10% yields? Read this first—learn which high-dividend Singapore REITs are real income machines and which are ticking traps, plus a clear game plan for CPF/SRS investors.

A double-digit dividend yield is the siren song of the income investor—it’s alluring, hypnotic, and if you sail too close, it can wreck your portfolio on the rocks of a payout cut. Right now, Singapore’s highest-yielding REITs are broadcasting that song loud and clear. But smart money doesn't just hear the yield; it listens for the reason behind the noise. In this piece, I’ll break down the warning signals flashing from these 8%+ yields, show you which names might still be worth a look, and give you my framework as a Singapore-based investor for building income with discipline—not desperation.

The allure of high yields can blind investors to core risks. In today’s market, a double-digit yield is rarely “free money.” It often means stress in the business, balance sheet, or both. In this piece, I’ll break down what those signals mean, which names may still be worth a look, and how a Singapore-based investor can build income with discipline. Expect a clear framework, simple risk checks, and direct guidance.

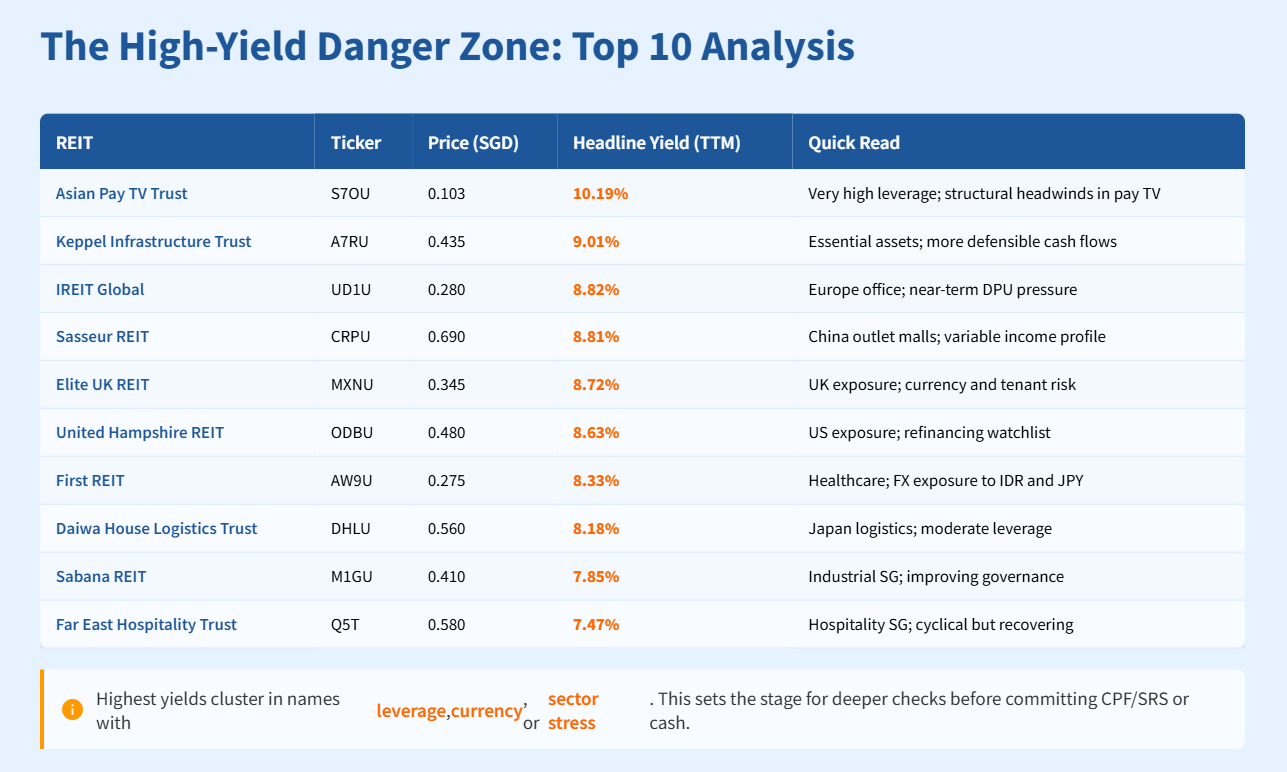

The High-Yield Danger Zone: Top 10 Analysis

High yields catch the eye, but what’s driving those high numbers is even more important. Here’s a look at 10 REITs to watch, plus the key checks you should make before you invest.

This table gives you a quick snapshot of yields and the main risk factors. You’ll notice the highest yields often belong to REITs dealing with high debt, currency swings, or sector troubles. Use this as a starting point for deeper checks before putting in your CPF, SRS, or cash.

Asian Pay Television Trust (APTT) shows the highest yield, but the business is shrinking. High debt and currency swings mean payouts are shaky—this is your classic yield trap.

Keppel Infrastructure Trust (KIT) offers about 9% yield, but with a stronger base. Its assets are essential, so cash flows are steadier and debt is well-managed. This makes KIT a rare high-yield REIT that could stand the test of time.

IREIT Global pays a good yield now, but it’s heavy on European offices. That brings risks with vacant space and loans coming due. Its payout could stay under pressure as properties get repositioned.