Singapore's Industrial REIT Champion Faces a Crossroads: Is CLAR Still Your Best Bet?

The S$724.6 million Singapore acquisition spree that most investors completely missed tells you everything about CLAR's real strategy.

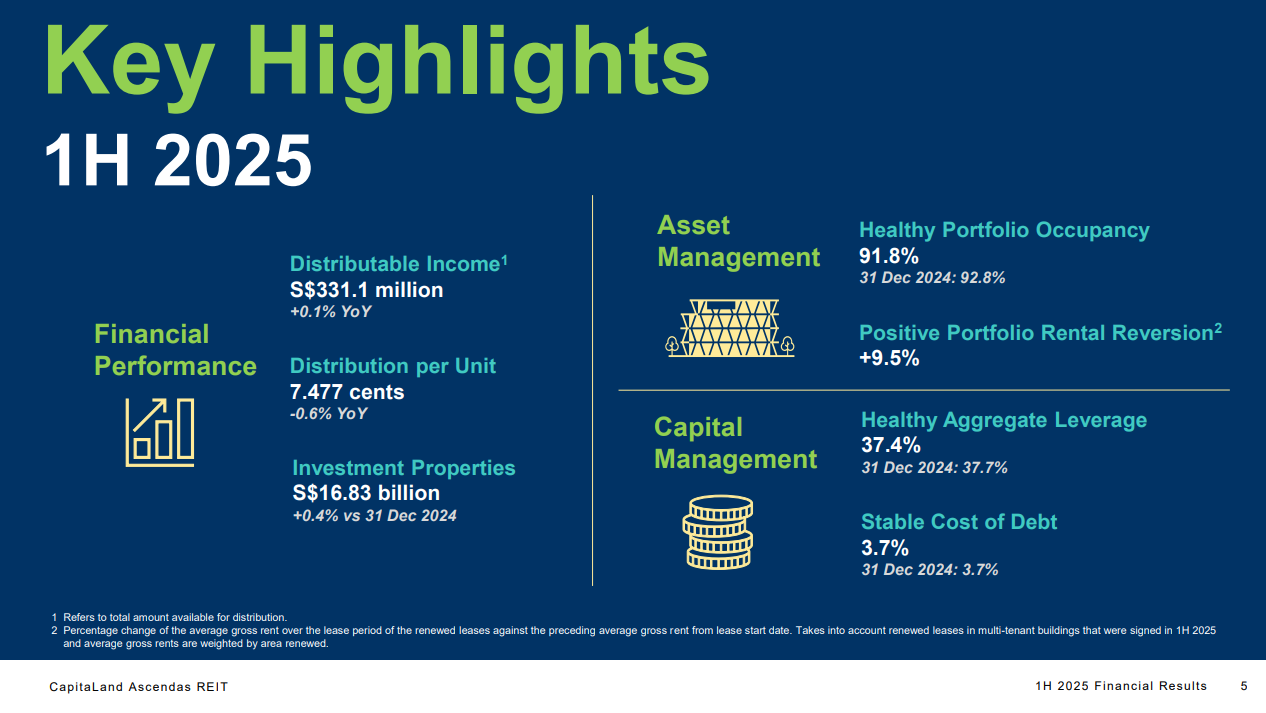

Most Singaporean investors are asking the wrong question about CapitaLand Ascendas REIT right now. They're wondering if the slight DPU dip means trouble ahead, but the real question is whether CLAR's strategic positioning in tomorrow's growth sectors—data centers, life sciences, and logistics—makes it the defensive play with upside potential that smart money needs in this uncertain environment.

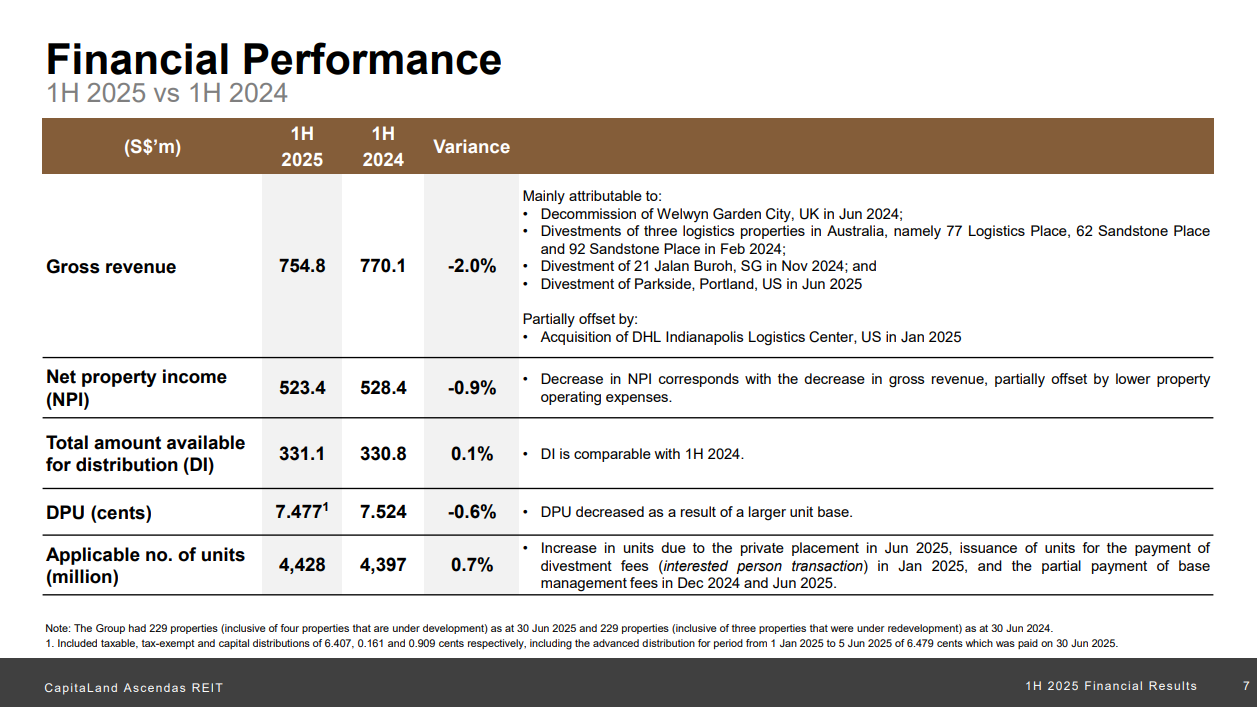

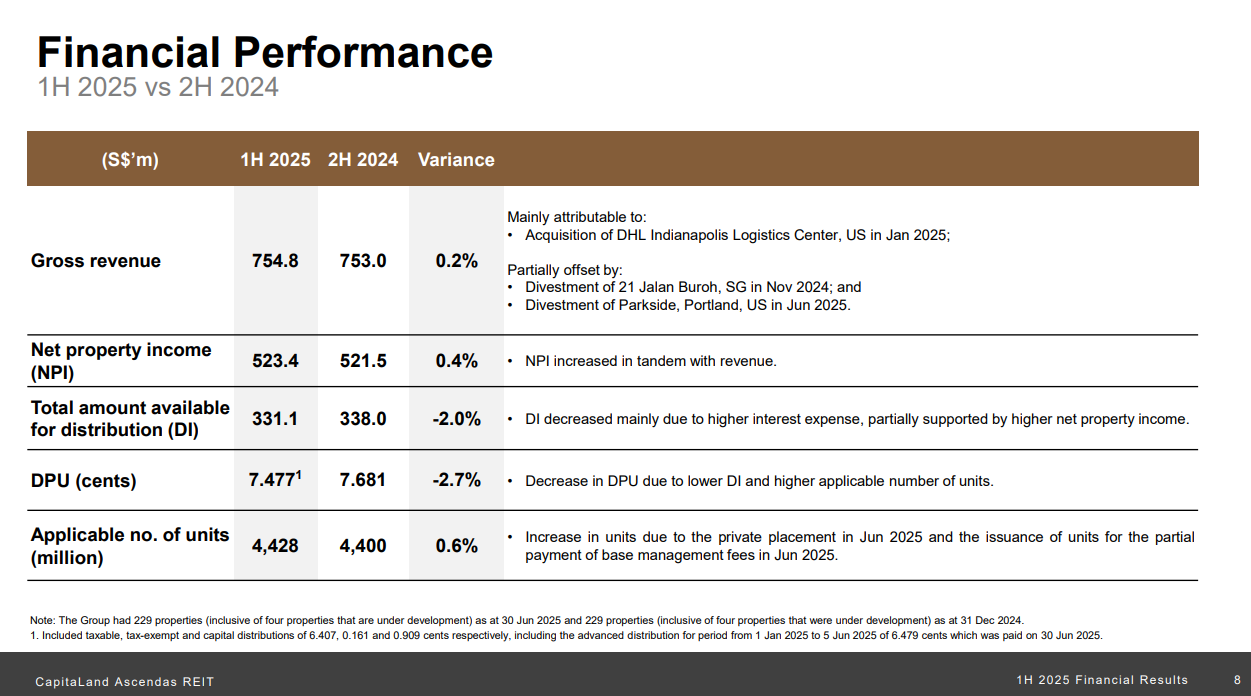

The numbers tell a story of resilience rather than weakness. While the headline DPU declined 0.6% to 7.477 cents, distributable income actually grew 0.1% year-over-year to S$331.1 million. This isn't operational decline—it's the temporary impact of strategic capital raising for growth.

Let me walk you through what really happened. The 2.0% revenue decline versus last year came entirely from strategic divestments—Welwyn Garden City in the UK, three Australian logistics properties, and Parkside in Portland. These were non-core assets sold at premiums to book value. Meanwhile, the DHL Indianapolis acquisition added S$153.4 million of quality logistics exposure.