Singtel’s 5.5% Yield Failure: Why Paper Profits From India Won’t Pay Your Bills

Your CPF is for retirement, not for keeping family heirlooms that haven't cleared the 4% Special Account hurdle.

Singtel at $3.20: Why Your Father’s Blue Chip Is Now a Forensic Red Flag

If your father bought Singtel at the 1993 privatisation IPO and passed the shares down to you, you are holding one of Singapore’s most emotionally complicated investment decisions. The investor who bought near the 52-week low of S$3.27 is feeling very smug right now — sitting on a near 52% capital gain. The stock has re-rated. The market has spoken.

But here is the uncomfortable forensic truth: at S$4.96, the dividend yield has quietly compressed to 3.67%. That does not clear our 150 basis point threshold above the forensic floor. The price has recovered. The yield has not kept pace. And for a retiree deploying fresh CPF or SRS capital today, you are now paying a premium price for a yield that no longer compensates for the turnaround risk still sitting inside this balance sheet.

The nostalgia is understandable. The math is not.

Today we run the Five-Layer Forensic Audit on Singtel. Not to tell you what to feel about your family heirloom. But to show you what happens when sentiment does the job that due diligence should be doing — and what it costs your CPF portfolio when the two get confused.

In This Article:

The Raw Facts on the Table

The Steelman: Three Genuine Positives

1. Regional Associate Value

2. Enterprise and Digital Business Growth

3. Dividend Stabilisation Signal

Step 1: The Health Check (Solvency)

Step 2: The Wealth Check (Yield & Cash Flow)

Step 3: The Price Check (Valuation)

Step 4: The Bottom Line

InvestingPro Reality Check

Iggy's Verdict

About Iggy & the Elite 190

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

The Elite 190 don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

👉 [Secure Your Seat in the Elite 190 Here]

The Raw Facts on the Table

Before we bring out the scalpel, we lay out the baseline metrics. No opinions, just the unvarnished numbers.

Current Price: S$4.96

Market Capitalisation: S$81.85 billion

Trailing Dividend Yield: 3.67%

Quarterly Dividend Amount: S$0.05

P/E Ratio: 13.27x

52-Week Range: S$3.27 — S$5.15

Last Dividend Cut: FY2023

Revenue Mix: Singapore core, Optus Australia, and regional associates (Airtel India, AIS Thailand, Globe Philippines)

Keep these figures in mind. We must build our foundation on verifiable reality before we can test the structural integrity of the investment.

The Steelman: Three Genuine Positives

We earn our credibility by being fair before we become forensic. Singtel is not a failing enterprise. It is a massive ship navigating a difficult transition. Here are three genuine, mathematically verifiable positives about the company today.

1. Regional Associate Value

Airtel India is genuinely one of the most valuable assets in Singtel’s entire portfolio. India’s telecommunications market is undergoing massive consolidation, and Airtel is emerging as a structural winner. On paper, Singtel’s 29% stake in Airtel is worth significantly more than the broader market is pricing into the parent stock. This is a textbook holding company discount situation — and it represents genuine unrealised value that a patient investor could eventually benefit from.

2. Enterprise and Digital Business Growth

Singtel’s NCS and Nxera data centre businesses are undeniably growing. The strategic pivot away from a pure consumer telco model toward enterprise digital services is the right move. Revenue from this segment is steadily rising and carries vastly better profit margins than legacy mobile plans. This is where Singtel’s future earnings power actually lives.

3. Share Price Recovery Momentum

From its 52-week low of S$3.27, Singtel has staged a significant recovery to S$4.96 — a 52% move that reflects genuine market confidence in the turnaround narrative. Management has signalled dividend stabilisation after two painful cuts. For an investor already holding from lower prices, the capital recovery is real. The question is whether the current price still offers sufficient margin of safety for fresh capital deployment.

Step 1: The Health Check (Solvency)

We must ask the most critical question first: can they survive the debt wall? This is the specific pressure point where a company must refinance significant debt burdens at higher interest rates.

Financial Health Checklist

🎓 Educational Note: Gearing In kopitiam logic, gearing is simply your HDB housing loan. If your flat is worth S$1 million and you owe HDB S$418,000, your gearing is 41.8%. It feels perfectly fine when your monthly salary is stable. But if your overtime pay gets cut, that 41.8% suddenly feels very heavy on your chest. Singtel’s gearing sits above our strict 35% fortress threshold.

🎓 Educational Note: ICR Think of ICR as your monthly take-home salary divided by your monthly mortgage interest. If you earn S$4,500 and your interest payment is S$1,000, your ICR is 4.5x. You can comfortably pay the bank and still afford to eat cai png with fish. Singtel passes this test comfortably.

Step 2: The Wealth Check (Yield & Cash Flow)

Now we audit the fuel. Is the payout organic, or is it an Engineered Yield? We deploy the Five-Layer Audit on the three biggest structural risks inside this balance sheet.

Red Flag 1: Optus Is a Structural Drag

Layer 1 (Raw Fact): The 2023 Optus cyberattack exposed deep operational vulnerabilities in Singtel’s second-largest revenue contributor.

Layer 2 (Historical Benchmark): Historically, Optus was a reliable cash cow. Today, remediation costs and customer churn remain severe. Margin recovery is much slower than management guidance previously suggested.

Layer 3 (Peer Context): Unlike NetLink Trust, which enjoys monopolistic fibre margins, Optus is bleeding in a structurally competitive Australian market against TPG and Telstra.

Layer 4 (Forward Scenario): If Australian macro conditions deteriorate by another 10%, or if regulatory fines increase, Optus will require even more capital injection from the parent company.

Layer 5 (Wallet Impact): Every dollar Singtel spends stabilising Optus is a dollar not flowing to your distribution cheque. For a 50+ Singaporean investor relying on this for retirement, that is a direct hit to your grocery budget.

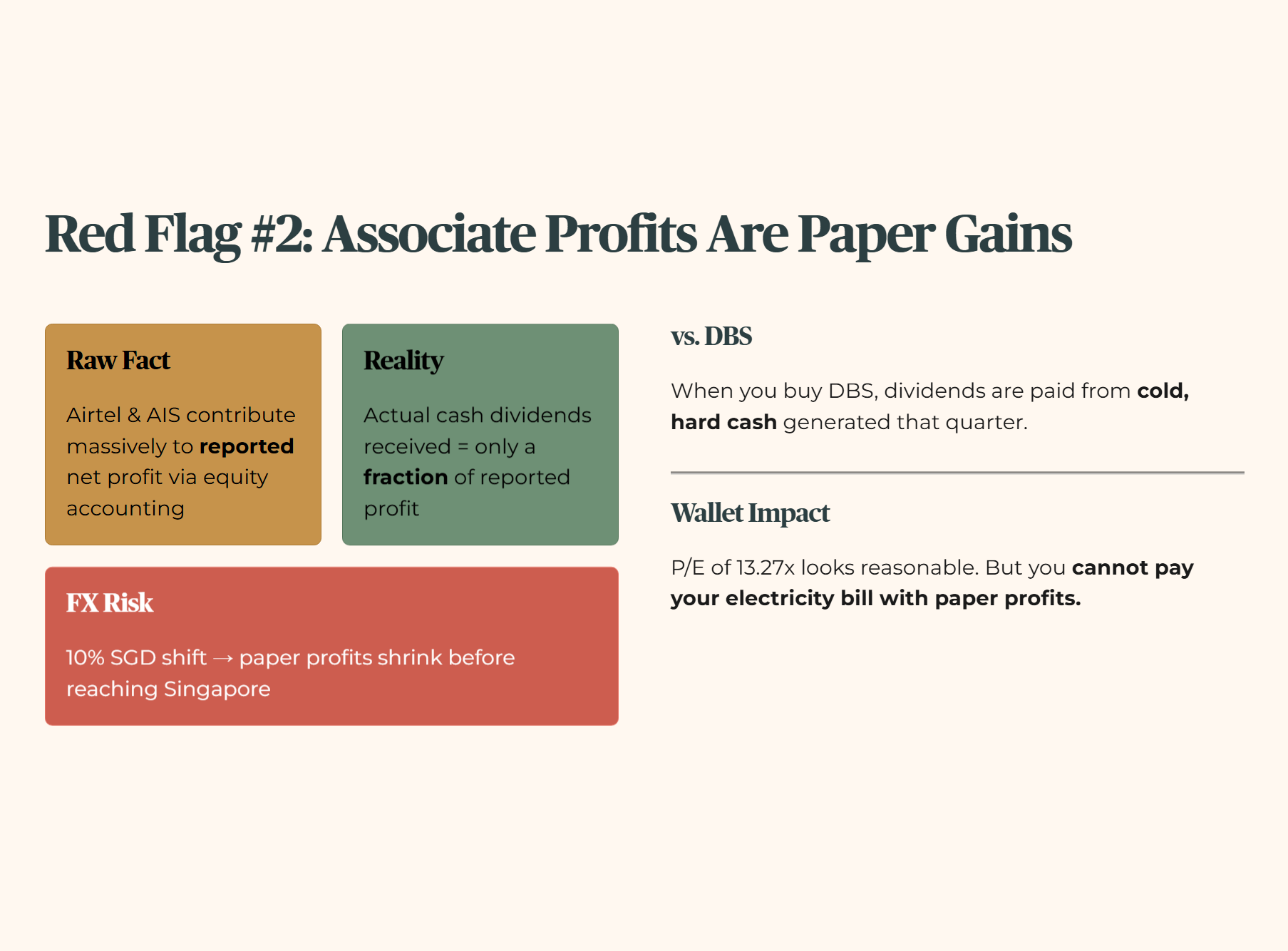

Red Flag 2: Associate Profits Are Paper Gains

Layer 1 (Raw Fact): Airtel and AIS contribute massively to Singtel’s reported net profit through equity accounting.

Layer 2 (Historical Benchmark): The actual cash dividends Singtel receives from these associates have historically been only a fraction of the reported profit contribution.

Layer 3 (Peer Context): When you buy DBS, the dividend is paid from cold, hard cash generated that quarter. Singtel’s associate profits are largely locked overseas.

Layer 4 (Forward Scenario): If foreign exchange rates shift unfavourably against the SGD by 10%, those paper profits shrink before they ever reach Singapore.

Layer 5 (Wallet Impact): The headline P/E of 13.27x looks reasonable. But you cannot pay your electricity bill with paper profits.

🎓 Educational Note: Equity Accounting Imagine your son wins S$10,000 in Toto. He tells you he will share the profits with you next year. You mentally add S$5,000 to your net worth today. That is equity accounting. But until he actually transfers the cash into your POSB account, you cannot use it at NTUC FairPrice. Profit is an opinion. Cash is a fact.

Red Flag 3: The Capital Expenditure Cycle

Layer 1 (Raw Fact): Singtel is in a heavy capex cycle due to 5G network rollouts and Nxera data centre expansions.

Layer 2 (Historical Benchmark): Compared to its 5-year historical average, free cash flow after capex is significantly tighter today.

Layer 3 (Peer Context): Mature REITs like CLAR can recycle capital by selling older properties. Singtel must constantly build new infrastructure just to stay relevant.

Layer 4 (Forward Scenario): If interest rates remain elevated, borrowing to fund this capex becomes exponentially more expensive.

Layer 5 (Wallet Impact): A company in a heavy capex cycle with a committed dividend is either borrowing money to pay you, or the dividend is at risk again. For an SRS investor, a second cut in three years is a scenario you must actively stress-test.

At this price, Singtel doesn’t just “look expensive”—once you apply the forensic adjustments, the dividend story breaks, and the real cash yield lands on the wrong side of my floor (next: the exact adjustment logic and what it changes for CPF/SRS deployment).