Singtel FY2026 Forensic Audit | The Dividend That Isn't What It Looks Like | EP1624🦖

Iggy Runs the Numbers on Singtel's FY2026 Payout — The Footnotes Tell a Different Story

Singtel FY2026 Earnings Forensic Audit

Results for the Full Year Ended 31 March 2026

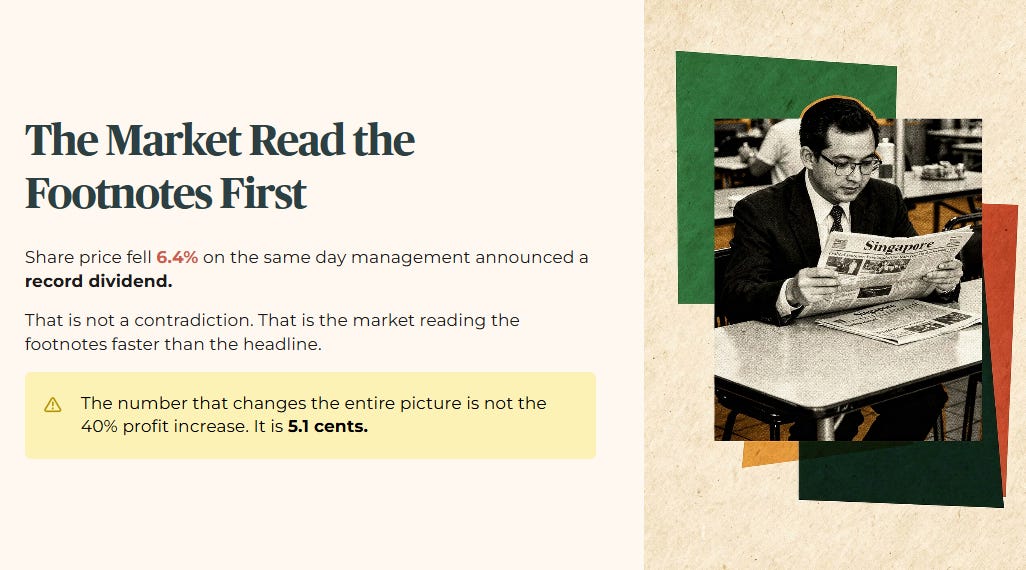

The share price fell 6.4 per cent on the same day management announced a record dividend. That is not a contradiction. That is the market reading the footnotes faster than the headline. If you are holding Singtel for retirement income, there is one number buried in this results presentation that changes the entire picture — and it is not the 40 per cent profit increase. It is 5.1 cents. We will come back to it.

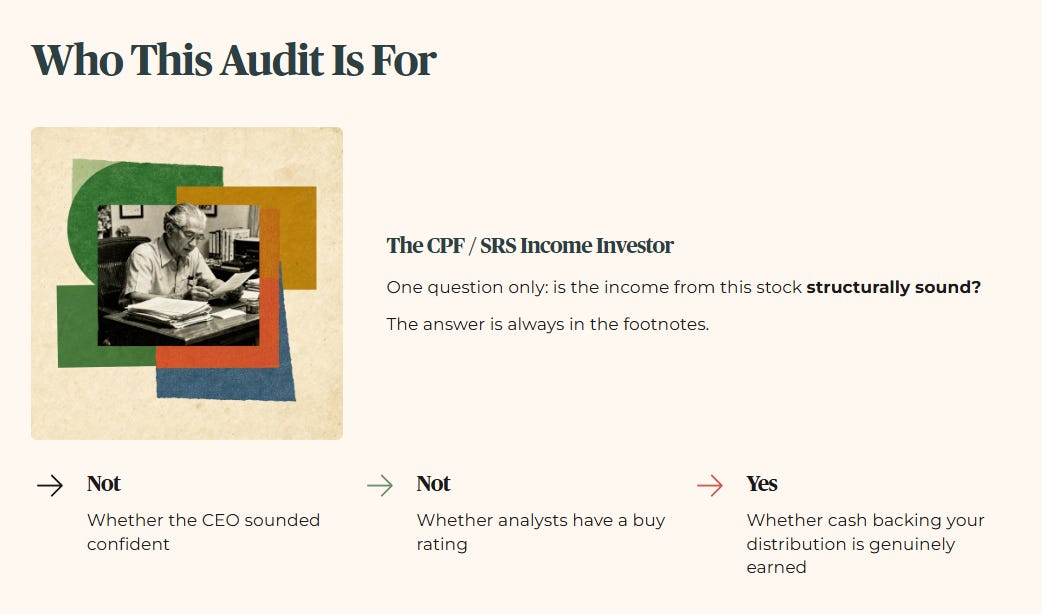

This audit is for the Singaporean investor holding Singtel shares inside a CPF Investment Scheme account or an SRS portfolio who wants to know one thing: is the income from this stock structurally sound? Not whether the CEO sounded confident on the call. Not whether analysts have a buy rating. Whether the cash backing your annual distribution is genuinely earned from running the business — or whether part of it depends on something more fragile.

The answer, as always, is in the footnotes.

In This Article:

The Slide-by-Slide Audit

The 40 Per Cent Profit Headline — Reading It Correctly

The Regional Associates — Where The Complexity Enters

NCS and Digital InfraCo — The Two Genuine Bright Spots

Iggy’s Insight — The Number Management Spent The Least Time On

The Reality Check - What the Numbers Say The Stock is Worth

The Scorecard and Yield Spread

Table 1 — Income Sustainability

Table 2 — Debt Health

The Forward Outlook

Table 3 — Scenario Analysis

Iggy’s Insight — The Management Credibility Verdict

Conclusion

Iggy’s Forensic Disclaimer

The Slide-by-Slide Audit

What Management Said — And What The Numbers Show

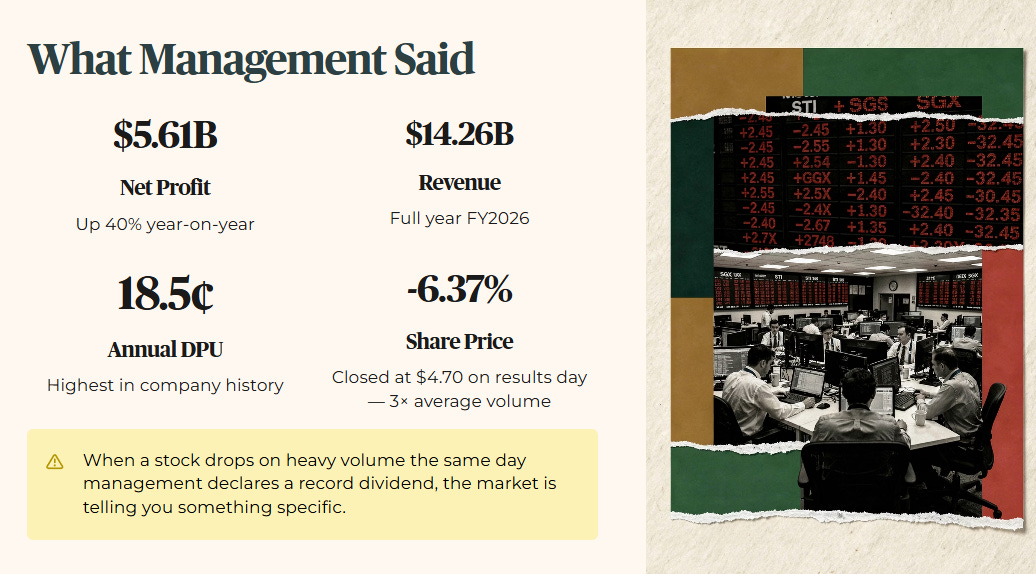

Singtel opened the results presentation with a confident headline. Full-year net profit of 5.61 billion dollars, up 40 per cent from the prior year. Revenue of 14.26 billion dollars. Annual dividend of 18.5 cents per share — the highest in the company’s history. Group CEO Yuen Kuan Moon described it as a strong set of results for the second year of the Singtel28 growth plan.

The market responded by selling the stock on volume nearly three times the 30-day average. The share price closed at 4.70 dollars on results day, down 6.37 per cent. When a stock drops sharply on heavy volume the same day management declares a record dividend, the market is telling you something specific. This audit is the process of finding out exactly what.

The 40 Per Cent Profit Headline — Reading It Correctly

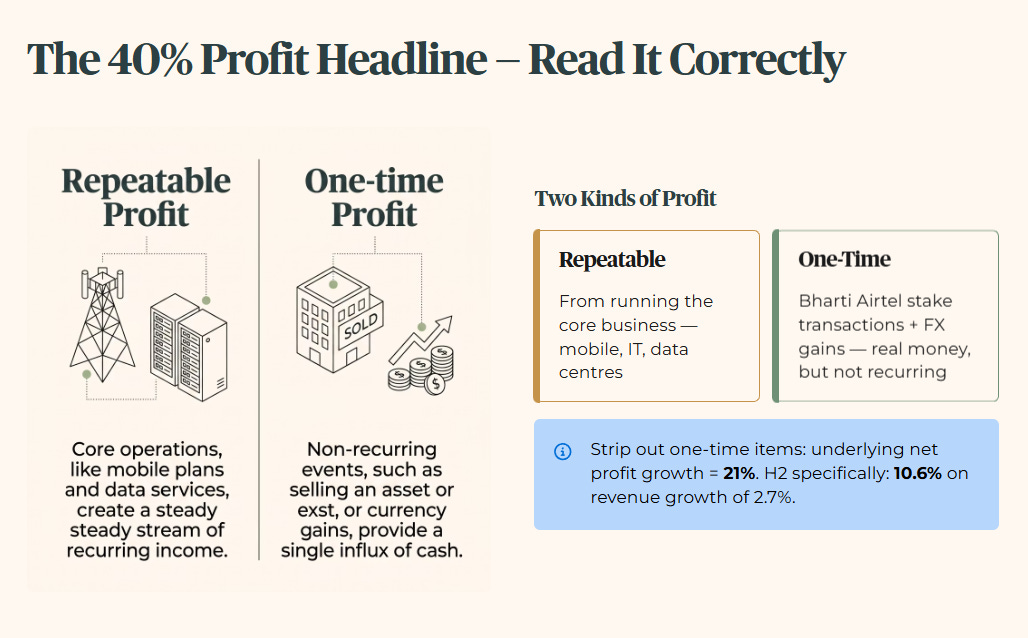

Net profit, in plain language, is what a company keeps after paying every bill — salaries, rent, loan interest, taxes, everything. A 40 per cent jump in one year sounds like a business firing on all cylinders.

But there are two kinds of profit. The first comes from running the core business well — selling mobile plans, winning IT contracts, operating data centres. This kind repeats next year and the year after. The second comes from one-time events — selling a stake in another company, booking a currency gain, completing a transaction that will not happen again.

Singtel’s 40 per cent net profit increase is heavily weighted toward the second kind. The gains from the Bharti Airtel stake transactions and foreign exchange movements are real money — but they are not money you can count on repeating. Strip those out and the underlying net profit growth is 21 per cent. For the second half of the financial year specifically, underlying net profit grew 10.6 per cent to 1.4 billion dollars on revenue growth of 2.7 per cent to 7.4 billion dollars.

That 10.6 per cent organic growth figure is the one that matters for a long-term income investor. It is real. It is earned from operations. And it is being buried under a headline that includes transactions the business cannot replicate on demand.

The forensic principle here is straightforward. When you are managing retirement income, you need to know whether the company can keep paying you from its regular business — not from selling the furniture.

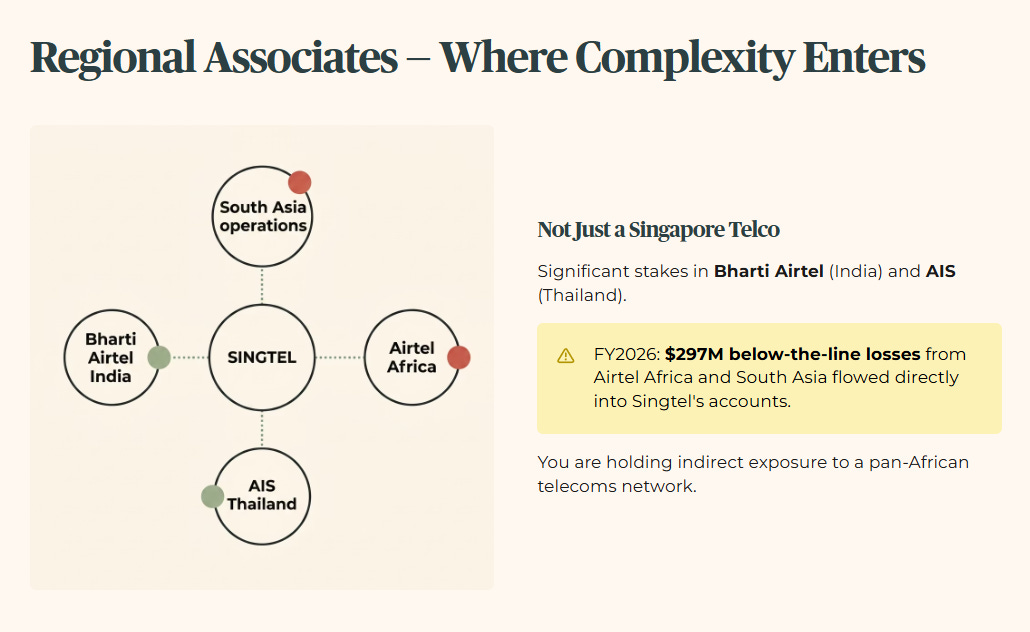

The Regional Associates — Where The Complexity Enters

Singtel is not purely a Singapore telco. It holds significant stakes in regional telecommunications companies, most notably Bharti Airtel in India and AIS in Thailand. These associates contribute meaningfully to reported profits — but the contribution comes with complexity.

In FY2026, below-the-line losses of 297 million dollars from Airtel Africa and South Asia reduced the post-tax profit contribution from these regional associates. In plain language: the parts of the Airtel business operating in Africa and parts of South Asia lost money, and that loss flowed directly into Singtel’s accounts.

This matters for two reasons. First, it explains part of the gap between the 40 per cent headline and the 21 per cent underlying figure. Second, it means Singtel’s earnings carry exposure that a Singapore telco investor did not necessarily price in when buying shares for stable local income. You are not just holding a Singapore telephone company. You are holding indirect exposure to the operational performance of a pan-African telecoms network. That exposure is not necessarily bad — Airtel India and AIS Thailand were genuine standout performers in FY2026 — but it is a layer of complexity that belongs in the forensic picture.

NCS and Digital InfraCo — The Two Genuine Bright Spots

Two business units delivered results that deserve to be taken seriously on their own terms.

NCS, Singtel’s technology and digital services arm, achieved record bookings in FY2026 driven by strong demand for artificial intelligence projects. Companies across the region are spending heavily on AI infrastructure, and NCS is winning the contracts to build and manage those systems. Record bookings do not immediately appear as revenue — bookings convert to revenue as projects are delivered over time — but the pipeline is the clearest available signal of where organic earnings are heading.

Digital InfraCo, which includes the Nxera data centre business, hit new operational milestones. Data centres are the physical infrastructure that AI systems run on — buildings full of servers that process and store the vast quantities of data that AI models require. This is a high-demand, capital-intensive business, and Singtel is building it with deliberate intent. The KKR-Singtel consortium’s 13.8 billion dollar acquisition of STT GDC is the single largest transaction in this programme.

For the income investor, these two growth engines matter because they represent the organic revenue streams that will fund future dividends without relying on asset sales. The forensic question is whether they are growing fast enough to close the gap between today’s yield and the minimum threshold a retirement portfolio requires.

🦎 Iggy’s Insight — The Number Management Spent The Least Time On

Buried in the results presentation, with minimal dedicated explanation relative to its forensic significance, is the Value Realisation Dividend — the VRD. In FY2026, 5.1 cents of the 18.5 cents total dividend — that is 27.6 per cent of your entire annual income from this stock — is not paid from running phone networks or data centres. It is paid from the proceeds of selling assets. This component grew from 4.7 cents in FY2025 to 5.1 cents in FY2026.

The direction of travel is the wrong way. Singtel needs to execute approximately 3.3 billion dollars of asset transactions over four years to sustain this component. If those transactions face delays — from market conditions, regulatory hurdles, or buyer financing problems — the VRD contracts. And your income drops with it. The record dividend headline is real. The structural dependency underneath it deserves equal attention.

The record dividend headline is real — but the 3.3 billion dollars of asset transactions required to fund that 5.1-cent VRD over the next four years is where the structural stress-test on Singtel’s retirement-income promise actually begins.