T-Bill yield at 1.47% sparks risky shift (Weekly SGX Gainers/Losers 12 Apr 26)

Heartland portfolios are leaking cash. If your blue-chip yield is under 4.7%, you are failing the forensic stress-test today.

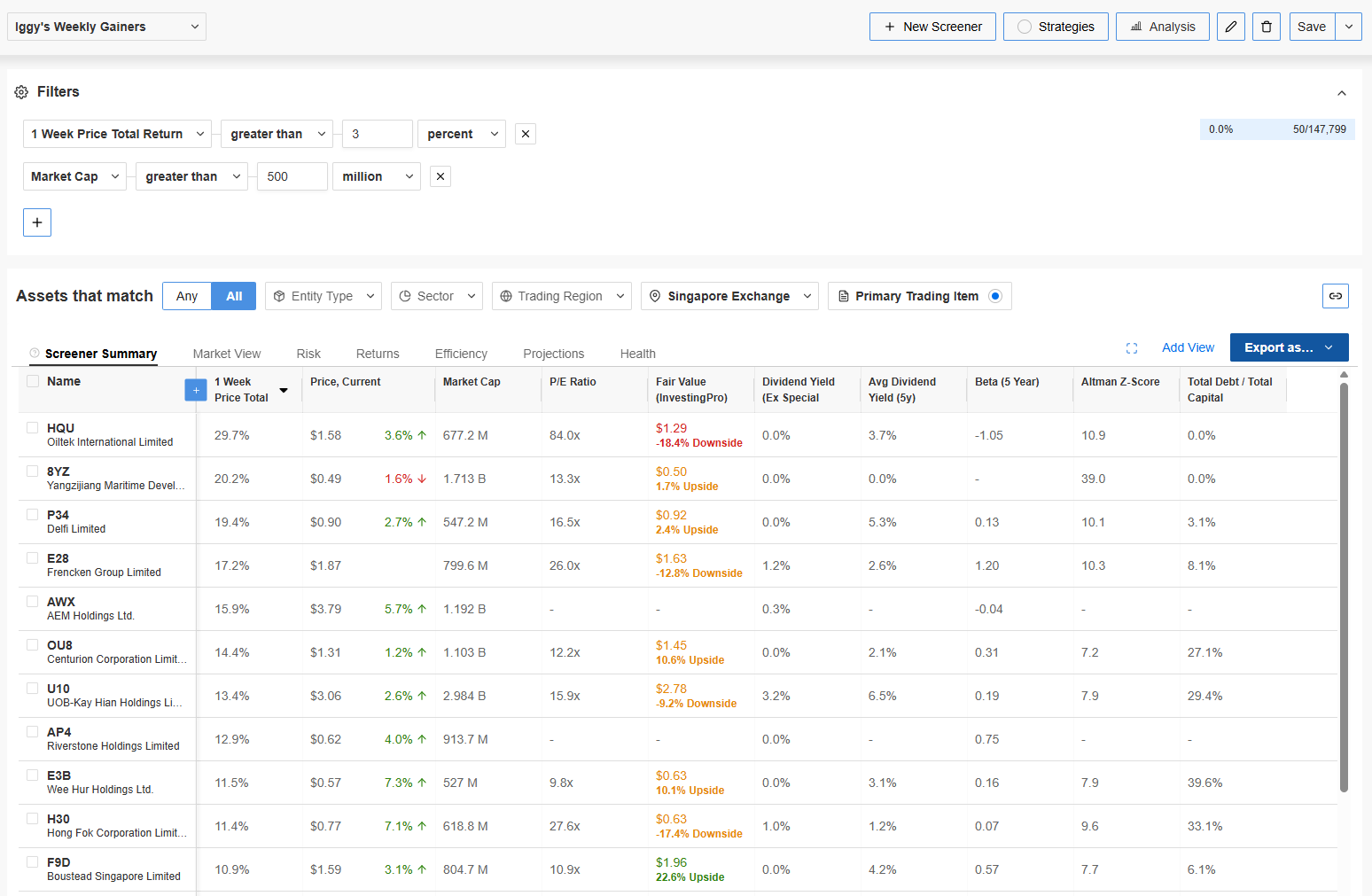

SGX Weekly Gainers & Losers (12 Apr 2026)

Retail investors are currently paying nearly 90 times earnings for small-cap momentum plays while simultaneously fleeing blue-chip dividends that have failed to outpace the CPF sanctuary benchmark. This valuation disconnect suggests that the “T-Bill Flight” is no longer seeking safety, but is instead stumbling into a high-octane risk environment that the heartland retirement portfolio is ill-equipped to handle.

In This Article:

The Macro Pulse

This Weeks Forensic Movers The Gainers

This Weeks Forensic Warnings The Losers

The Forensic Yield Spread Monitor

The Macro Connector

Iggys Weekly Verdict

Iggys Forensic Compliance Standards Standard Disclaimer

The Macro Pulse

The Straits Times Index (STI) reached a psychological peak of 4,996.05 on April 7, though it failed to hold the 5,000-point handle, closing the week at 4,989.41. This hesitation at the threshold indicates a standoff between retail “Fear Of Missing Out” (FOMO) and institutional profit-taking.

Regionally, the Hang Seng Index exhibited continued volatility, swinging across a 777-point range before finishing at 25,893 [DATA GAP]. The primary macro driver remains the domestic liquidity shift triggered by the April 9 T-Bill auction, which delivered a cut-off yield of 1.47%. With the risk-free rate effectively bottoming, capital is rotating into the equity market, but doing so with a visible disregard for traditional valuation floors.

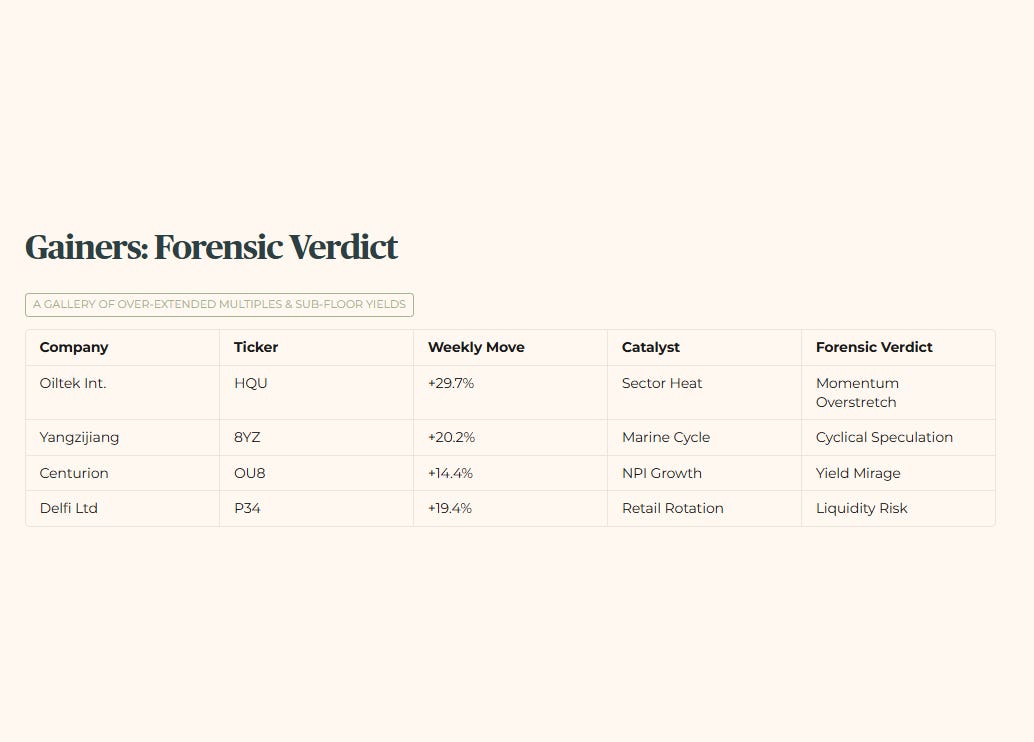

This Week’s Forensic Movers: The Gainers

The gainers this week are dominated by engineering and industrial plays that have decoupled from their underlying book values.

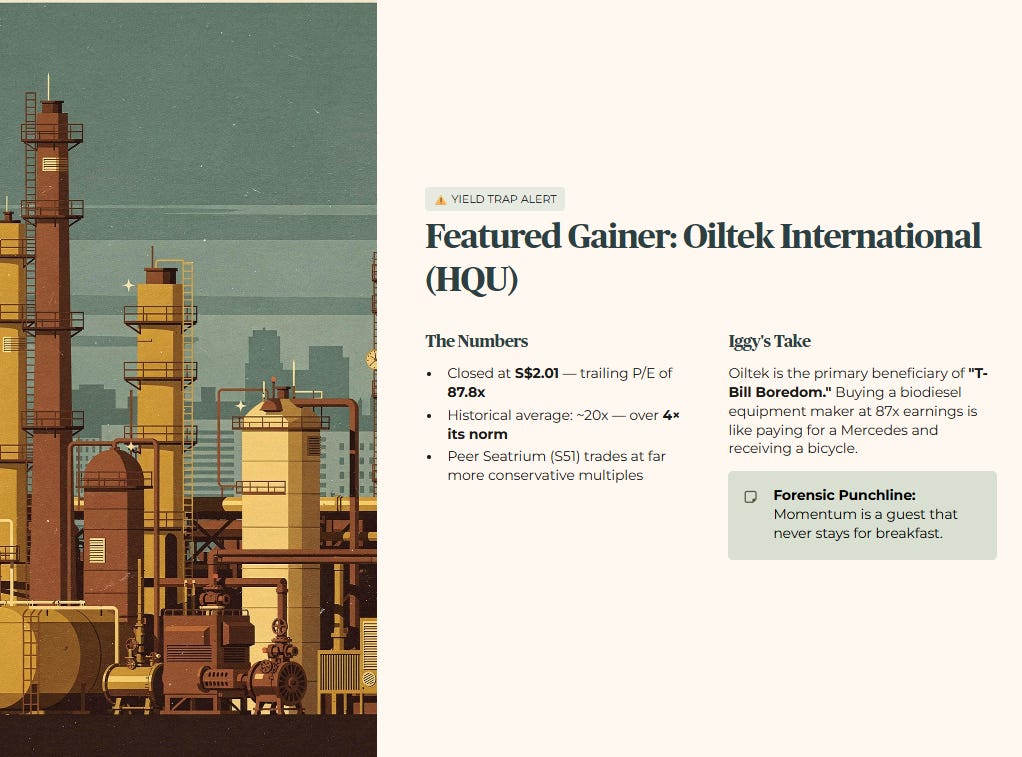

Featured Gainer: Oiltek International Limited (HQU)

YIELD TRAP ALERT

Oiltek has transitioned from a fundamental engineering story into a speculative momentum vehicle.

1. Raw Fact: Oiltek closed the week at S$2.01, representing a trailing P/E ratio of 87.8x following an aggressive price surge.

2. Historical Benchmark: This 87.8x multiple is more than four times its 3-year historical average. Historically, the stock has traded closer to 20x, suggesting the current price is pricing in decades of growth that has yet to manifest in the order book.

3. Peer Context: Direct peer Seatrium (S51) is trading at a significantly more conservative valuation despite having a broader global footprint and more diversified revenue streams. Oiltek’s current premium is an anomaly in the SGX engineering space.

4. Forward Scenario: If biodiesel equipment demand softens by 10% due to regional policy shifts, a mean reversion to its historical 20x P/E would result in a capital drawdown of approximately 75%. A macro trigger would be a sudden reversal in palm oil price trends affecting CAPEX in the sector.

5. Wallet Impact: For a 55-year-old investor near retirement, an entry at S$2.01 is a high-stakes gamble. A $50,000 position could see $37,500 in principal evaporated in a mean-reversion event. The forensic stance is that this is a momentum trap, not a long-term sanctuary.

Iggy’s Take: Oiltek is the primary beneficiary of “T-Bill Boredom.” When the safe 1.47% yield feels too low, retail money chases the steepest chart. But buying a biodiesel equipment maker at 87 times earnings is like paying for a Mercedes and receiving a bicycle.

Forensic Punchline: Momentum is a guest that never stays for breakfast.

Compressed Gainers

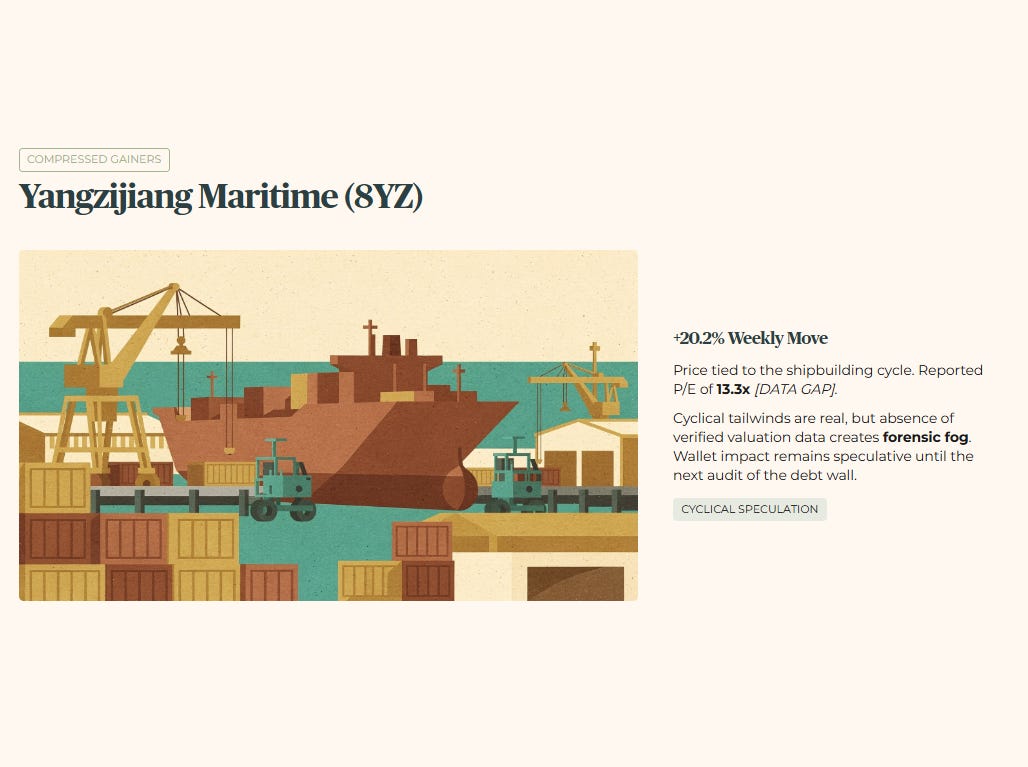

Yangzijiang Maritime Development (8YZ): Price activity remains tied to the shipbuilding cycle, supported by a reported P/E of 13.3x [DATA GAP]. While the cyclical tailwinds are real, the absence of verified valuation data via standard tools suggests a forensic fog. For the heartland investor, the wallet impact remains speculative until the next audit of the debt wall.

Centurion Corporation Limited (OU8): Moved higher on NPI growth expectations, but carries a trailing yield of only 2.40%. This is a “Yield Mirage” where price growth masks a return that sits below the 3.2% forensic floor. The wallet impact is a net loss in real purchasing power when compared to the 4.0% CPF SA benchmark.

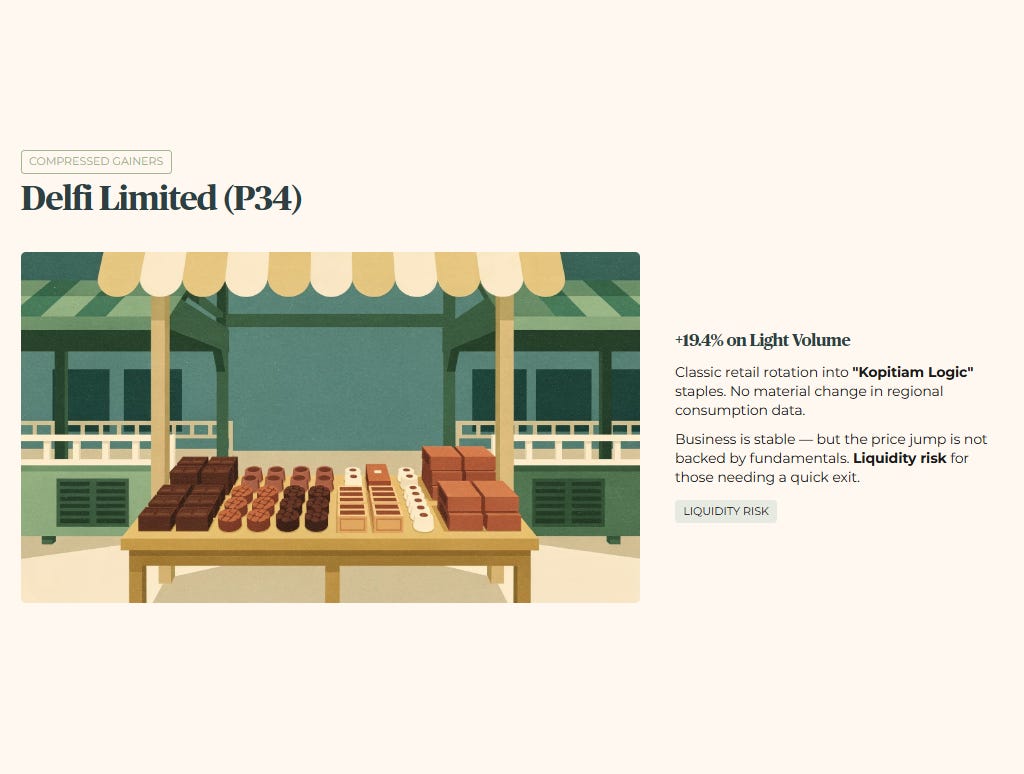

Delfi Limited (P34): The chocolate manufacturer rose on light volume, a classic retail rotation into “Kopitiam Logic” staples. While the business is stable, the 19.4% price jump is not backed by a material change in regional consumption data. It remains a liquidity risk for those needing a quick exit.

Forensic Verdict: The gainers’ list is a gallery of over-extended multiples and sub-floor yields.

Note: InvestingPro data is in USD.

“Don’t overpay for the hype. See the math behind the momentum.” .....

Use the Fair Value models I use in every video. Code INVESTINGIGUANA gets you 50% off the world’s most powerful stock screener.

🦎 [Spot Undervalued Gems Here]

The gainers show momentum traps at extreme multiples — but the losers' forensic yield spreads reveal the true sanctuary failures that are draining heartland CPF portfolios right now.