Soon Hock Enterprise IPO: A Mixed Signal for Singapore’s Industrial Property Play

Can a relatively small industrial developer ride Singapore’s mega infrastructure wave to deliver solid returns for new shareholders?

Editor’s Note: This post has been updated on October 19, 2025, to ensure it is fresh and accurate, and now includes the latest analysis on the Soon Hock Enterprise IPO’s valuation and its strategic comparison against industrial S-REITs.

The Singapore Exchange is buzzing with fresh IPO activity, and Soon Hock Enterprise’s $48.1 million Mainboard debut represents another test case for local investors weighing the industrial property sector. While the company promises exposure to Singapore’s structural industrial demand story, its volatile revenue patterns and modest scale raise important questions about timing and valuation. The real question isn’t whether Singapore’s industrial market will grow – it’s whether Soon Hock can execute consistently enough to justify investor confidence at 58 cents per share.

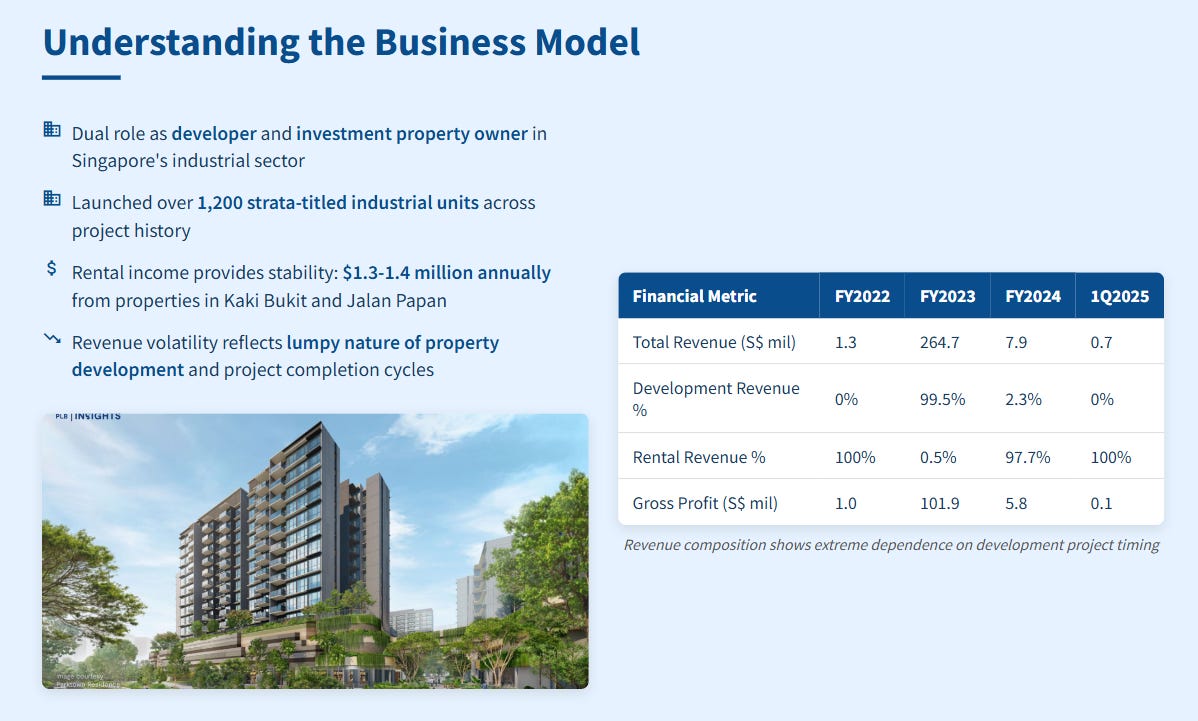

Soon Hock Enterprise has built a track record in Singapore’s industrial development space, but like many property developers, its financial performance swings dramatically based on project completion cycles. Revenue plunged 97% from $264.7 million in FY2023 to just $7.9 million in FY2024, entirely due to the absence of new project sales. This dramatic volatility reflects the lumpy nature of property development, where revenue recognition depends on obtaining Temporary Occupation Permits (TOPs) and completing sales.

Understanding the Business Model

Soon Hock operates as both a developer and investment property owner, focusing exclusively on Singapore’s industrial sector. The company has launched over 1,200 strata-titled industrial units across its project history, giving it meaningful experience in this specialized market. Their portfolio includes both development projects for sale and investment properties generating rental income.

The rental income component provides some stability, generating around $1.3-1.4 million annually from properties in Kaki Bukit and Jalan Papan. The Jalan Papan property includes a 300-bed workers’ dormitory that achieved full occupancy through a master lease arrangement, demonstrating demand for purpose-built worker accommodation.

Chart 1: Soon Hock Revenue (FY2023 vs. FY2024) shows extreme volatility based on project completion

Project Pipeline and Growth Strategy

Soon Hock has two key projects under development that should drive near-term revenue recognition: Stellar@Tampines and Skye@Tuas. Stellar@Tampines expects partial TOP in Q4 2025 and full TOP in Q1 2026, with 168 units pre-sold out of 311 total units as of September 2025. This strong pre-sales rate suggests healthy demand for well-located industrial properties.

Skye@Tuas represents a more strategic bet on Singapore’s western industrial corridor, designed specifically for heavy-duty logistics users who should benefit from the nearby Tuas Mega Port development. The project has already received expressions of interest for one entire floor, indicating corporate users are planning their space requirements around the mega port timeline.

The company plans to use IPO proceeds for three main purposes: acquiring new development sites, partially financing the 20 Shaw Road redevelopment, and funding existing pipeline projects including Senang Crescent redevelopment. This capital deployment strategy makes sense given Singapore’s competitive industrial land tender process.

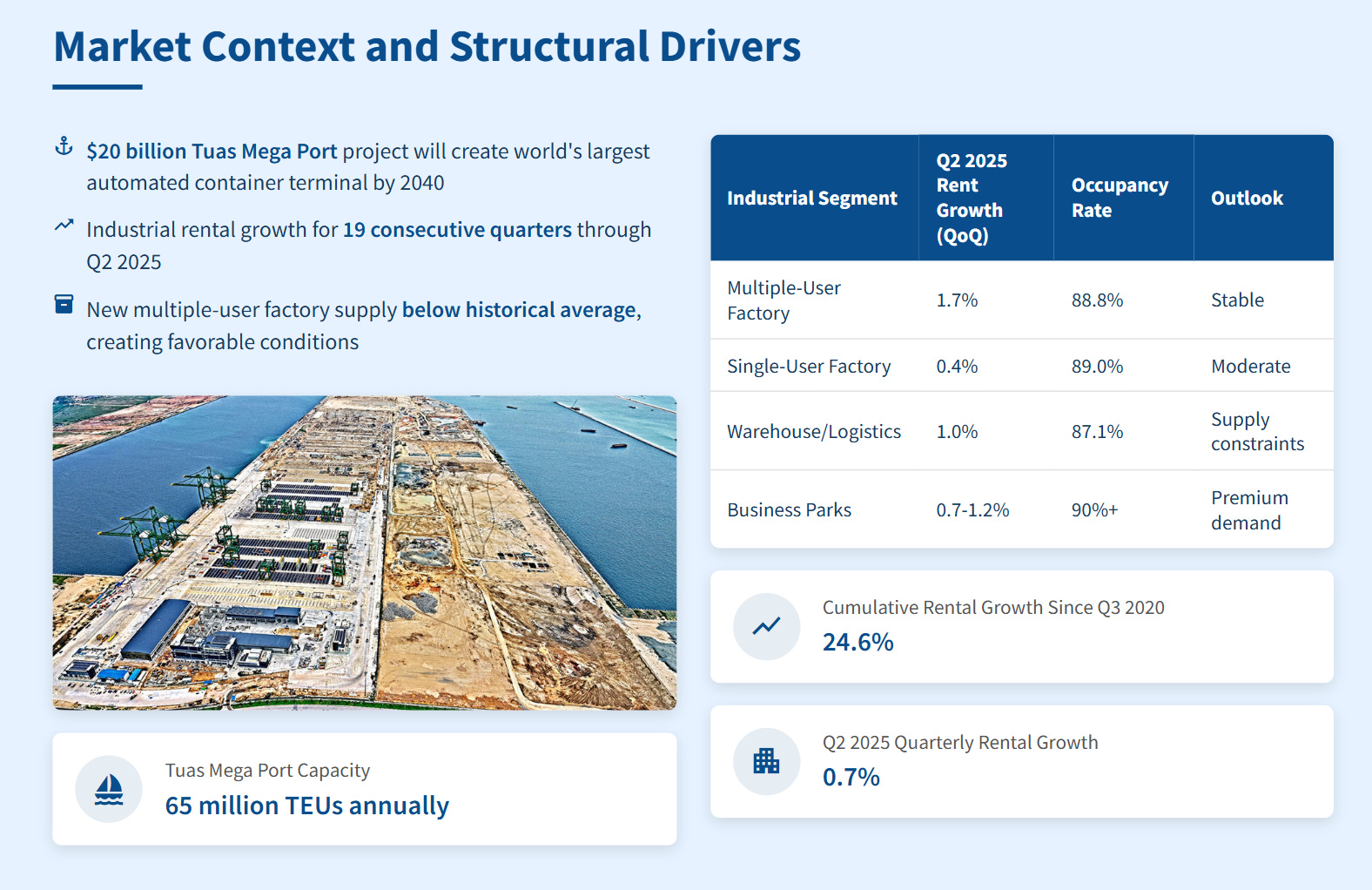

Market Context and Structural Drivers

Singapore’s industrial property market presents a compelling long-term story built around several structural trends. The $20 billion Tuas Mega Port project will create the world’s largest automated container terminal by 2040, with capacity to handle 65 million TEUs annually. This infrastructure investment should drive sustained demand for logistics, warehousing, and manufacturing space in western Singapore.

Industrial rental growth has been remarkably consistent, with the JTC All Industrial rental index rising for 19 consecutive quarters through Q2 2025. Rents increased 0.7% quarter-on-quarter in Q2 2025, building on a 24.6% cumulative increase since the Q3 2020 trough. Business park rents showed particularly strong growth at 1.2% quarterly.

Singapore’s industrial rental market shows broad-based growth across segments, supported by limited new supply and steady absorption

The supply pipeline remains relatively constrained, particularly for multiple-user factory space where Soon Hock competes. New multiple-user factory supply is running below its ten-year historical average, creating favorable conditions for both rental growth and sales absorption. However, some segments face higher incoming supply, particularly prime logistics space, though much of this is pre-committed to single users.

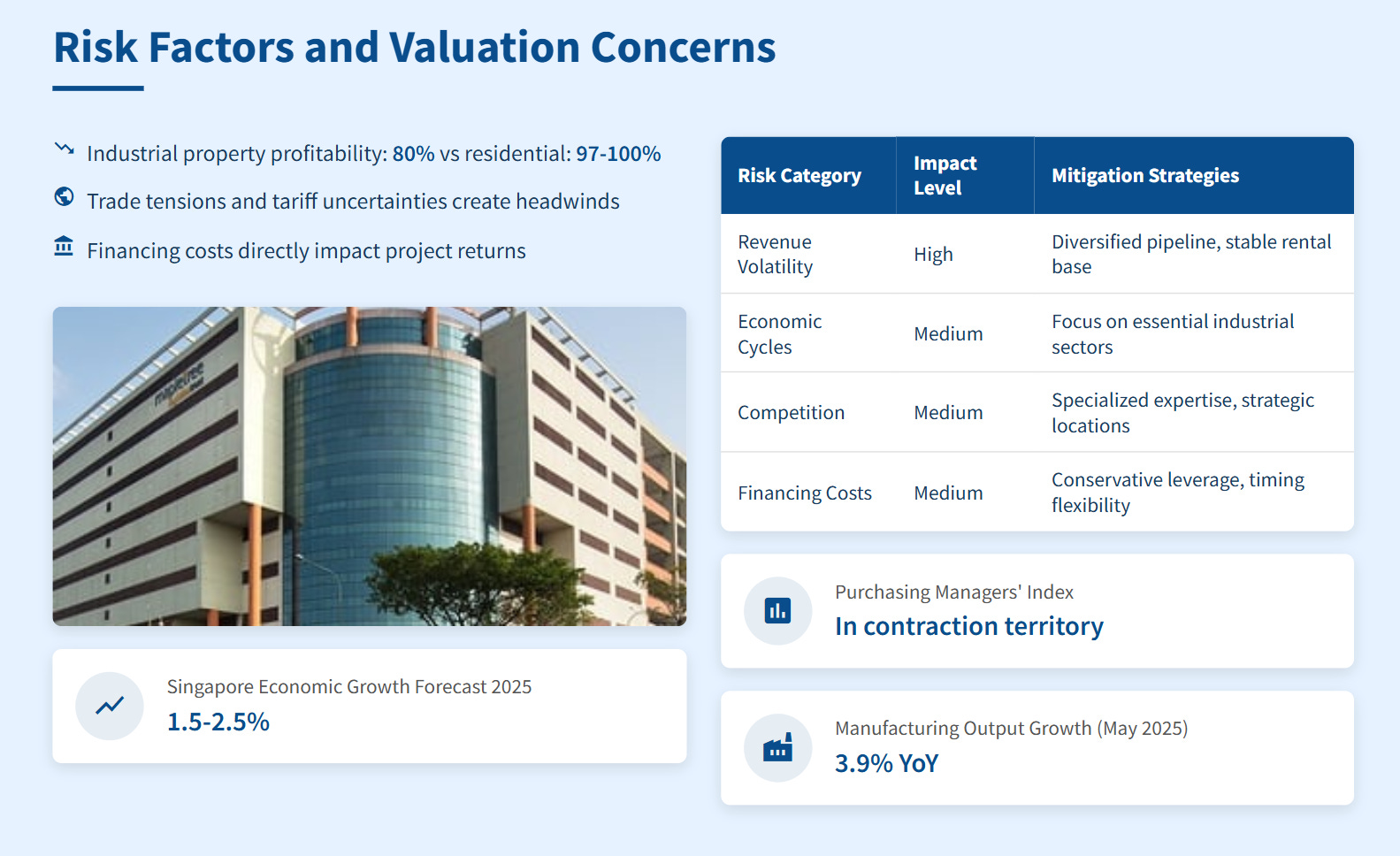

Risk Factors and Valuation Concerns

Industrial property investment carries higher risks than residential real estate, with profitability ratios averaging around 80% versus 97-100% for residential properties. This reflects the more specialized nature of industrial assets and their sensitivity to economic cycles.

The broader macroeconomic environment presents mixed signals for industrial demand. Singapore’s economic growth forecast has been upgraded to 1.5-2.5% for 2025, but ongoing trade tensions and tariff uncertainties create headwinds for manufacturing and logistics activity. The Purchasing Managers’ Index remains in contraction territory, though manufacturing output showed 3.9% year-over-year growth in May 2025.

Currency and interest rate risks also matter for property developers. While Singapore REITs have weathered recent rate increases relatively well, developers face financing costs that directly impact project returns. Soon Hock’s relatively modest scale may limit its ability to secure the most competitive project financing compared to larger developers.

IPO Structure and Investment Thesis

The IPO will issue 83 million shares at 58 cents each, consisting of 18.8 million placement shares, 2.8 million public shares, and 16.6 million existing shares sold by founder Tan Yeow Khoon. Cornerstone investors including Maybank Asset Management, UOB Kay Hian, and several private investors have committed to 61.4 million shares worth $35.6 million, providing solid institutional backing.

Post-listing market capitalization of $180.1 million values Soon Hock at roughly 0.57 times its current asset base of around $316.5 million, implying the company is listing at a significant discount to its assets. The company commits to distributing at least 25% of net profits as dividends from listing through December 2026, though given the volatile earnings pattern, this may result in irregular dividend payments.

The key investment question centers on execution risk versus market opportunity. Singapore’s industrial property fundamentals remain solid, supported by mega infrastructure projects, regional supply chain shifts, and consistent rental growth. However, Soon Hock’s relatively small scale and project-dependent revenue model create inherent volatility that may not suit all investors.

Iggy’s Take: The Real Choice—Volatile Developer vs. Stable REIT

“Before you consider this IPO, you must ask one question: ‘Why buy this over a blue-chip industrial S-REIT like CapitaLand Ascendas (CLAR) or Mapletree Logistics (MLT)?’