S’pore Retirees Chasing Gold Lose $3,300 Yearly

Chasing gold at record highs is like paying $10 for a kopi—it’s a luxury that drains your grocery budget.

MAS just revised inflation forecasts upward — and your cash yield is quietly evaporating. If you are chasing gold at these record highs for your SRS account, you are building an income vacuum that will drain S$3,300 out of your retirement budget every single year. Today I will show you why a seemingly safe 20 percent gold allocation is actually the most expensive insurance policy your portfolio will ever buy.

In This Article:

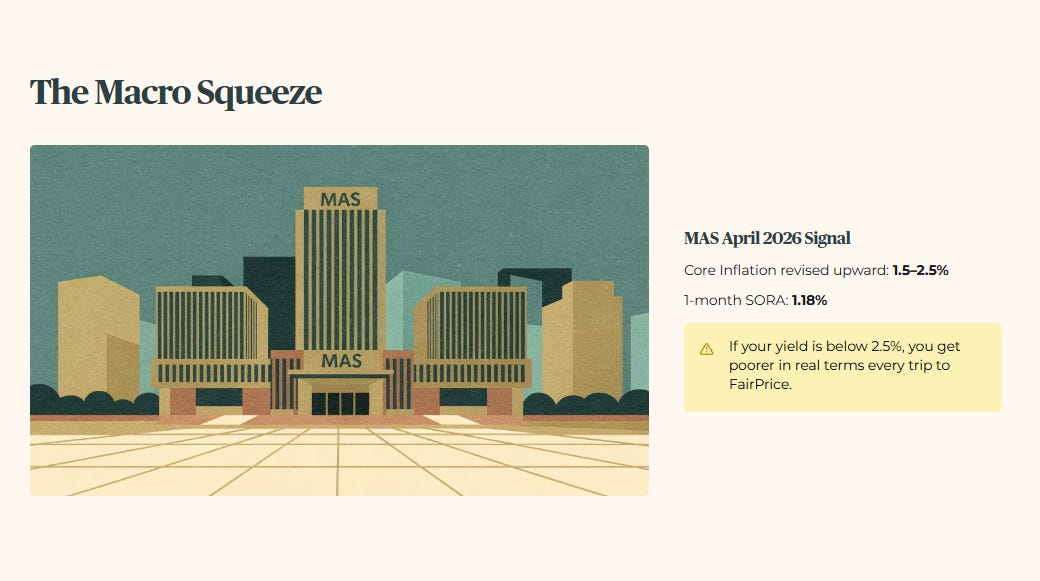

The Macro Squeeze Why the Heartland is Feeling the Burn

Step 1 The Health Check Solvency

Financial Health Checklist CNMC Goldmine 5TP

Step 2 The Wealth Check Yield and Cash Flow

Dividend Trajectory The Income Vacuum

Step 3 The Price Check Valuation

Peer Comparison The Mining Sector Audit

Iggy’s Insight The Mining Premium Trap

Step 4 The Bottom Line Forensic Stance

Iggy’s Forensic Compliance Standards Standard Disclaimer

The Macro Squeeze: Why the Heartland is Feeling the Burn

The Monetary Authority of Singapore delivered a significant signal in their April 14, 2026 policy statement. While the headlines focus on the S$NEER policy band holding steady, the forensic reality is buried in the inflation forecasts. MAS Core Inflation has been revised upward to a range of 1.5 to 2.5 percent.

At the same time, the 1-month SORA rate has moved to 1.18 percent. This creates a Real Yield Squeeze. For a retiree, the arithmetic is brutal. If your money sits in a product yielding less than 2.5 percent, you get poorer in real terms every time you walk into a FairPrice.

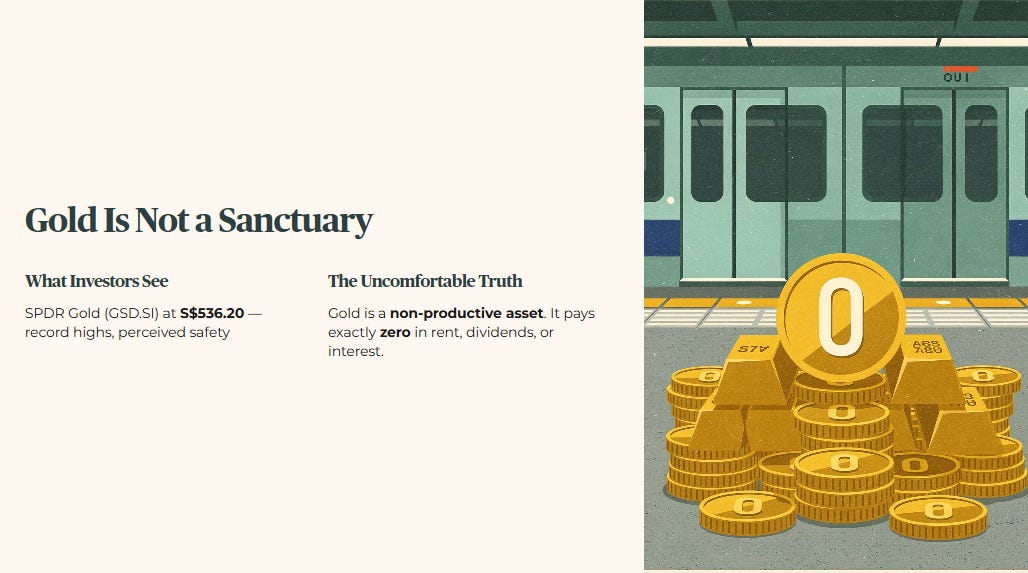

Many investors are panicking into gold — specifically the SPDR Gold Shares (GSD) or the UOB Gold Savings Account (GSA). They see the record highs, with the SGD counter GSD.SI trading at S$536.20, and think they have found a sanctuary.

Here is the uncomfortable truth. Gold is not a sanctuary for an income-starved retiree. It is a non-productive asset that pays you exactly zero dollars in rent, dividends, or interest.

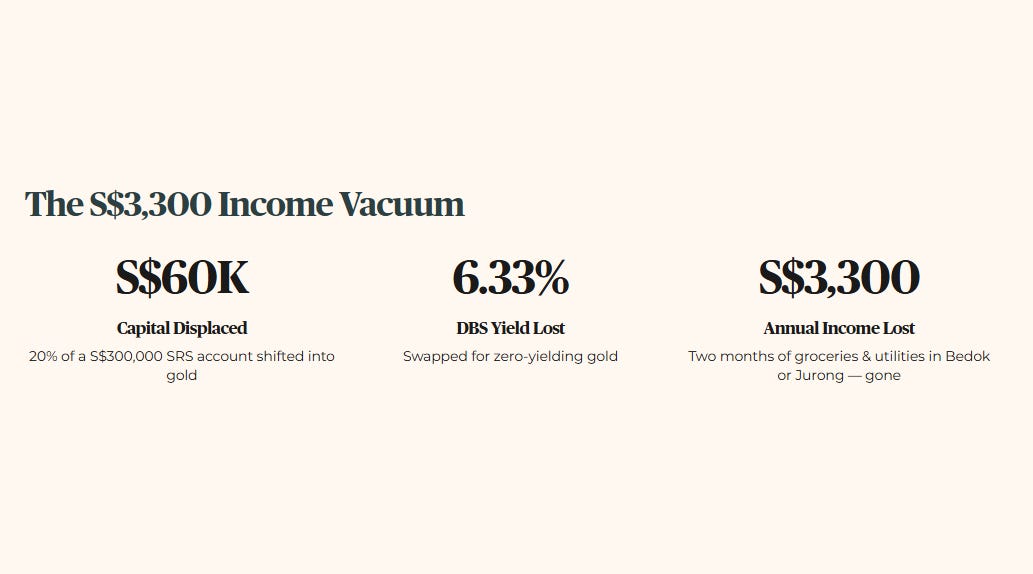

When you swap a 6.33 percent yielding DBS allocation for gold, you are not just buying safety. You are firing your most productive workers. For a 58-year-old managing a S$300,000 SRS account, a 20 percent shift into gold displaces S$60,000 of capital. That displacement creates an annual income vacuum of S$3,300. That is two months of groceries and utilities for a typical household in Bedok or Jurong, gone in the name of hedging.

Step 1: The Health Check (Solvency)

When the macro environment shifts, forensic discipline demands we look for a Fortress Balance Sheet first. If you insist on playing the gold theme through equities rather than bullion, you likely ended up looking at CNMC Goldmine (5TP).

On paper, CNMC is untouchable. With an ICR of 363x, they are the uncle who owns his HDB flat fully paid and keeps six figures in the bank. He is safe. But at a stock price of S$1.51, you pay a king’s ransom to sit at his table.

Financial Health Checklist: CNMC Goldmine (5TP)

The balance sheet is a mathematical fortress. But a fortress sitting behind a 118.8 percent entry premium is a fortress you cannot afford to live in.

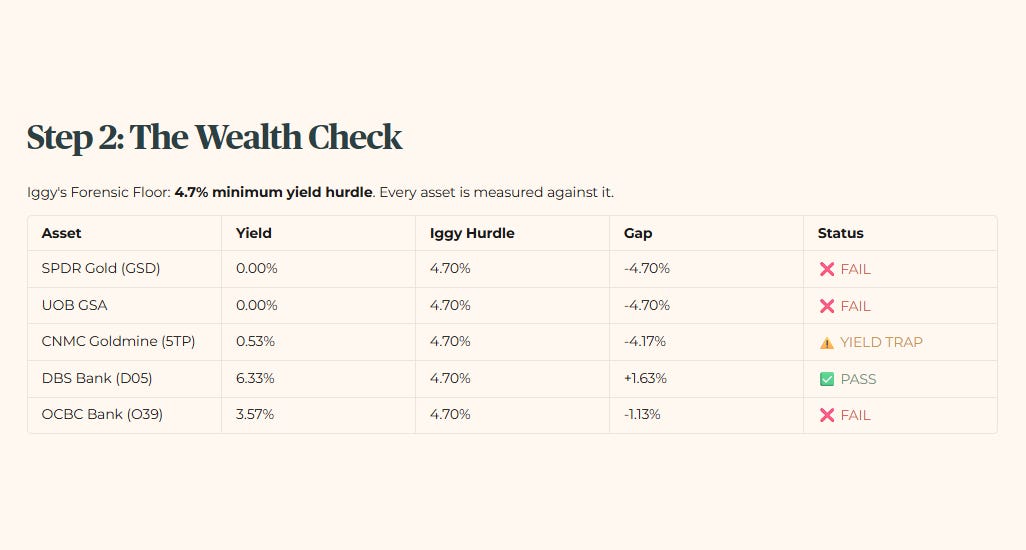

Step 2: The Wealth Check (Yield and Cash Flow)

This is where the dividend arithmetic breaks for the Singaporean retiree. We do not just look at absolute yield. We look at the Risk Premium above Iggy’s Forensic Floor.

Dividend Trajectory: The Income Vacuum

Iggy’s Insight: The OCBC Warning Shot

Take a hard look at that OCBC figure. At 3.57 percent, a cornerstone of the Singapore Sanctuary has officially fallen below Iggy’s 4.7 percent Minimum Yield Hurdle. When even our local banks start to squeeze the yield, the retiree’s margin for error disappears.

You cannot afford to park 20 percent of your portfolio in gold earning zero percent while your safe alternatives also begin to lean out. In the Kopitiam of Singapore finance, the free coffee is gone. This is not a rotation signal. It is a concentration warning. With one leg of the bank trio wobbling, the burden on your remaining high-fidelity yielders just got heavier. If your Sanctuary yields less than a T-Bill plus a risk premium, it is just a decorated vault.

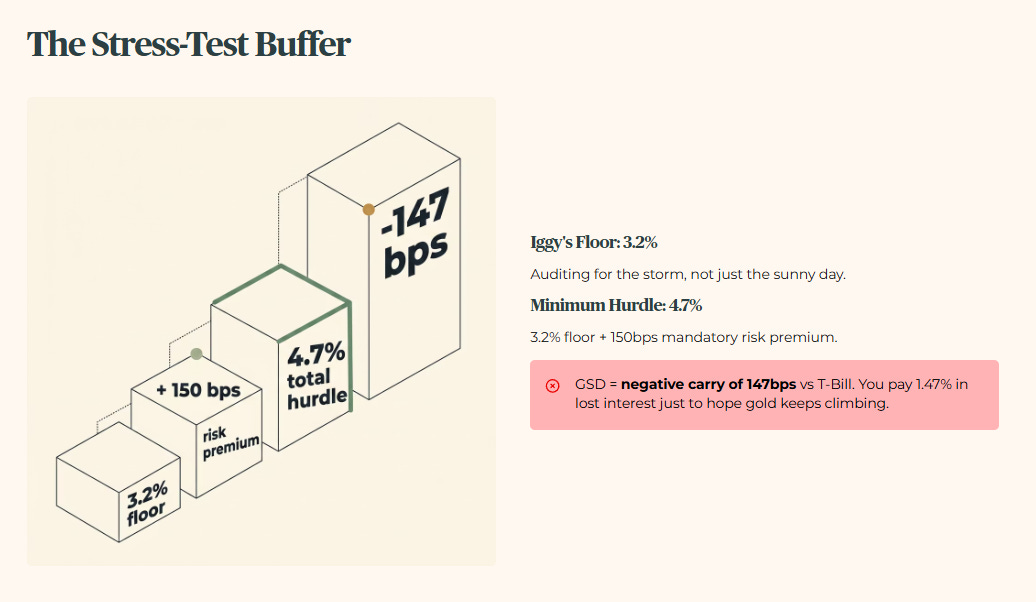

A note on the Stress-Test Buffer: For this audit, I apply a conservative floor of 3.2 percent. We audit for the storm, not just the sunny day. While the T-Bill sits at 1.47 percent, I do not lower my standards to match a temporary market dip. My floor remains at 3.2 percent to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle is 4.7 percent: the 3.2 percent floor plus 150 basis points of mandatory risk premium.

With the T-Bill at 1.47 percent, GSD represents a negative carry of 147 basis points. You are paying 1.47 percent in lost interest just to hope a yellow metal keeps going up in price.

The yield gap and negative carry are already brutal — but once we run the valuation spread in the next section, the 118.8 percent premium on CNMC turns that “insurance” into the most expensive S$3,300 mistake in your retirement math.