ST Engineering 3Q2025: The $32.6B Order Book That Changes Everything for SGX Investors

Is ST Engineering’s record-high order book and 23-cent dividend payout the next growth catalyst for Singapore’s aerospace and defence titans? Here’s what your portfolio needs to know.

It’s not often you see a Singapore-listed company hit a 30-billion-dollar order book while simultaneously rewarding shareholders with a 23-cent dividend that translates to a ~5% yield. But that’s exactly what ST Engineering just delivered. And frankly, most investors haven’t caught up to what this means.

The question that landed in my inbox repeatedly this week was simple: Should I be piling into STE right now, or is the story already priced in? That’s the exact conversation we need to have. Because the numbers tell a very different story depending on when you’re reading this, and more importantly, where the company is actually heading.

Here’s what’s happening with ST Engineering, and why the next 18 months will define whether this is a buy-and-hold dividend play or a cyclical momentum trade.

As always, I’ve attached ST Engineering’s Results (in PDF) for you to download and refer to as you read this article. Download it below:

In This Article:

• The Headlines You’ve Seen (But Probably Misunderstood)

• Group Highlights: The Organic Revenue Story Behind The Growth

• Revenue by Segment: Where The Real Growth Is

• Commercial Aerospace: The Engine MRO Boom (And The Coming Plateau)

• Defence & Public Security: The Fortress

• Urban Solutions & Satcom: The Story That Didn’t Deliver

• Contract Wins and Order Book: The Real Treasure

• Portfolio Management: The Honest Truth About STE’s Capital Allocation

• Dividends: Why This Matters More Than You Think

• Dividend Policy: What Comes Next

• Five-Year Targets: The Ambition

• Deep Analysis: What The Numbers Really Mean

• The Investment Case: Buy, Hold, or Sell?

• Key Risks You Need To Watch

• Strategic Next Steps For Your Portfolio

• Related Deep-Dive Reading

• The Bottom Line

The Headlines You’ve Seen (But Probably Misunderstood)

ST Engineering just reported 9M2025 results that look solid on the surface. Nine percent revenue growth year-on-year to S$9.1 billion. Strong growth across all three business segments. And that record S$32.6 billion order book as of 30 September 2025.

But here’s where most Singapore investors stop reading. And that’s exactly where the real story begins.

Group Highlights: The Organic Revenue Story Behind The Growth

ST Engineering’s 9-month revenue hit S$9.1 billion, up 9 percent compared to 9M2024. In the third quarter alone, quarterly revenue climbed 13 percent to S$3.1 billion, compared to S$2.8 billion in 3Q2024.

Now, before you get too excited, I need to pull back the curtain on one critical detail. This company divested LeeBoy in 3Q2025. Without that divestment distortion, the actual organic revenue growth was 10 percent for the nine-month period. That’s still solid, but it tells you two things. First, management is actively cleaning up the portfolio. Second, the core business is growing steadily, not explosively.

Think of it this way. If your hawker stall revenue goes from S$100,000 to S$105,000, but you sold off your curry puff section for S$20,000 cash, are you really growing at 5 percent? Not really. Your core noodle business might be growing at 8 percent. That’s the distinction you’re looking at here.

For a Singaporean investor with CPF funds or SRS allocations, this matters because you need to know if you’re buying a business that’s genuinely accelerating or simply liquidating assets. ST Engineering is doing both. The question is which one dominates.

Revenue by Segment: Where The Real Growth Is

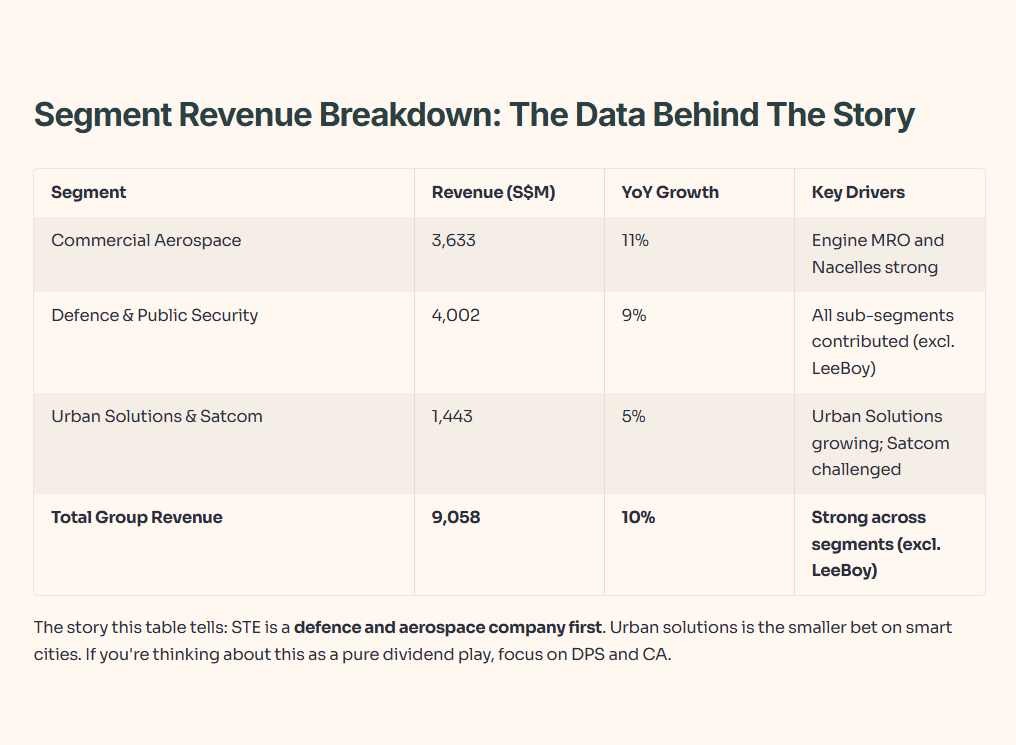

Commercial Aerospace grew 11 percent to S$3.6 billion. Defence & Public Security hit S$4.0 billion, up 9 percent. Urban Solutions & Satcom reached S$1.4 billion, up 5 percent.

Here’s the breakdown that matters for your portfolio.

Commercial Aerospace is the star. An 11-percent revenue increase in a post-pandemic aviation environment is genuinely impressive. The company is benefiting from two massive tailwinds. First, the recovery in commercial aviation MRO (maintenance, repair, and overhaul). Airlines are flying more, older aircraft need more maintenance, and that’s money in STE’s pocket. Second, there’s this thing called Passenger-to-Freighter conversions. With e-commerce booming across Asia, freight capacity is gold. STE is converting old passenger planes into cargo machines, and that’s a high-margin business.

The challenge? The company notes that lower PTF revenue partially offset the gains. Translation: the conversion business might be cooling. That’s worth watching in the fourth quarter and into 2026.

Defence & Public Security grew 9 percent organically when you strip out LeeBoy. That’s the backbone of this company. Government contracts. Long-term relationships. Sticky revenue. The segment won S$6.6 billion in new contracts during the first nine months of 2025. That’s where the order book strength is coming from. For Singapore investors focused on dividend sustainability, this segment is your safety net.

Urban Solutions & Satcom? It’s growing at 5 percent. Honestly, this is the laggard. It’s driven by Urban Solutions specifically, but the Satcom side has real headwinds. The company took a S$689 million impairment charge on iDirect Group, a satcom business that they now clearly view as overvalued. And there’s a S$22 million impairment on JetTalk, another satellite product. These write-downs tell you that the satcom market isn’t playing out as management expected. That’s important context because this segment represents your exposure to the smart city boom across Southeast Asia.

The story this table tells: STE is a defence and aerospace company first. Urban solutions is the smaller bet on smart cities. If you’re thinking about this as a pure dividend play, focus on DPS and CA.

Commercial Aerospace: The Engine MRO Boom (And The Coming Plateau)

Commercial Aerospace revenue jumped 22 percent in 3Q alone, reaching S$1.3 billion. For the nine months, that’s S$3.6 billion, up 11 percent.

This is the segment where the post-pandemic recovery is most visible. The reason? Airlines are running harder and longer. Engines need maintenance. MRO shops are swamped. And STE has world-class maintenance capabilities across multiple aircraft platforms.

The company won S$1.4 billion in new contracts during 3Q. Here’s what caught my attention: multi-year Airbus A380 heavy maintenance and cabin modification. That’s a contract that could run for five to ten years. Engine MRO. Component MRO. And an A330 Passenger-to-Freighter conversion from an air freight provider.

Why does this matter? Because it tells you that STE is building long-term recurring revenue streams. The A380 contract is exactly the type of sticky, multi-year business that justifies a high dividend. You’re not relying on one-off deals. You’re building a durable maintenance base.

But here’s the risk that nobody’s talking about. The global aerospace MRO market is starting to plateau. We’re two years into the post-pandemic recovery. Airlines are reaching a steady-state flying pattern. The explosive growth phase might be ending. That means STE’s Commercial Aerospace segment could face headwinds in 2026 if the market normalizes.

For CPF investors considering STE as a core holding, this is the segment to watch closely. A slowdown here affects your dividend.

Defence & Public Security: The Fortress

This is where STE prints money. S$4.0 billion in revenue for 9M2025, up 9 percent. Excluding LeeBoy, the base business grew 11 percent.

The contracts STE won in 3Q are worth examining closely. AI-powered 5G edge solutions. Data centre services. Next-gen broadband communications systems. Advanced cybersecurity systems. Secure data transfer products. Earth observation satellite systems. Commercial satellite imagery. Ammunition. Hybrid electric vehicles. And a floating power plant for the Dominican Republic.

I’ll be direct with you. This is not glamorous. But it’s where the dividends come from. Governments need these capabilities. They’re not shopping around based on price. They’re buying security, resilience, and trust. And STE has the track record and certifications to win those contracts repeatedly.

The order book for DPS is now over S$20 billion. Think about that. That’s visibility into revenue for the next five to seven years. For a dividend investor, that’s extraordinarily valuable. You’re not guessing whether the company will have revenue in 2027. You know it will, because the government already contracted for it.

The challenge? Geopolitical volatility. If military spending cycles shift, or if a major customer like the Singapore government deprioritizes certain programs, revenue could flatten. But that’s a tail risk, not a base case.

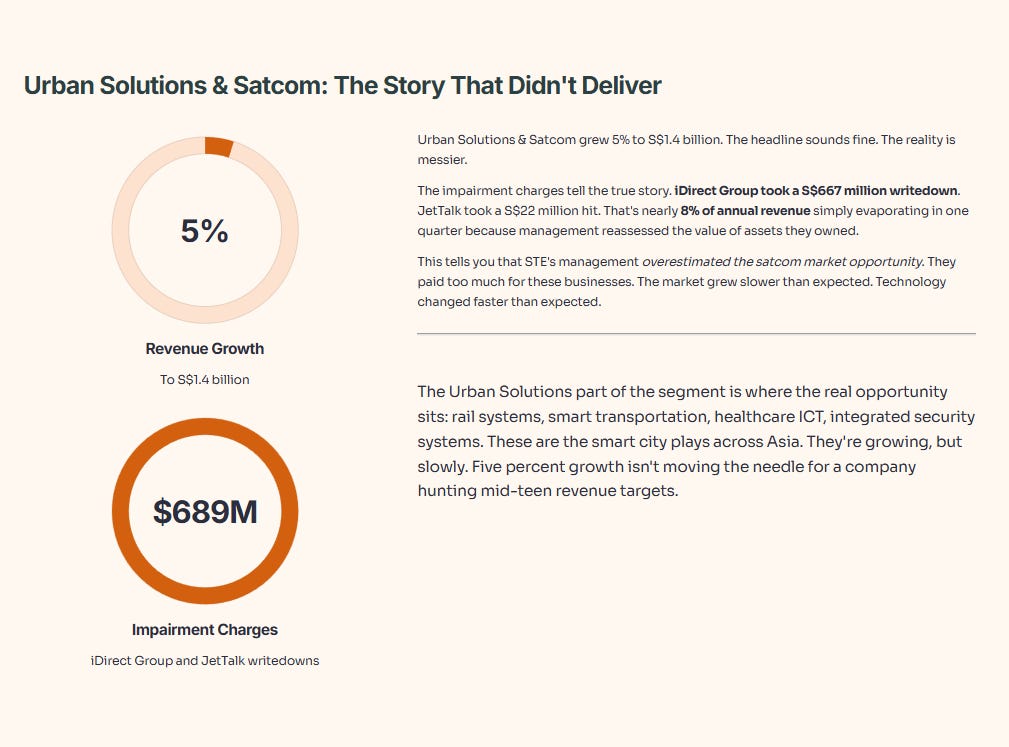

Urban Solutions & Satcom: The Story That Didn’t Deliver

Urban Solutions & Satcom grew 5 percent to S$1.4 billion. The headline sounds fine. The reality is messier.

The impairment charges tell the true story. iDirect Group took a S$667 million writedown. JetTalk took a S$22 million hit. That’s S$689 million in total impairment losses. To put that in perspective, that’s nearly eight percent of annual revenue, simply evaporating in one quarter because management reassessed the value of assets they owned.

Why does this matter? Because it tells you that STE’s management overestimated the satcom market opportunity. They paid too much for these businesses. The market grew slower than expected. Technology changed faster than expected. And now they’re cleaning up. For a conservative investor, this is a necessary evil. It hurts shareholder equity today, but it prevents a slower bleed from overvalued assets tomorrow.

The Urban Solutions part of the segment is where the real opportunity sits. Rail systems. Smart transportation. Healthcare ICT. Integrated security systems. These are the smart city plays across Asia. They’re growing, but slowly. Five percent growth isn’t going to move the needle for a company hunting mid-teen revenue targets over the next five years. This is clearly the “black sheep” of the portfolio compared to the “Golden Child” (Defence).

Contract Wins and Order Book: The Real Treasure

This is the headline that matters most. S$14.0 billion in contract wins for 9M2025. S$32.6 billion in order book as of 30 September 2025. And S$2.8 billion expected to be delivered in 4Q2025.

Here’s why this matters for your dividend. That S$32.6 billion order book is not speculative. It’s contractual. Governments and customers have signed on the dotted line. They’re paying STE to deliver services and products. That cash is coming in.

For a CPF or SRS investor, this is what you want to see. Not growing revenue. Contracted revenue. There’s a meaningful difference.

The breakdown by segment tells you where the durability sits. CA won S$4.1 billion. DPS won S$6.6 billion. USS won S$3.4 billion.

Defence is the fortress. But Commercial Aerospace is the growth engine. S$4.1 billion in new CA contracts, mostly for maintenance and modification work. That’s durable. That’s sticky. And that’s repeatable.

Portfolio Management: The Honest Truth About STE’s Capital Allocation

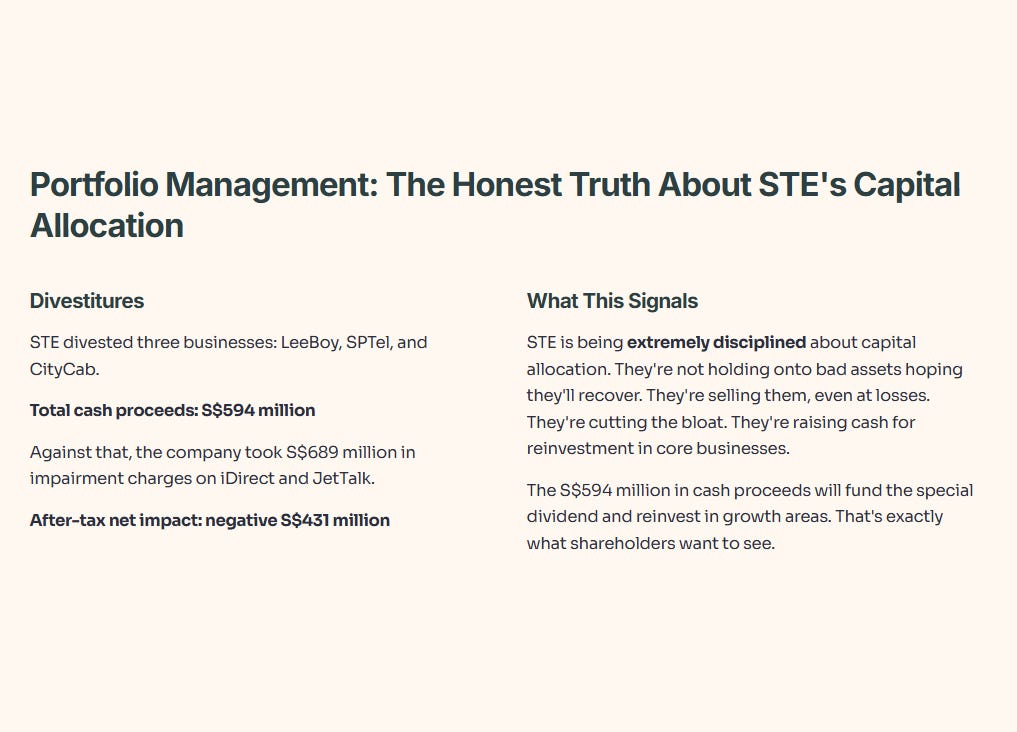

STE divested three businesses: LeeBoy, SPTel, and CityCab. Total cash proceeds: S$594 million.

Against that, the company took S$689 million in impairment charges on iDirect and JetTalk. After-tax net impact: negative S$431 million.

Translation? STE is being extremely disciplined about capital allocation. They’re not holding onto bad assets hoping they’ll recover. They’re selling them, even at losses. They’re cutting the bloat. They’re raising cash for reinvestment in core businesses.

For a dividend investor, this is actually reassuring. The company is not pretending to be bigger than it is. It’s not padding the balance sheet with overvalued assets. It’s cleaning house.

The S$594 million in cash proceeds will be used to fund the special dividend and reinvest in growth areas. That’s exactly what shareholders want to see.

Dividends: Why This Matters More Than You Think

Here’s what STE declared for FY2025.

Three quarterly interim dividends of 4.0 cents per share each. That’s 12.0 cents paid in the first three quarters.

A final dividend of 6.0 cents per share is planned for shareholder approval at the 2026 AGM.

And here’s the kicker: a special dividend of 5.0 cents per share, also pending shareholder approval.

Total FY2025 dividend: 23.0 cents per share.

Let me put that in context. STE shares trade around S$4.50 – S$4.80 depending on market conditions. A 23-cent dividend on a S$4.60 share price (mid-range) is approximately a 5.0% yield.

That is jaw-dropping for a blue-chip Singaporean defence and aerospace company with this kind of order book visibility. For a CPF or SRS investor hunting dividend yield, this is exceptional. You’re getting a significantly higher yield than your CPF Ordinary Account, backed by steady, growing dividends from contracted revenue.

But here’s what matters more: the dividend is growing. The board is targeting to increase dividends in tandem with profit growth. And with that S$32.6 billion order book, profit growth is the baseline scenario for the next three to five years.

Dividend Policy: What Comes Next

This is where the real opportunity sits. Starting in FY2026, STE is implementing a new dividend policy.

Base dividend of 18 cents per share (equivalent to FY2025’s ordinary portion).

Plus one-third of year-on-year incremental net profit, paid as additional dividends.

This is a super important framework for Singaporean investors because it means dividends scale directly with profit. If the company grows net profit from S$2 billion to S$2.5 billion, shareholders get one-third of that S$500 million incremental profit as dividends.

The CEO’s message confirms this thinking. Quote: “The Group remains financially strong to re-invest to pursue growth or pay down debt.” Translation? STE is choosing to grow. And as it grows, dividends will follow.

Five-Year Targets: The Ambition

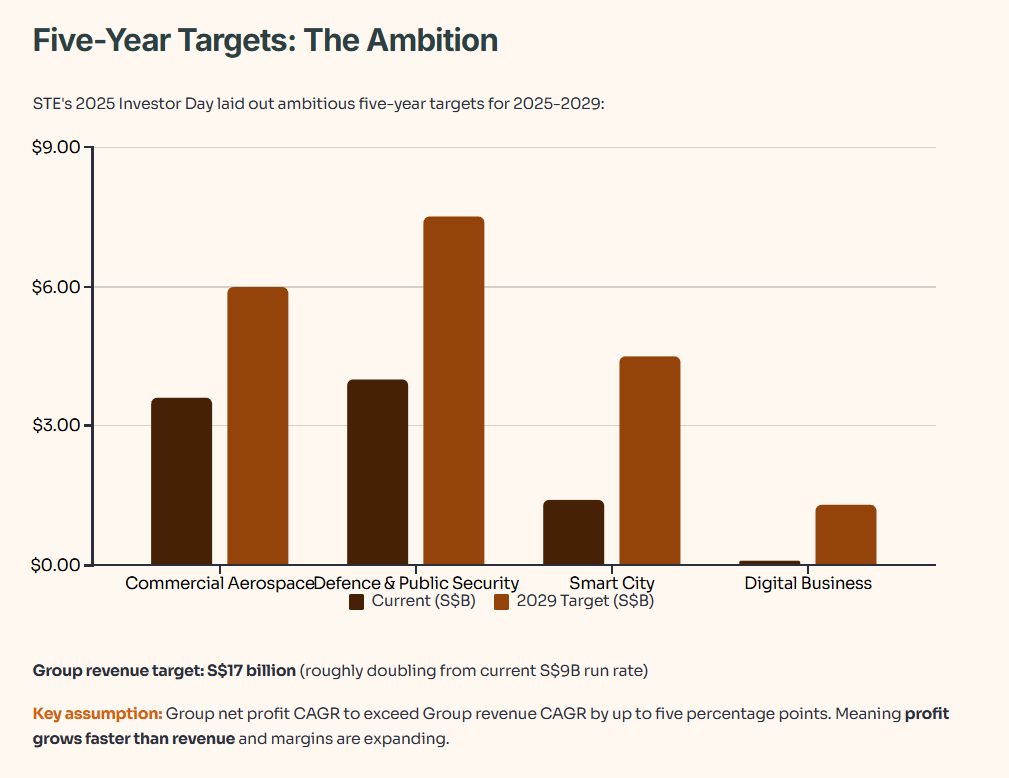

This is the final piece of the puzzle. STE’s 2025 Investor Day laid out five-year targets for 2025-2029.

Group revenue to S$17 billion. That’s roughly doubling from the current run rate of S$9 billion for nine months.

Commercial Aerospace revenue to S$6.0 billion. That’s a doubling from the current S$3.6 billion run rate.

Defence & Public Security revenue to S$7.5 billion. That’s roughly a 100-percent increase.

Smart City revenue to S$4.5 billion. That’s a near-tripling from the current S$1.4 billion run rate.

Digital business revenue to S$1.3 billion. That’s a greenfield business area where they’re starting from near-zero.

And here’s the kicker: Group net profit CAGR to exceed Group revenue CAGR by up to five percentage points. Meaning profit grows faster than revenue. Meaning margins are expanding.

Now, is this realistic? Let’s do the math. S$17 billion revenue by 2029 from S$9 billion in 2024 (base year). That’s a CAGR of roughly 17 percent over five years. The company is assuming global GDP growth of 3.15 percent. So they’re targeting to grow at 5.4x the rate of global GDP. That’s ambitious, but not ridiculous in aerospace and defence.

The key assumption is that global aerospace MRO and OE markets grow at a specific rate, and STE captures more than its fair share. That’s the bet you’re making as a shareholder.

Deep Analysis: What The Numbers Really Mean

Here’s the honest assessment.

ST Engineering is a transition story. It’s moving from a diversified industrial conglomerate toward a focused aerospace, defence, and smart city company. The portfolio cleanup, the impairments, the divestitures, they’re all part of that reshaping.

The dividend opportunity is real. S$32.6 billion in order book is real. The five-year growth targets are ambitious, but grounded in market fundamentals.

But there are risks you need to see clearly.

First, the Commercial Aerospace segment is cyclical. Post-pandemic recovery has been strong, but the MRO market can cool fast if airline flying hours decline or if excess maintenance capacity emerges. That’s a 2026 risk worth monitoring.

Second, Satcom is proving harder than expected. The massive impairments suggest management misjudged technology transition and market demand. That’s not a death blow, but it’s a warning flag about strategic planning.

Third, Urban Solutions is growing slowly. For a company hunting mid-teen growth rates, a 5-percent growing segment is a drag on consolidated numbers.

Fourth, geopolitical risk. Defence & Public Security represents the largest segment. A shift in government spending priorities, a trade conflict, or a policy change could affect revenue visibility. It’s unlikely, but not impossible.

The Investment Case: Buy, Hold, or Sell?

Here’s my verdict.