ST Engineering: Riding High But Is the Valuation Party Over?

When Defence Darlings Meet Reality - A 70% Rally That Has Smart Money Asking Questions

Editor’s Note: This post has been updated on October 19, 2025, to ensure it is fresh and accurate. It now includes new analysis on ST Engineering’s stretched valuation and what its collapsed 2% dividend yield means for investors holding the stock in their CPF Investment Account (CPFIA).

ST Engineering has soared to record highs, but seasoned investors are asking the million-dollar question: Can this defence darling keep defying gravity, or is it time to take profits before the music stops?

If you’ve been watching ST Engineering’s meteoric rise, you’re not alone. The stock has jumped 70% this year while the broader market crawled ahead by just 13%. But here’s the thing that’s keeping smart money awake at night: OCBC’s Ada Lim just dropped a reality check that every Singapore investor needs to hear.

She says the company’s growth story stays strong, but the risk-reward balance is getting “balanced” – Wall Street speak for “maybe we’ve run too far, too fast.” This isn’t doom and gloom talk. It’s the kind of honest assessment that separates winning investors from those who ride the elevator all the way back down.

In This Article

Introduction: Can This Defence Darling Keep Defying Gravity?

The Numbers Behind the Hype

Where the Money’s Coming From

The Global Defence Spending Tsunami

The Valuation Reality Check

What Smart Money Is Thinking

The Iguana’s Take

The Numbers Behind the Hype

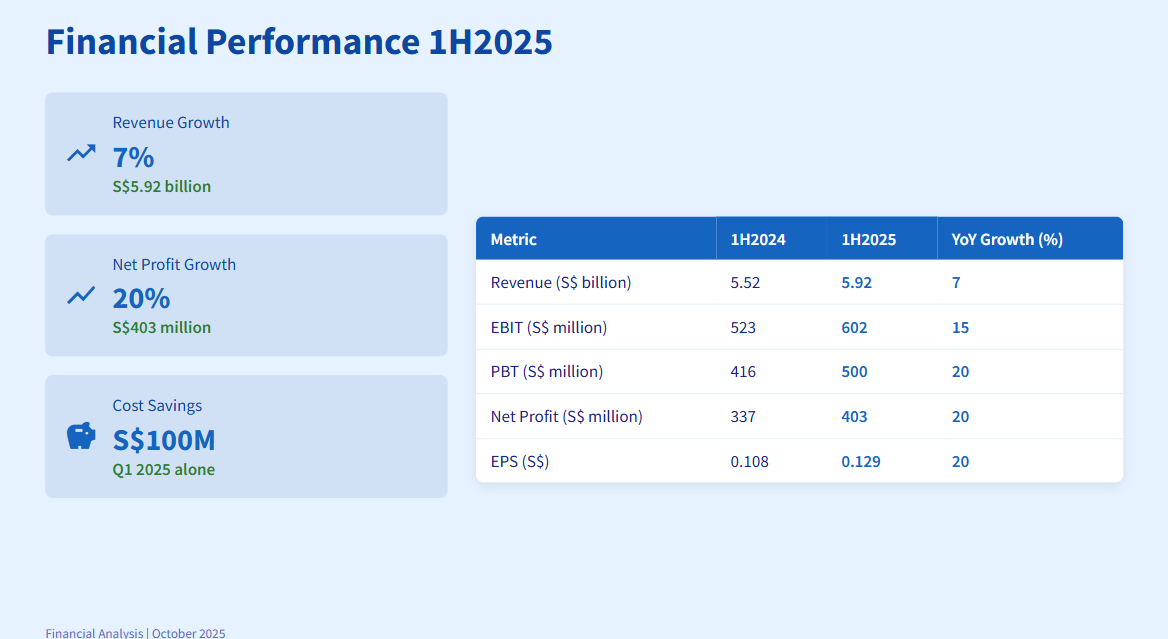

ST Engineering delivered exactly what the bulls wanted in 1H2025. Revenue jumped 7% to S$5.92 billion, but the real story was profit growth crushing revenue growth. Net profit rocketed 20% to S$403 million, showing this isn’t just about top-line expansion – it’s about operational excellence.

Table 1: Profit Soars Past Revenue (1H2025 vs 1H2024)

The company’s profit margins expanded while revenue grew – that’s the hallmark of a business firing on all cylinders. Management slashed S$100 million in costs during the first quarter alone, proving they can walk the walk on operational efficiency.

Where the Money’s Coming From

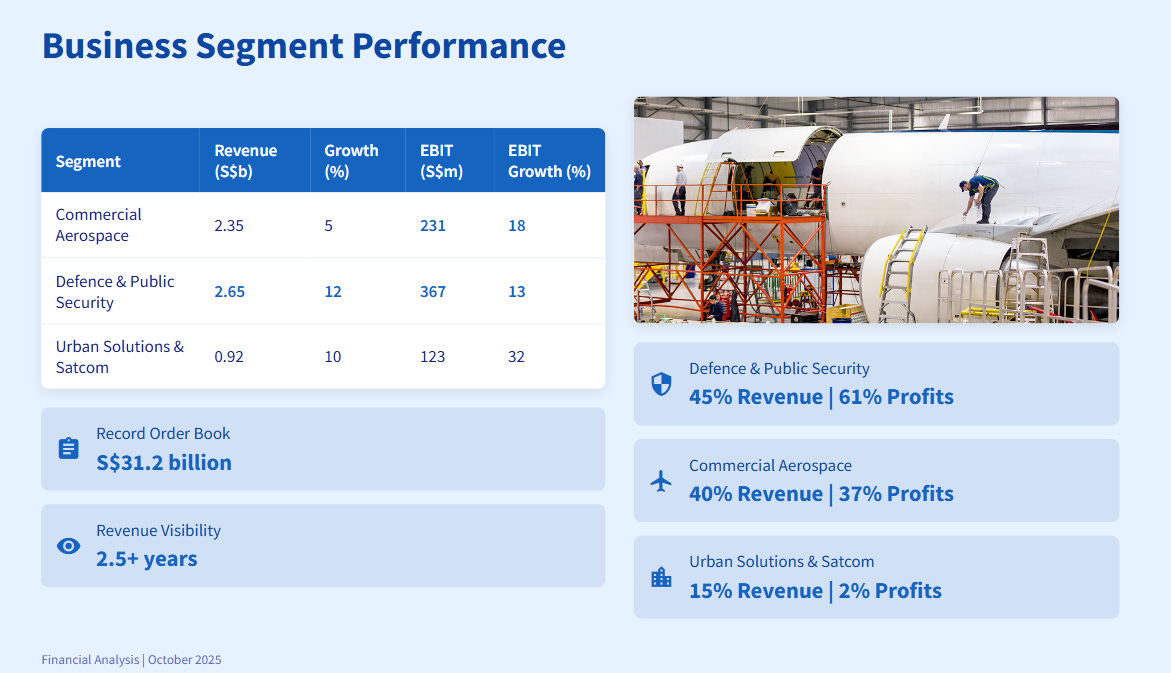

Three business segments drove this performance, but they’re not all created equal. Defence & Public Security dominated with 45% of revenue and a whopping 61% of profits. This segment grew revenue 12% and saw EBIT jump 13% to S$367 million.

Table: Business Segment Performance 1H2025

Commercial Aerospace contributed 40% of revenue with steady 5% growth, while EBIT surged 18%. The segment benefits from post-pandemic recovery and strong MRO demand. Urban Solutions & Satcom stayed flat on revenue but EBIT jumped 32% – small but improving.

The company’s order book tells the real story about future prospects. It hit a record S$31.2 billion, up from S$27.4 billion at year-end 2024. That’s over 2.5 years of revenue visibility – a luxury most companies can only dream about.

The Global Defence Spending Tsunami

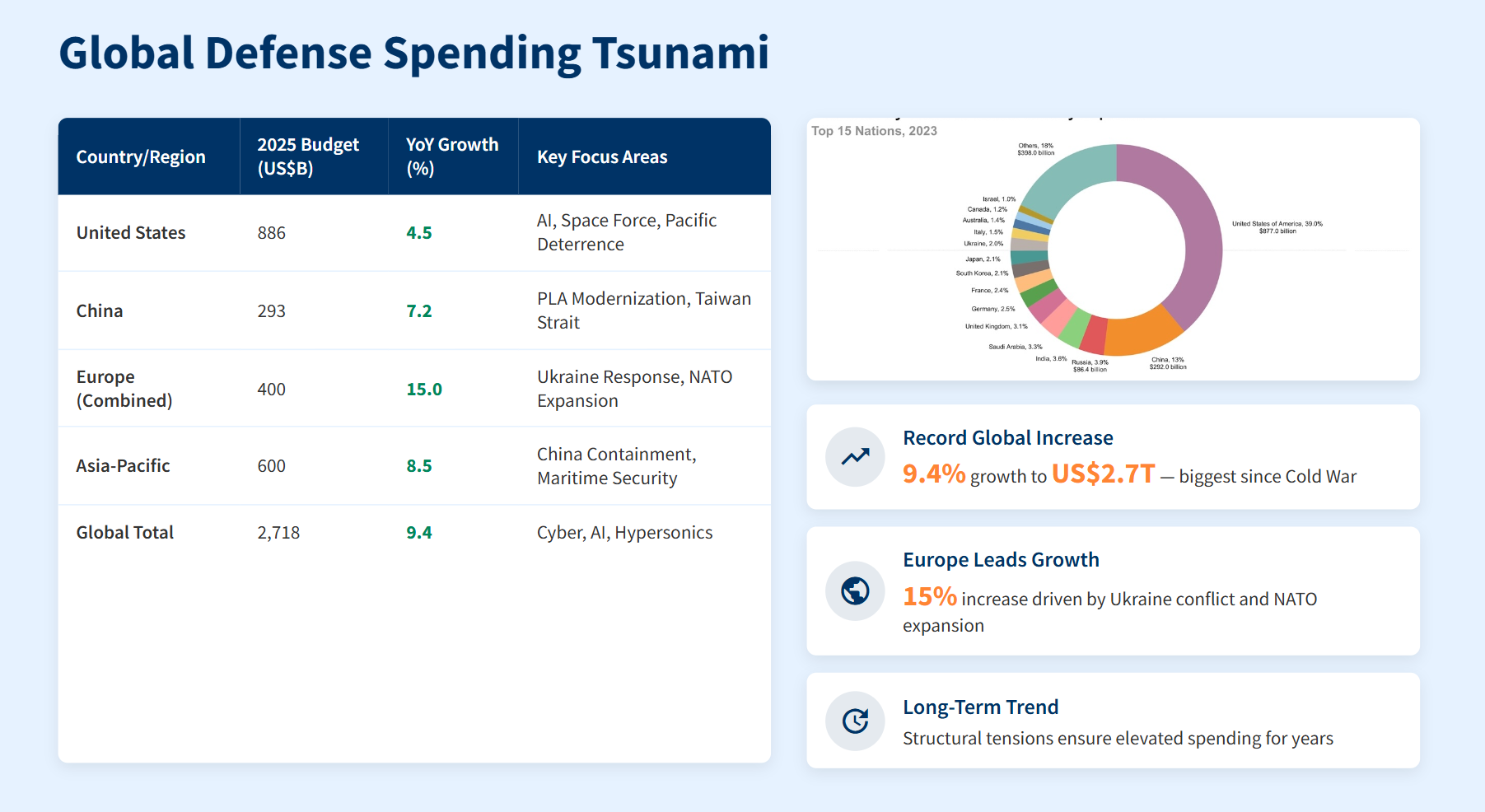

Here’s why OCBC’s Ada Lim calls the growth story “intact” – global defence spending is exploding. The numbers are staggering: worldwide military budgets jumped 9.4% in 2024 to US$2.7 trillion, the biggest increase since the Cold War ended.

Table: Global Defence Spending Growth 2025

Europe leads with 15% growth, driven by the Ukraine conflict and NATO expansion. China bumped spending 7.2% to US$293 billion, focusing on Taiwan Strait tensions. Even the US, already spending US$886 billion, keeps pushing higher for AI and Pacific deterrence.

This isn’t a short-term spike. Structural tensions around Taiwan, Russia-Ukraine, and Middle East conflicts ensure defence spending stays elevated for years. ST Engineering sits perfectly positioned to capture this wave through its global defence contracts and technology expertise.

The Valuation Reality Check

Here’s where things get uncomfortable for bulls. ST Engineering trades at a PE ratio of 52.7 times earnings – more than double its historical average of 21.8 times. The stock hit S$9.00, while analyst consensus targets average just S$8.43.

Table 4: Analysts See No Further Upside (Oct 2025 Targets)

Most analysts maintain positive ratings but their targets suggest 8-18% downside from current levels. CGS International downgraded to HOLD, noting the stock trades three standard deviations above historical averages.

The dividend yield dropped to 2% as the share price rocketed – well below the historical 3.5-4.5% range. That’s a red flag for income investors who bought ST Engineering for its reliable payouts.

For the thousands of Singaporeans holding ST Engineering in their CPF Investment Accounts (CPFIA), this is the real red flag. The dividend yield has collapsed to just 2%, which is now below the CPF-OA’s risk-free 2.5% interest rate. Investors are now paying a 52x P/E multiple for a yield that doesn’t even beat their basic CPF-OA, fundamentally challenging the ‘safe dividend’ thesis that made this a portfolio cornerstone for years

What Smart Money Is Thinking

Source: The Edge Singapore, Oct 8, 2025

OCBC’s Ada Lim hit the nail on the head: growth story intact, but risk-reward balanced. Translation? The easy money has been made. Future returns depend on flawless execution and continued defence spending growth.

The bull case remains compelling. Global defence spending shows no signs of slowing. ST Engineering’s diversified portfolio across aerospace, defence, and urban solutions provides multiple growth vectors. The record order book guarantees revenue visibility through 2027.

But the bear case is equally valid. Valuations stretch beyond reasonable levels. Any disappointment in growth rates or margin expansion could trigger sharp corrections. The stock has priced in perfection – a dangerous place for any investment.

The Iguana’s Take