4.7% Hurdle Kills Suntec At 4.69% | SGX Daily Pulse 22 Apr 2026 | 🦖EP1563

When STI hits 4,996 your broker celebrates but KIT runs 56.1% gearing on 1.3x cover while Suntec fails the 4.7% hurdle at 4.69%

A 4,996 STI level is a headline-grabbing vanity metric that pays exactly zero dollars toward your retirement. The index chases psychological milestones. The forensic truth is found in debt issuance pricing and the breach of gearing ceilings. You are holding assets where management cheers for growth while the balance sheet quietly screams for air.

Your SRS portfolio is not a tool for index-chasing. It is a sanctuary that requires the 4.7% hurdle to remain sacred.

You will walk away knowing why an 8.4% NPI growth figure is a forensic distraction in a high-leverage regime.

In This Article:

Market snapshot

The audit

Keppel Infrastructure Trust KIT structural red flag

OUE REIT gearing cleared ICR fails

Suntec REIT yield trap confirmed

Hong Leong Asia HLA yield trap confirmed

Bumitama Agri Sanctuary

Analyst chatter

Watchlist and yield spread

🦎 Iggys take the bottom line

Iggys forensic disclaimer

MARKET SNAPSHOT

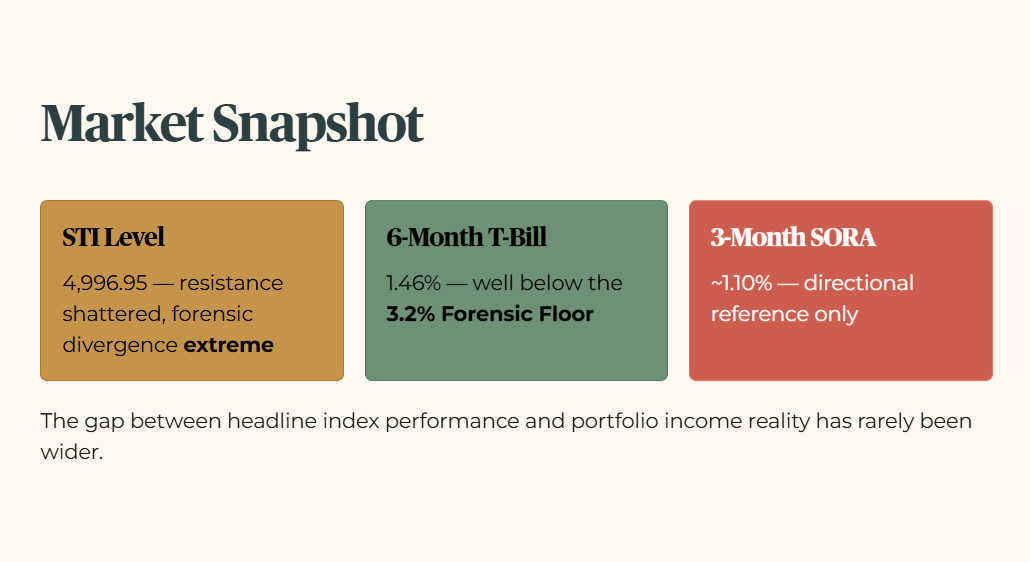

STI Level: 4,996.95 — Resistance is effectively shattered, but forensic divergence remains high.

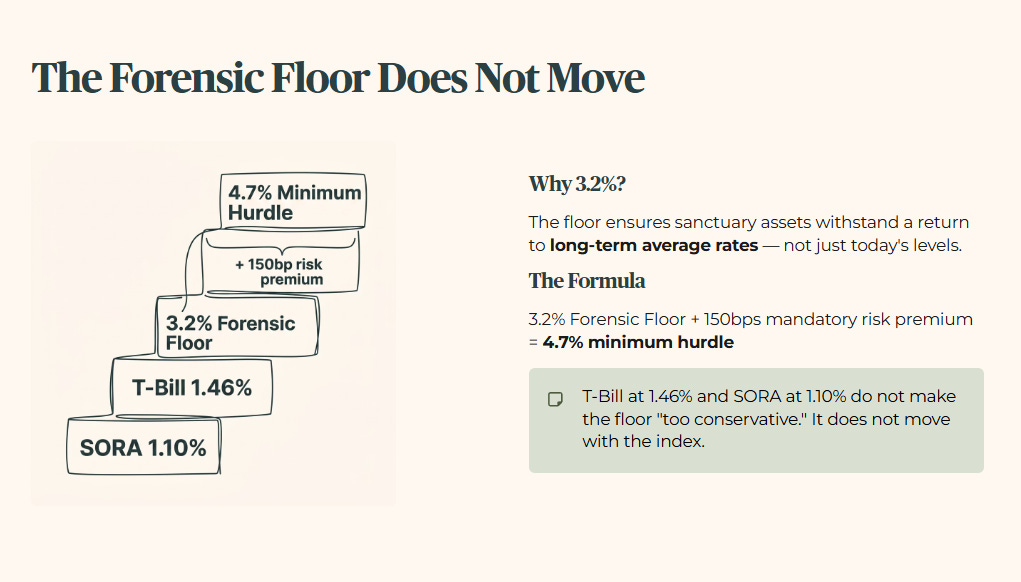

6-Month T-Bill: 1.46% (BS26106T, 26 March auction) — well below the 3.2% Forensic Floor.

3-Month SORA: ~1.10% — directional reference only; live rate fluctuating across this range.

Forensic Context: With the STI approaching 5,000, yield compression risk is at an extreme. The 3.2% floor holds regardless of index euphoria. The gap between headline index performance and portfolio income reality has rarely been wider.

THE AUDIT

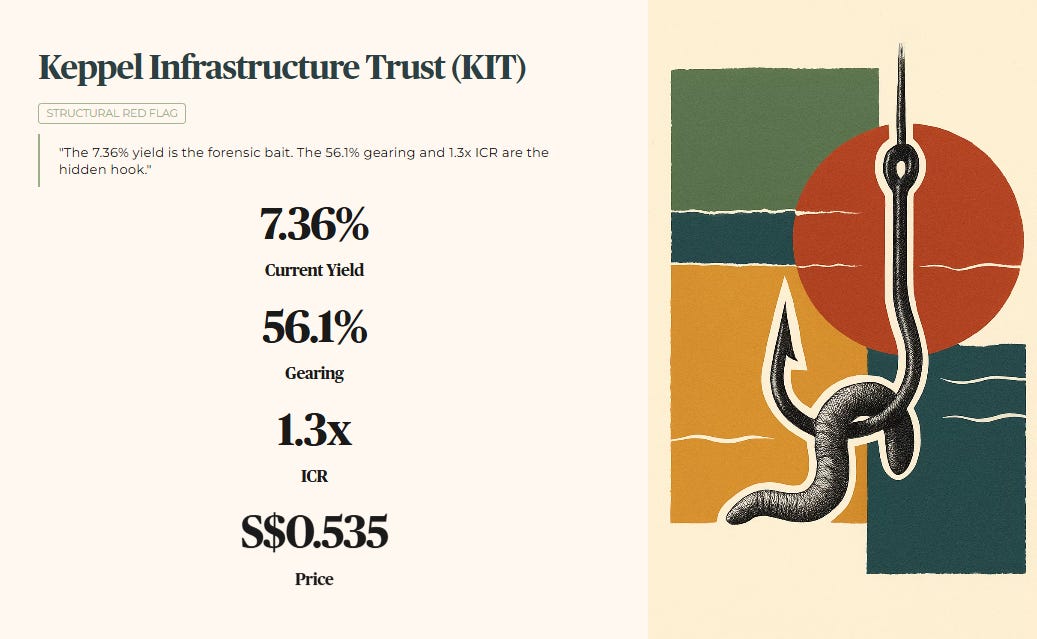

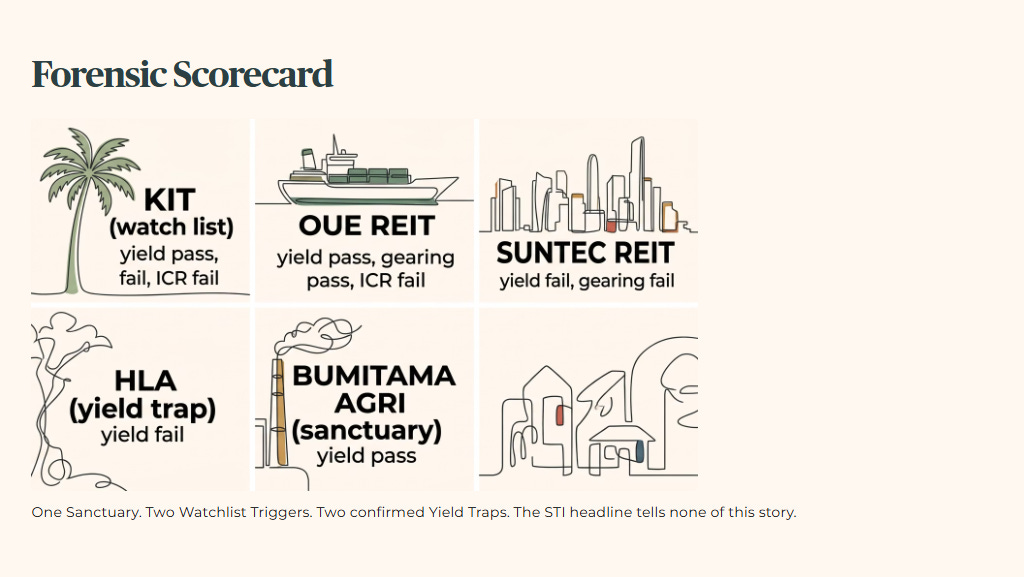

KEPPEL INFRASTRUCTURE TRUST (KIT) — STRUCTURAL RED FLAG

“The 7.36% yield is the forensic bait. The 56.1% gearing and a 1.3x ICR are the hidden hook.”

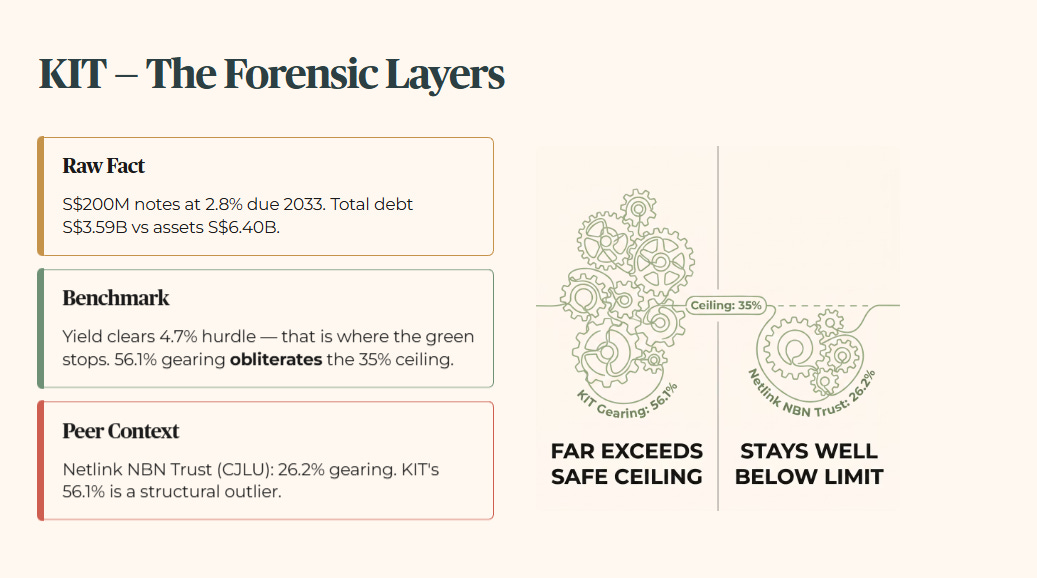

Layer 1 — Raw Fact: KIT is proposing to price S$200 million in notes due 2033 at 2.8% per annum. Total debt stands at S$3.59 billion against total assets of S$6.40 billion.

Layer 2 — Benchmark: The 7.36% yield clears the 4.7% hurdle. That is where the forensic green stops. Aggregate leverage at ~56.1% breaches the 35% gearing ceiling by a wide margin. ICR of approximately 1.3x fails the 4x Fortress Balance Sheet screen comprehensively. This is not a borderline case.

Layer 3 — Peer Context: Netlink NBN Trust (CJLU) carries gearing of 26.2%. Against that benchmark, KIT’s 56.1% is not a sector norm. It is a structural outlier that the high yield does not compensate for.

Layer 4 — Forward Scenario: New debt issuance at 2.8% into a balance sheet already running at 56.1% gearing tightens the refinancing corridor further. Any upward rate movement compresses the already-thin interest coverage. There is no buffer here for an adverse macro shift.

Layer 5 — Wallet Impact: For a 60-year-old retiree in Jurong managing an SRS drawdown, the 7.36% yield is not a gift. It is the market pricing in the structural risk that the balance sheet carries. High yield without debt clarity is a forensic red flag, not a sanctuary signal. This stays as a Watchlist Trigger until gearing normalises.

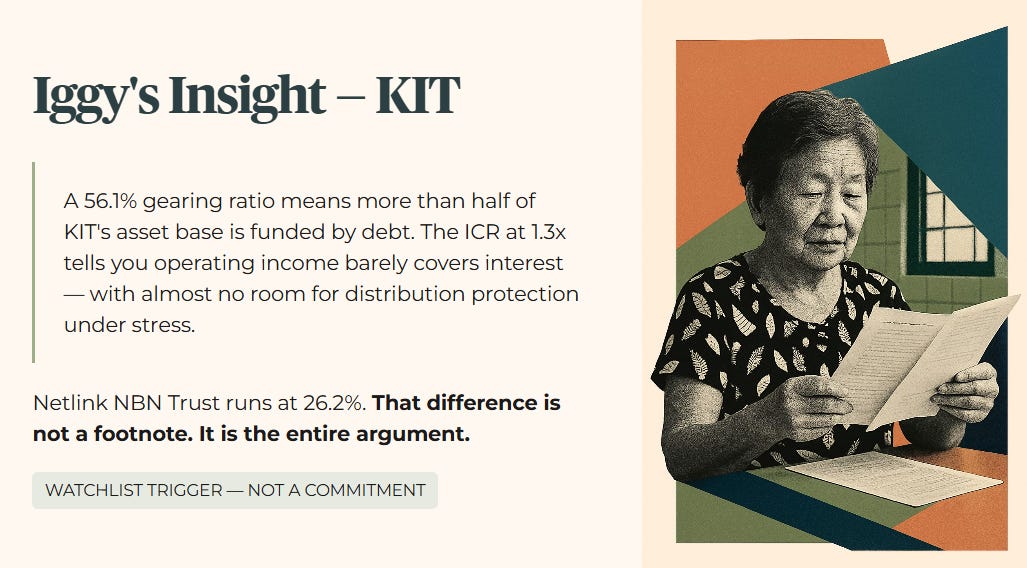

IGGY’S INSIGHT — KIT

KIT’s 7.36% yield will attract attention on a day when the STI is touching 5,000 and investors are hunting income. That is exactly the environment where forensic discipline matters most. A 56.1% gearing ratio means more than half of KIT’s asset base is funded by debt. The ICR sitting at approximately 1.3x tells you that operating income barely covers interest obligations, with almost no room left for distribution protection under stress. Netlink NBN Trust runs its infrastructure book at 26.2% gearing. That difference is not a footnote. It is the entire argument. The yield is real. The risk attached to it is equally real. Watchlist Trigger — not a commitment.

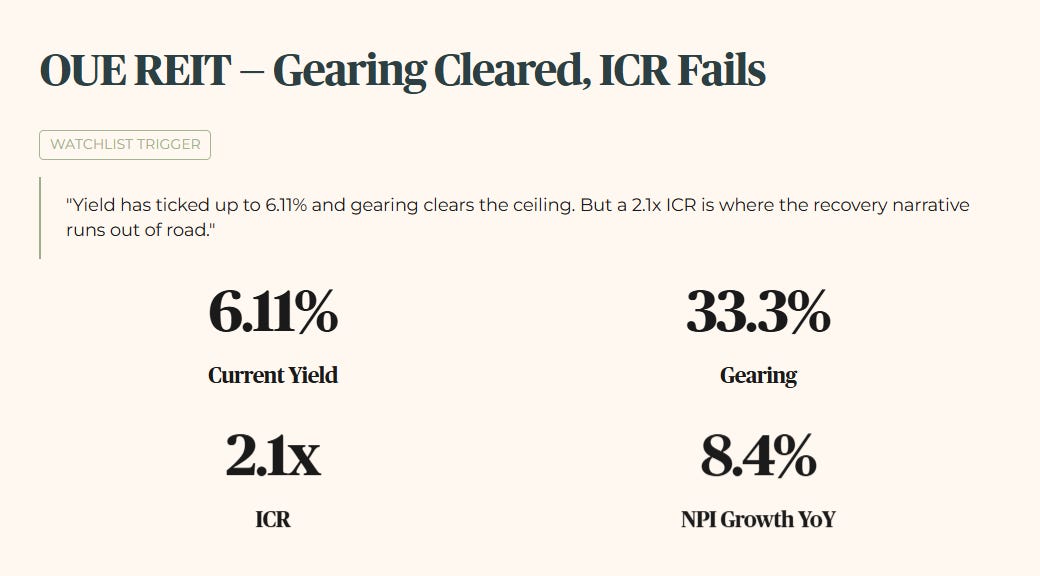

OUE REIT — GEARING CLEARED, ICR FAILS

“Yield has ticked up to 6.11% and gearing clears the ceiling. But a 2.0x ICR is where the recovery narrative runs out of road.”

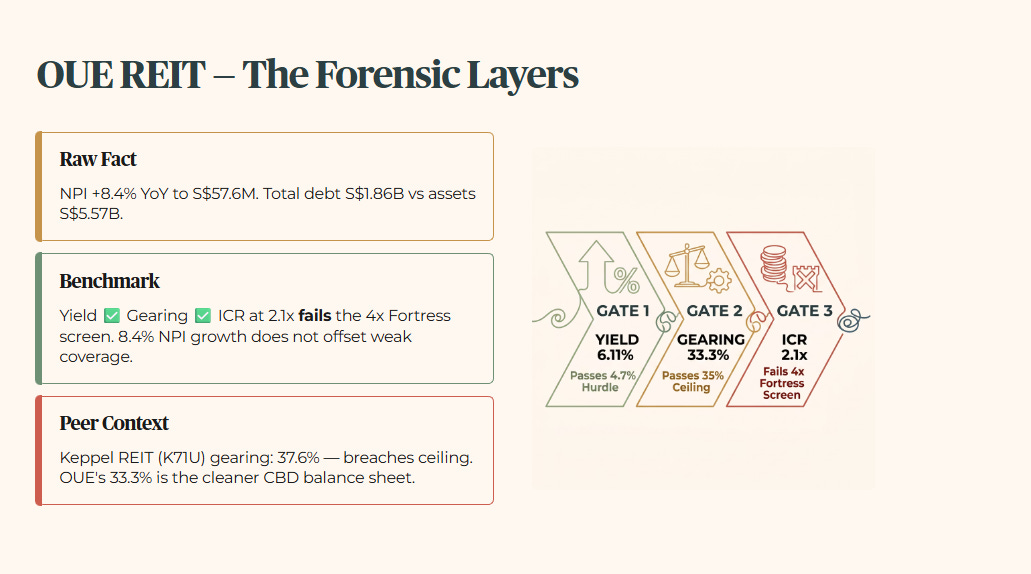

Layer 1 — Raw Fact: NPI rose 8.4% YoY to S$57.6 million, driven by hospitality segment growth. Total debt stands at S$1.86 billion against total assets of S$5.57 billion, producing a gearing ratio of 33.3%.

Layer 2 — Benchmark: The 6.11% yield clears the 4.7% hurdle. Gearing at 33.3% clears the 35% ceiling. On those two metrics, OUE REIT passes. The Fortress Balance Sheet screen adds a third gate: ICR above 4x. At approximately 2.1x, OUE REIT fails that screen. The 8.4% NPI growth is a real operational improvement. It is not sufficient to offset an interest coverage position that leaves limited headroom.

Layer 3 — Peer Context: Keppel REIT (K71U) carries gearing of 37.6%, breaching the ceiling. OUE REIT’s 33.3% is the cleaner balance sheet across the CBD-heavy peer group. That is a relative point in its favour. ICR comparison across the sector remains directionally weak.

Layer 4 — Forward Scenario: A hospitality revenue slowdown would compress NPI and press the ICR further toward the 2.0x floor. At that level, distribution sustainability becomes a live question. The gearing headroom provides some protection, but the ICR position limits the margin of safety.

Layer 5 — Wallet Impact: A 45-year-old HDB owner in Punggol using dividends as a salary supplement should treat this as a Watchlist Trigger. Gearing is under control. ICR is not. Wait for evidence that interest coverage is trending toward 3x before committing new capital.

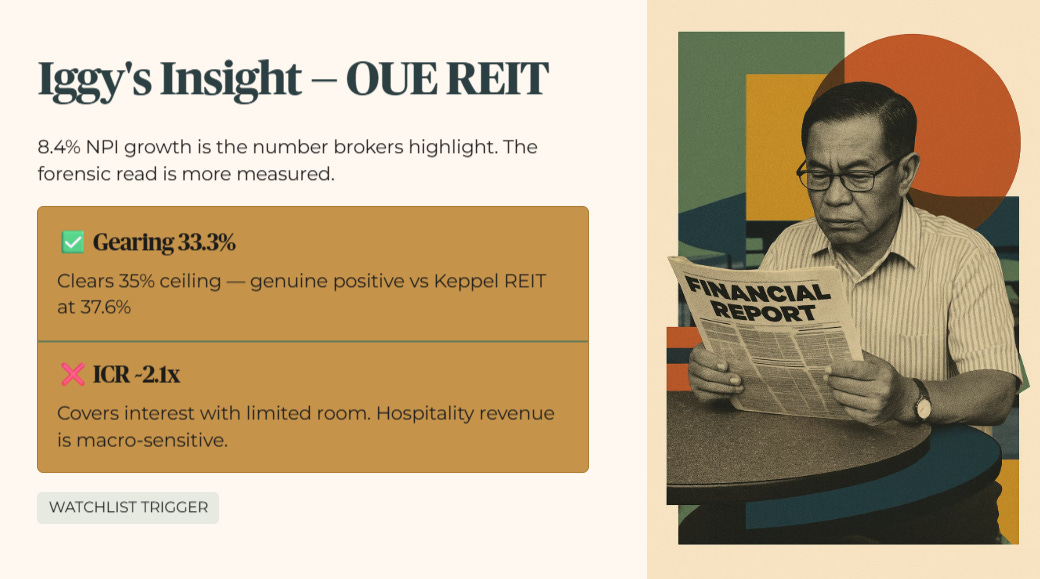

IGGY’S INSIGHT — OUE REIT

OUE REIT’s 8.4% NPI growth is the kind of number that gets highlighted in broker notes and investor presentations. The forensic read is more measured. Gearing at 33.3% clears the 35% ceiling, which is a genuine positive in a sector where peers like Keppel REIT are already over the line at 37.6%. The problem is the ICR. At approximately 2.1x, OUE REIT is covering its interest bill with limited room to spare. NPI growth improves that picture, but hospitality revenue is sensitive to macro sentiment. The Iran war wait-and-see effect on convention bookings is a live risk to that growth trajectory. Watchlist Trigger — the gearing story is better than expected. The ICR story is not.

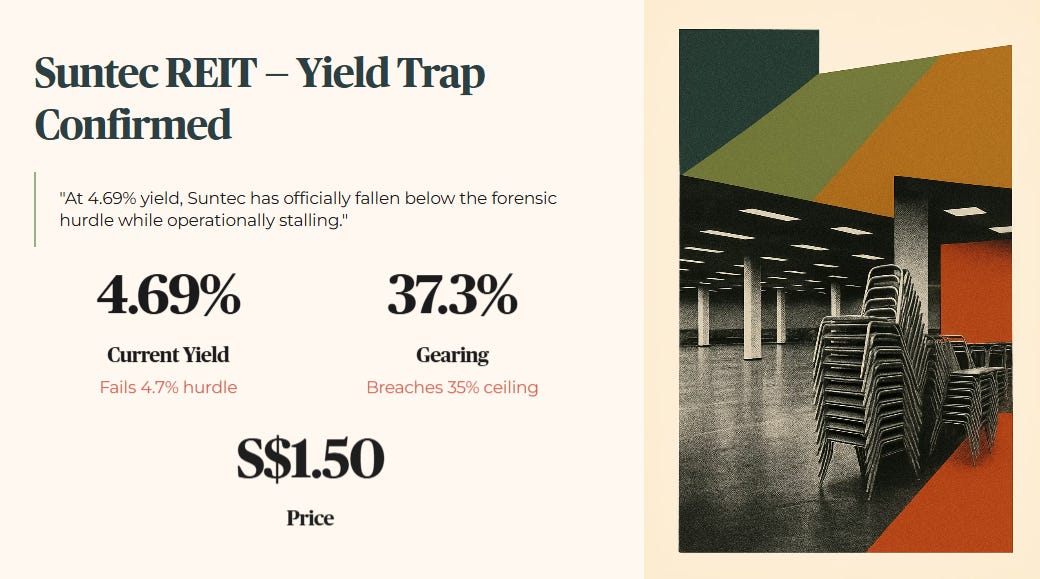

SUNTEC REIT — YIELD TRAP CONFIRMED

“At 4.69% yield, Suntec has officially fallen below the forensic hurdle while operationally stalling.”

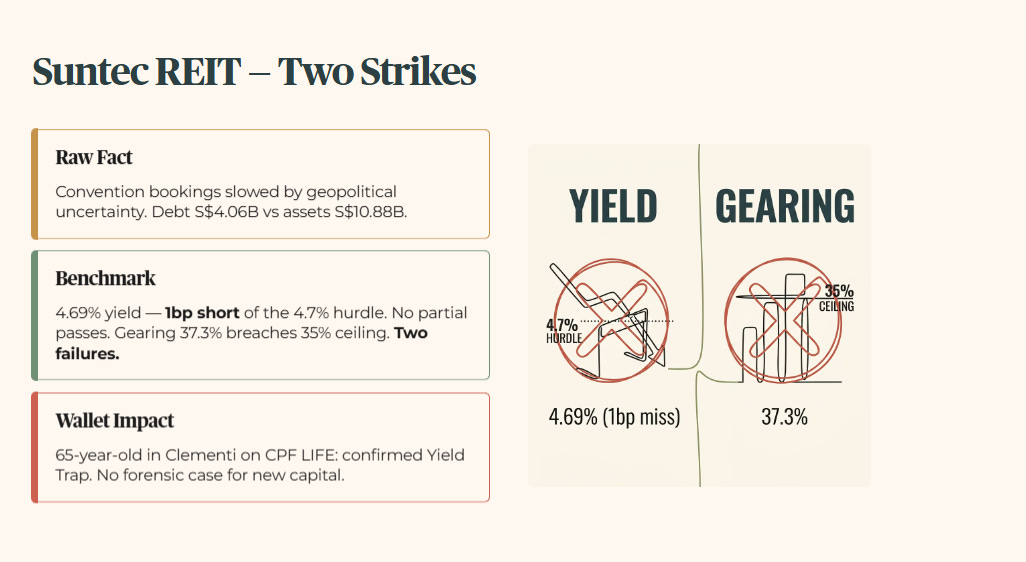

Layer 1 — Raw Fact: Convention business bookings have slowed due to geopolitical uncertainty. Total debt stands at S$4.06 billion against total assets of S$10.88 billion, producing a gearing ratio of 37.3%.

Layer 2 — Benchmark: The 4.69% yield fails the 4.7% forensic hurdle. It is 1 basis point short, but in this framework there are no partial passes. Gearing at 37.3% breaches the 35% ceiling. Two failures against two core screens.

Layer 3 — Peer Context: Mapletree Pan Asia Commercial Trust (N2IU) carries gearing of 36.8%, also above the ceiling. Neither stock offers the balance sheet discipline this environment demands. The CBD commercial and convention segment is carrying leverage without the yield to justify it.

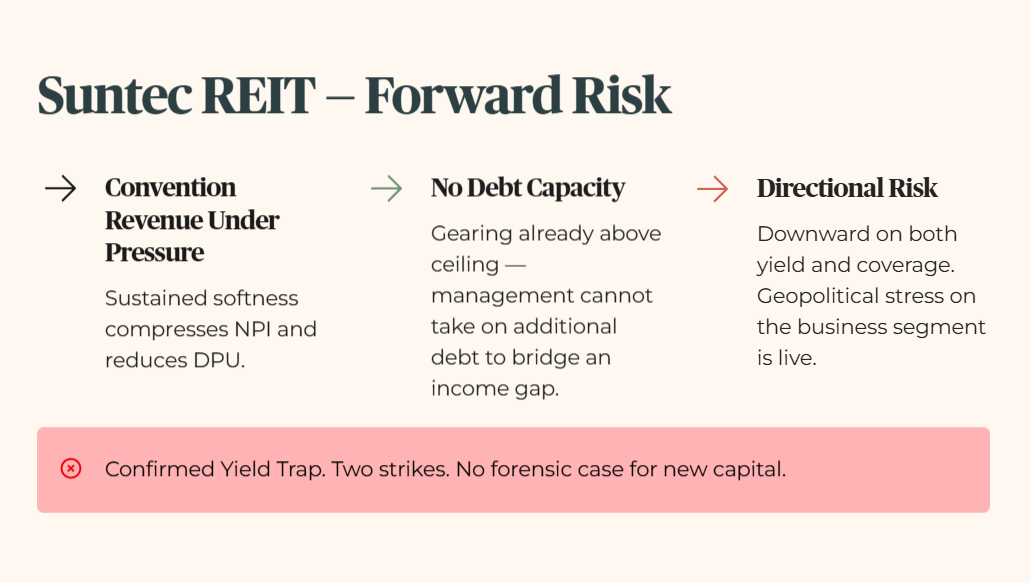

Layer 4 — Forward Scenario: A sustained softness in convention bookings would pressure NPI and reduce DPU. With gearing already above the ceiling, management has limited capacity to take on additional debt to bridge an income gap. The directional risk is downward on both yield and coverage.

Layer 5 — Wallet Impact: For a 65-year-old in Clementi drawing CPF LIFE payouts, this is a confirmed Yield Trap. The income does not clear the hurdle. The balance sheet does not clear the ceiling. The business segment is under geopolitical stress. There is no forensic case for new capital here.

HONG LEONG ASIA (HLA) — YIELD TRAP CONFIRMED

“Expansion via acquisition cannot mask a 1.53% yield that is a total failure for income investors.”

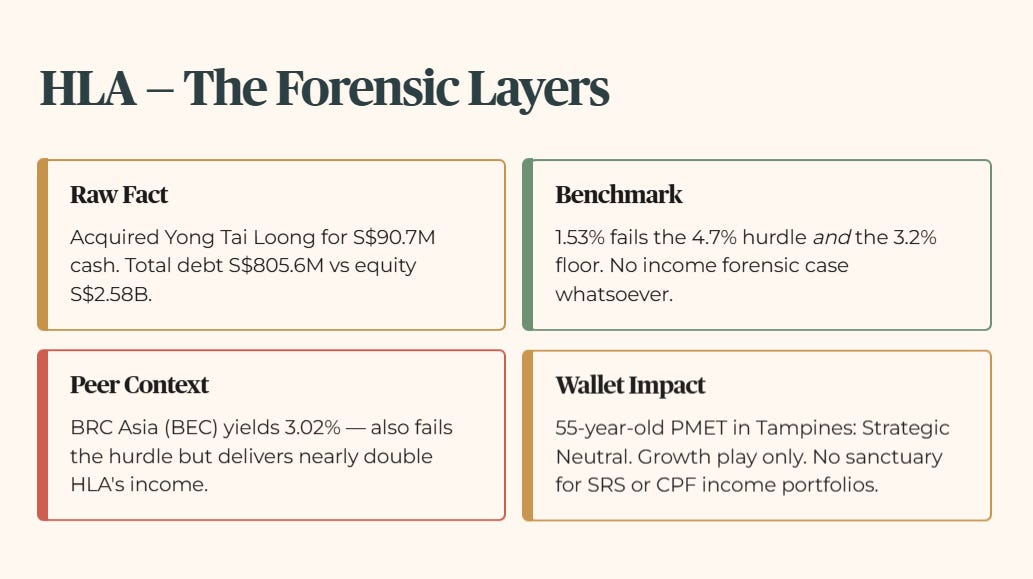

Layer 1 — Raw Fact: HLA acquired architectural building products supplier Yong Tai Loong for S$90.7 million in cash. Debt-to-equity stands at 31.2%, with total debt of S$805.6 million against equity of S$2.58 billion.

Layer 2 — Benchmark: The 1.53% yield is a comprehensive failure against the 4.7% hurdle and the 3.2% floor. There is no income forensic case for a dividend-focused portfolio.

Layer 3 — Peer Context: BRC Asia (BEC) yields 3.02%, which also fails the 4.7% hurdle but delivers nearly double the income of HLA. Neither stock clears the forensic bar for income investors. HLA’s acquisition strategy is a growth narrative, not a yield narrative.

Layer 4 — Forward Scenario: A cash-funded acquisition of S$90.7 million into a business with a 31.2% debt-to-equity ratio is directionally manageable on the balance sheet, but does not resolve the yield gap. Until the acquired operations generate material DPU uplift, the income shortfall is structural.

Layer 5 — Wallet Impact: A 55-year-old PMET in Tampines should view this as a Strategic Neutral. It is a growth play. It offers no sanctuary for a dividend-focused SRS or CPF portfolio. File it and move on.

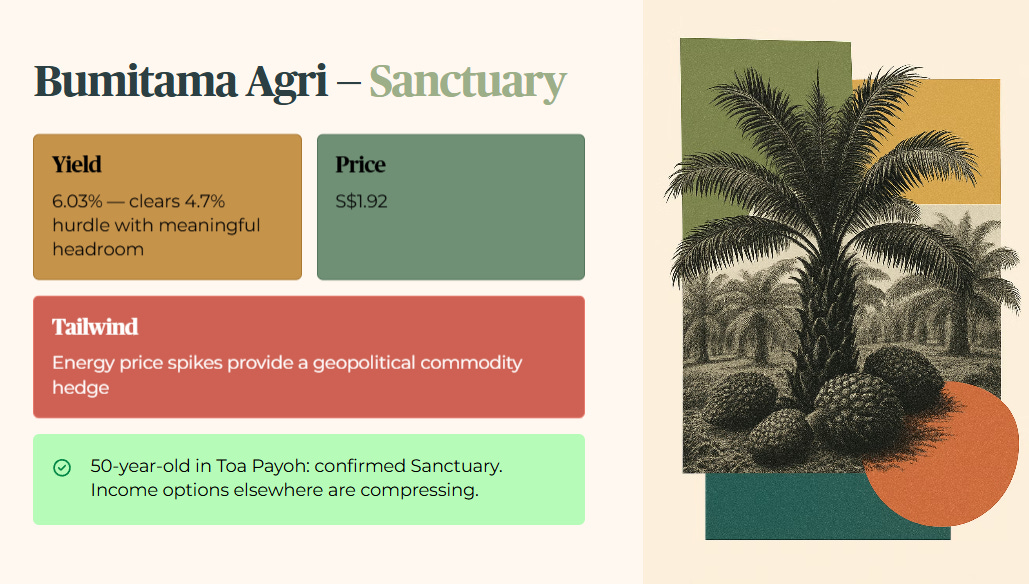

BUMITAMA AGRI — SANCTUARY

Raw Fact: Palm oil producer notes energy price spikes may provide a business tailwind. Price at S$1.92, yield confirmed at 6.03%.

Wallet Impact: A 50-year-old in Toa Payoh should view this as a Sanctuary. The 6.03% yield clears the 4.7% hurdle with meaningful headroom and provides a geopolitical commodity hedge in a market where most income options are compressing.

ANALYST CHATTER

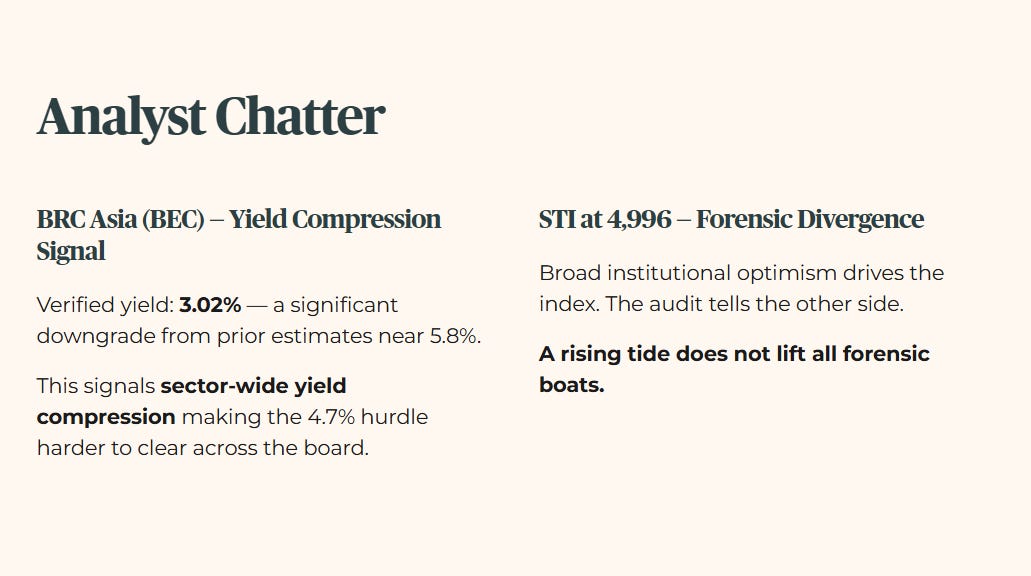

BRC Asia (BEC) — Yield Compression Signal: Verified yield at 3.02%, a significant downgrade from prior estimates near 5.8%. This is not an isolated data point. It signals sector-wide yield compression that makes the 4.7% hurdle harder to clear across the board.

STI at 4,996 — Forensic Divergence: Broad institutional optimism is driving the index. The audit above tells the other side of that story. Suntec fails the hurdle. HLA is forensic noise for income investors. A rising tide does not lift all forensic boats.

WATCHLIST AND YIELD SPREAD

A note on the stress-test buffer: the 3.2% Forensic Floor is applied across this entire audit. With the 6-month T-Bill at 1.46% and SORA running around 1.10%, some investors will argue the floor is too conservative. It is not. The floor exists to ensure that sanctuary assets can withstand a return to long-term average interest rates, not just today’s levels. The minimum yield hurdle remains 4.7%, which is the 3.2% floor plus 150 basis points of mandatory risk premium. That does not move with the index.

The Window Is Already Open

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

🦎 IGGY’S TAKE: THE BOTTOM LINE

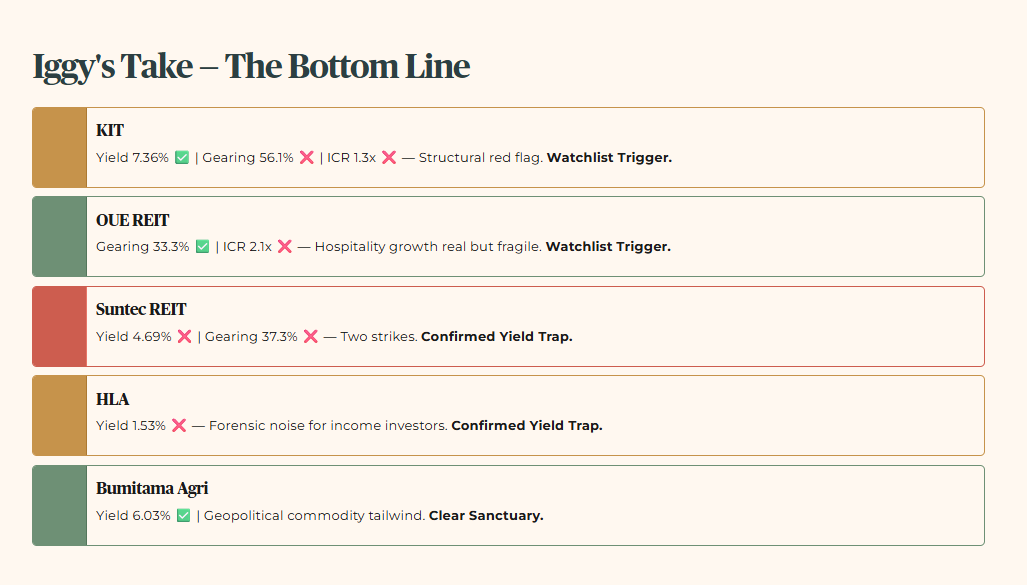

KIT: Yield verified at 7.36%, but gearing at 56.1% and ICR at approximately 1.3x make this a structural red flag. Watchlist Trigger.

OUE REIT: Gearing clears at 33.3%. ICR at approximately 2.1x fails the Fortress screen. Hospitality growth is real but fragile. Watchlist Trigger.

Suntec REIT: Confirmed Yield Trap. Yield fails the hurdle at 4.69%. Gearing breaches the ceiling at 37.3%. Two strikes.

HLA: Confirmed Yield Trap for income investors. The 1.53% yield is forensic noise in a 4.7% hurdle world.

Bumitama Agri: The clear Sanctuary in today’s audit. A 6.03% yield with a geopolitical commodity tailwind.

The divergence between the Bedok retiree still holding Suntec and the Woodlands investor positioned in Bumitama has rarely been wider. The STI at 4,996 is a distraction. The only truth is the yield that actually lands in your pocket.

Iggy’s Forensic Disclaimer

This content is produced for educational and informational purposes only. I am not a financial advisor — I am a retail investor who applies forensic analysis to my own portfolio and shares that process publicly. Nothing here constitutes a recommendation to buy, sell, or hold any security, and no specific target prices or personalised financial advice are offered. Stocks assessed under Iggy’s Forensic Yield Standard are benchmarked against a 4.7% minimum yield hurdle; stocks flagged as Growth Watch fall below this threshold but demonstrate clean balance sheet metrics and an identifiable growth catalyst — these carry a materially different risk profile and are not suitable as yield replacements for income-dependent investors. All data is sourced from public filings and verified sources; where data is unverified it is explicitly flagged. All investments carry risk, including the potential loss of principal, and past performance is not indicative of future results. If you are making investment decisions involving CPF, SRS, or personal capital, please conduct your own due diligence or consult a MAS-licensed financial adviser before committing funds.