STI 4600 Warning: Don't Buy DBS or CLAR Yet

Why chasing the index blindly is a mistake, and where the “Smart Money” is actively rotating for 2026.

The Straits Times Index (STI) has finally done what the skeptics said was impossible—it has shattered the 4,600 ceiling. For investors holding DBS and OCBC, this feels like a victory lap. But for those sitting on cash in their CPF Ordinary Accounts or SRS, a dangerous emotion is creeping in: The fear of missing out.

The question flooding my inbox this week isn’t “what do I buy?” It is “Iggy, is it too late?”

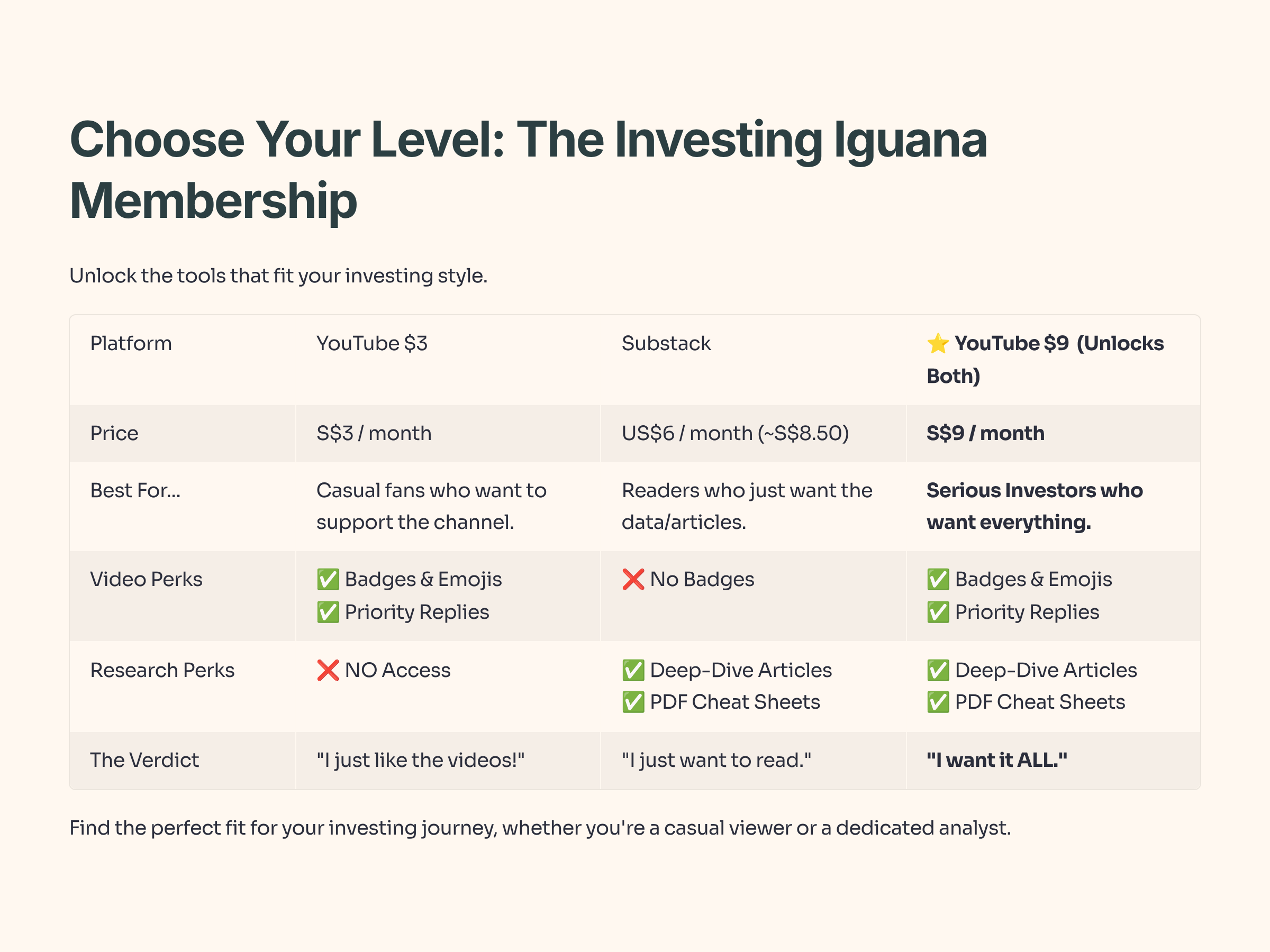

If you’re new here, welcome. I’m Iggy, your Singapore-based market analyst. Since October 2025, we’ve produced over 1,300 videos and 400 articles with 1.1 million watch hours. We are also home to a growing community of over 70 YouTube Premium subscribers and 30 paid Substack members.

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the ‘smart money’ move. Now, let’s get to the numbers.

In This Article:

• The Victory Lap: What Just Happened?

• The Reality Check: Are Banks Too Expensive?

• InvestingPro Reality Check

• The “Dogs of the STI”: Where the Alpha Is Hiding?

• The 2026 Outlook: The Stock Picker’s Market

• Iggy's Verdict / Conclusion

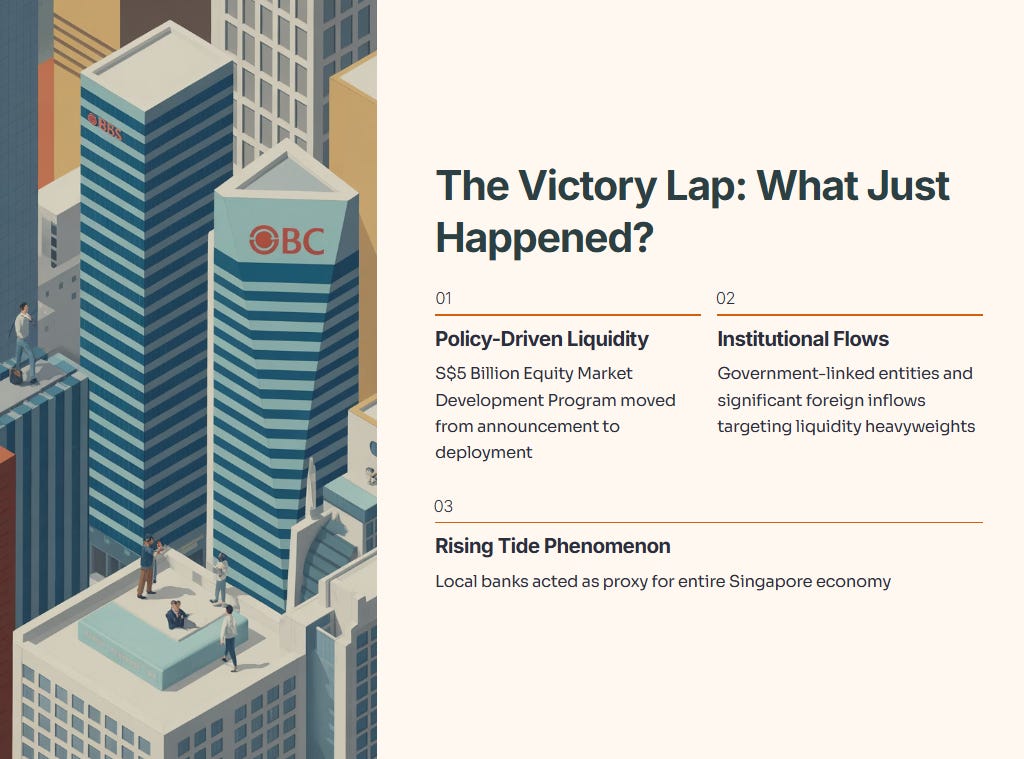

The Victory Lap: What Just Happened?

To understand where we are going in 2026, we have to brutally analyze how we got here. The rally to 4,600 wasn’t accidental, and it wasn’t magic. It was policy-driven liquidity meeting undervalued fundamentals.

Throughout 2024 and early 2025, the narrative was sluggish. But the catalyst we identified back in Q3—the S$5 Billion Equity Market Development Program—has finally moved from “announcement” to “deployment.” We are seeing institutional flows not just from local government-linked entities, but significant foreign inflows targeting the liquidity heavyweights.

The “Rising Tide” phenomenon has been stark. The local banks have effectively acted as a proxy for the entire Singapore economy. If you were holding the trio, your portfolio likely looks incredible right now.

Table 1: The Banking Behemoths (2025 YTD Performance Estimate)

Note: DBS Price updated to reflect recent surge to S$56.23. Yields reflect trailing 12-month distributions adjusted for price appreciation.

However, looking at this table should give you pause, not excitement. The gains have been made. The “easy money”—the gap between value and price—has closed. In fact, for DBS, the gap has inverted.

The mistake retail investors make is looking at this table and thinking, “I should buy the winner.” The smart money looks at this table and asks, “Who hasn’t moved yet?”

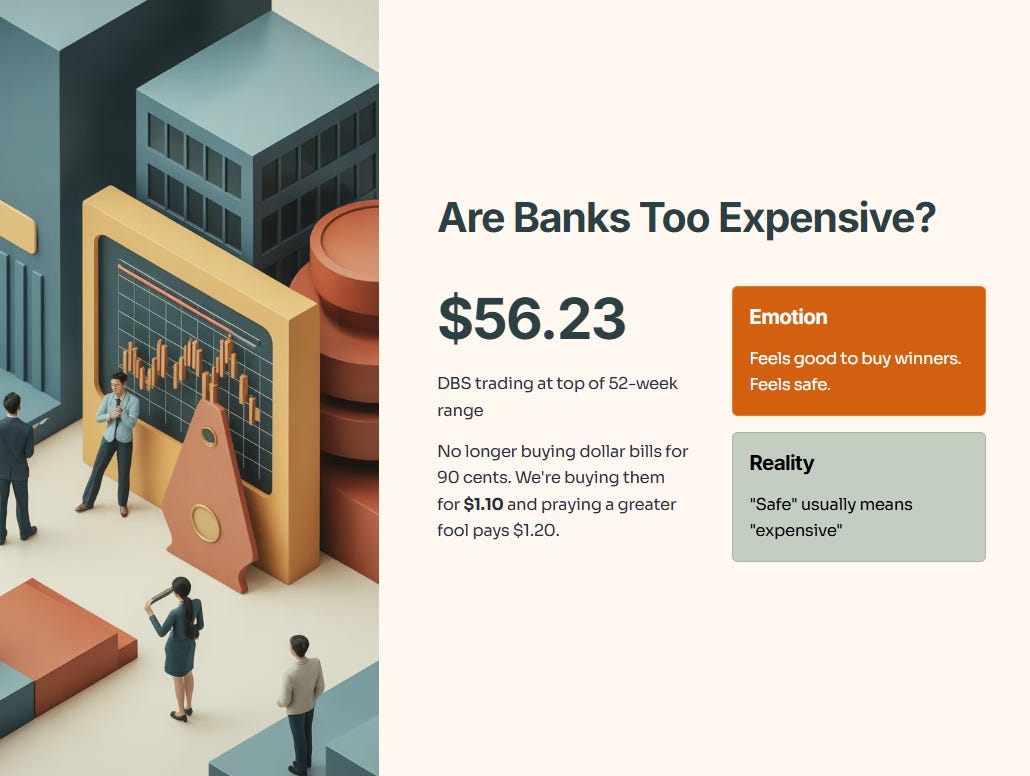

The Reality Check: Are Banks Too Expensive?

This is where we need to separate emotion from valuation. It feels good to buy winners. It feels safe. But in investing, “safe” usually means “expensive.”

At $56.23, DBS is trading at the very top of its 52-week range. We are no longer buying dollar bills for 90 cents. We are buying dollar bills for $1.10 and praying a greater fool comes along to pay $1.20.

Iggy’s Insight: I don’t just guess at valuations. I check the institutional models. And right now, the models are screaming “Caution.”

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

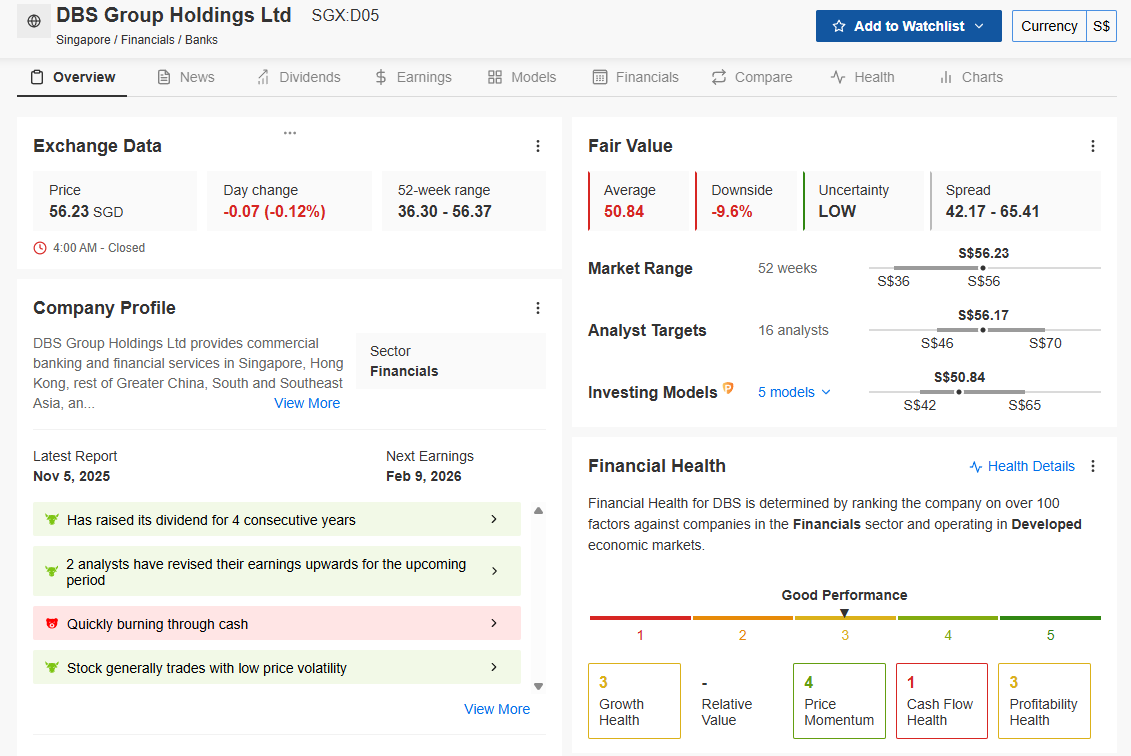

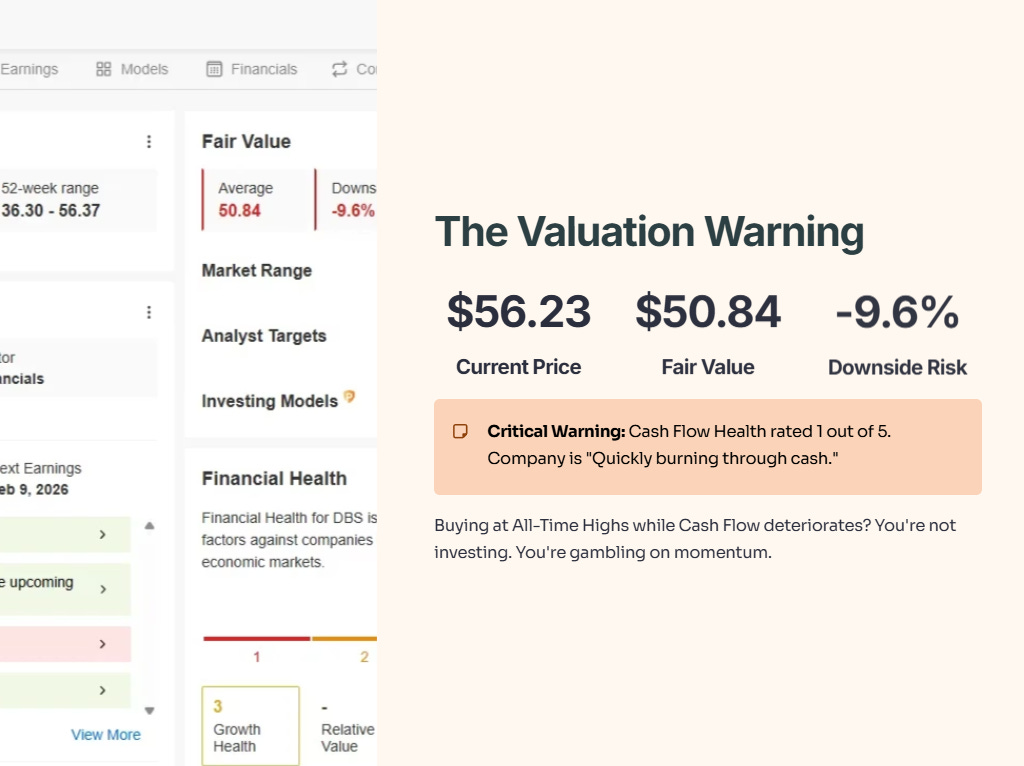

Data Check: Look closely at the screenshot above. The InvestingPro model pegs the Fair Value of DBS at S$50.84.

Current Price: S$56.23

Fair Value: S$50.84

Downside Risk: -9.6%

The model is flashing a clear signal: The price has disconnected from the fundamentals. Even more concerning is the Financial Health check. While Price Momentum is strong (4/5), look at the Cash Flow Health. It is a 1 out of 5. The platform explicitly warns that the company is “Quickly burning through cash.”

If you are buying at All-Time Highs while Cash Flow health is deteriorating, you are not investing. You are gambling on momentum.

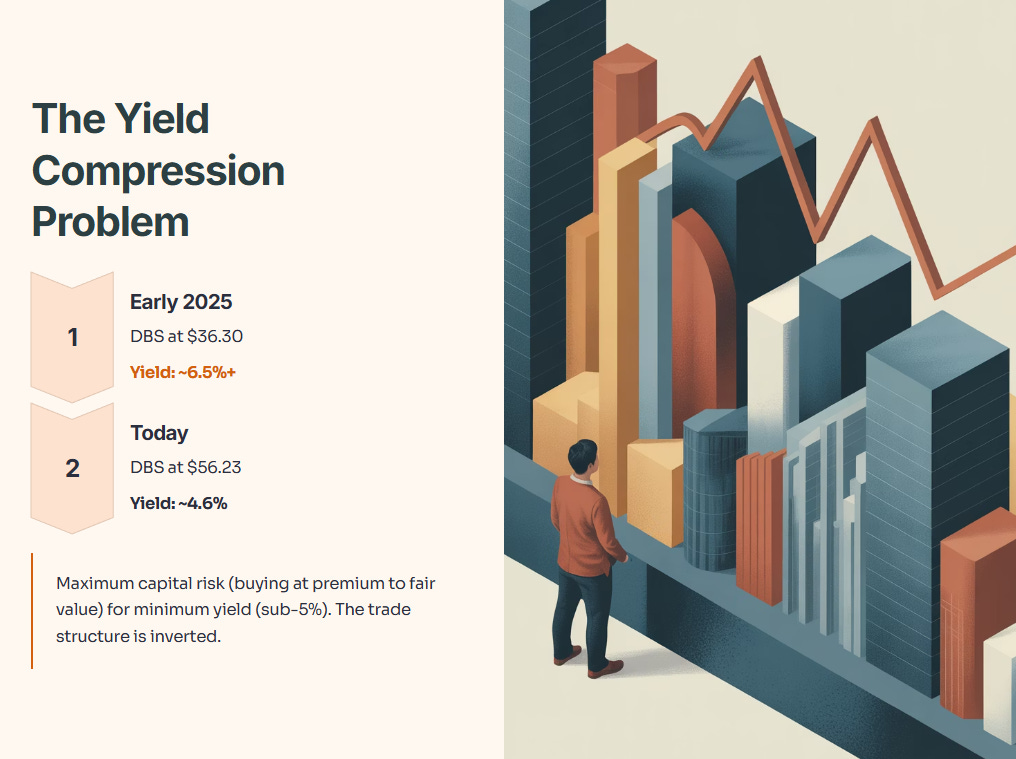

The Yield Compression Problem

For the income-focused investor (which is most of us), the math has broken.

Scenario A (Early 2025): Buying DBS at $36.30 yielded ~6.5%+.

Scenario B (Today): Buying DBS at $56.23 yields ~4.6%.

You are taking on maximum capital risk (buying at a premium to fair value) for minimum yield (sub-5%). In the context of capital preservation, this trade structure is inverted. We want high yield with a safety margin. Currently, the market leader offers neither.

The “Dogs of the STI”: Where the Alpha Is Hiding (Or Is It?)

If the banks are the engine that got us to 4,600, they are likely running hot. The logical move for 2026 is to rotate profits into laggards—what we call the “Dogs of the STI.”

Primarily, the street is screaming at us to buy S-REITs. The narrative is simple: “Rates are falling, so REITs must rise.”

But I don’t trade on narratives. I trade on numbers. And when I pulled up the dashboard for the blue-chip standard, CapitaLand Ascendas REIT (CLAR), I found a warning sign that most YouTubers are ignoring.

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

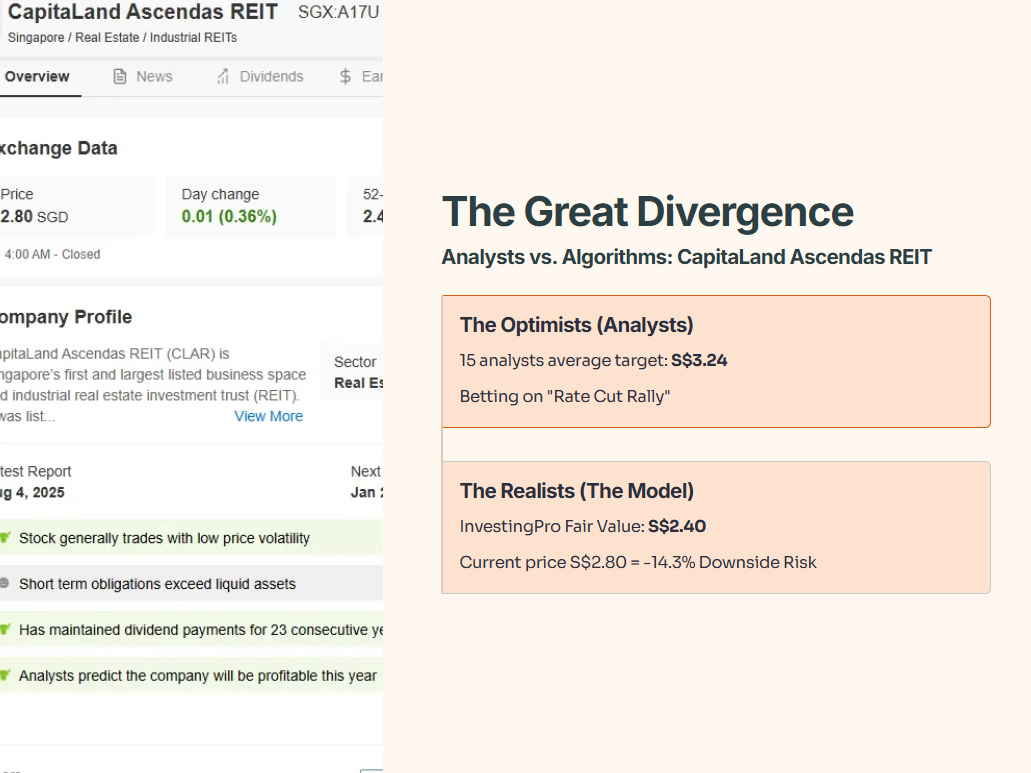

The Great Divergence: Analysts vs. Algorithms

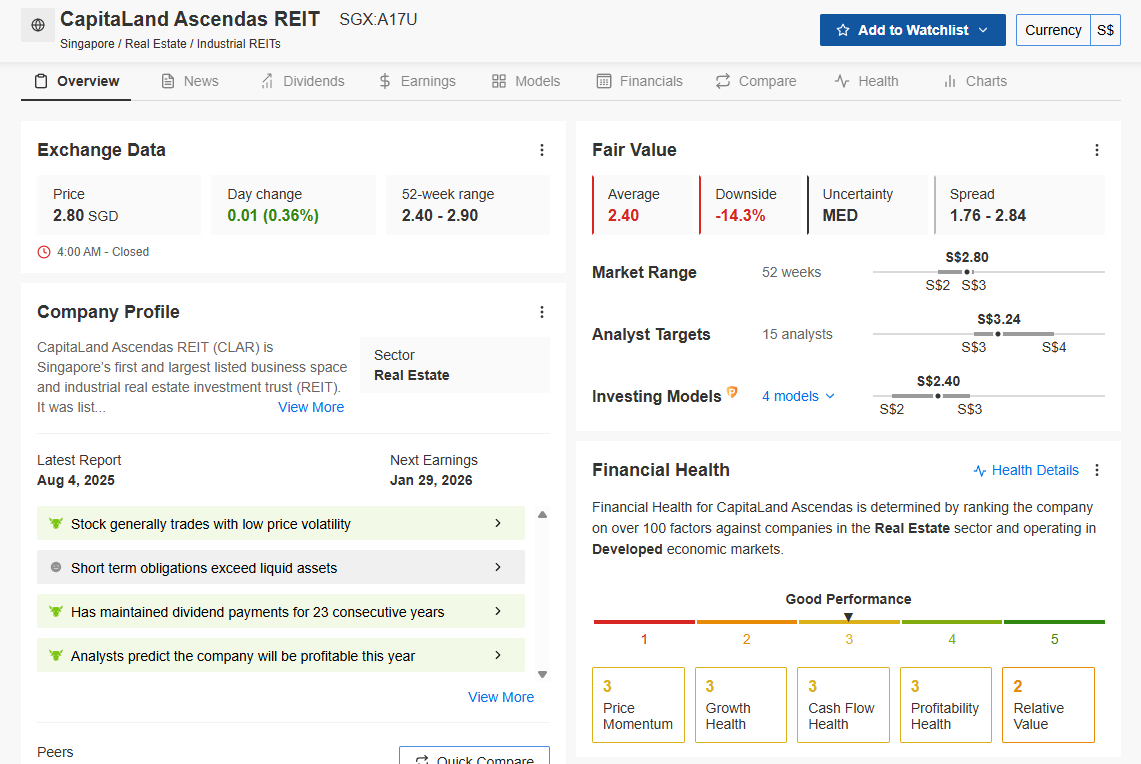

Typically, we expect “Dogs” to be trading at a deep discount to Fair Value. We want a safety margin. But look at what the institutional data is saying about CLAR.

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

Data Check: This is one of the most dangerous charts I have seen this month.

The Optimists (Analysts): The 15 analysts covering the stock have an average target of S$3.24. They are betting on the “Rate Cut Rally.”

The Realists (The Model): The InvestingPro Fair Value model—which looks at cash flow, multiples, and book value—pegs the true value at S$2.40.

At the current price of S$2.80, the model suggests a -14.3% Downside Risk.

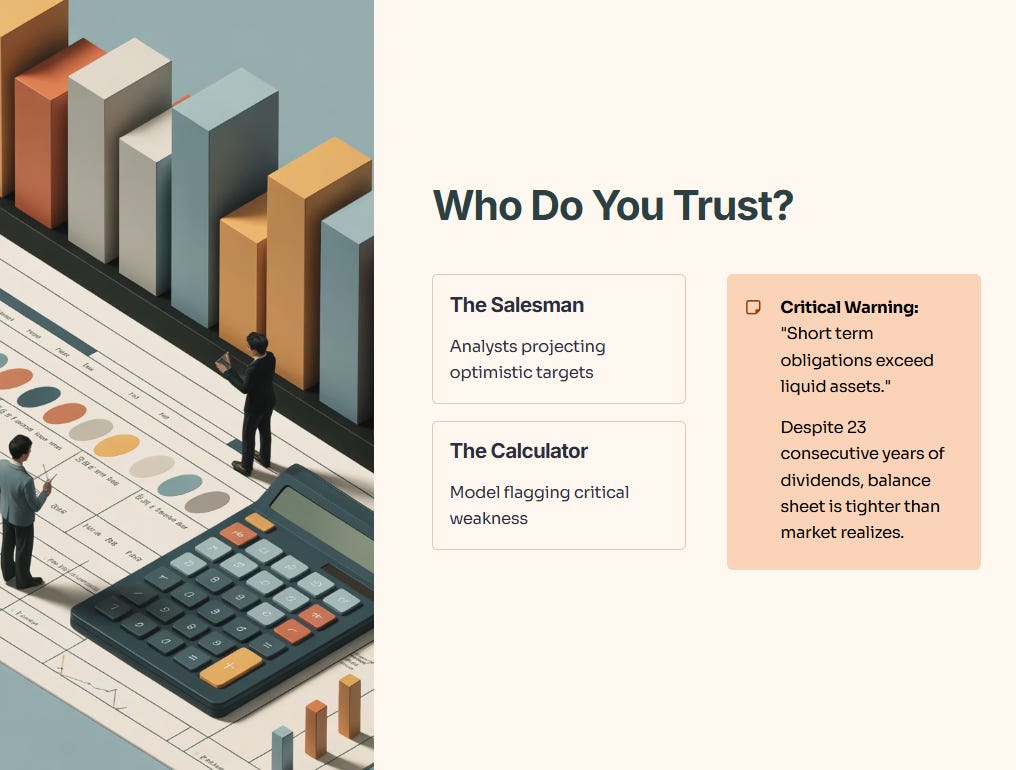

Iggy’s Insight: Who do you trust? The salesman (Analysts) or the calculator (The Model)? The InvestingPro model is flagging a critical weakness: “Short term obligations exceed liquid assets.” While the dividend history is stellar (23 consecutive years), the balance sheet is tighter than the market realizes.

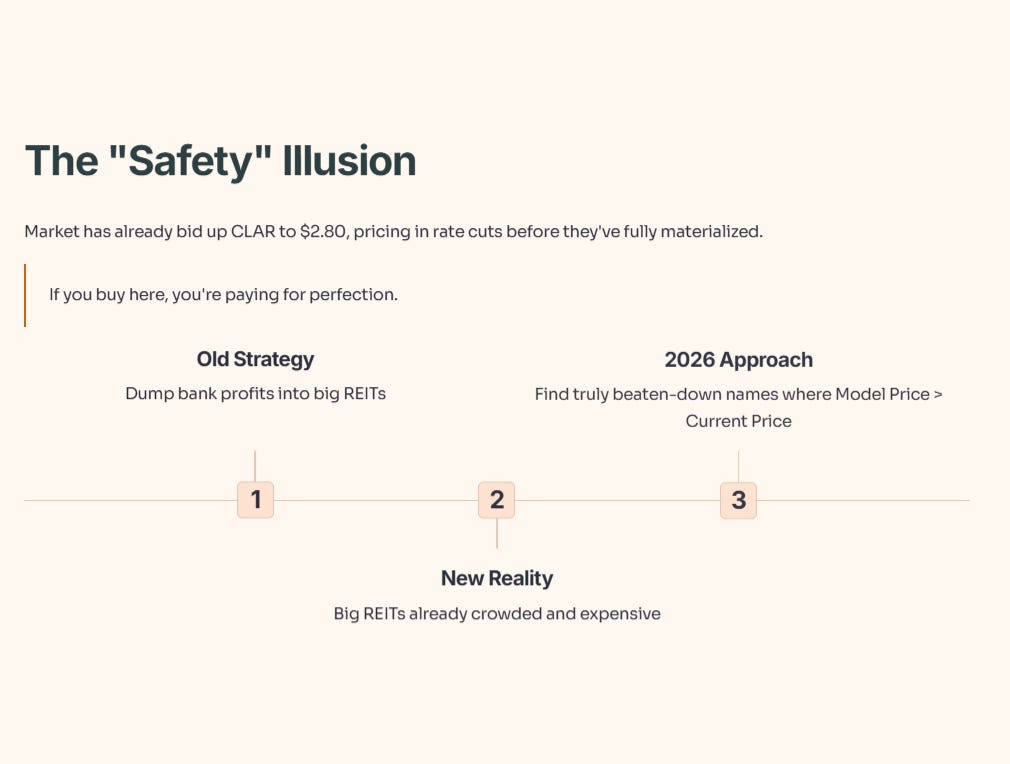

The “Safety” Illusion

This changes our rotation strategy for 2026. We cannot blindly dump bank profits into just any big REIT.

The market has already bid up CLAR to $2.80, effectively pricing in the rate cuts before they have fully materialized. If you buy here, you are paying for perfection.

So, where is the actual value?

We need to look deeper than the “Big Cap” REITs. The rotation shouldn’t be into the crowded REITs, but into the truly beaten-down names where the Model Price is HIGHER than the Current Price.

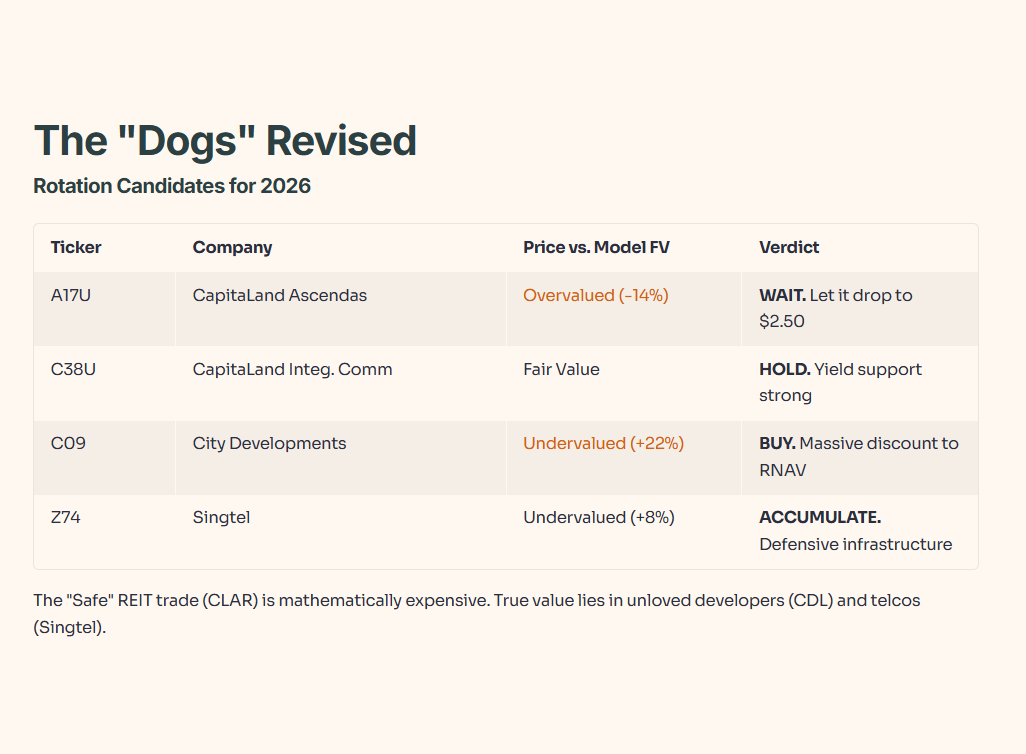

Table 2: The “Dogs” (Revised Rotation Candidates)

The disparity is glaring. The “Safe” REIT trade (CLAR) is actually mathematically expensive right now. The true value lies in the unloved developers (CDL) and telcos (Singtel) which haven’t had their “pre-emptive” rally yet.

The 2026 Outlook: The Stock Picker’s Market