The "Missing Middle": 3 Undervalued SG Stocks ProPicks AI Says "BUY" 🤖

Blue chips are stagnant. Small caps are gambling. Here is where the smart money is quietly rotating for 2025.

You know my philosophy: Boring is beautiful.

While the retail crowd chases the latest US tech rally or gets burned on speculative crypto plays, the Singapore market has been doing something interesting—but only if you look beneath the surface.

The Straits Times Index (STI) often feels like a stagnant pond. You have your three local banks (DBS, UOB, OCBC), a handful of REITs, and... well, that’s about it. But if you’ve been frustrated by the lack of growth in the giants, you’ve been looking in the wrong place.

The real action is happening in the “Missing Middle”—Mid-Cap stocks (market cap S$500M - S$2B). These companies are large enough to have real cash flow and dividends, but small enough that a single contract win or sector rotation actually moves the needle on their share price.

Iggy’s Insight:

The “Blue Chip Trap” is real. Many investors hold SingTel or CapitaLand purely out of nostalgia or safety. But safety doesn’t mean growth. In 2025, capital preservation isn’t enough; you need capital efficiency. Mid-caps are currently offering that sweet spot: institutional stability with actual earnings momentum.The Data: Who Is Actually Moving?

Table of Contents

• The Data: Who Is Actually Moving?

• Deep Dive: The Industrial & Construction Play

• The Income Hunt: Yield Traps vs. Real Deals

• The Iggy Playbook: How to Position for 2025

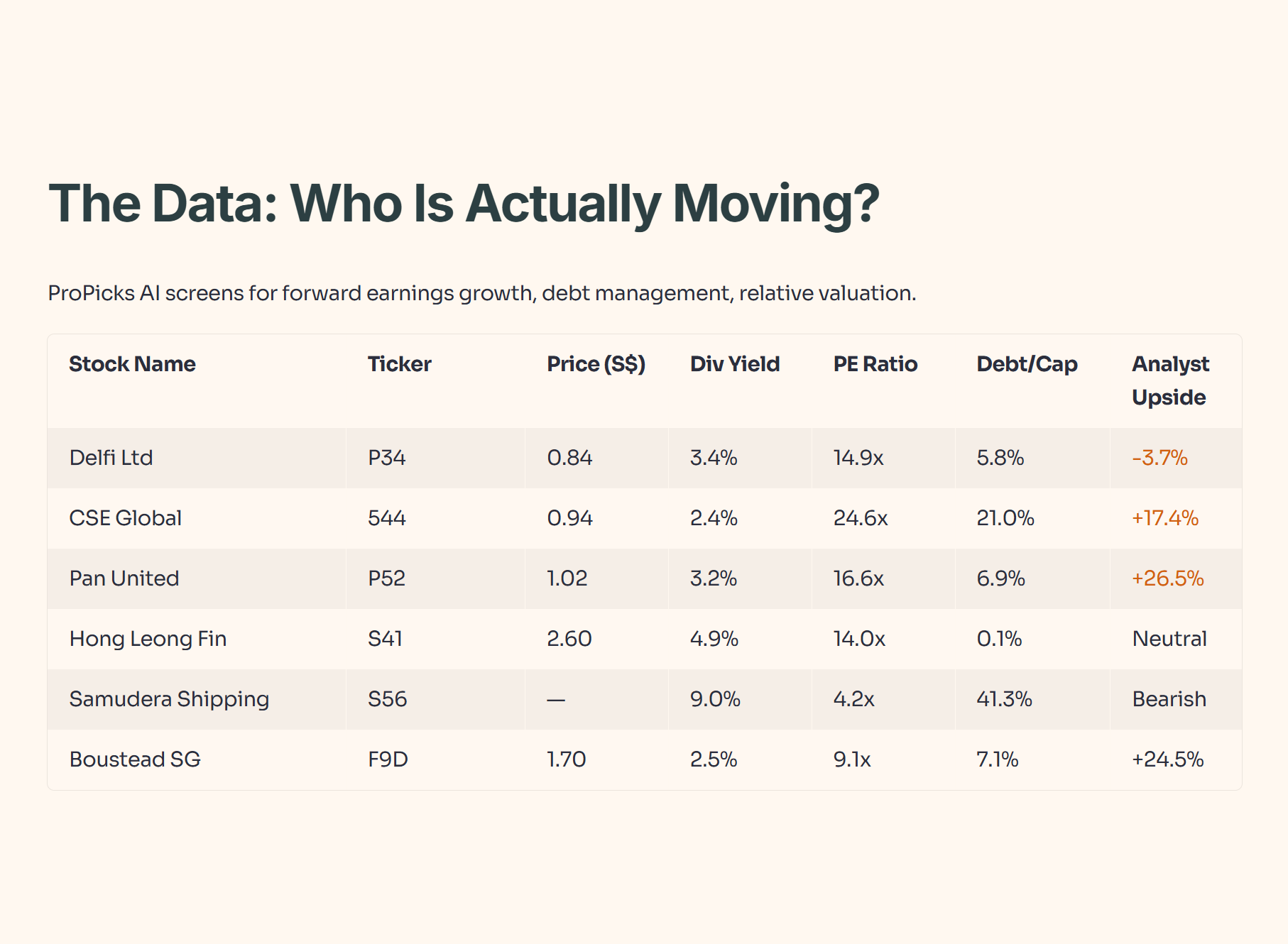

• Closing Thoughts: The Price of “Gut Feeling”The Data: Who Is Actually Moving?

ProPicks AI—an institutional-grade model from InvestingPro by Investing.com I use to filter noise—has flagged a specific list of Singapore mid-caps that are exhibiting strong fundamentals. These aren’t just random picks; they are screened for forward earnings growth, debt management, and relative valuation.

Let’s look at the raw numbers for the top movers this month.

Deep Dive: The Industrial & Construction Play

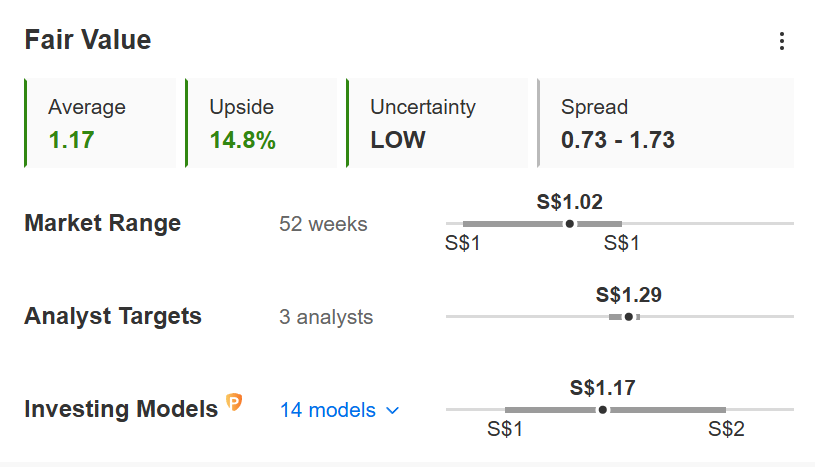

Pan United (P52) standing out with a 26.5% analyst upside is not an accident.

The Context: Singapore’s construction sector is in a multi-year upcycle (HDB ramp-up, Changi T5, infrastructure renewal). Pan United is the largest concrete and cement provider.

The Second-Order Effect: When construction volume goes up, raw material providers win first. Unlike the developers who take on the risk of selling the units, Pan United gets paid as long as the concrete pours.

But is the market getting ahead of itself? I don’t like to guess at valuations. I check the institutional models to see if there’s any meat left on the bone.

Iggy’s Data Check:

Source: InvestingPro (Data as of Dec 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

The Verdict: The InvestingPro “Fair Value” model—which averages 12 different financial models like DCF and Dividend Discount—confirms the analysts’ optimism. It shows Pan United is trading roughly 20% below its intrinsic value. When both the human analysts and the AI models agree on double-digit upside, that’s a “Fat Pitch” setup I like to swing at.

Source: InvestingPro (Data as of Dec 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

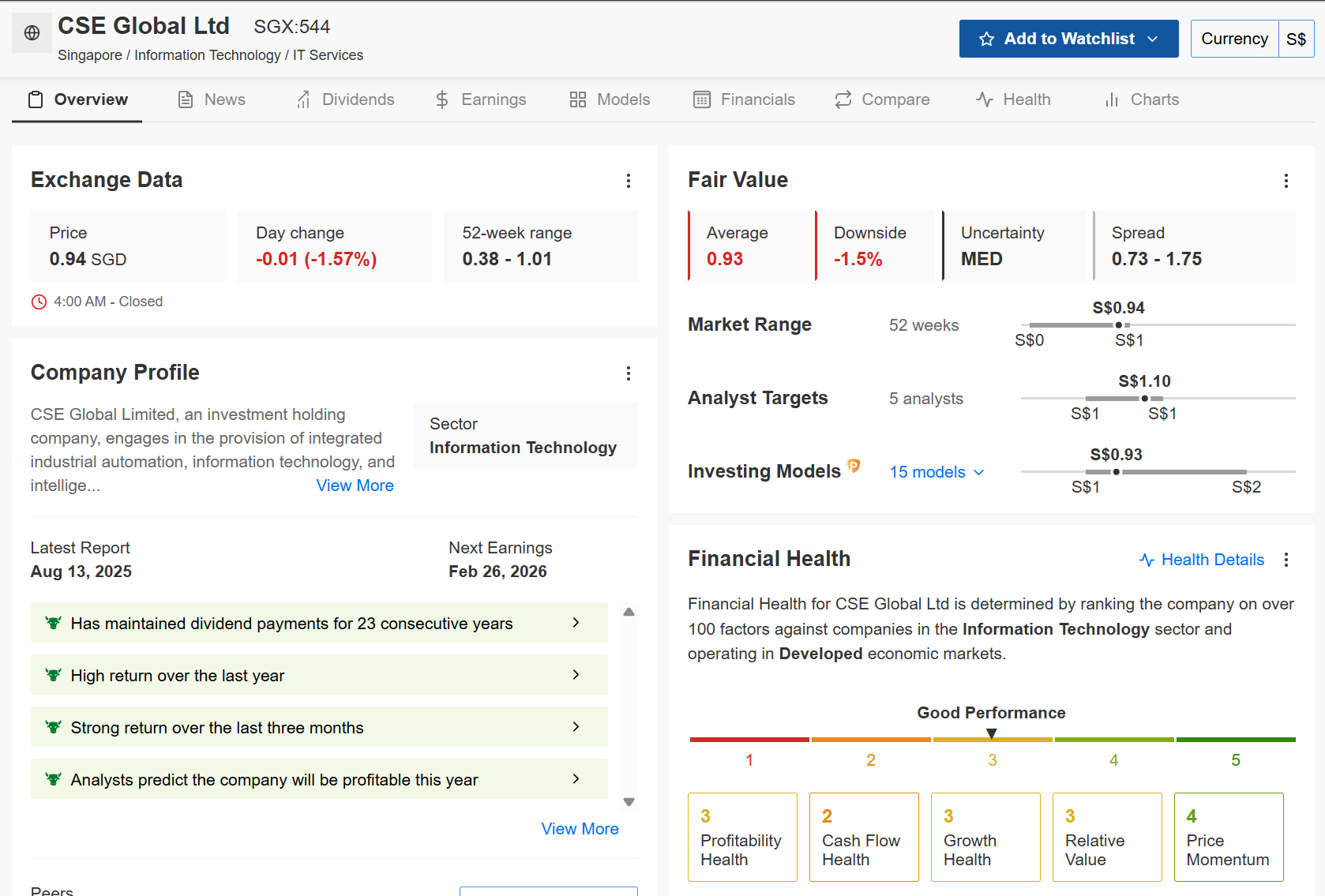

CSE Global (544), on the other hand, is trading at a PE of 24.6x.

The ProTip Warning: InvestingPro’s “ProTips” feature flags this immediately: “Trading at a high earnings multiple relative to near-term growth.”

Iggy’s Take: The market is pricing in perfection here. If they miss one earnings beat, that multiple will contract fast. I prefer Boustead (F9D) at 9.1x PE—it’s the classic “value investing” play where you get real estate and energy engineering assets for a single-digit multiple.

The Income Hunt: Yield Traps vs. Real Deals

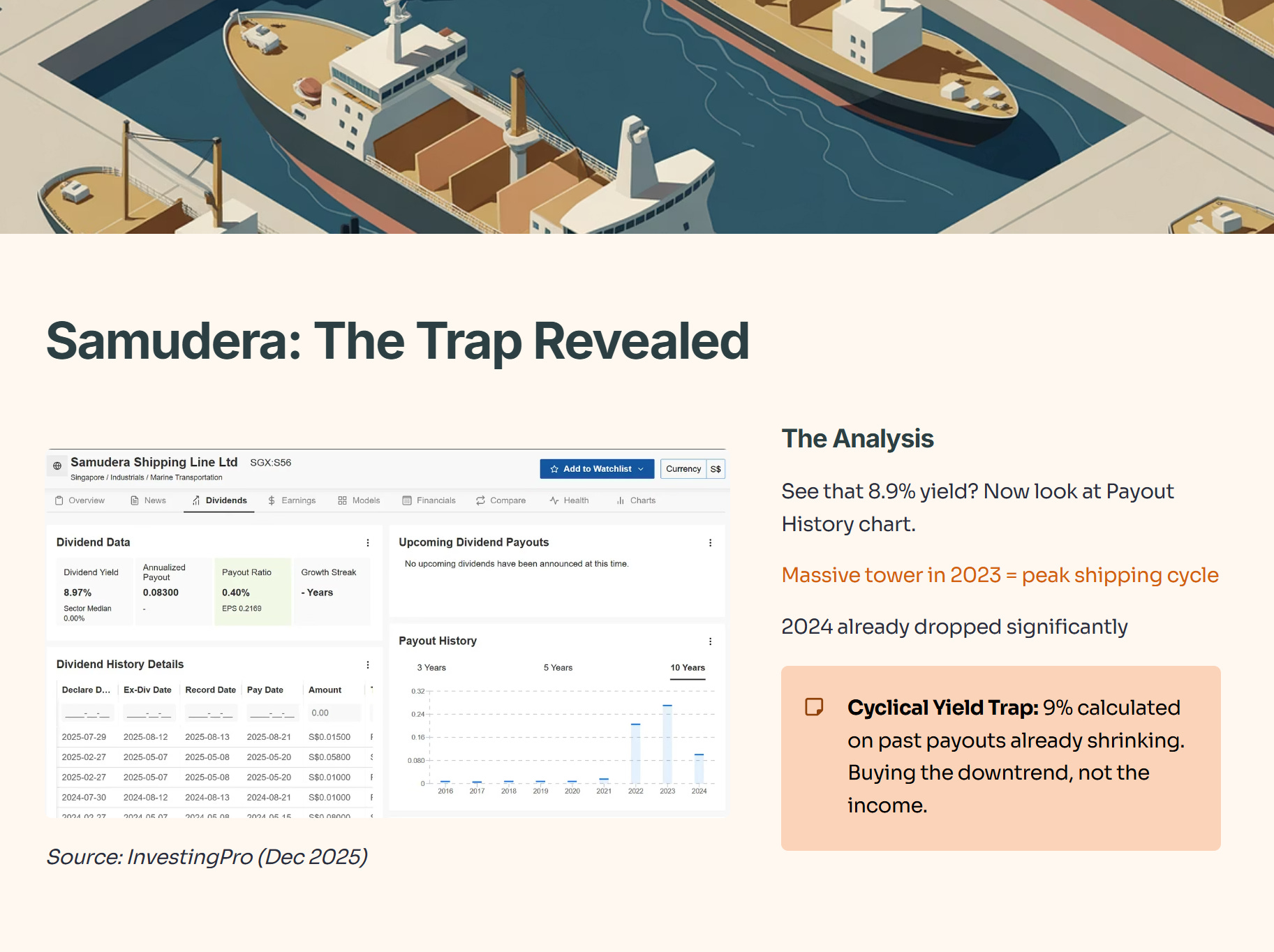

Singaporeans love dividends. It’s in our DNA. But looking at the table, we see a massive disparity: Samudera Shipping (S56) at 9.0% yield vs. Hong Leong Finance (S41) at 4.9%.

The Trap: Samudera’s 9% looks juicy, but that figure is likely based on trailing 12-month payouts during a shipping boom. Is it safe? Let’s look at the Financial Health Score.

Iggy’s Data Check:

Source: InvestingPro (Data as of Dec 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

The Analysis: You see that 8.9% yield and think it’s a bargain. But look at the “Payout History” chart on the right.

Do you see that massive tower in 2023? That was the peak of the shipping cycle. Now look at 2024—it’s already dropped significantly.

The Verdict: That 9% yield is looking in the rear-view mirror. It’s calculated based on past payouts that are already shrinking. This is the definition of a “Cyclical Yield Trap.” You are buying the downtrend, not the income.

The Real Deal: Hong Leong Finance. 4.9% yield is lower, but look at the Debt/Capital ratio: 0.1%. It is effectively debt-free. In a “higher-for-longer” interest rate environment, a finance company with zero debt leverage is a fortress.

Iggy’s Data Check:

Source: InvestingPro (Data as of Dec 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

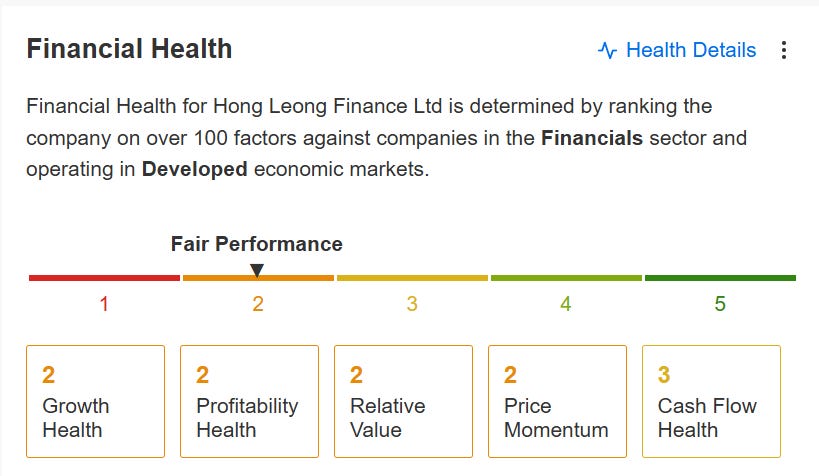

The Verdict: This is why I never trade on “gut feeling” alone.

I saw the 0.1% debt and assumed this was a fortress. But the InvestingPro models rate it a 2/5 (Fair Performance).

What the data found: While the balance sheet is safe, the Growth Health and Profitability Health are both scoring a weak 2. This tells me the company is struggling to expand margins or revenue meaningfully. It’s not going bankrupt, but it might be “dead money”—a stock that goes sideways for years. The 4.9% dividend is likely safe (Cash Flow is decent at 3), but don’t expect capital appreciation here.

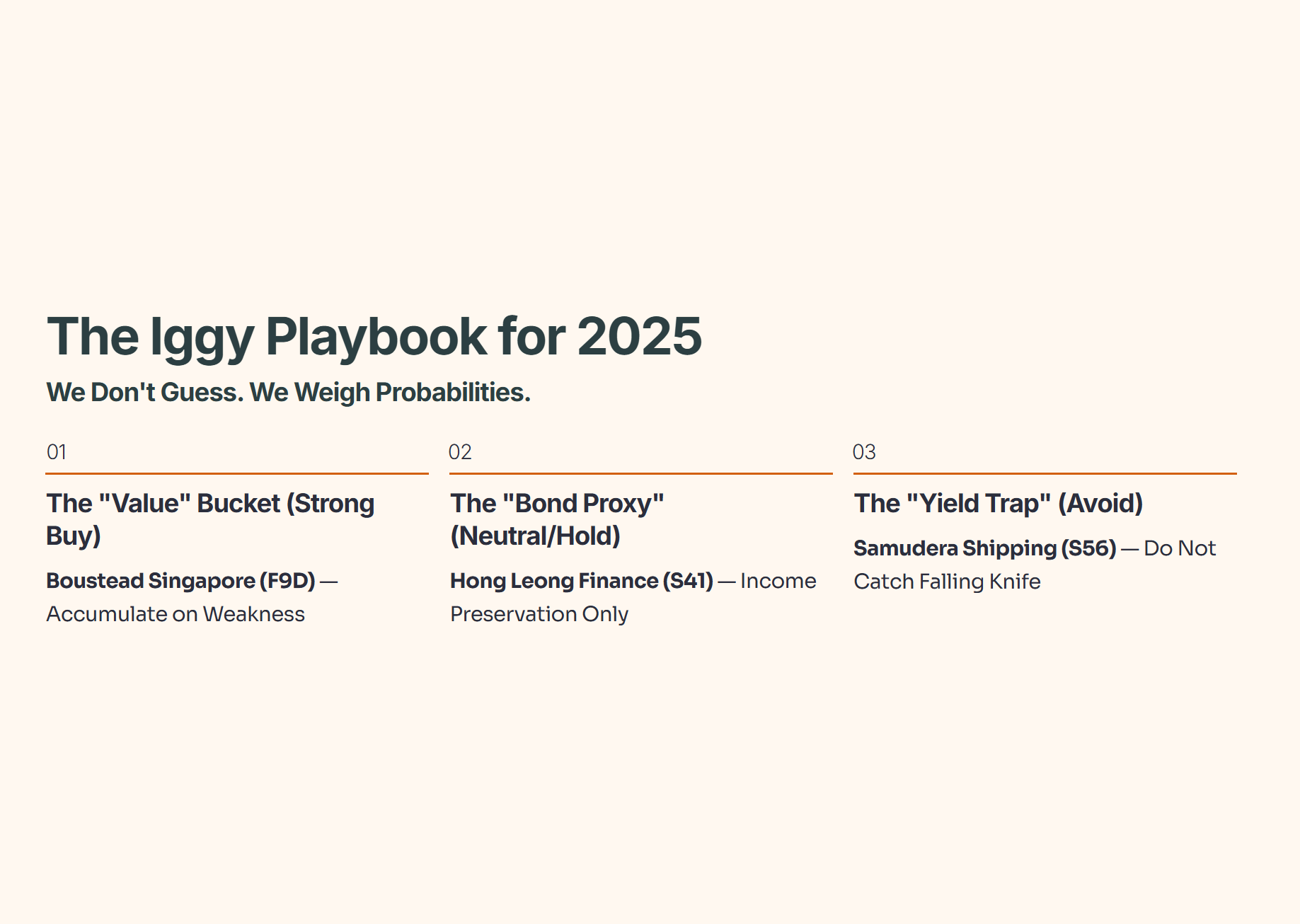

The Iggy Playbook: How to Position for 2025

We don’t guess. We weigh the probabilities. Based on the data we’ve uncovered today, here is how I am structuring my mid-cap watchlist.