Why I Am Accumulating BYD with SRS (3 Good, 3 Red Flags)

While the market panics over trade wars, the “Toyota of EVs” is trading at a crisis-level discount. Here is the math.

1. The Hook & The Housekeeping

The headlines are screaming about trade wars. The EU is slapping tariffs on Chinese imports, and the US market is effectively a walled garden. As a result, BYD—the undeniable global leader in electric vehicles—has seen its Singapore Depository Receipt (SDR) price languish near S$1.58.

Most investors see a falling knife. I see a mispriced asset caused by geopolitical noise and a misunderstood corporate action. Today, we are going to disassemble the numbers to see if this is a value trap or the buying opportunity of 2026.

Who is this for?

If you’re new here, welcome. I’m Iggy, your Singapore-based Private Investor and Market Researcher. Since October 2025, we’ve built a community of over 5,300 investors and produced over 1,300 videos and 400 articles. We are home to a growing ‘Inner Circle’ of over 100 paid members across YouTube and Substack.

Quick Housekeeping:

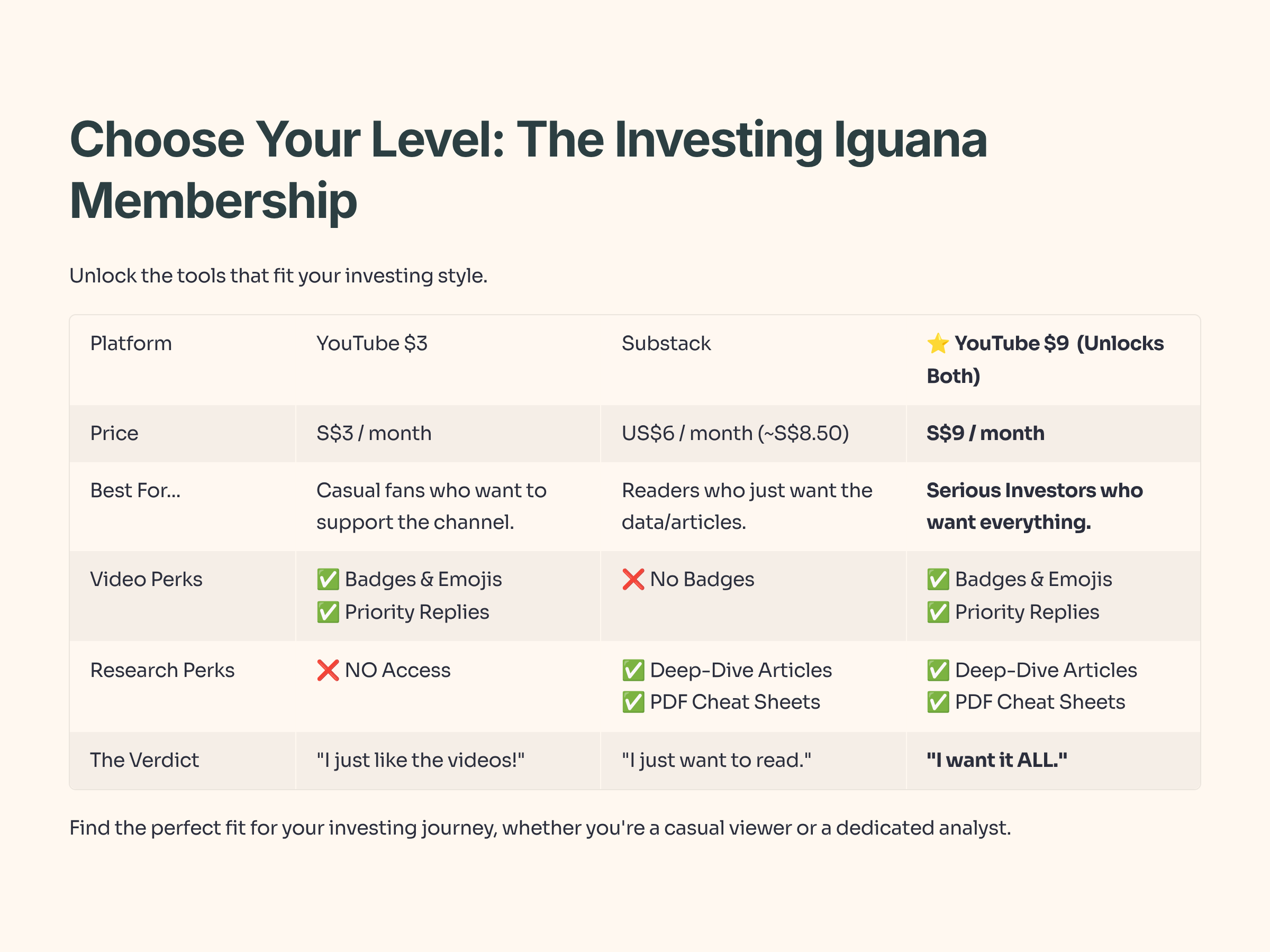

If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the “smart money” move. Now, let’s get to the numbers.

In This Article:

• The Financial Snapshot (The Hard Numbers)

• The “Data Check”: Valuation Reality

• The “3 Good” (The Bull Case)

• The “3 Red Flags” (The Bear Case)

• The Singaporean Context: How to Play This?

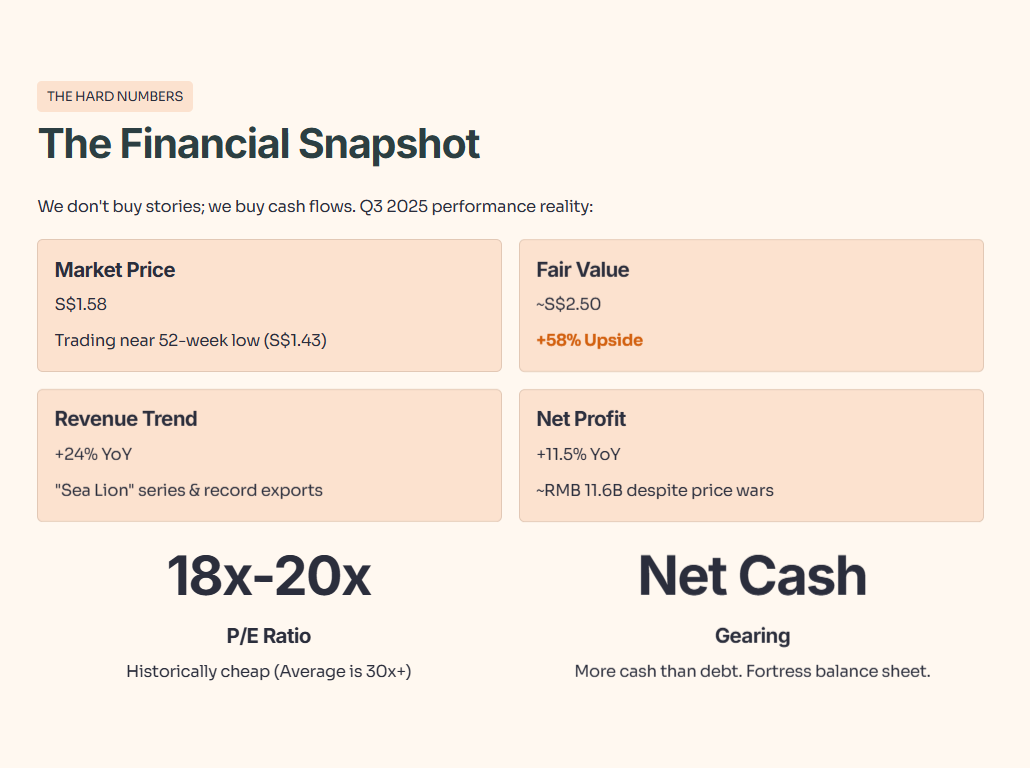

• The Actionable Conclusion (The Investor’s Playbook)2. The Financial Snapshot (The Hard Numbers)

We don’t buy stories; we buy cash flows. Let’s look at the reality of BYD’s Q3 2025 performance, stripping away the news cycle hype.

Iggy’s Insight:

The market is pricing BYD as if it’s a distressed auto-maker. It is not. It is a technology company with a “Net Cash” position. In a high-interest rate environment (even as rates cool slightly), companies that fund their own growth without needing to beg banks for money are the ones that survive. BYD funding its own operations is a massive “Quality” signal that the algorithm is missing.

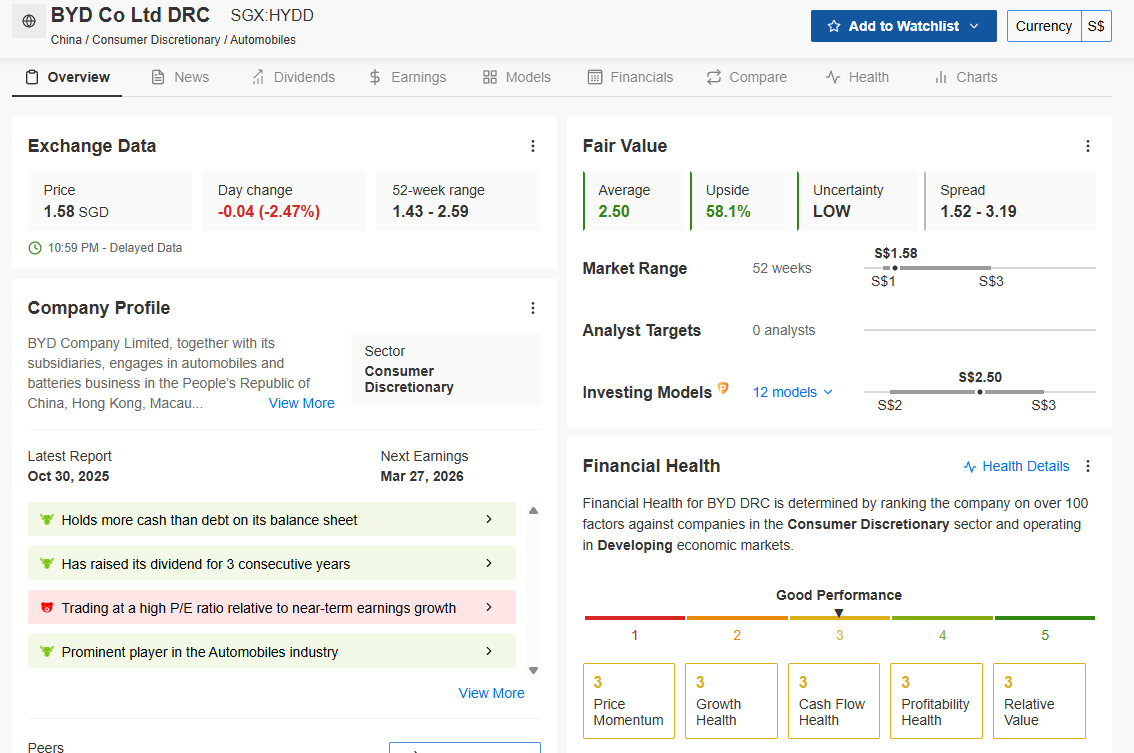

The “Data Check”: Valuation Reality

I don’t just guess at valuations. I check the institutional models to see if my napkin math aligns with the pros.

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

Iggy’s Take:

The InvestingPro models confirm a distinct divergence. While price action (Technical) is weak, the Financial Health Score remains in the “Great” territory. The Fair Value model suggests the stock should be trading closer to S$2.50. We are effectively buying a dollar for 63 cents right now.

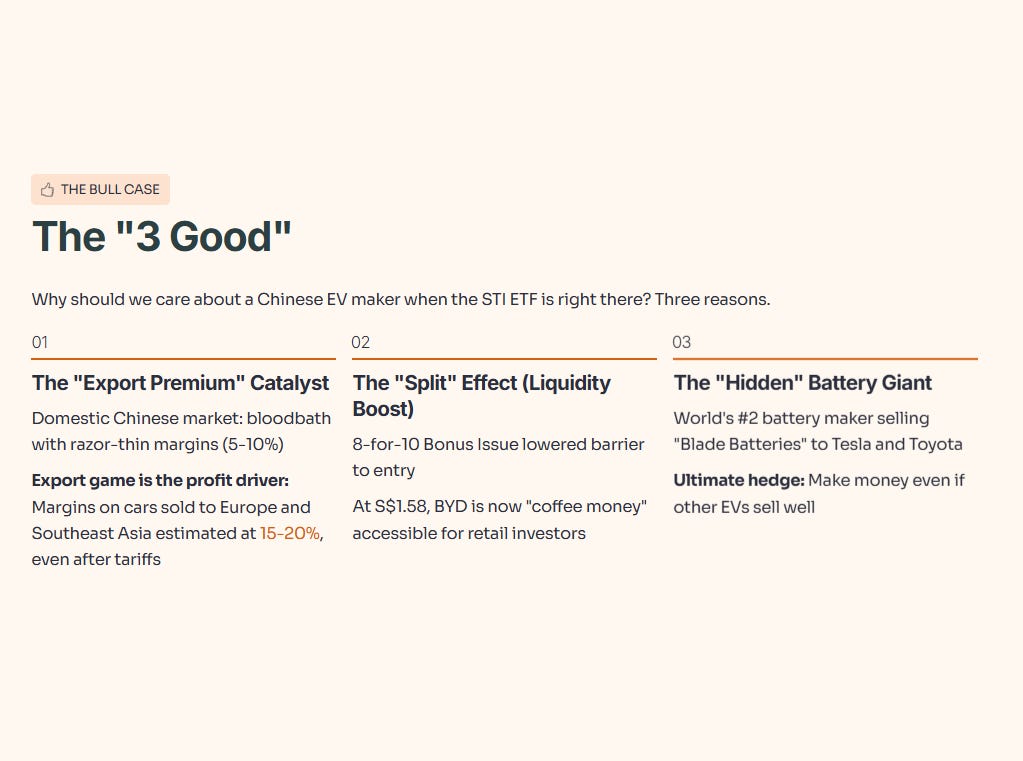

3. The “3 Good” (The Bull Case)

Why should we care about a Chinese EV maker when the STI ETF is right there? Three reasons.

1. The “Export Premium” Catalyst

The domestic Chinese market is a bloodbath with razor-thin margins (~5-10%). However, BYD’s export game is the profit driver. Margins on cars sold to Europe and Southeast Asia are estimated at 15-20%, even after accounting for tariffs.

The Evidence: Export volumes surged 32% YoY in 2024/25.

The Pivot: By localizing production in Hungary and Turkey, BYD is bypassing the worst of the EU tariffs. They aren’t just shipping cars; they are shipping factories.

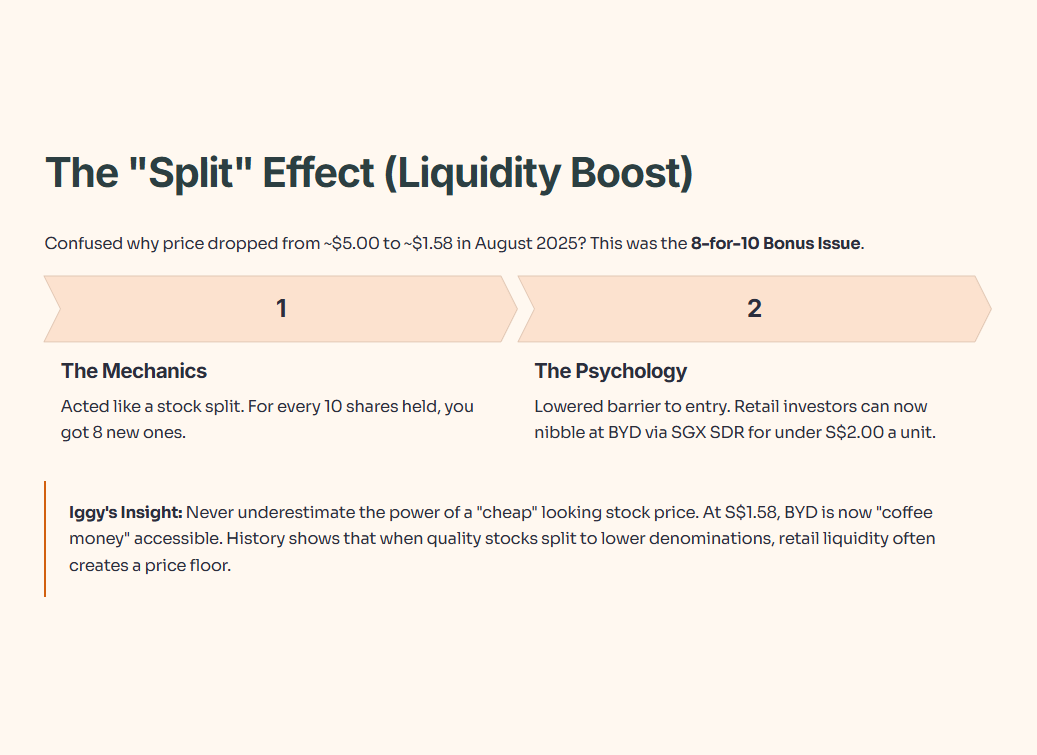

2. The “Split” Effect (Liquidity Boost)

If you were confused why the price dropped from ~$5.00 to ~$1.58 in August 2025, you aren’t alone. This was the 8-for-10 Bonus Issue.

The Mechanics: This acted like a stock split. For every 10 shares you held, you got 8 new ones.

The Psychology: This lowered the barrier to entry. Retail investors who found the HK “board lot” too expensive can now nibble at BYD via the SGX SDR for under S$2.00 a unit.

Iggy’s Insight:

Never underestimate the power of a “cheap” looking stock price. Institutional investors look at market cap, but retail investors look at unit price. At S$1.58, BYD is now “coffee money” accessible. History shows that when quality stocks split to lower denominations, retail liquidity often creates a price floor.

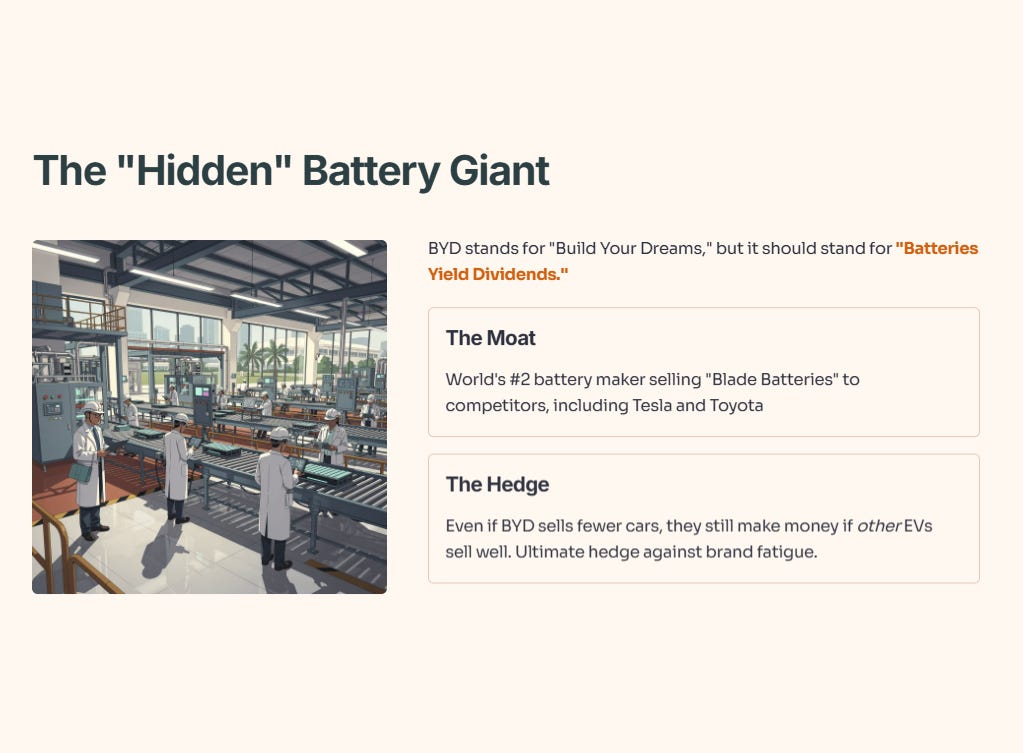

3. The “Hidden” Battery Giant

BYD stands for “Build Your Dreams,” but it should stand for “Batteries Yield Dividends.” They are the world’s #2 battery maker.

The Moat: They sell their “Blade Batteries” to competitors, including Tesla and Toyota.

The Hedge: Even if BYD sells fewer cars, they still make money if other EVs sell well. This is the ultimate hedge against brand fatigue.

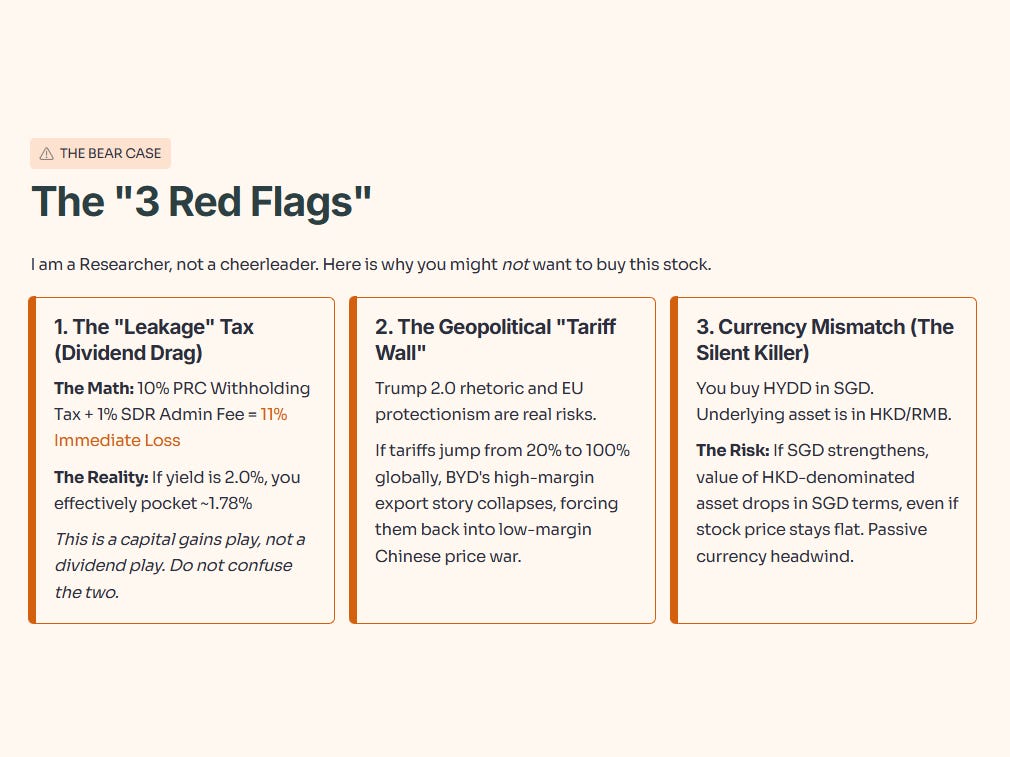

4. The “3 Red Flags” (The Bear Case)

I am a Researcher, not a cheerleader. Here is why you might not want to buy this stock.

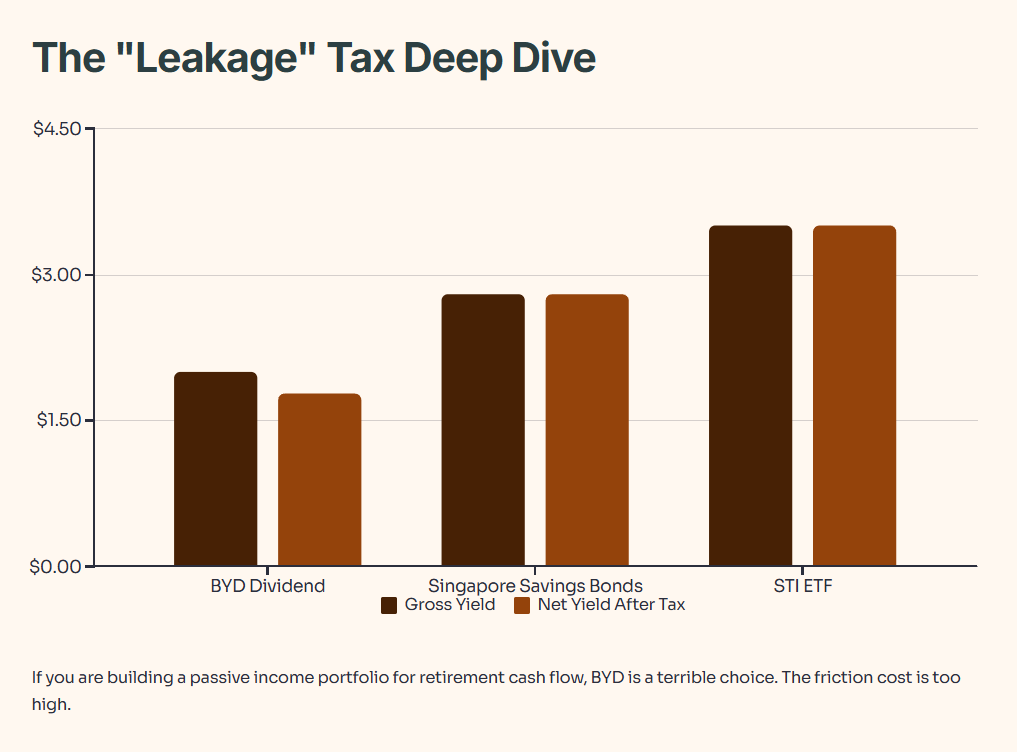

1. The “Leakage” Tax (Dividend Drag)

This is the deal-breaker for many Singaporean income investors. BYD pays dividends, but the journey to your bank account is leaky.

The Math: 10% PRC Withholding Tax + 1% SDR Admin Fee = 11% Immediate Loss.

The Reality: If the yield is 2.0%, you effectively pocket ~1.78%.

Iggy’s Insight:

If you are building a passive income portfolio for retirement cash flow (i.e., money to buy chicken rice today), BYD is a terrible choice. The friction cost is too high. This is a capital gains play, not a dividend play. Do not confuse the two.

2. The Geopolitical “Tariff Wall”

Trump 2.0 rhetoric and EU protectionism are real risks. If tariffs jump from 20% to 100% globally, BYD’s high-margin export story collapses, forcing them back into the low-margin Chinese price war.

3. Currency Mismatch (The Silent Killer)

You buy HYDD in Singapore Dollars (SGD). The underlying asset is in Hong Kong Dollars (HKD/RMB).

The Risk: If the SGD strengthens (which MAS tends to ensure), the value of your HKD-denominated asset drops in SGD terms, even if the stock price stays flat. You are fighting a passive currency headwind.

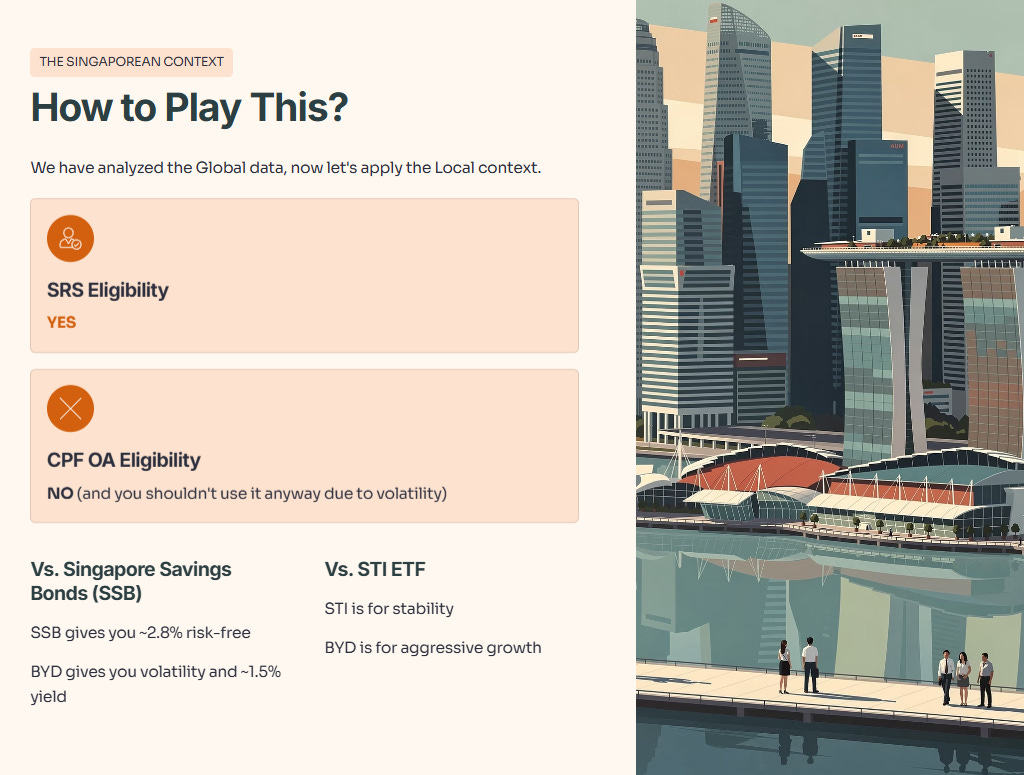

5. The Singaporean Context: How to Play This?