Why "Smart Money" is Selling DBS (Valuation Trap)

Fair Value Analysis: Why 'Smart Money' Is Waiting For $51.52

The yield looks safe, but the price is screaming “exit.” While retail investors are chasing record highs above S$58, institutional models are flashing a warning: DBS is currently trading 12.3% above its fair value. The 35% rally since the start of FY2025 has priced in perfection, leaving zero room for the reality of falling interest rates and flat earnings growth. If you’re holding this for a “safe” 5% yield, you might be about to lose two years of dividends in a single valuation correction.

In This Article:

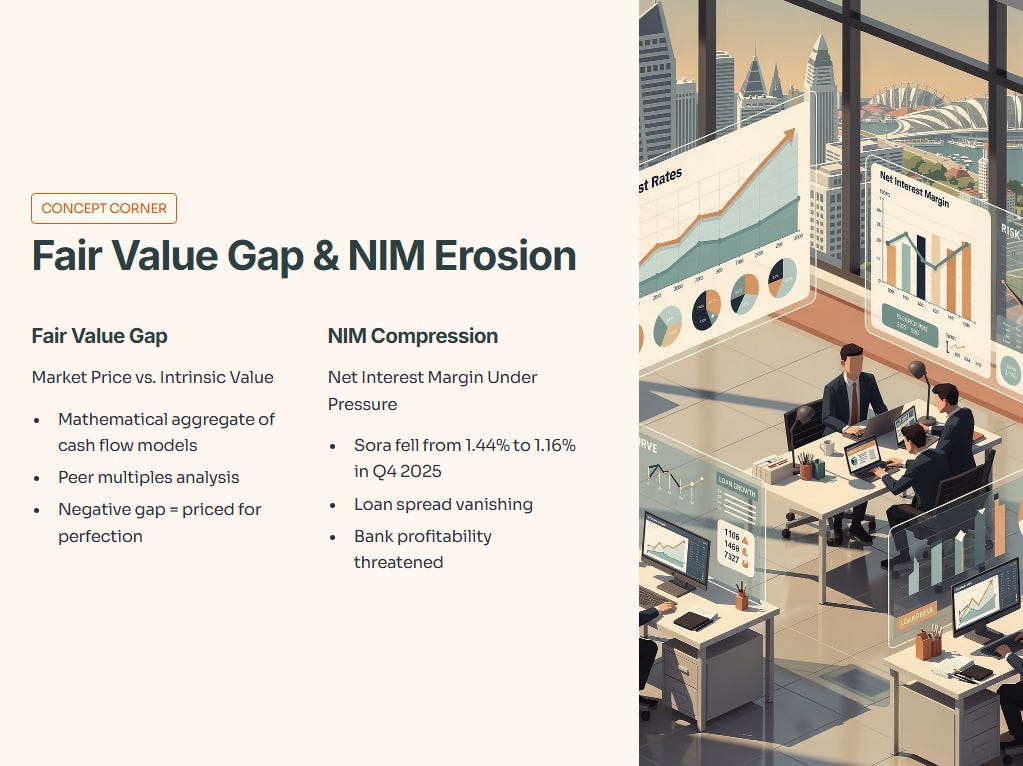

Concept Corner: The Fair Value Gap & NIM Erosion

The Balance Sheet

The Iggy Audit: A “Hold” That Feels Like a Sell

The Data Fortress: Evidence of the Squeeze

The Scenario Matrix: 2026 Forecast

InvestingPro Reality Check

The Verdict: The StrategyAbout Iggy the Investing Iguana channel

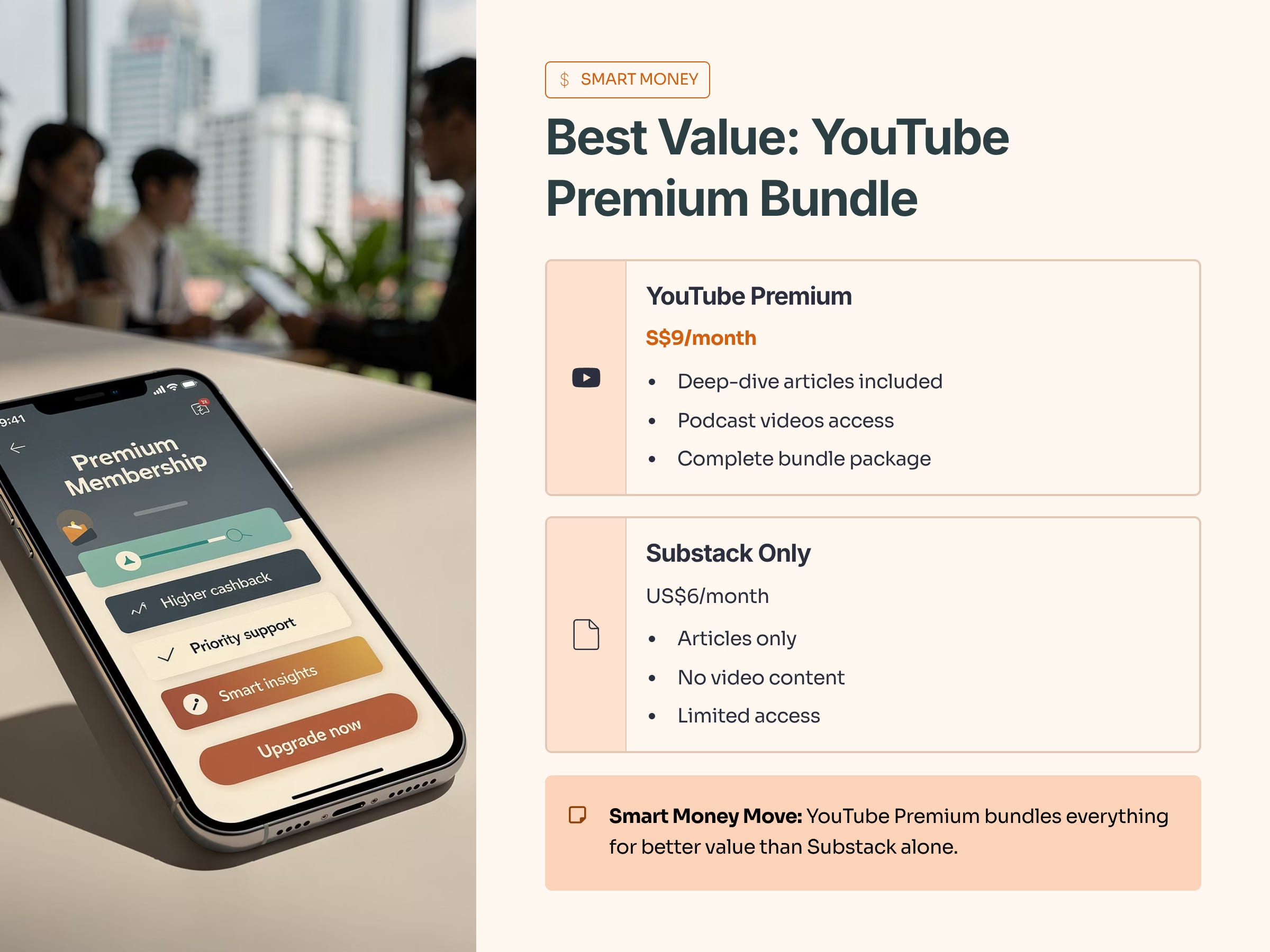

If you’re new here, welcome. I’m Iggy, your Singapore-based market analyst. Since October 2025, we’ve produced over 1,300 videos and 400 articles with 1.1 million watch hours. We are also home to a growing community of over 5,300 subscribers and an “Inner Circle” of 140+ paid members across YouTube and Substack.

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the ‘smart money’ move. Now, let’s get to the numbers.

Concept Corner: The Fair Value Gap & NIM Erosion

In a “Smart Money” portfolio, we look at the gap between Market Price and Intrinsic (Fair) Value. Intrinsic value isn’t a guess; it’s a mathematical aggregate of cash flow models and peer multiples. When the gap turns negative (market price > fair value), the stock is “priced for perfection.”

For banks like DBS, this perfection is threatened by Net Interest Margin (NIM) Compression. As the Singapore Overnight Rate Average (Sora) fell from 1.44% to 1.16% in Q4 2025, the “spread” the bank earns on loans is vanishing.

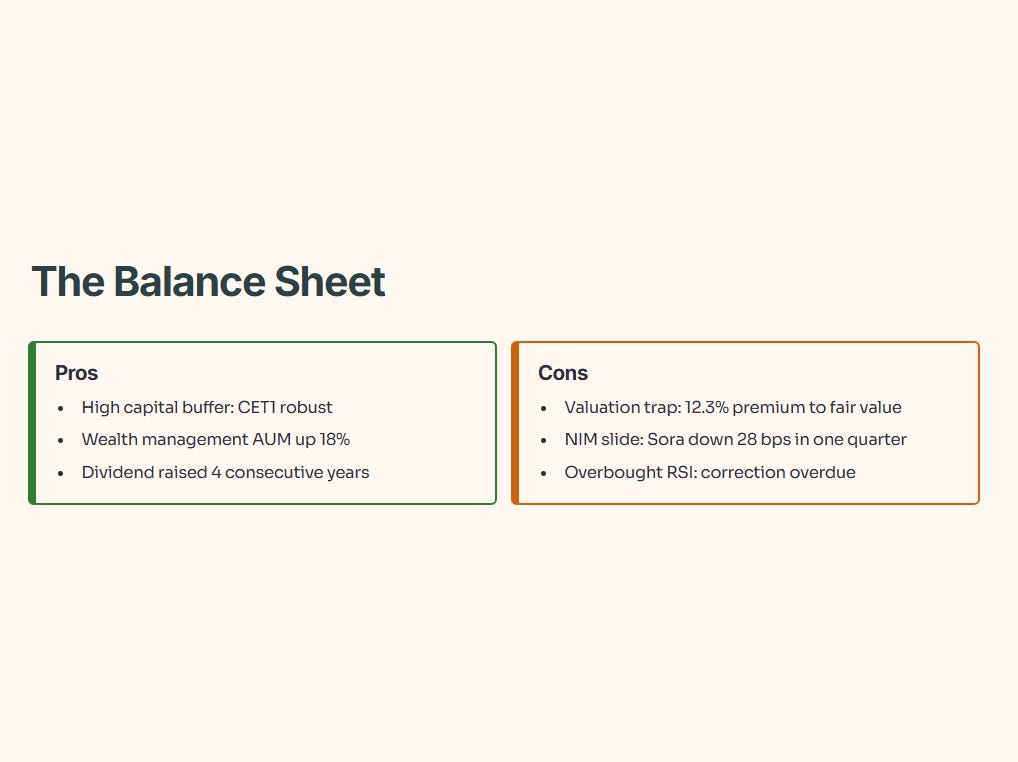

The Balance Sheet

Pros

High capital buffer: CET1 around the high‑teens, well above regulatory minimums.

Growing fee engine: wealth management AUM and fees up double digits, reducing reliance on NIM.

Shareholder‑friendly: dividends raised repeatedly, with management signalling ongoing capital returns.

Cons

Valuation trap: trades at a rich premium to fair value implied by normalised ROE and NIM.

Margin pressure: SORA and other benchmarks rolling over, pointing to further NIM compression.

Crowded trade: technicals flashing overbought, making a correction on bad news more likely.

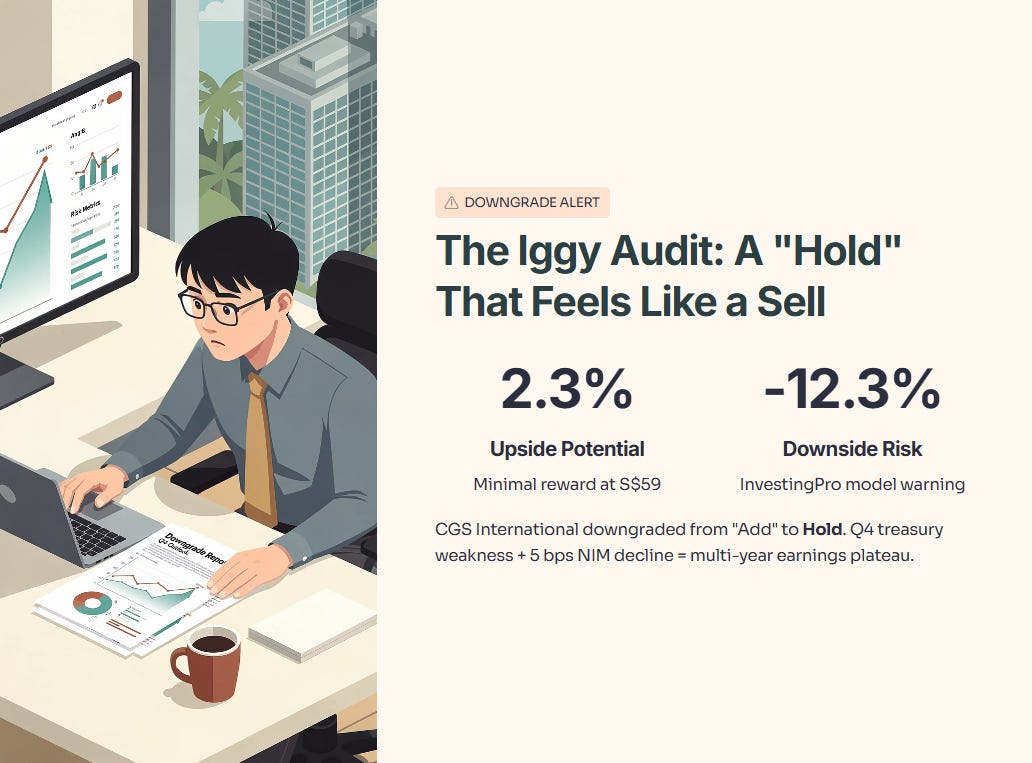

The Iggy Audit: A “Hold” That Feels Like a Sell

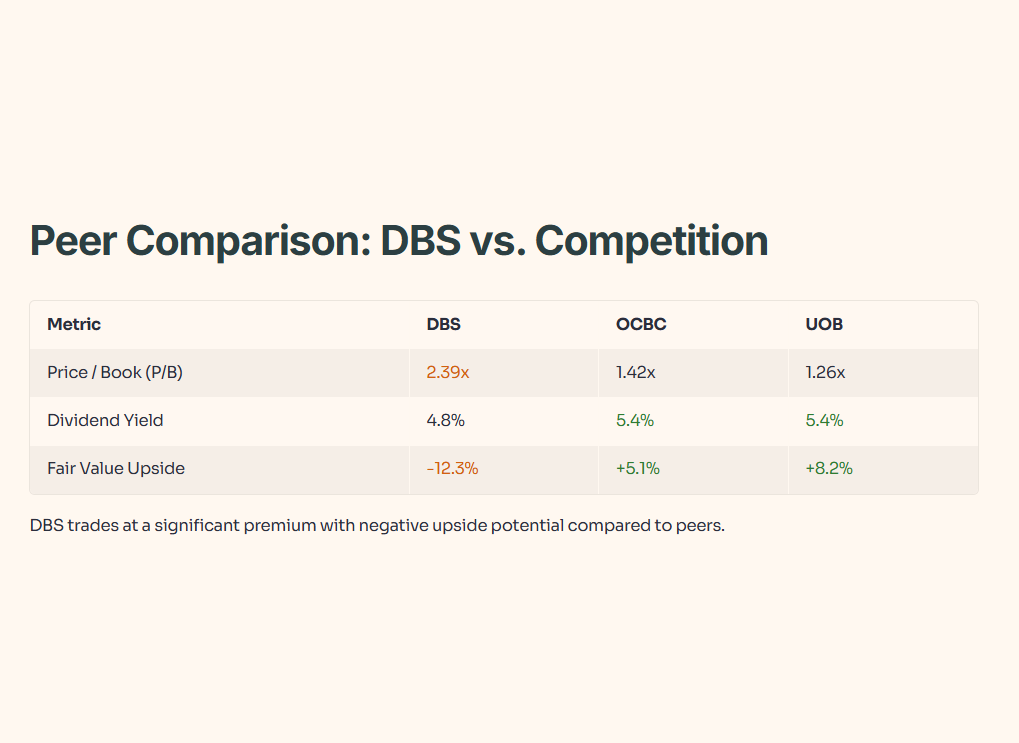

The narrative is shifting. CGS International (CGSI) recently downgraded DBS from “Add” to “Hold”. Why? Because at S$59, the potential upside is a measly 2.3%, but the downside risk identified by InvestingPro models is -12.3%.

We are seeing a “seasonal weakness” in Q4 treasury and trading income, paired with a projected NIM decline of 5 basis points. This isn’t just a bump in the road; it’s a multi-year earnings plateau.

Peer Comparison Table

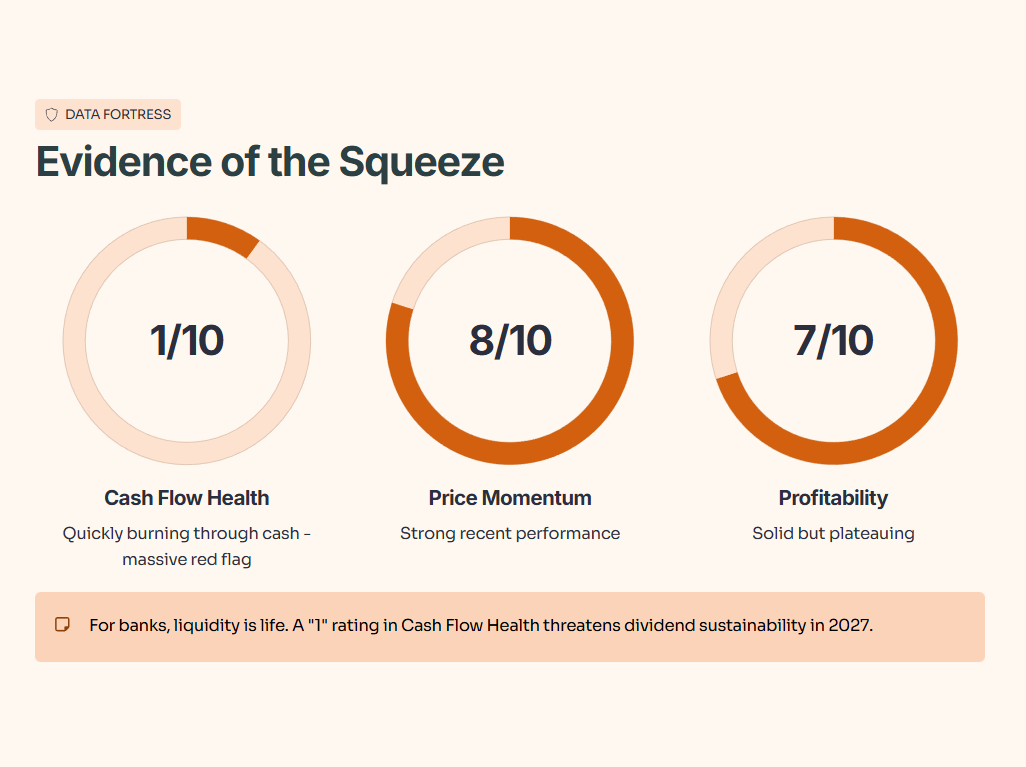

The Data Fortress: Evidence of the Squeeze

DBS’s financial health is a mixed bag. While it scores well on price momentum and profitability, it is “quickly burning through cash”. For a bank, liquidity is life, and a “1” rating in Cash Flow Health is a massive red flag for dividend sustainability in 2027.