The "Safe" REIT Trap: Why You Are Paying a "Fear Tax"

Two REITs can have the same elite management. One is a bargain. The other is a wealth trap waiting to snap.

Beyond Dividends: The “Elite” REIT Trap (Good Company vs. Good Price) 🦖

You’ve been sold a comfortable lie: “Buy blue-chip REITs, collect the dividend, sleep well.”

It sounds prudent. It appeals to the Singaporean desire for steady, passive income. But here is the painful truth that most retail investors miss: A great company can be a terrible investment if you overpay for it.

You can buy the best building in Singapore, but if you overpay for it by 30%, you will still lose money.

In Singapore’s current market, we have a “Tale of Two REITs.” Both have elite managers. Both are growing. But the data tells a brutal story about which one is a “Buy” and which one is a “Wait.”

I’ve analyzed the moves of Singapore’s top REITs and cross-referenced them with institutional valuation models. The difference between the Business Quality (the prose) and the Stock Valuation (the math) might shock you.

In This Article:

• About Iggy the Investing Iguana channel

• Part 1: The “Iggy Audit” (The Quality Scorecard)

• Metric 1: The “Rights Issue” Litmus Test

• Metric 2: The “Sponsor Lifeline” Test

• Metric 3: The “AEI Hustle” Test

• Part 2: The InvestingPro Data Check (The Valuation Reality Check)

• The Verdict: The Action Plan

• [InvestingPro Reality Check]

• [Iggy's Verdict / Conclusion]🦎 About Iggy the Investing Iguana

Welcome to the Iguana Pit! If you’re new here, I’m Iggy: your guide through the dense jungle of the Singapore markets. My mission is simple: to spot the predators before they spot your portfolio.

We are now 5,800+ subscribers strong across YouTube and Substack, focusing purely on the data-driven alpha that mainstream media misses.

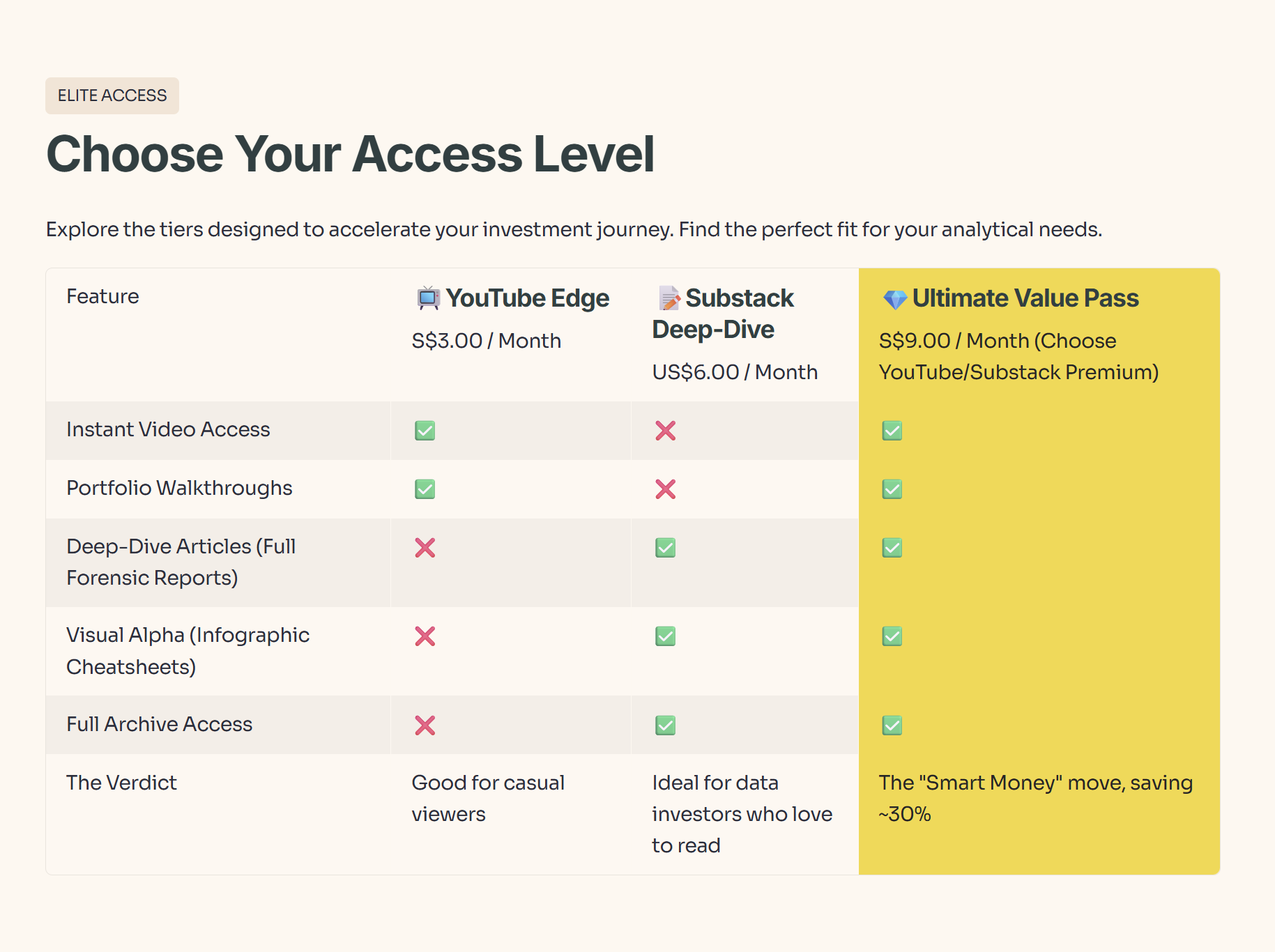

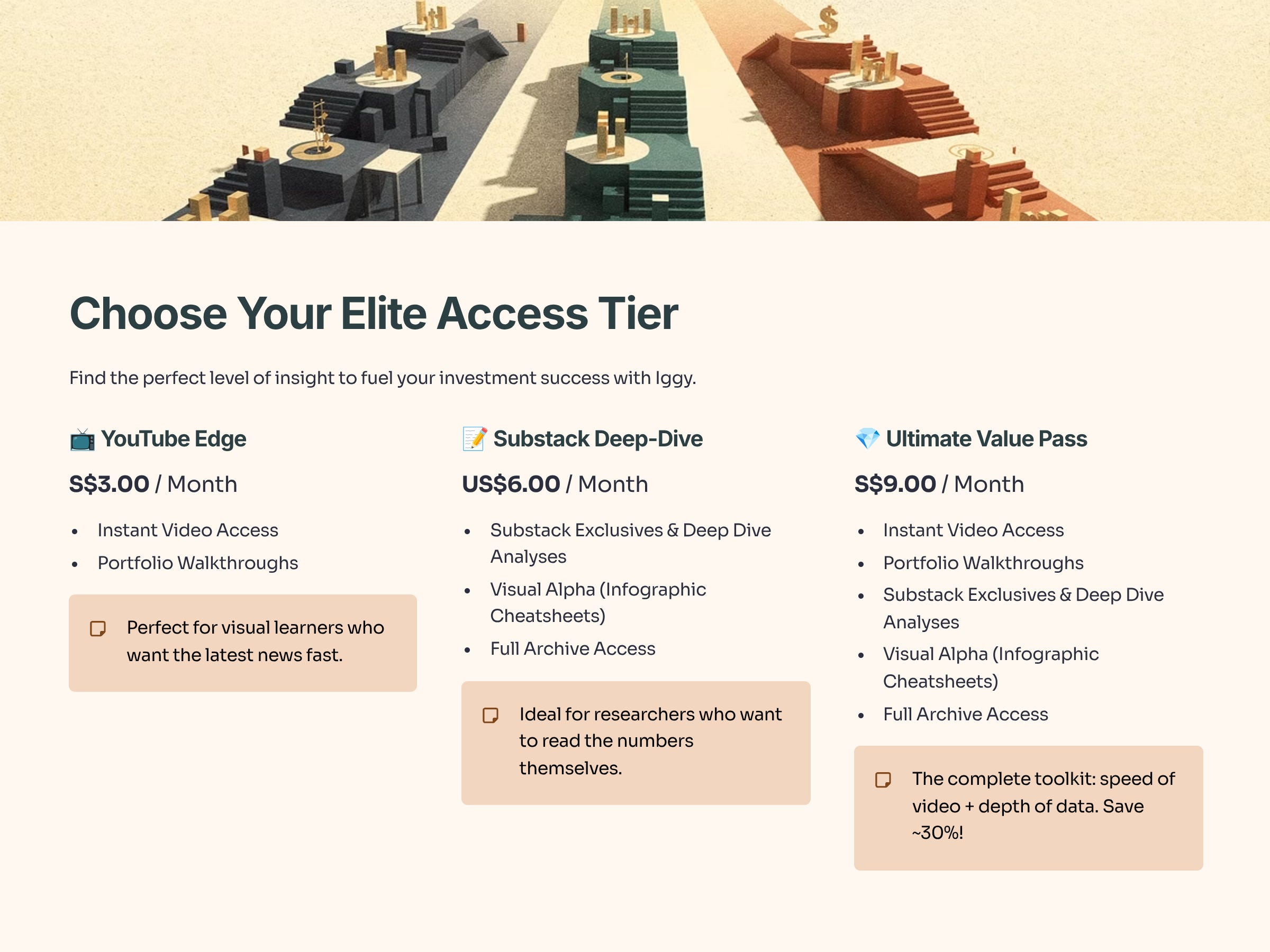

🚀 Join the “Elite 150” Inner Circle

Real alpha is found behind the velvet rope. Stop following the herd and start following the data with our 150+ paid members.

📺 The YouTube Edge (S$3/mo): Beat the Delay.

Instant Access: Watch new videos the moment they drop.

The Free Tier Trap: Free subscribers wait up to 14 days to see the same video. (By then, the news is old and the trade is gone).

📝 The Substack Deep-Dive (US$6/mo): Unlock the Vault.

Zero Paywalls: Read the full “Deep Dive” articles and “Substack Exclusive” articles found only on Substack.

Visual Alpha: Download exclusive Infographic Cheatsheets not available to free readers.

💎 The Ultimate Value Pass (S$9/mo): (BEST VALUE)

Get It All: Paid via YouTube, this bundle grants you Instant Video Access AND Full Substack Access.

The Math: You save ~30% compared to buying them separately. It’s the “Smart Money” move.

Why wait 2 weeks for old news? Get the data while it’s fresh. 👉 Join Here: https://www.youtube.com/@InvestingIguana/membership

Concept Corner: Price vs. Valuation

Now, to see why a “good” company can still be a “bad” investment, we need to go back to school for a moment. Today, we are going to rewire how you think about valuation versus price.

Most investors treat these as synonyms. They are not. They often move in opposite directions.

Price is what you pay. It is the number flashing on your brokerage screen, driven by mood, hype, fear, and liquidity.

Valuation is what you get. It is the present value of all the future cash flows that asset will produce for you, discounted back into today’s money.

Think of it like buying a chicken. The price is the twenty dollars you hand to the farmer. The valuation is the total value of every egg that chicken will lay over its life, translated into today’s dollars. If the chicken costs twenty dollars but only lays ten dollars worth of eggs, you have bought a great chicken, but you made a poor investment. You overpaid for the cash flow.

In the REIT market, this distinction is critical because investors often confuse “safety” with “value.” They see a big name, a famous building, and a stable sponsor, and assume any price is justified. But financial gravity always wins.

If you pay a price that assumes perfection—rents never fall, occupancy stays at one hundred percent, and interest rates drift back to zero—you leave yourself no margin for error. This is what “priced for perfection” looks like. When a stock is priced for perfection, even a small piece of bad news can trigger a sharp drop.

On the flip side, when a stock is priced for disaster but the business is actually holding up, that is where the margin of safety lives. That is where the smart money hunts: in the gap between the price on the screen and the intrinsic value of the cash flows.

Part 1: The “Iggy Audit” (The Quality Scorecard)

First, we separate the trash from the treasure. I’ve watched dozens of REITs make capital moves. The elite managers follow a pattern: They reinvest, they expand, and they sweat their assets. The weak ones? They sell and shrink.

Here is the “Elite Manager Scorecard” I use to vet the business before I look at the price.

Metric 1: The “Rights Issue” Litmus Test

When a REIT asks for fresh cash, are they raising money to save the ship (dilutive, defensive) or to grow the ship (accretive, offensive)?

The Elite Move: CICT’s 2025 CapitaSpring Acquisition

In August 2025, CapitaLand Integrated Commercial Trust (CICT) didn’t ask for cash to pay down bad debt. They raised S$600 million to buy the remaining stake in CapitaSpring—a trophy asset. This added 1.1% to DPU. The message: “We are doubling down on Singapore.”

The Trap: Manulife US REIT (MUST)

Contrast this with Manulife US REIT (MUST). They sold assets (Plaza 2, Peachtree) just to pay debt. That is not growth; that is an amputation.

💡 Iggy’s Insight:

“Never blindly participate in a rights issue. Ask yourself: Is this money buying a new engine, or patching a hole in the hull? Elite managers use cash to buy cash-flow machines. Distressed managers use cash to pay the banker.”

Metric 2: The “Sponsor Lifeline” Test

When interest rates climbed, did the parent company step in?

The Elite Move: FCT's Northpoint Consolidation — Frasers Centrepoint Trust (FCT) acquired Northpoint City South Wing because its sponsor (Frasers Property) fed it the deal. This pipeline support is why FCT’s FY2025 DPU hit 12.113 cents.

The Trap: The Orphan REIT

MUST is an “orphan.” Its parent didn’t feed it assets when the U.S. office market cracked. It was left to fend for itself, and the result was a halted distribution.

Metric 3: The “AEI Hustle” Test

Are the managers sweating their assets with renovations (Asset Enhancement Initiatives)?

The Elite Move: FCT’s Tampines 1 Transformation

FCT completed the renovation of Tampines 1 with an ROI exceeding 8%. They didn’t just collect rent; they upgraded the mall to match the demographic shift in the East.

💡 Iggy’s Insight:

“Boring is good, but passive is fatal. If you don’t see ‘AEI’ in the annual report, run. It means the manager is milking the asset dry rather than feeding it to ensure it lives another 10 years.”

Part 2: The InvestingPro Data Check (The Valuation Reality Check)

Now for the plot twist.

We have established that CICT and FCT are both “Elite” businesses. But does that mean you should buy both today?

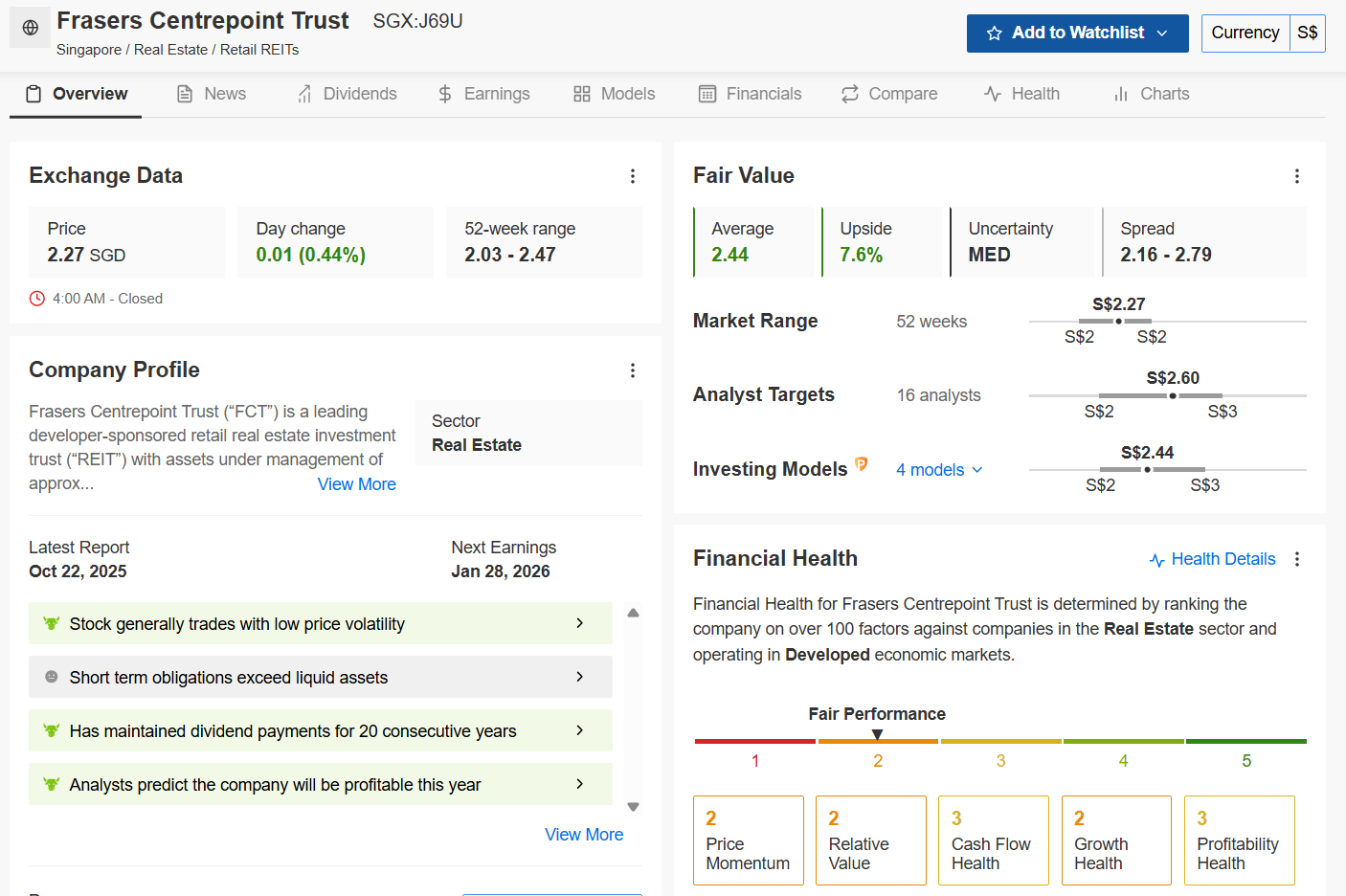

I don’t guess at valuations. I check the InvestingPro Fair Value Model. This aggregates 10+ distinct financial models (DCF, Dividend Discount, P/E Multiples) to find the true intrinsic value.

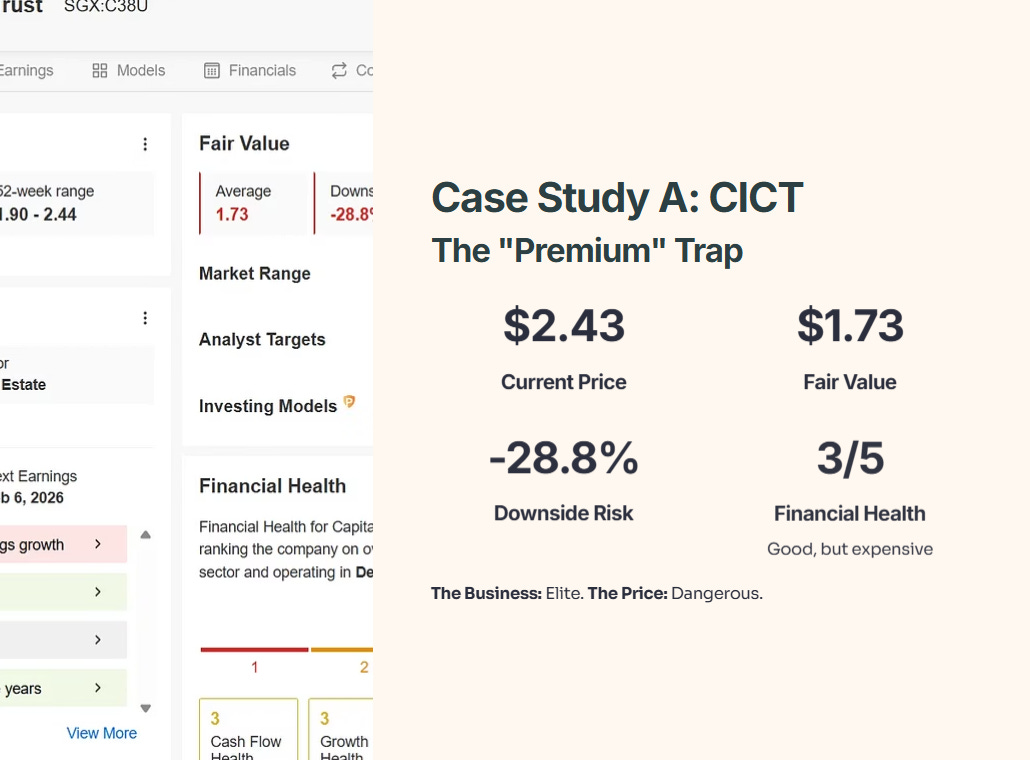

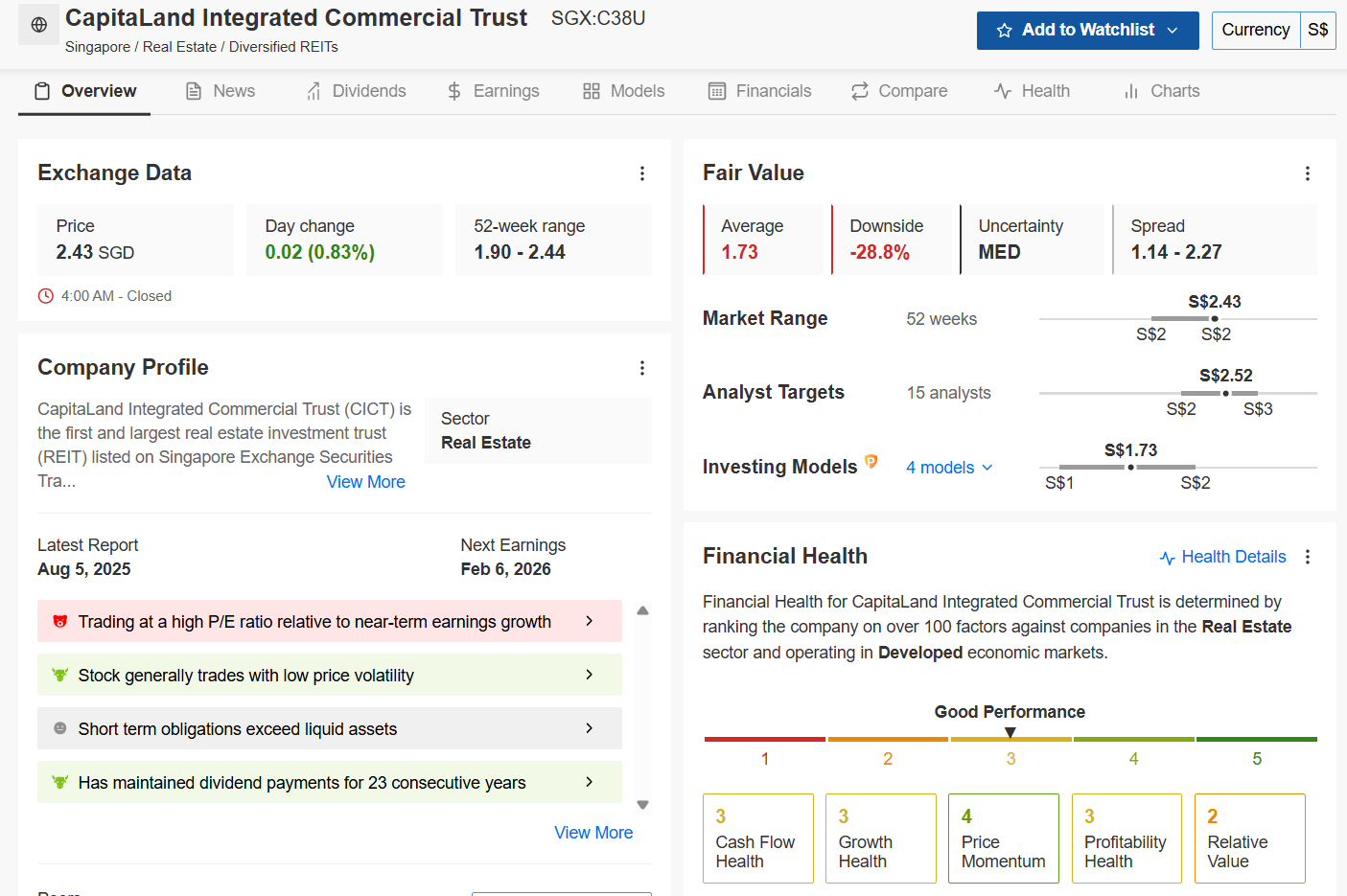

Case Study A: CICT (The “Premium” Trap)

The Business: Elite. The Price: Dangerous.

Current Price: S$2.43

Fair Value (Models): S$1.73

The Warning: -28.8% Downside Risk

Financial Health: Good (3/5), but expensive.

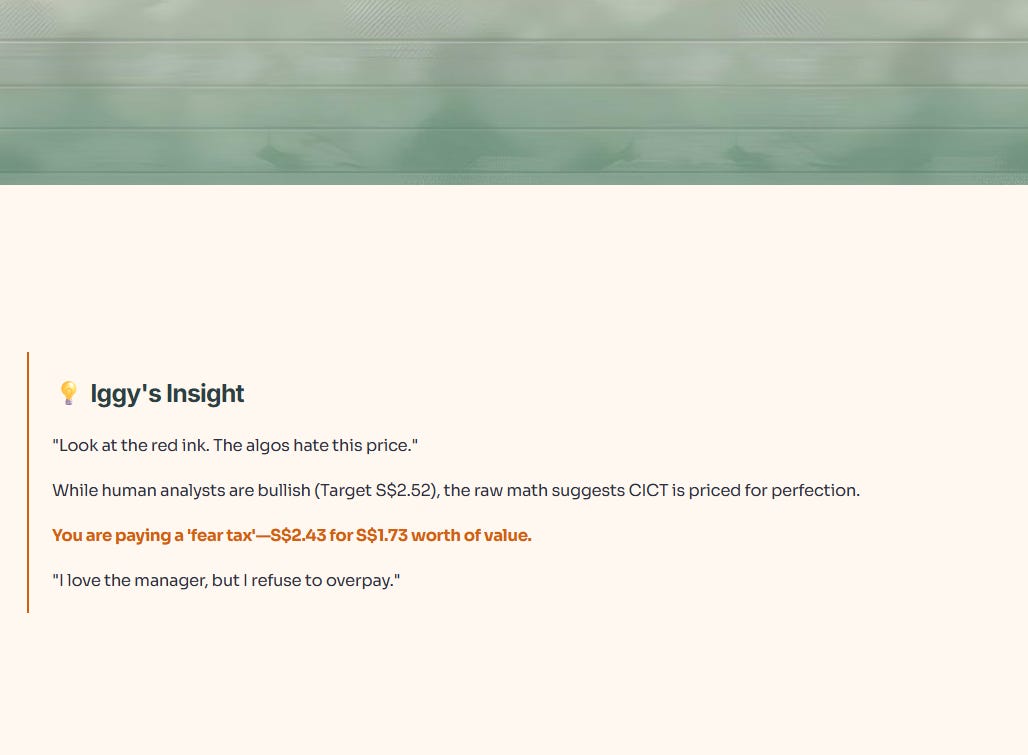

💡 Iggy’s Insight:

“Look at the red ink. The algos hate this price. While human analysts are bullish (Target S$2.52), the raw math suggests CICT is priced for perfection. Everyone wants safety, so they have bid the price up to the moon. You are paying a ‘fear tax’—paying S$2.43 for S$1.73 worth of value. I love the manager, but I refuse to overpay.”

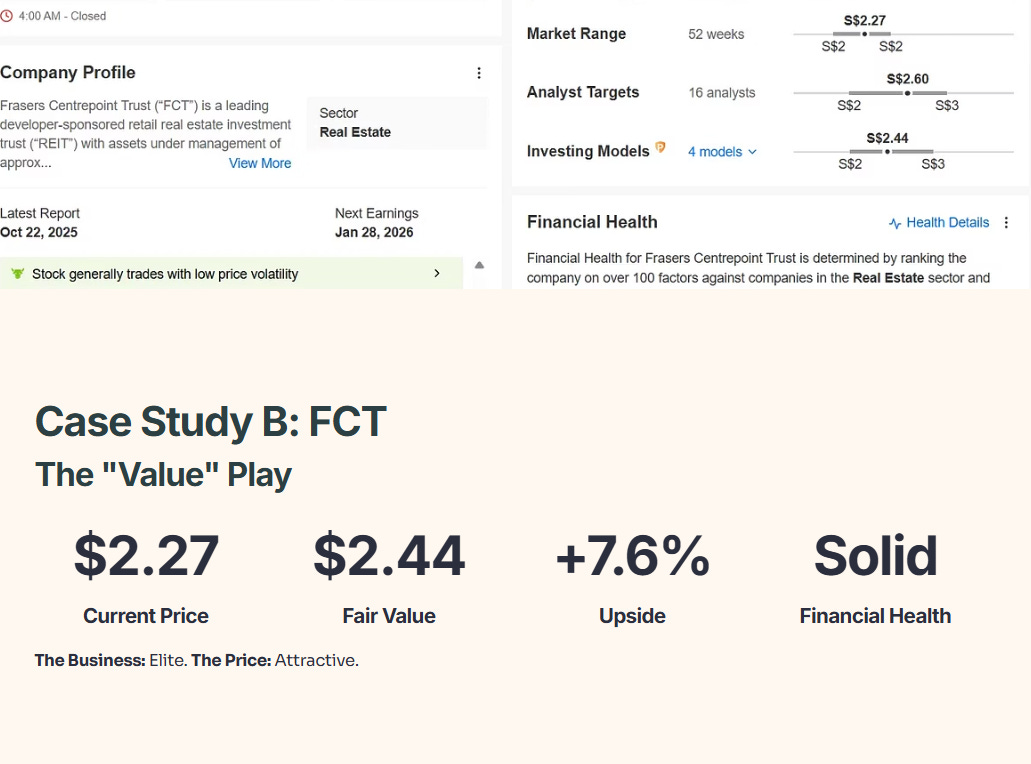

Case Study B: FCT (The “Value” Play)

The Business: Elite.The Price: Attractive.

Current Price: S$2.27

Fair Value (Models): S$2.44

The Opportunity: +7.6% Upside

Financial Health: Solid.

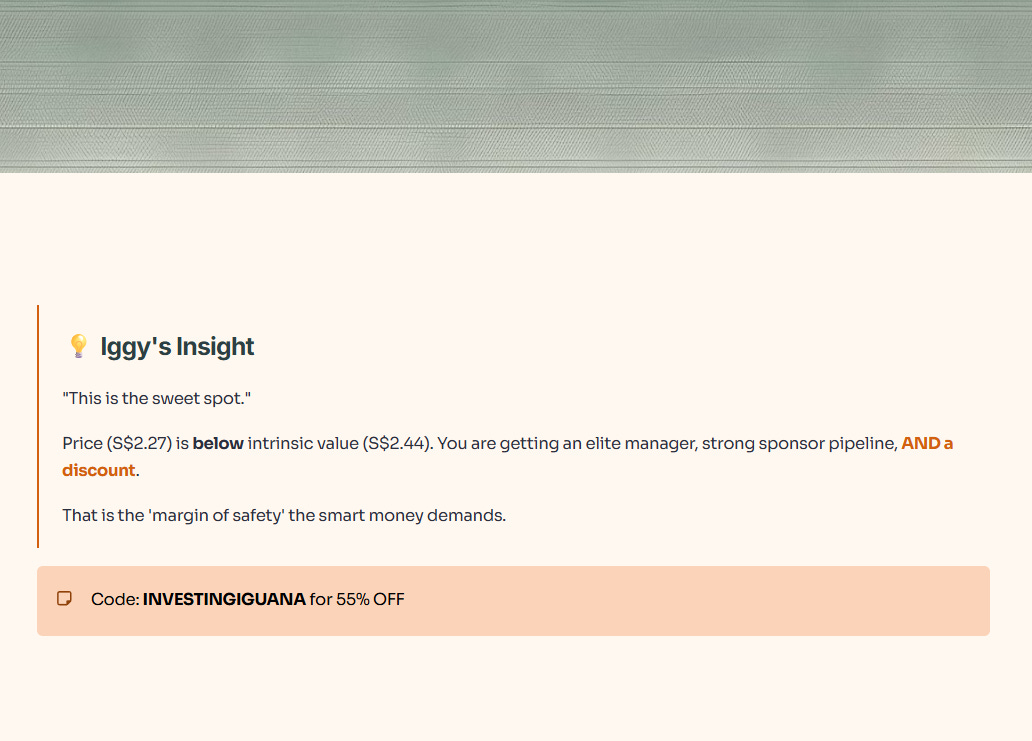

💡 Iggy’s Insight:

“This is the sweet spot. The price (S$2.27) is *below* the intrinsic value (S$2.44). You are getting an elite manager, a strong sponsor pipeline, AND a discount. That is the ‘margin of safety’ the smart money demands.”

(Code: INVESTINGIGUANA for 55% OFF)

The Verdict: The Action Plan