Stop Leaving Yield on the Table: A 2026 Playbook to Park Cash Safely, Simply, and at Competitive Yield

Unlock the smart way to park your cash in 2025—discover proven strategies that give you top yields, easy access, and no hidden traps, so your money always works its hardest for you.

Many savers feel stuck in 2025. Headline rates are easing. “Up to” numbers hide hoops and caps. Cash solutions look like funds, which can feel complex. This guide fixes that. Here’s a clear, Singapore-focused playbook to park cash for bills, emergencies, mid-term goals, and dry powder—so liquidity stays high, risk stays controlled, and yield stays fair.

We’ll keep the same four-bucket framework. Then we’ll pick the right tools for each bucket, give explicit Buy/Hold/Sell calls, and show how to stack promos without letting them run the plan. You’ll also get CPF/SRS angles, a clean risk radar, a sample allocation, and five practical tables you can apply today.

The Problem in One Line

Lower rates, higher noise. Banks price deposits off short-term rates. As policy eases, bonus rates tend to shrink and hoops rise. Money market funds (MMFs) track short-term instruments like bills and repo—yields are real, but they drift as rates move. The edge comes from a fit-for-purpose setup: match each dollar to a job, then diversify platforms to cut operational risk.

The Four-Bucket Framework

Bucket A: Transactions (0–1 month of spend). Priority: instant access. Treat interest as a bonus.

Bucket B: Emergency Fund (3–6 months). Priority: safety and fast access. Mix fuss-free cash and MMFs.

Bucket C: Mid-Term Savings (6–24 months). Priority: predictable return. Use SSB ladders, fixed deposits, and short-duration funds.

Bucket D: Opportunistic Cash (dry powder). Priority: rapid deployment with fair yield. Keep it close to the trading ecosystem.

The Four-Bucket Framework is a simple way to organise your cash by purpose and time horizon. Bucket A is for your daily or monthly spending—keep this cash easily accessible and see any interest earned as a nice extra. Bucket B is your emergency fund meant for quick access in case of loss of income or sudden expenses; store this safely in fuss-free accounts or money market funds. Bucket C is for savings you’ll need in the next 6 to 24 months, so aim for safe, predictable returns with government bonds, fixed deposits, or short-term funds. Bucket D is "dry powder" for opportunities—cash you might invest or deploy quickly, so keep it near your trading account and earn a fair yield while waiting. This setup balances access, safety, and interest based on your needs.

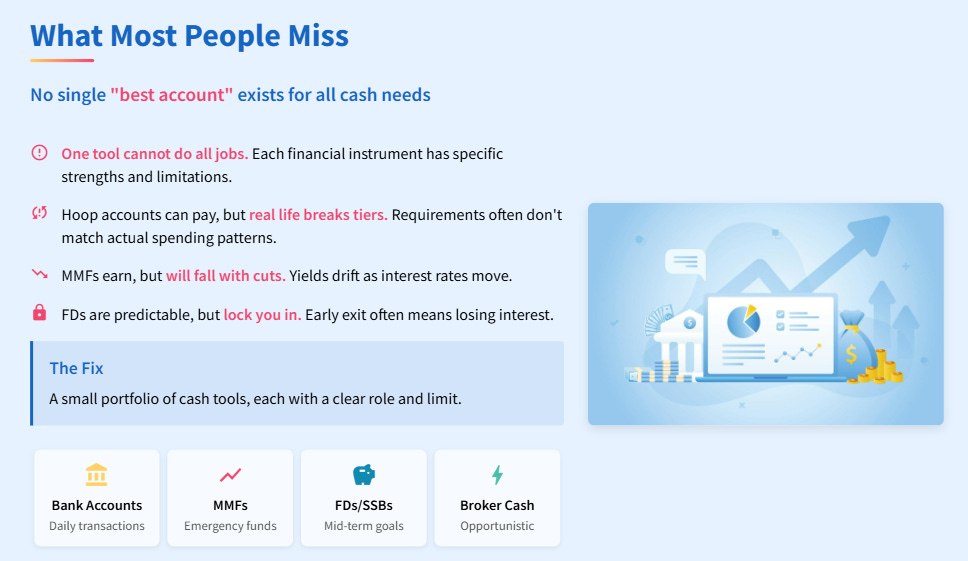

What Most People Miss

There is no single “best account.” One tool cannot do all jobs. Hoop accounts can pay, but real life breaks tiers. MMFs earn, but will fall with cuts. FDs are predictable, but lock you in. The fix is a small portfolio of cash tools, each with a clear role and limit.