Stop Paying $25 'Taxi Fare' Every Time You Buy Your Monthly REITs

Institutional funds never pay retail 'flag-down' rates. Here is the 3-layer forensic audit to protect your investment compounding today.

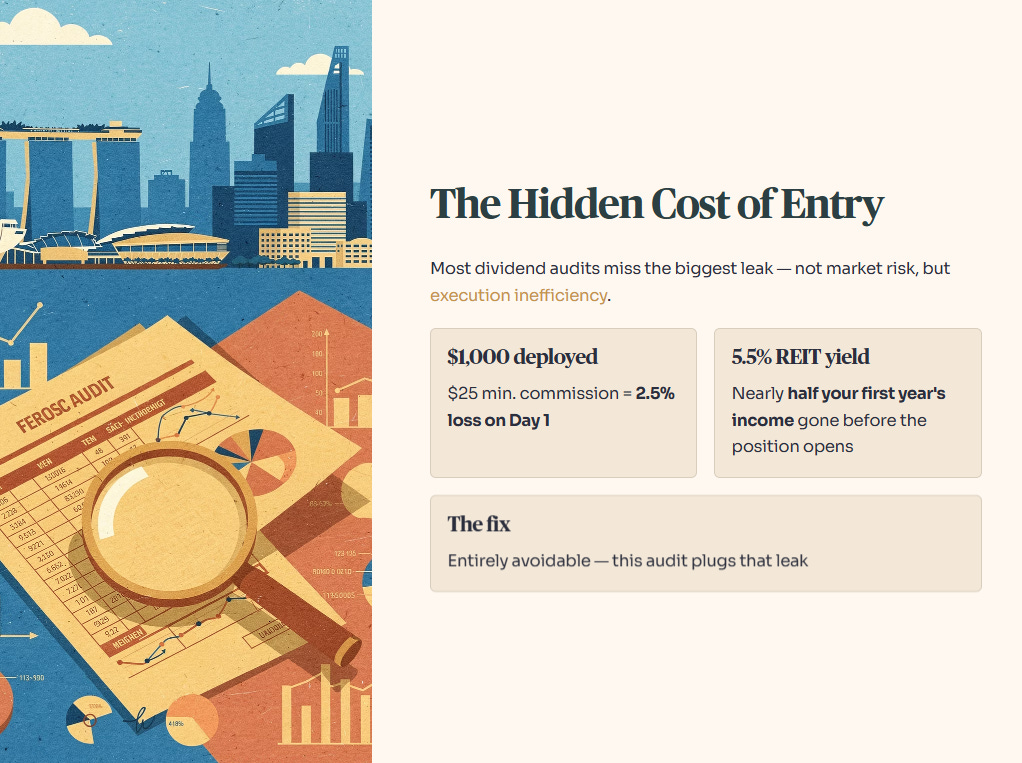

The Forensic Problem: The Cost of Getting In

Most forensic audits of a dividend portfolio start in the right place — gearing ratios, interest coverage, yield spread above the risk-free floor. But there is a cost that rarely appears in any of those calculations, and it has nothing to do with the underlying asset.

It is the cost of getting in.

For a retail investor deploying S$1,000 a month into a Singapore REIT through a legacy bank brokerage, a S$25 minimum commission represents a 2.5% immediate loss of principal on Day 1. If that REIT yields 5.5%, you have surrendered nearly half of your first year’s income before the position even opens. That is not market risk. That is execution inefficiency — and it is entirely avoidable.

This piece is about plugging that specific leak.

This Article:

The SRS Trap: Friction Inside a Tax-Efficient Wrapper

The $25 Minimum Commission Trap

The Compounding Audit: What Friction Costs Over 20 Years

The Fee Audit: What You Are Actually Paying

Peer Comparison: The Friction Impact on a S$10,000 Portfolio

The Timing Fallacy: Why Waiting for a Dip Doesn’t Fix a Leak

The Forensic Stress Test: Your Margin of Safety

Forensic Conclusion: Plugging the Leaks

Mandatory Financial Health Checklist

Final Compliance Disclosure

InvestingPro Reality Check

Iggy's Verdict

About Iggy & the Elite Investors

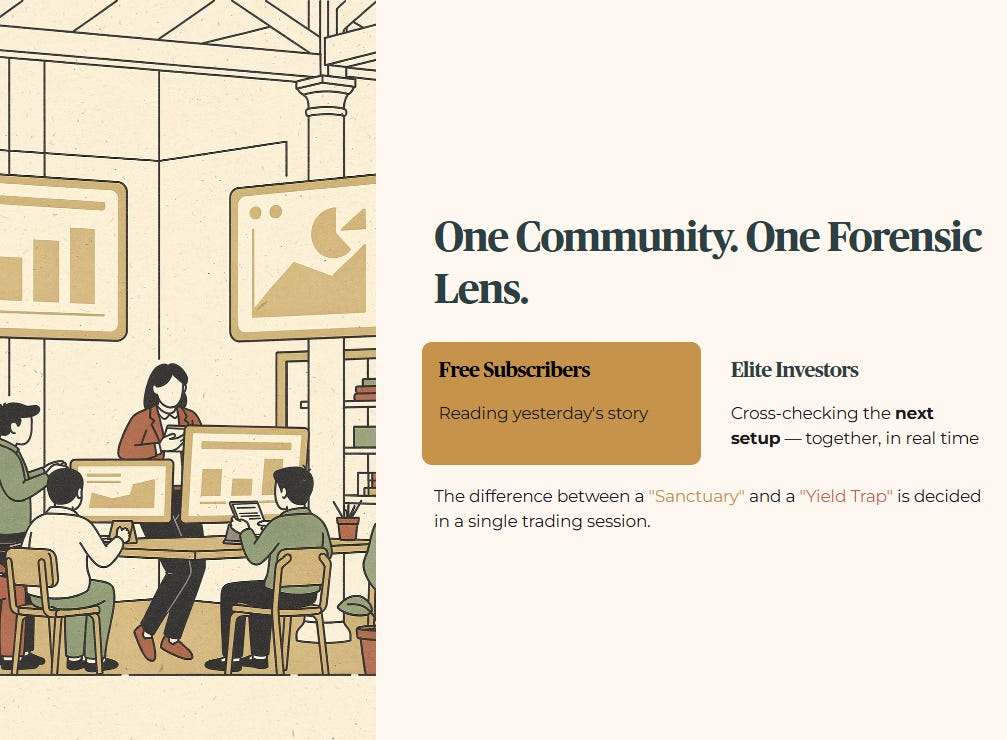

One Community. One Forensic Lens. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. While free subscribers are reading yesterday’s story, Iggy’s Elite Investors are already cross-checking the next setup — together, in real time.

Iggy’s Elite Investors don’t just get the report earlier. They get the full forensic picture the moment it’s finalised — zero-day breakdowns, the complete “Red Zone” watchlist, and institutional-grade cheatsheets built around the same Five-Layer Audit you see here. The difference is they get it before the market opens, not after it has already moved.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

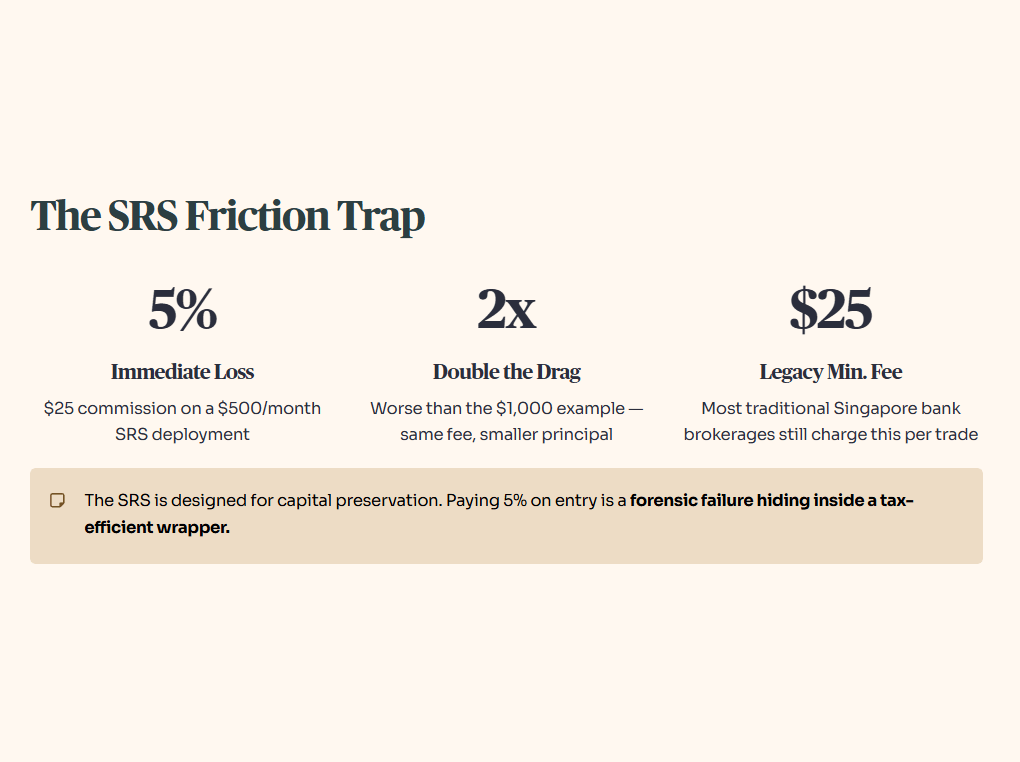

The SRS Trap: Friction Inside a Tax-Efficient Wrapper

For many investors in this community, the SRS is the primary deployment vehicle. It is a well-constructed tax deferral tool — contributions reduce your assessable income in the year they are made, and the capital compounds without annual tax drag. Used correctly, it is one of the cleanest structural advantages available to the Singapore retail investor.

But it carries a specific friction trap that most SRS holders never audit.

Because annual contributions are capped and most disciplined investors deploy in monthly or quarterly tranches rather than a single lump sum, every deployment is a separate transaction. Every transaction is a separate commission event. If you are using a legacy bank brokerage and deploying S$500 a month into a REIT through your SRS, that S$25 minimum commission represents a 5.0% immediate loss of principal — double the drag of the S$1,000 example we opened with.

The SRS is designed for capital preservation. Paying 5% on entry to a legacy broker is not capital preservation. It is a forensic failure hiding inside a tax-efficient wrapper.

The SRS friction problem is real — but it is not unique to SRS. The same commission drag applies to every cash account, every regular savings deployment, every DCA tranche you place through a legacy broker. Whether your capital sits in an SRS wrapper or a standard brokerage account, the execution inefficiency is identical. The SRS example simply makes the numbers harder to ignore. What follows applies to your general investment account — where you have full flexibility over platform choice.

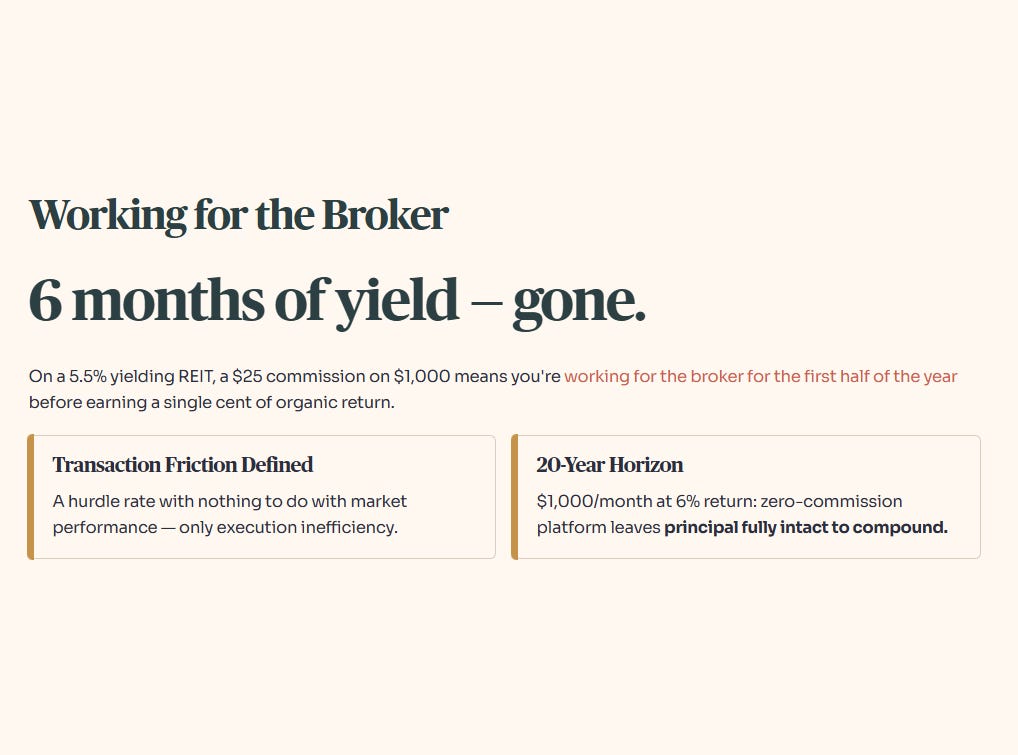

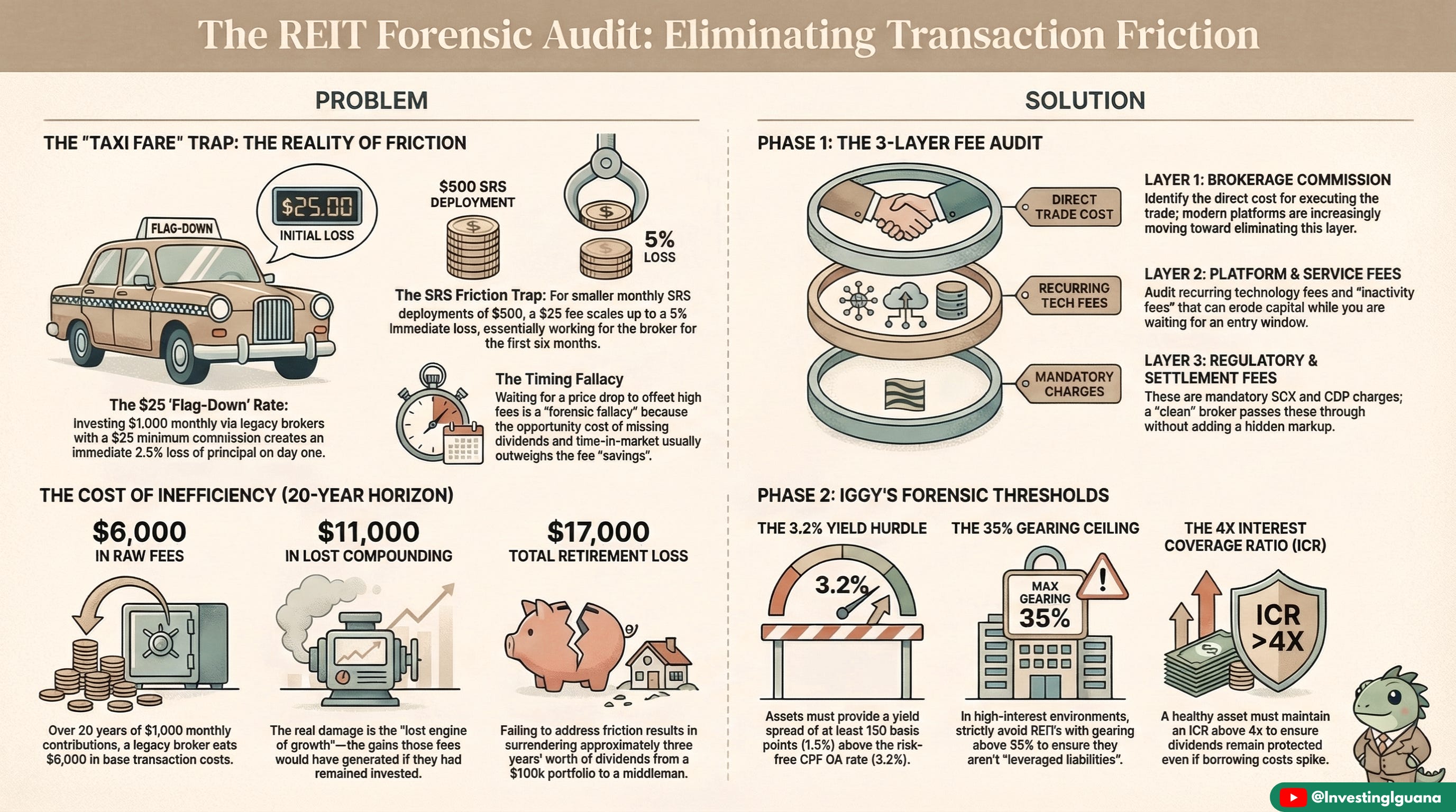

The $25 Minimum Commission Trap

The core of this hidden tax lies in the structure of legacy brokerage fees. Most traditional banks and brokerages in Singapore still operate on a minimum commission model — often hovering around S$25 per trade.

For an institutional fund moving S$10 million, a S$25 fee is a rounding error. But for a retail investor practising disciplined Dollar Cost Averaging, it is a forensic disaster.

The math is straightforward. A S$25 minimum fee on a S$1,000 monthly deployment represents a 2.5% immediate loss of principal. If that REIT is yielding 5.5% annually, nearly half of your first year’s income has vanished on Day 1. You are essentially working for the broker for the first six months of the year before you see a single cent of organic return. This is the definition of transaction friction — a hurdle rate that has nothing to do with market performance and everything to do with inefficient execution.

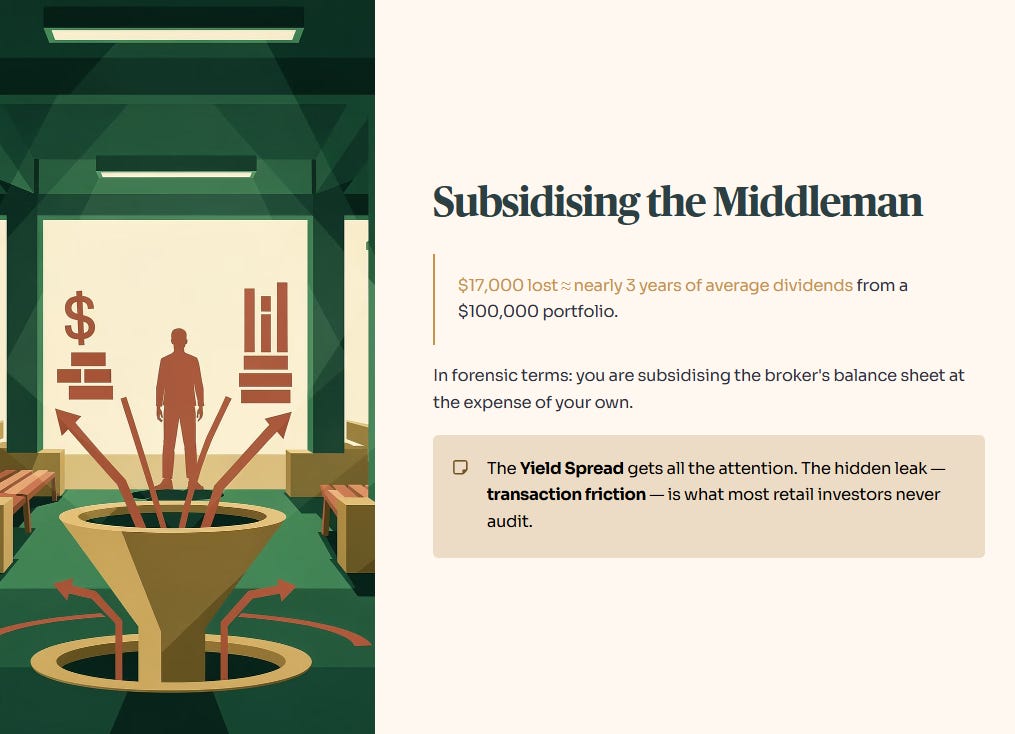

The Compounding Audit: What Friction Costs Over 20 Years

When we extrapolate this over a 20-year horizon, the numbers shift from annoying to serious.

Table 1: 20-Year Friction Comparison (Assumes S$1,000 monthly contribution at 6% annual return)

By simply failing to address transaction friction, the average investor surrenders S$17,400 of retirement capital to a middleman. That is equivalent to nearly three years of average dividends from a S$100,000 portfolio. In forensic terms, you are subsidising the broker’s balance sheet at the expense of your own.

— Partner Note —

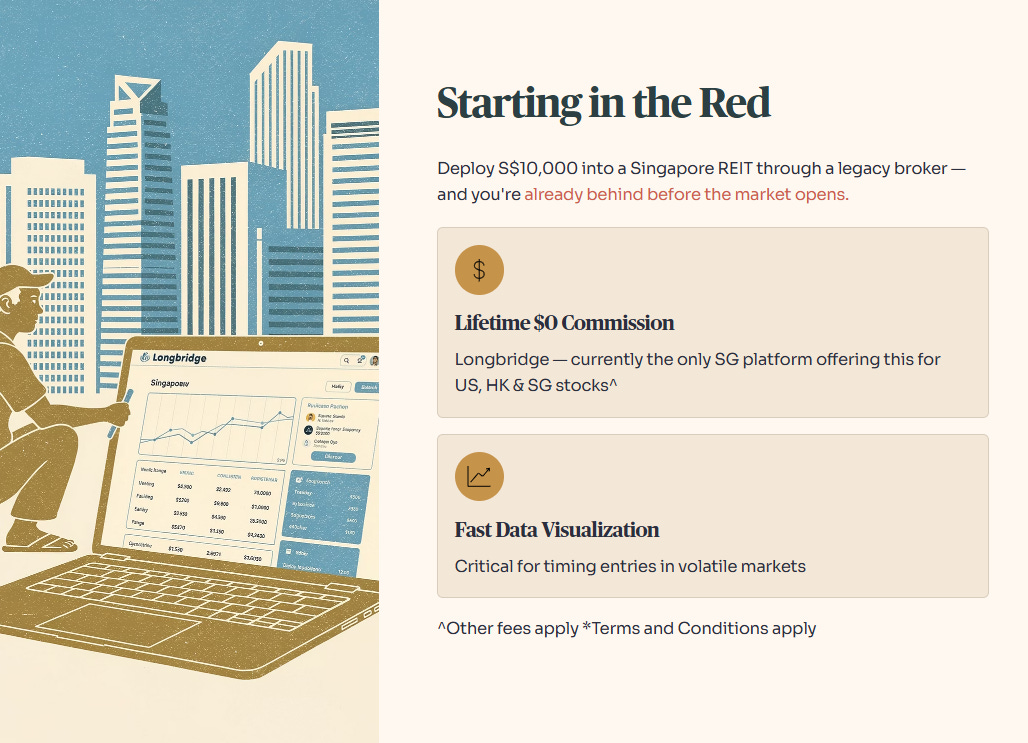

Fixing the analysis is the easy part. Fixing the execution requires the right tools.

I’ve shifted my own deployment to Longbridge for one forensic reason: they are currently the only platform in Singapore offering Lifetime S$0 Commission on US, HK, and SG stocks. For a DCA investor running monthly tranches, that single change eliminates the entire minimum commission drag we just calculated. Their data visualisation is also fast enough for volatile entry windows — which matters when you are trying to time a position, not just place one.

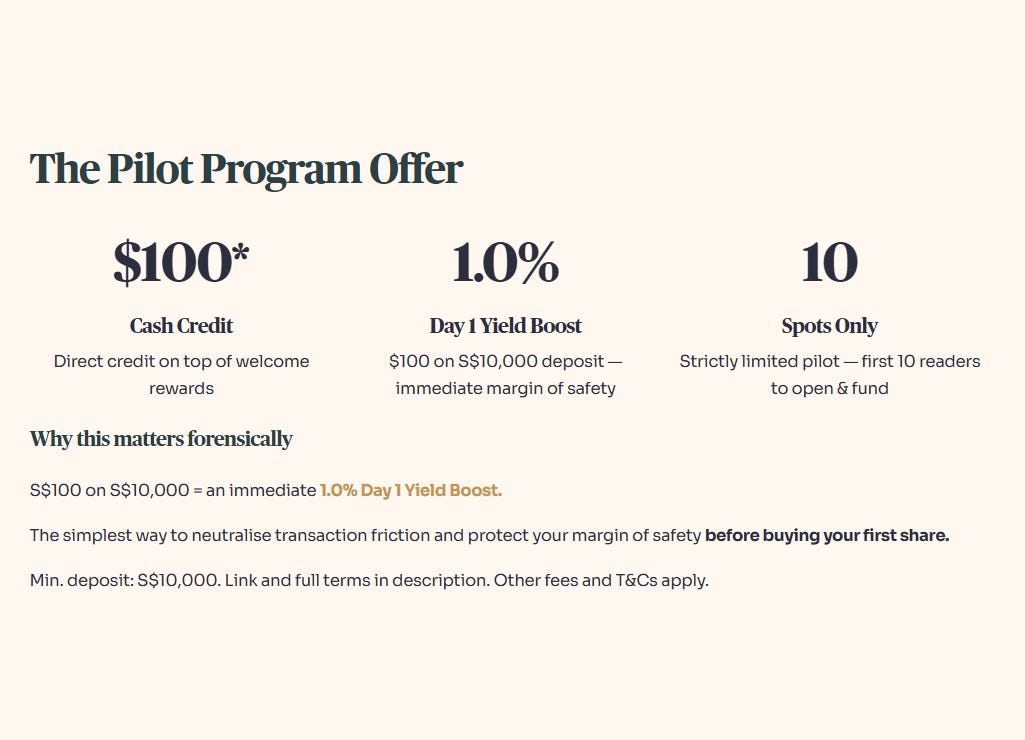

I’ve partnered with Longbridge on a specific pilot for this community. The first 10 readers to open and fund an account with a minimum of S$10,000 will receive a direct S$100 cash credit.

The forensic math: S$100 on a S$10,000 deployment is a 1.0% Day 1 Yield Boost — effectively neutralising your entry cost before you’ve bought a single share. For context, that’s better than the yield spread on several SGX blue chips I’ve reviewed this quarter.

This is strictly limited to 10 spots. Full terms and conditions are linked below — read them before committing, as standard platform fees apply.

— End Partner Note —

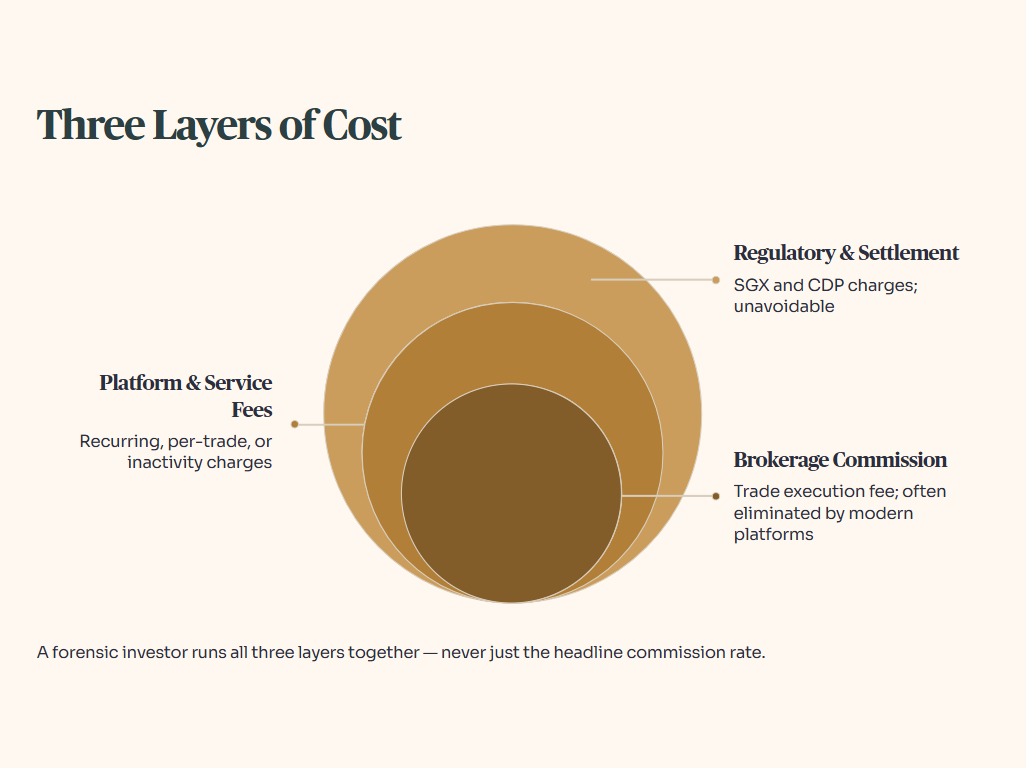

The Fee Audit: What You Are Actually Paying

Before you can eliminate transaction friction, you need to know exactly what you are being charged for. Most retail investors conflate three distinct cost layers into one vague sense of “fees.” A forensic investor separates them precisely.

Brokerage Commission is what the broker charges for executing your trade. This is the layer Longbridge has eliminated with their Lifetime S$0 Commission structure. It is also the layer most commonly used in marketing — which means it is the one most worth scrutinising.

Platform and Service Fees are recurring or per-trade charges for using the technology infrastructure. Some platforms charge a percentage of assets under custody. Others use flat monthly fees. The forensic question is not whether these fees exist — it is whether they are disclosed clearly and whether inactivity fees can erode your capital while you are waiting for the right entry window.

Regulatory and Settlement Fees are non-negotiable. SGX, CDP, and clearing house charges apply to every trade on every platform. No broker can remove them. What a clean broker will not do is mark them up quietly.

When evaluating any platform, run all three layers through Table 2. The headline commission rate is rarely the full picture.

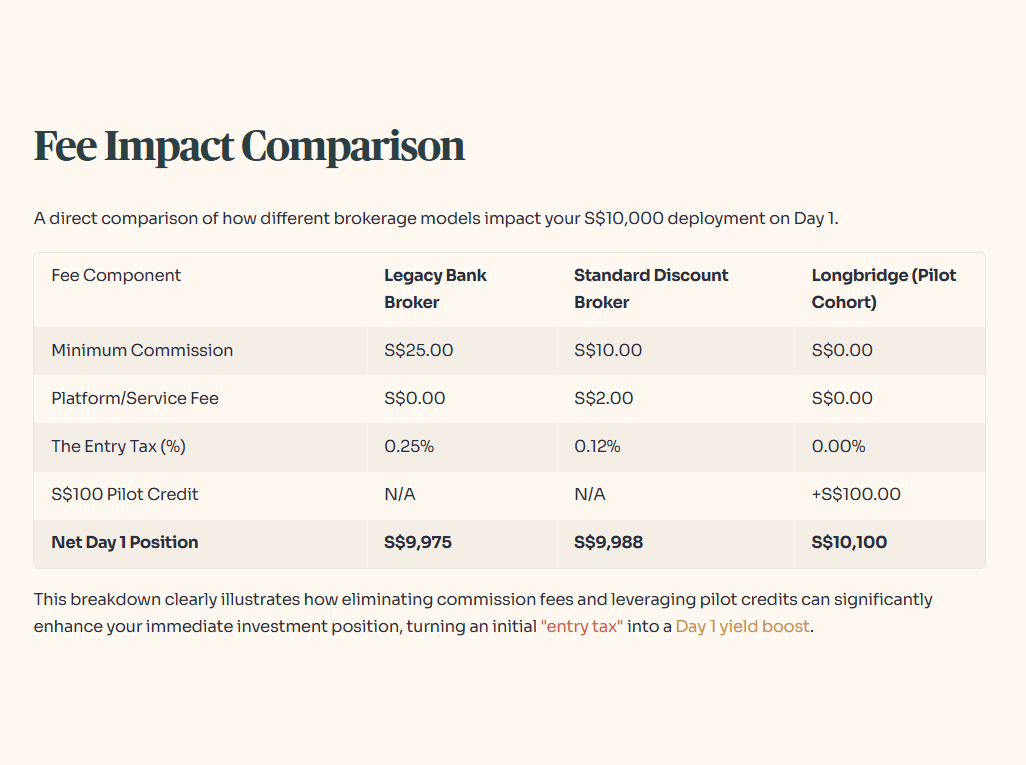

Peer Comparison: The Friction Impact on a S$10,000 Portfolio

Table 2: Fee Impact on S$10,000 Single Deployment

The Timing Fallacy: Why Waiting for a Dip Doesn’t Fix a Leak

A common pushback is that investors can “make up” for high transaction fees by timing a better entry price. The logic goes: if I wait for the REIT to drop by S$0.03, I’ve saved more than the S$25 commission.

This is a forensic fallacy on two counts. First, it assumes timing precision that even institutional algorithms cannot consistently deliver. Second, and more critically, it ignores the opportunity cost of waiting. While you are holding cash hoping for a microscopic price improvement to offset your broker’s fee structure, you are missing dividend accrual and the compounding effect of time in the market. You are not solving the friction problem. You are just delaying it while forfeiting yield.

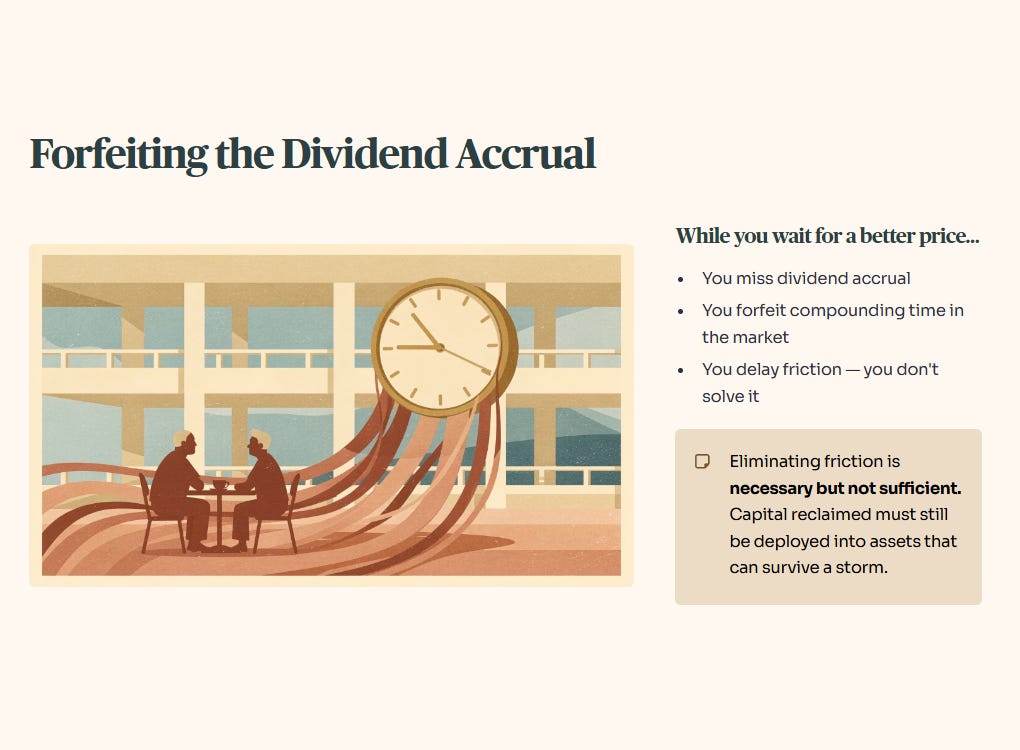

The Forensic Stress Test: Your Margin of Safety

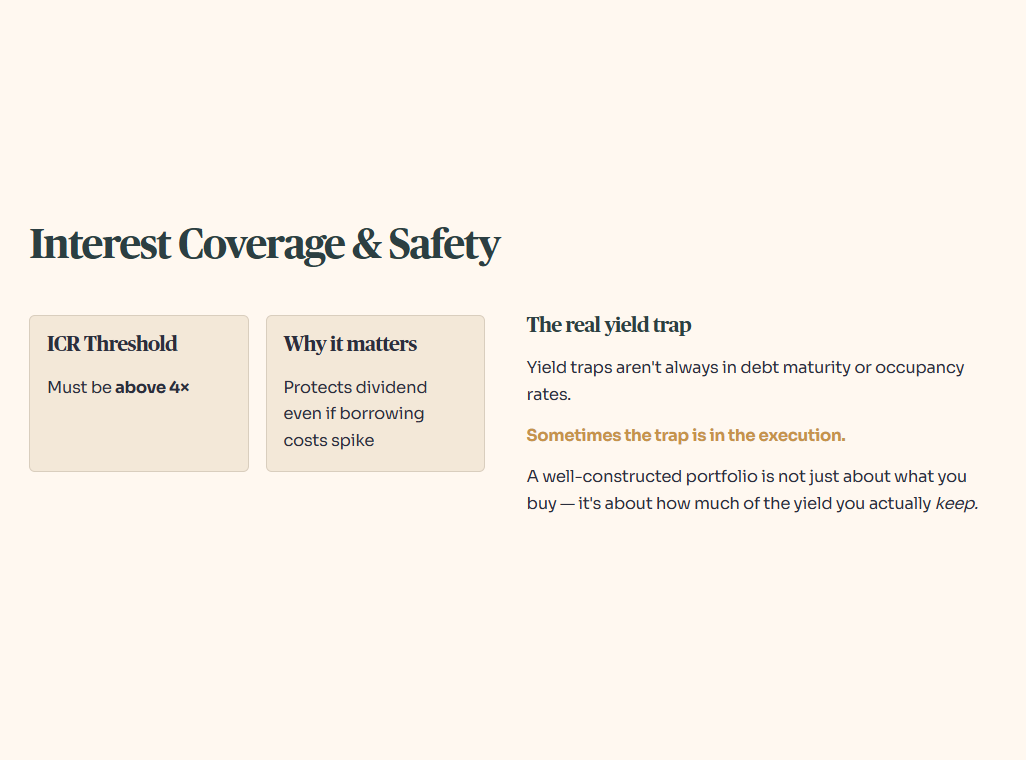

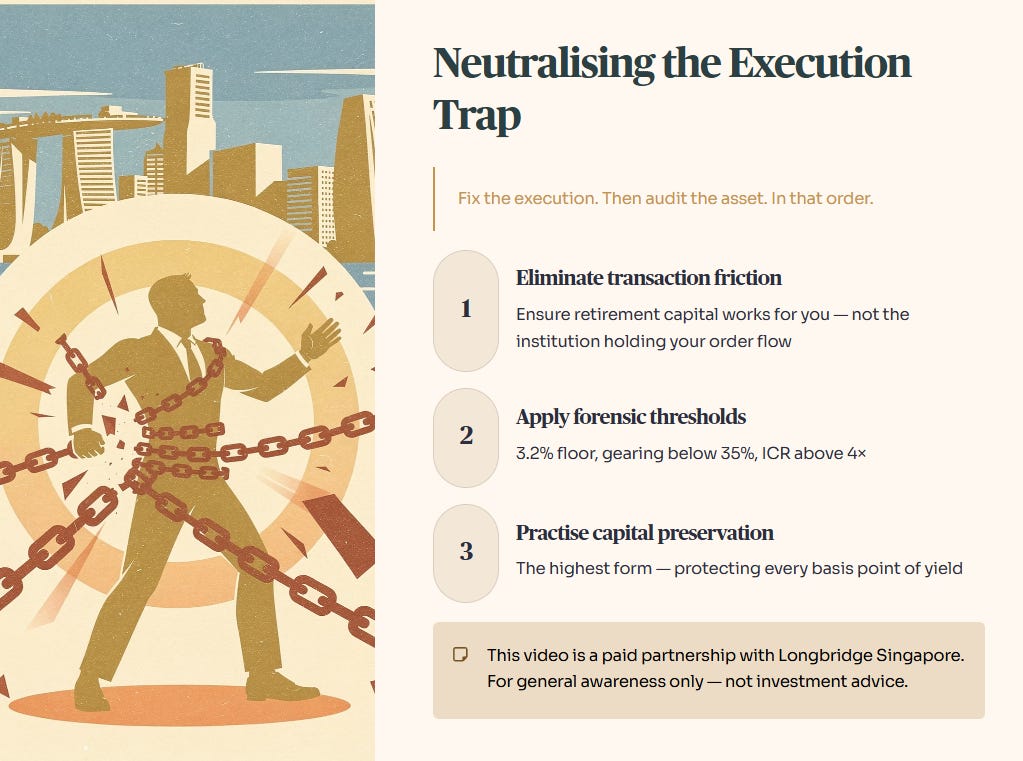

Eliminating transaction friction is necessary but not sufficient. The capital you’ve reclaimed still needs to be deployed into assets that can survive a storm. Every position must clear Iggy’s Forensic Thresholds before deployment.

The 3.2% Hurdle: We use a conservative 3.2% floor — the CPF OA rate — as our risk-free benchmark. If an asset cannot provide a yield spread of at least 150 basis points above this floor, the risk-to-reward ratio is insufficient.

The Gearing Ceiling: Gearing strictly below 35%. In a high-interest-rate environment, REITs hugging the 45% regulatory limit are not sanctuaries — they are leveraged liabilities.

The Interest Coverage Ratio: A healthy asset must have an ICR above 4x. This ensures that even if borrowing costs spike, the dividend remains protected.

Forensic Conclusion: Plugging the Leaks

Yield traps aren’t always found in a REIT’s debt maturity profile or occupancy rates. Sometimes the trap is in the execution.

A well-constructed portfolio isn’t just about what you buy. It is about how much of the yield you actually keep. By neutralising transaction friction, you are practising the highest form of capital preservation — ensuring that your retirement capital is working for you, not for the institution holding your order flow.

Fix the execution. Then audit the asset. In that order.

“Don’t rely on your memory alone. The market moves too fast for that.” .....

This 1-Page Cheat Sheet is your permanent reference guide. Whether you are analyzing a stock or reviewing your portfolio, run your thesis through this visual checklist first.

👇 Save the image or download the High-Res PDF below:

Iggy’s Forensic Compliance Standards — Standard Disclaimer

This content is produced for educational and informational purposes only. I am not a financial advisor — I am a retail investor who applies forensic analysis to my own portfolio and shares that process publicly. Nothing here constitutes a recommendation to buy, sell, or hold any security, and no specific target prices or personalised financial advice are offered. All data is sourced from public filings and verified sources; where data is unverified it is explicitly flagged. All investments carry risk, including the potential loss of principal, and past performance is not indicative of future results. If you are making investment decisions involving CPF, SRS, or personal capital, please conduct your own due diligence or consult a MAS-licensed financial adviser before committing funds.

IMPORTANT PARTNER DISCLOSURE

This content is a paid collaboration with Longbridge Singapore. It is intended for general awareness and does not constitute investment advice or a recommendation for any specific financial product.

Licensing Note: The presenter is not a licensed financial adviser. Views expressed are solely those of the presenter and do not necessarily reflect the position of Longbridge Singapore. Investments involve risk; you may lose your principal. This advertisement has not been reviewed by the Monetary Authority of Singapore. Always seek independent professional advice if unsure.

Where is your Long Bridge signup link?