Why "No Dividend" Labels Are Wrong (The IPO Data Trap)

Why Data Centers Are the New Gold Mine: The NTT DC REIT Case

1. The Hook: When a “Tech Powerhouse” Tenant Changes Everything

Data center REITs usually bore you. They are steady, predictable, and deliver yields like a government bond. But what happens when your largest tenant is not just any corporation—but a company racing to build an AI empire?

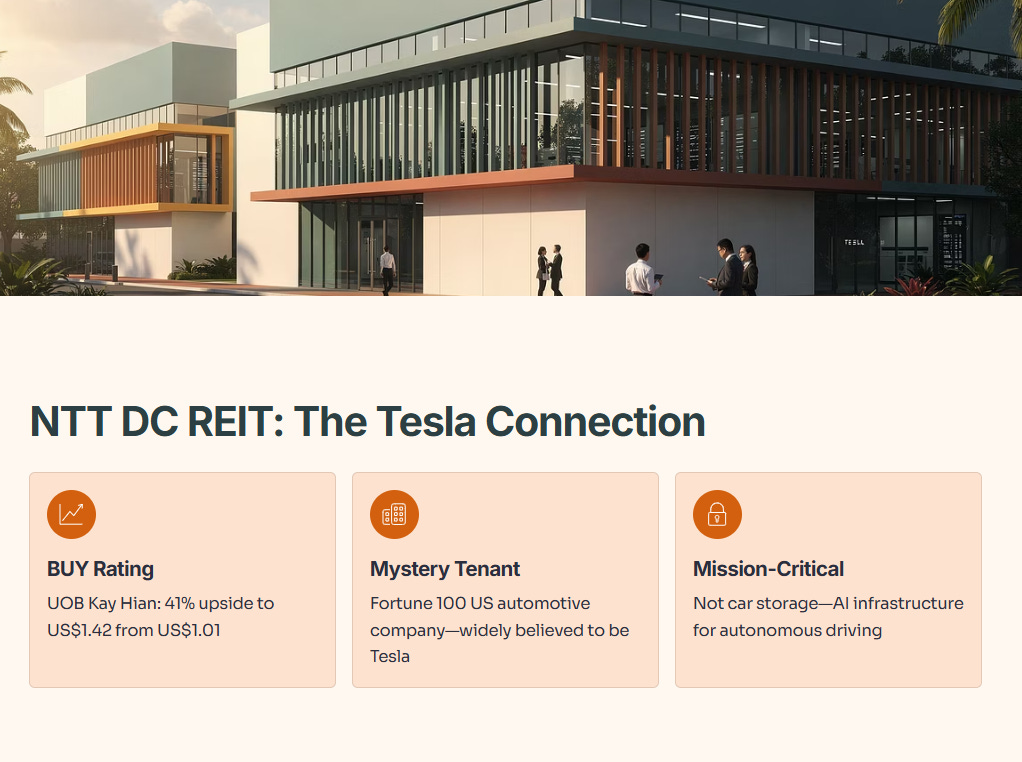

That’s the story of NTT DC REIT (SGX: NTDU), which just received a thundering BUY rating from UOB Kay Hian on January 8, 2026, with a 41% upside to US$1.42 per unit (as of 8 Jan 2026 UOB report) from the current price of US$1.01. The catalyst? A mysterious “Fortune 100 US automotive company” that is widely believed to be Tesla. And it is not just renting space for electric cars anymore.

Most investors see “tenant concentration” and run. I see “mission-critical leverage.” Let me explain why this trade is misunderstood.

In This Article:

• About Iggy the Investing Iguana channel

• The “Iggy Audit”: Is the Risk Real?

• The “InvestingPro” Data Check: Man vs. Machine

• The Verdict: The “Early Bird” Risk

• Constraints & Safety Rails (🚨 CRITICAL COMPLIANCE)🦎 About Iggy the Investing Iguana

Welcome to the Iguana Pit! If you’re new here, I’m Iggy: your guide through the dense jungle of the Singapore markets. My mission is simple: to spot the predators before they spot your portfolio.

We are now 5,800+ subscribers strong across YouTube and Substack, focusing purely on the data-driven alpha that mainstream media misses.

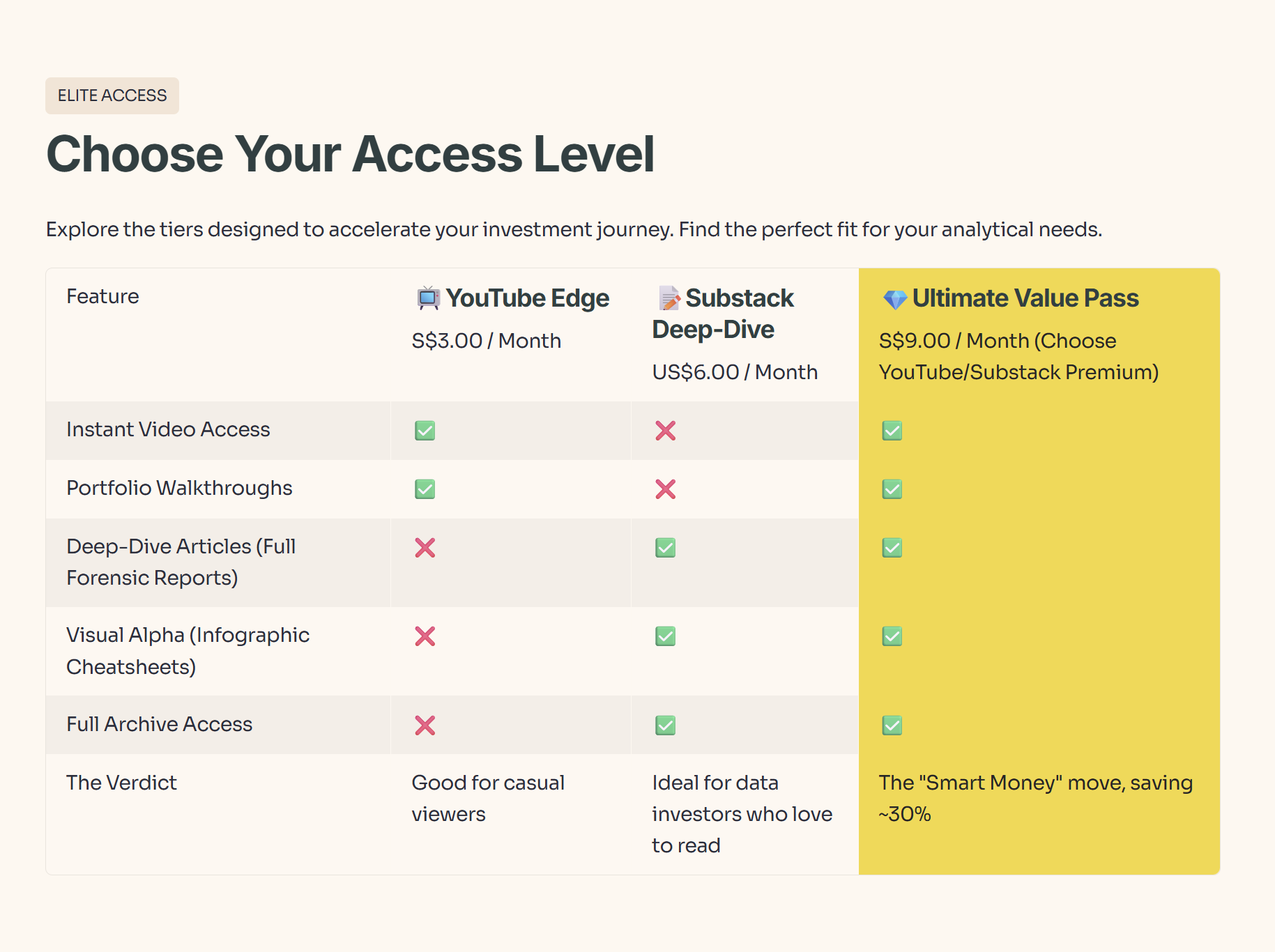

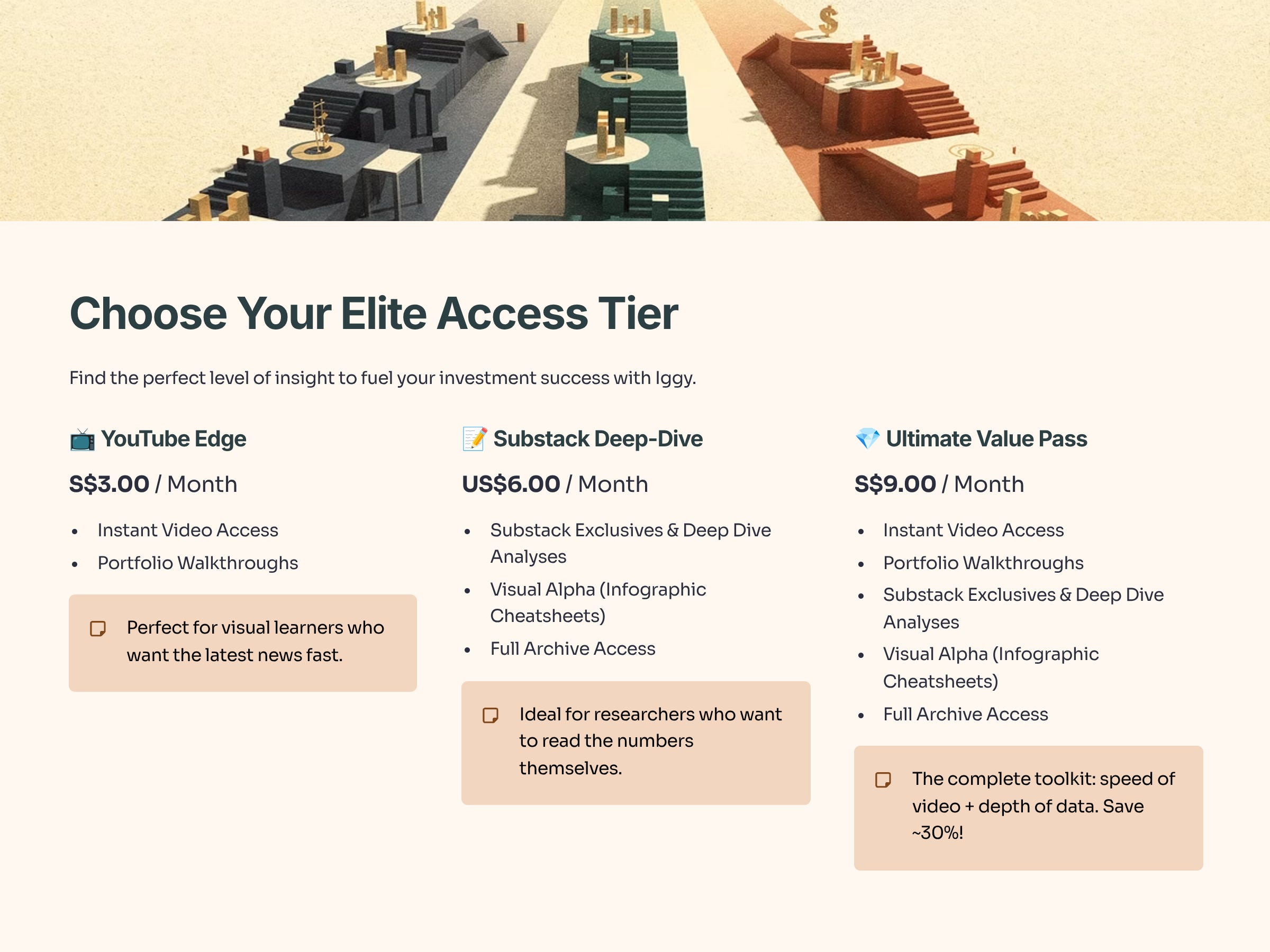

🚀 Join the “Elite 150” Inner Circle

Real alpha is found behind the velvet rope. Stop following the herd and start following the data with our 150+ paid members.

📺 The YouTube Edge (S$3/mo): Beat the Delay.

Instant Access: Watch new videos the moment they drop.

The Free Tier Trap: Free subscribers wait up to 14 days to see the same video. (By then, the news is old and the trade is gone).

📝 The Substack Deep-Dive (US$6/mo): Unlock the Vault.

Zero Paywalls: Read the full “Deep Dive” articles and “Substack Exclusive” articles found only on Substack.

Visual Alpha: Download exclusive Infographic Cheatsheets not available to free readers.

💎 The Ultimate Value Pass (S$9/mo): (BEST VALUE)

Get It All: Paid via YouTube, this bundle grants you Instant Video Access AND Full Substack Access.

The Math: You save ~30% compared to buying them separately. It’s the “Smart Money” move.

Why wait 2 weeks for old news? Get the data while it’s fresh. 👉 Join Here: https://www.youtube.com/@InvestingIguana/membership

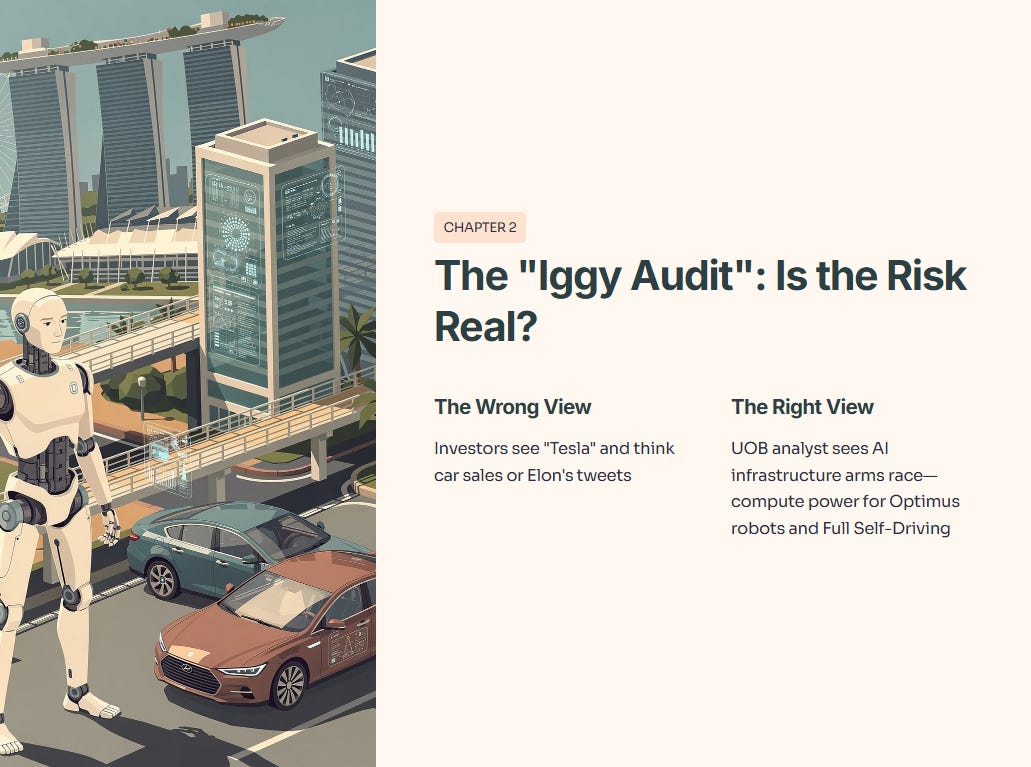

3. The “Iggy Audit”: Is the Risk Real?

Here is where most investors go wrong: they see “Tesla” and think about car sales or Elon’s latest tweet. But UOB Kay Hian analyst Jonathan Koh is looking at something far more important—the AI infrastructure arms race.

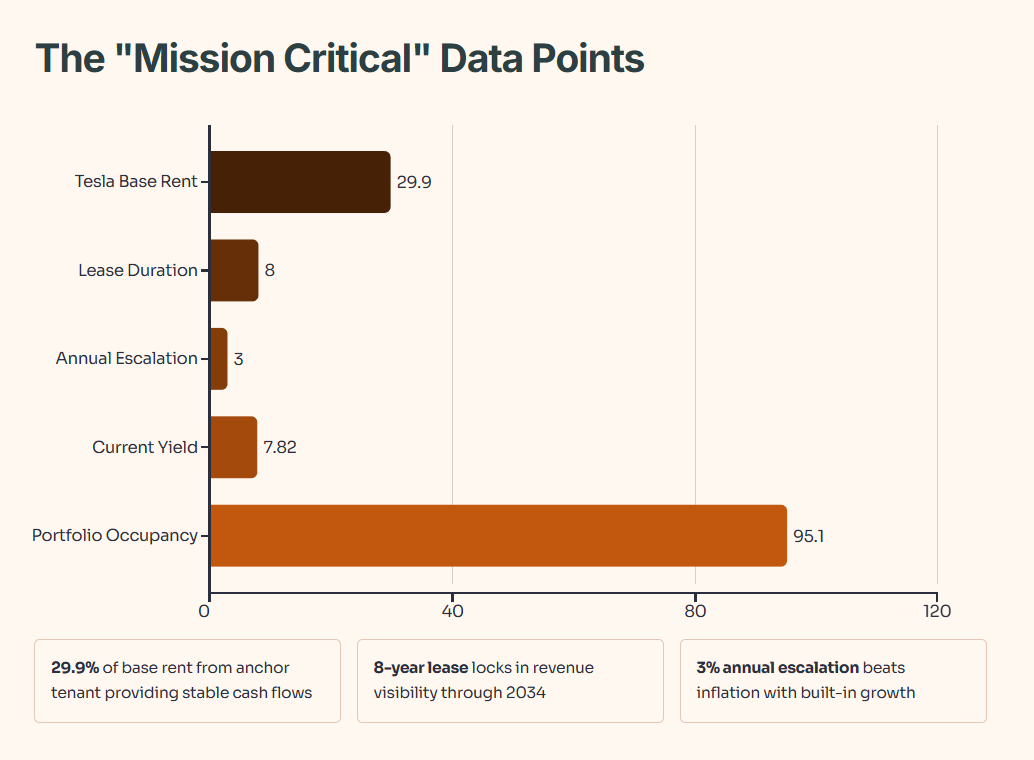

Tesla accounts for 29.9% of NTT DC REIT’s total base rent. That is a massive concentration. But here is the insight: this tenant has an 8-year lease with 3% annual rental escalation. In other words, NTT DC REIT doesn’t just get paid today—it is getting locked-in growth until 2034.

This isn’t storage space; it’s compute power for Optimus (humanoid robots) and FSD (Full Self-Driving).

The “Mission Critical” Data Points

💡 Iggy’s Insight:

The “Stickiness” Factor: Why won’t Tesla just leave? Because moving an AI training cluster is a logistical nightmare. The cost of downtime for autonomous driving algorithms is measured in millions per hour. “Mission-critical” means the tenant is hostage to the location. That is your safety margin.

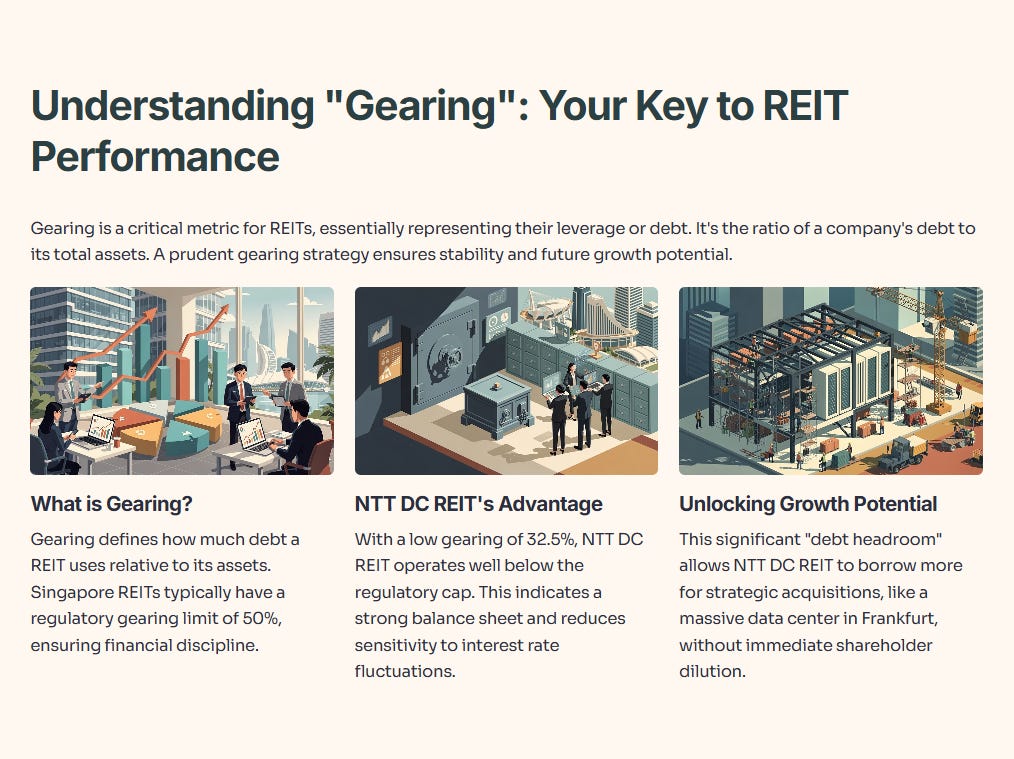

Gearing, Debt Headroom and Your Income

Before going further, it helps to understand gearing. In REIT language, gearing is just the ratio of debt to total assets. For Singapore REITs, the regulatory cap is usually around 50%, and NTT DC REIT is sitting at roughly 32.5%. That means there is still plenty of “debt headroom” to fund growth before hitting any red lines.

Why does this matter for you? Lower gearing means the REIT is less fragile when interest rates move and still has firepower to borrow for acquisitions like the Frankfurt data center without immediately turning to shareholders for a dilutive cash call. In simple terms, more room to grow the asset base, while keeping the structure within safe limits.

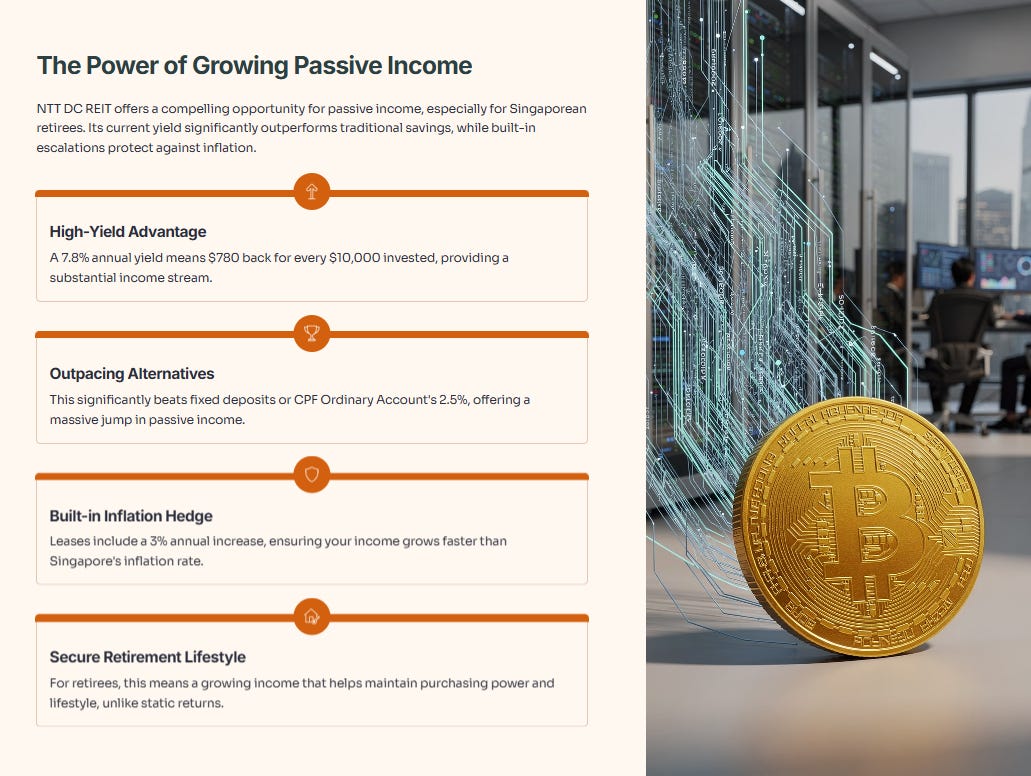

At the same time, the projected yield is about 7.8%. For every S$10,000 you put into this counter, that is roughly S$780 a year in distributions if the payout holds. Compare that with a 2.5% CPF Ordinary Account rate or a typical fixed deposit, and you can see the jump in cash flow.

Now layer in rental escalation. NTT DC REIT’s key leases are structured with about 3% annual rental step-ups built in, which means your income is not just high today—it is designed to rise over time. In a world where kopi, chicken rice and utilities keep creeping up, that difference between a flat 2–3% and a growing 7–8% can decide whether your retirement income falls behind inflation or keeps your lifestyle intact.

The Tesla Risk, WALE and “Bond-Like” Income

Tesla currently contributes about 29.9% of NTT DC REIT’s base rent, which looks scary on paper. For a conservative income investor, losing a tenant like that would feel like a disaster.

This is where WALE comes in. WALE, or Weighted Average Lease Expiry, tells you how long, on average, tenants are locked in. For Tesla, the WALE is roughly eight years, which means they are contracted to pay rent until around 2034. In practice, that makes your income stream feel a lot closer to a long-term bond than a short-term trading bet.

The bullish camp goes even further. They argue that Tesla is not just renting storage space; it is renting the “brains” needed to power autonomous driving and Optimus robots. If that AI vision plays out, demand for compute could grow faster than the REIT’s current footprint, and Tesla’s presence becomes a growth engine rather than a risk factor.

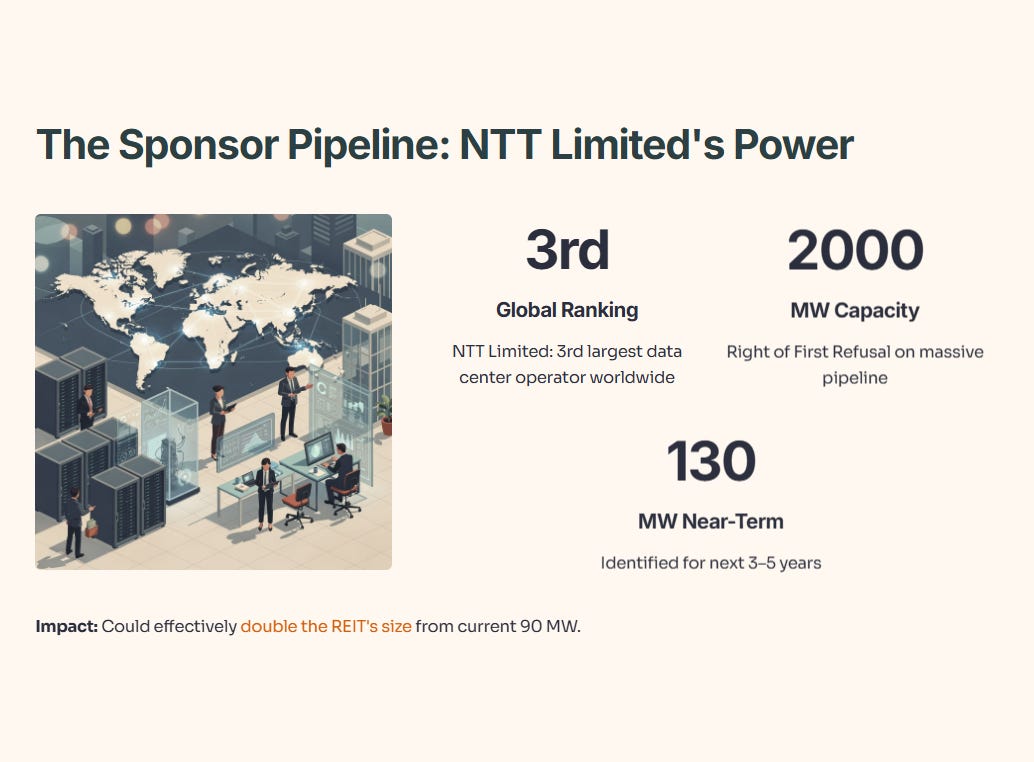

On top of that, the sponsor, NTT Limited, remains a key upside lever. As the third-largest data centre operator globally with a multi‑gigawatt pipeline and a Right of First Refusal arrangement, it gives NTT DC REIT a long runway to scale beyond its current base, even if Tesla eventually becomes a smaller percentage of the rent roll.

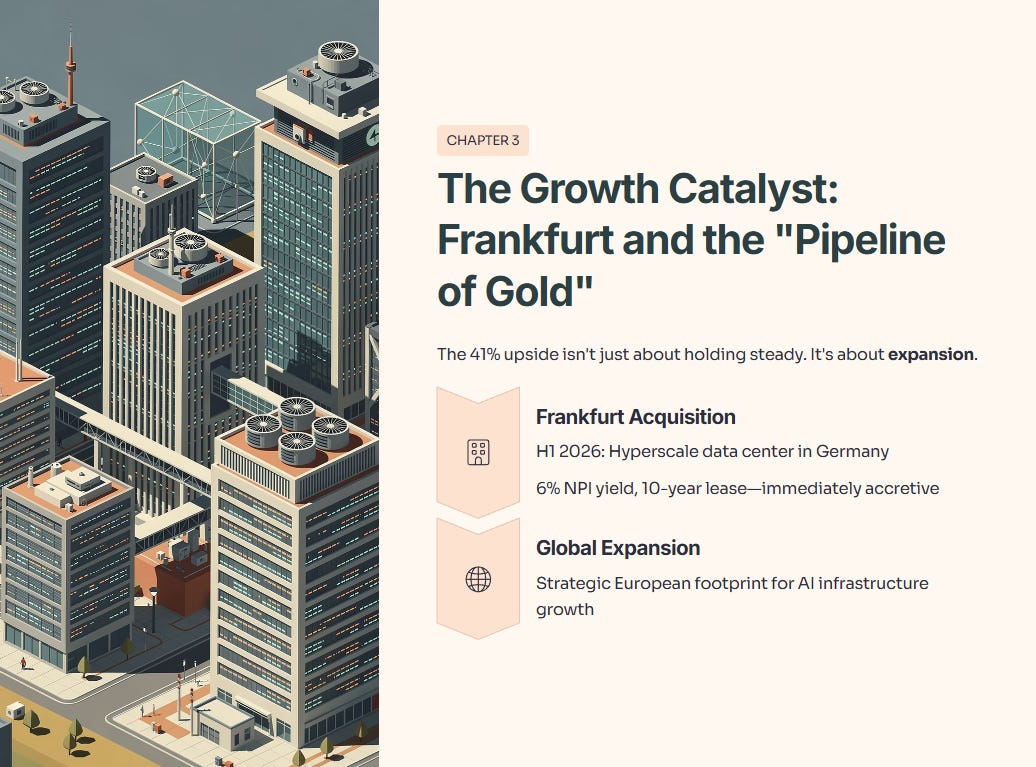

The Growth Catalyst: Frankfurt and the “Pipeline of Gold”

The 41% upside isn’t just about holding steady. It’s about expansion.

Frankfurt Acquisition (H1 2026): NTT DC REIT is evaluating a hyperscale data center in Germany with a 6% NPI yield and a 10-year lease. This is immediately accretive.

The Sponsor Pipeline: The sponsor, NTT Limited, is the 3rd largest data center operator globally. They have granted the REIT a Right of First Refusal (ROFR) on 2,000 MW of capacity.

Near-term Target: 130 MW identified for the next 3–5 years.

Impact: This could effectively double the REIT’s size from its current 90 MW.

💡 Iggy’s Insight:

The “Sponsor” Moat: In the REIT world, a weak sponsor kills you (remember Eagle Hospitality?). A strong sponsor saves you. NTT Limited has deep pockets and a massive pipeline. They need this REIT to succeed so they can recycle capital. You are riding on their coattails.

4. The “InvestingPro” Data Check: Man vs. Machine

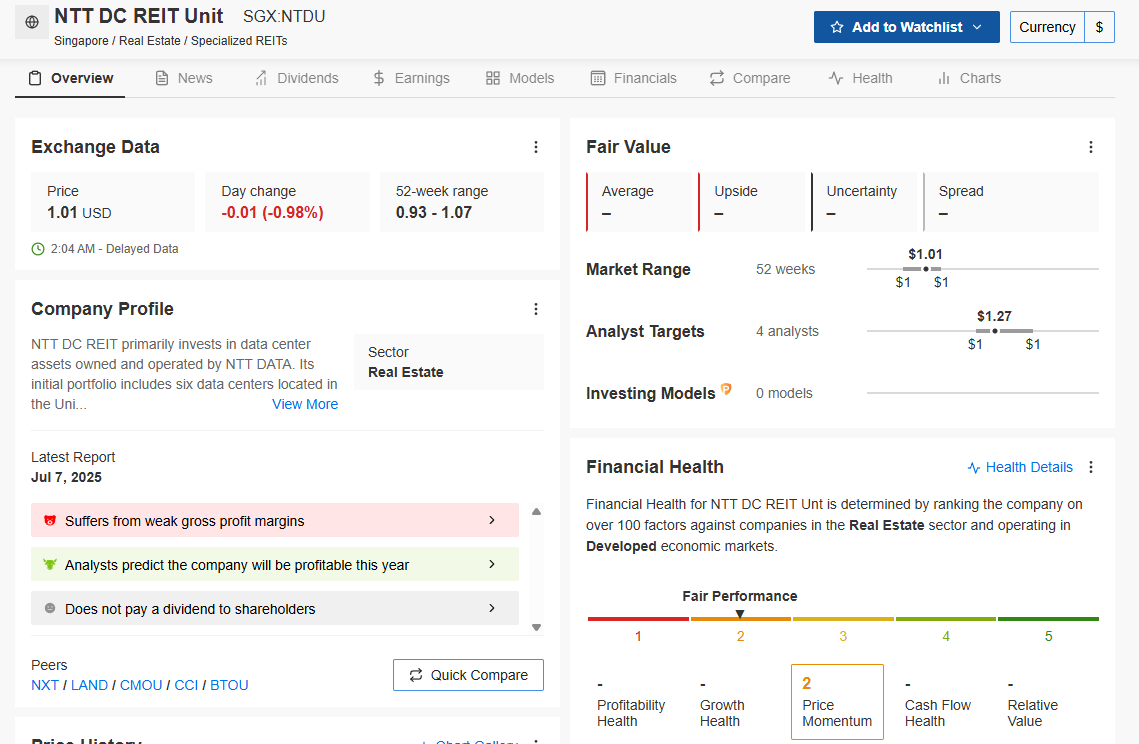

I don’t guess at valuations. I usually let the InvestingPro algorithms run the numbers to remove human bias. But when I ran the audit on NTT DC REIT today, the “machine” gave me a warning sign you need to see.

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

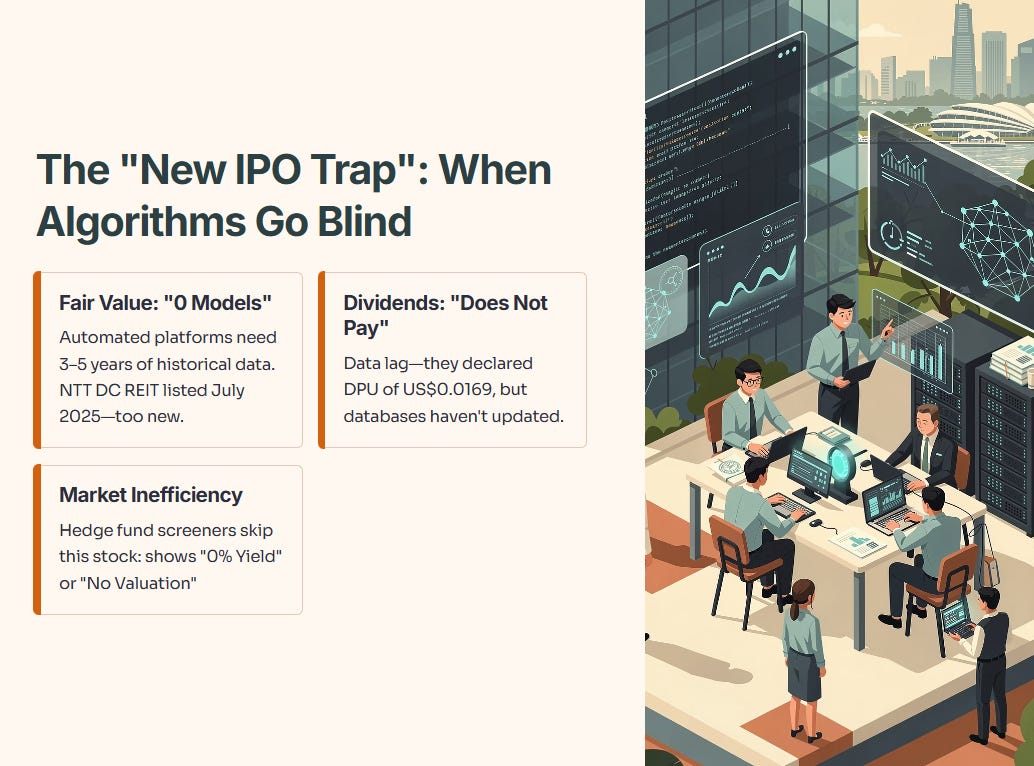

The “Blind Spot” Insight: Look closely at the Fair Value section. It says “0 Models.” Look at the Dividends section. It says “Does not pay a dividend.”

Is the data broken? No. It’s a “New IPO Trap.” Automated platforms like InvestingPro require 3–5 years of historical cash flows to build reliable DCF (Discounted Cash Flow) models. Since NTT DC REIT listed recently (July 2025), the algorithms are flying blind. They literally do not have enough data points to calculate a Fair Value yet.