Why I’m Ignoring the ATH “Sell” Signal (The Iggy Verdict)

While holding 40% cash at record highs feels like prudent risk management, the data shows it’s actually a ticking time bomb for your wealth. Here is the 60/40 deployment strategy I’m using.

If You’re New Here, Welcome

I’m Iggy, your Singapore-based market analyst. Since October 2025, we’ve produced over 1,300 videos and 400 articles with 1.1 million watch hours. We are also home to a growing community of over 70 YouTube Premium subscribers and 30 paid Substack members.

The “Smart Money” Move: Why YouTube Premium is the Strategic Choice

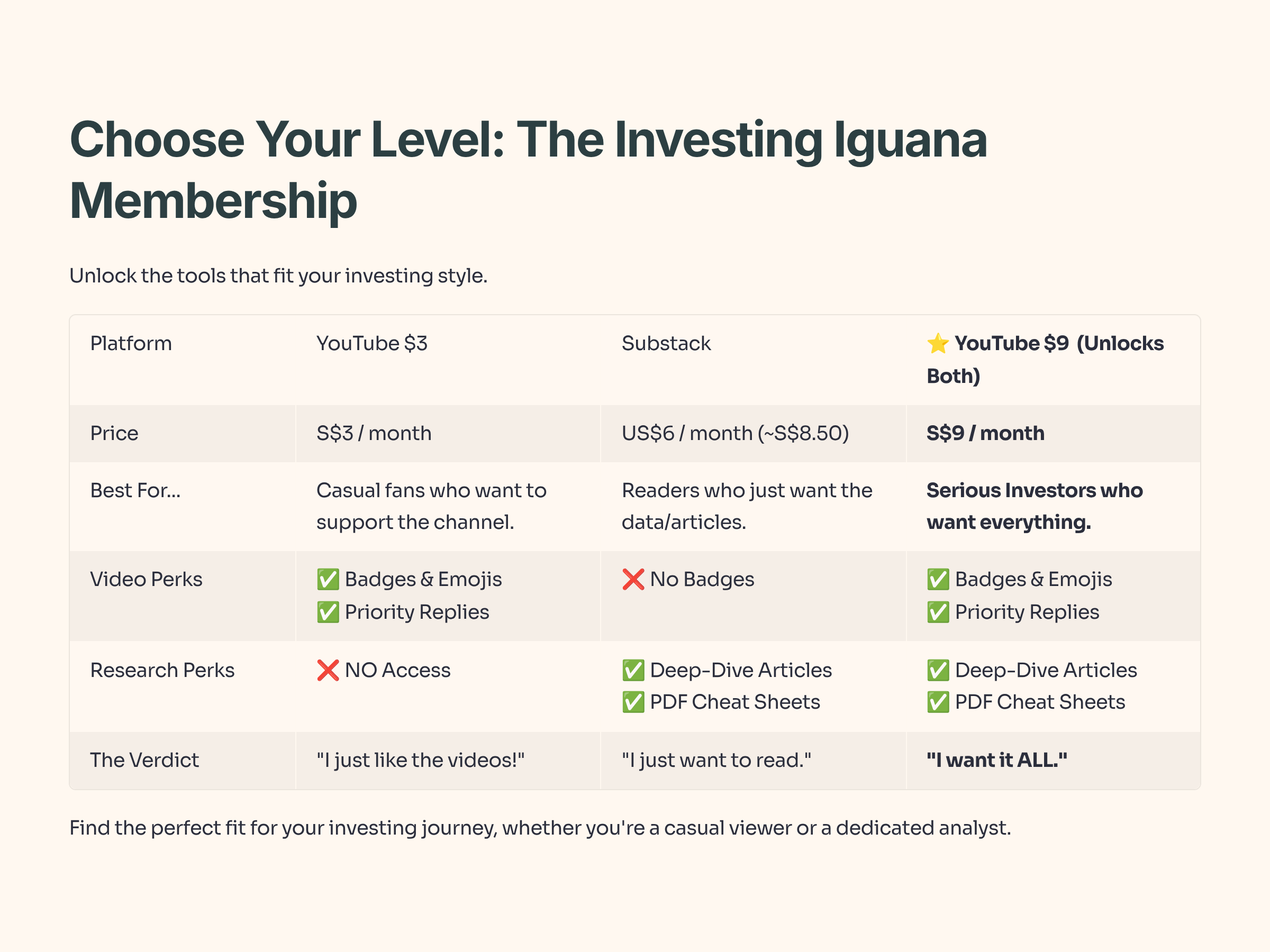

Quick Housekeeping: I often get asked why we maintain both a Substack and a YouTube Premium channel. Here is the breakdown for those who want to optimize their investment in financial literacy.

While a standalone Substack subscription (US$6/mth) gives you full access to these long-form deep dives, the YouTube Premium Membership (S$9/mth) is the clear “Alpha” move for the serious investor.

By choosing the YouTube bundle, you are essentially getting a 33% discount on the following premium deliverables:

Iggy’s Take: If you are serious about capital preservation and yield optimization, the S$3 difference is negligible. YouTube Premium members get the Downloadable Infographic Reports—these are high-density, visual summaries of the exact models I use to calculate “Safe Harbor” entry points. For less than the cost of a Laksa in the CBD, you get the full analytical toolkit to stop guessing and start growing.

Quick Housekeeping: Substack alone is US$6, so the bundle is the “smart money” move. Now, let’s get to the numbers.

In This Article:

• The Invisible Cost of “Waiting for the Dip”

• Lump Sum vs. DCA—The 68% Rule

• The “Safe Harbor” Play—Where to Park Your Powder

• InvestingPro Reality Check

• The “Investor’s Playbook”—Actionable Steps

• Iggy’s Strategic Summary

Section 1: The Invisible Cost of “Waiting for the Dip”

Most investors in Singapore and Malaysia—especially those approaching retirement—are currently paralyzed by “All-Time High (ATH) Phobia.” The logic seems sound: the market is expensive, a correction must be coming, so I will wait in cash.

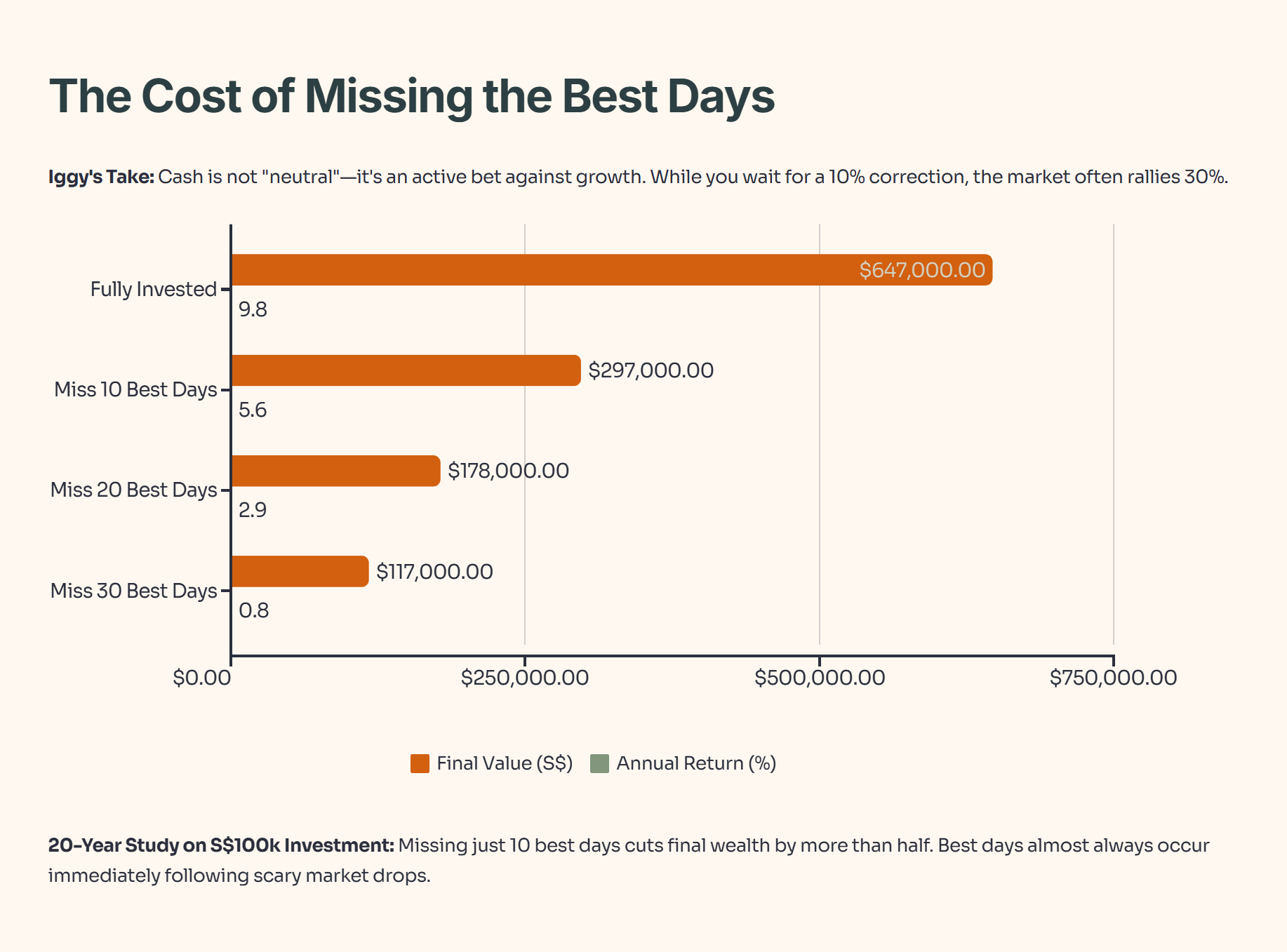

However, history is a brutal teacher. During the 2013 Taper Tantrum, investors who fled to cash to “avoid the crash” missed a decade-long bull run that would have quadrupled a S$100,000 investment. By the time the “dip” finally arrived, the discounted price was still significantly higher than the price they originally refused to pay.

Iggy’s Take: Cash is not a “neutral” position; it is an active bet against global growth. While you wait for a 10% correction, the market often rallies 30%. You are paying a massive “opportunity tax” for the illusion of safety.

Iggy’s Insight: Notice that missing just the 10 best days—which almost always occur immediately following a “scary” market drop—cuts your final wealth by more than half. If you aren’t in the market during the panic, you won’t be there for the recovery.

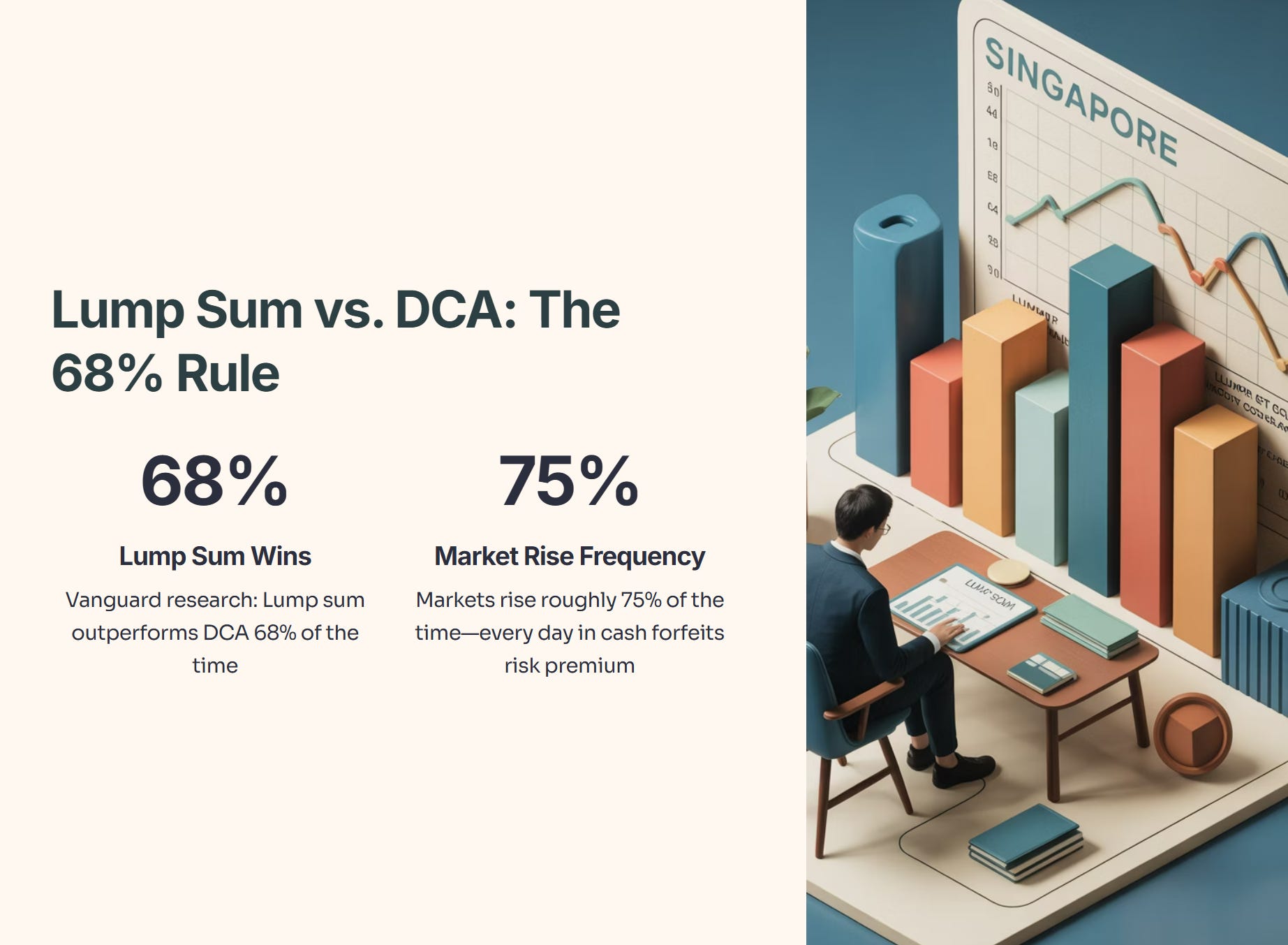

Section 2: Lump Sum vs. DCA—The 68% Rule

Once you accept that cash is a losing strategy, the next hurdle is how to enter. Should you throw it all in (Lump Sum) or trickle it in (Dollar Cost Averaging)?

Vanguard’s research is definitive: Lump sum investing outperforms DCA 68% of the time, even when markets are at all-time highs. This is because markets rise roughly 75% of the time; every day you sit in cash, you forfeit the “risk premium” the market pays you for being exposed to equity risk.

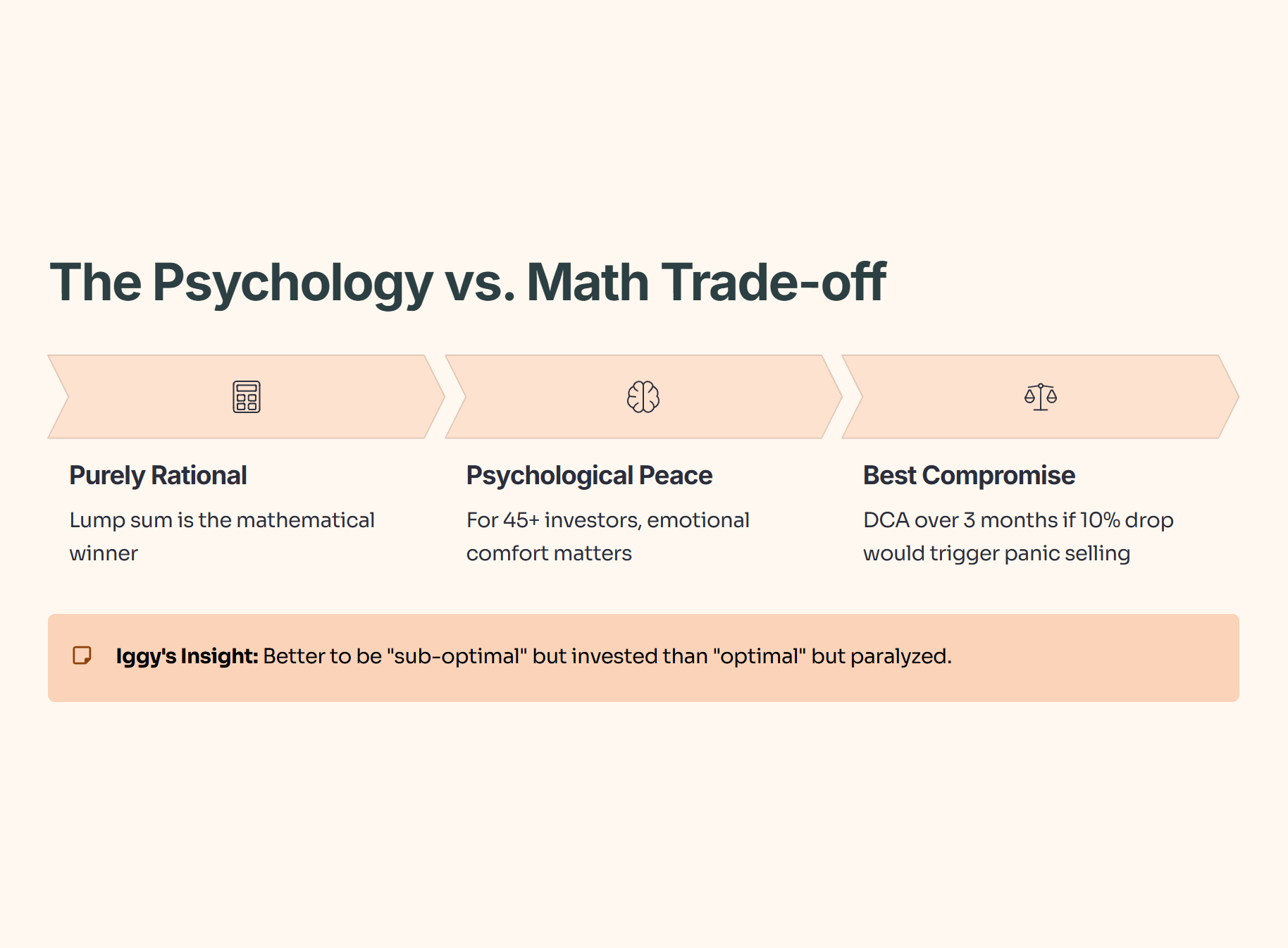

Iggy’s Insight: If you are a purely rational math-driven investor, Lump Sum is the winner. However, for my 45+ audience, psychological peace matters. If a 10% drop next week would make you sell in a panic, then DCA over 3 months is your best compromise. It’s better to be “sub-optimal” but invested than “optimal” but paralyzed.

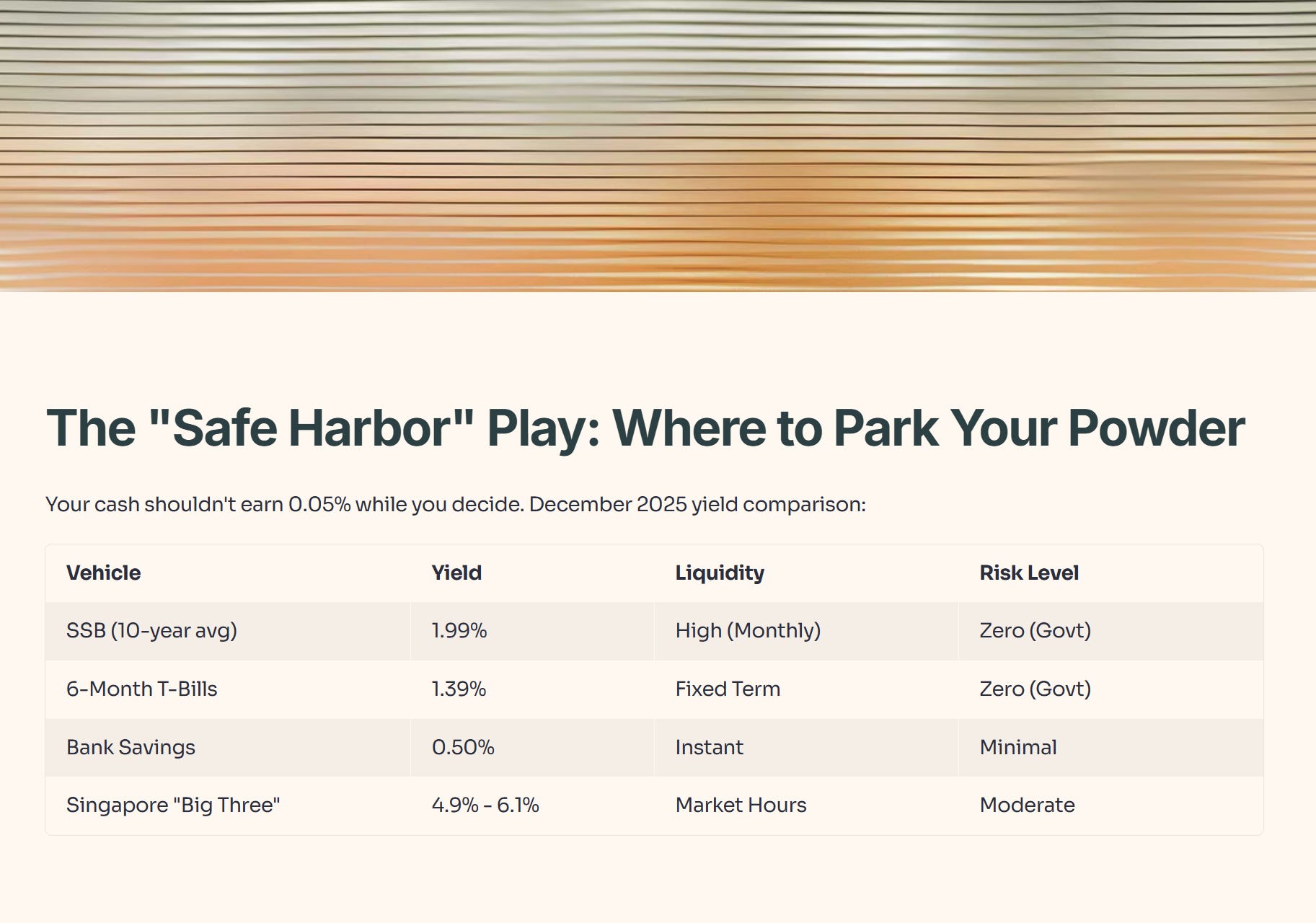

Section 3: The “Safe Harbor” Play—Where to Park Your Powder

While you decide on your deployment speed, your cash shouldn’t be sitting in a standard savings account earning 0.05%. In December 2025, the Singaporean investor has unique vehicles to bridge the gap.

December 2025 Yield Comparison

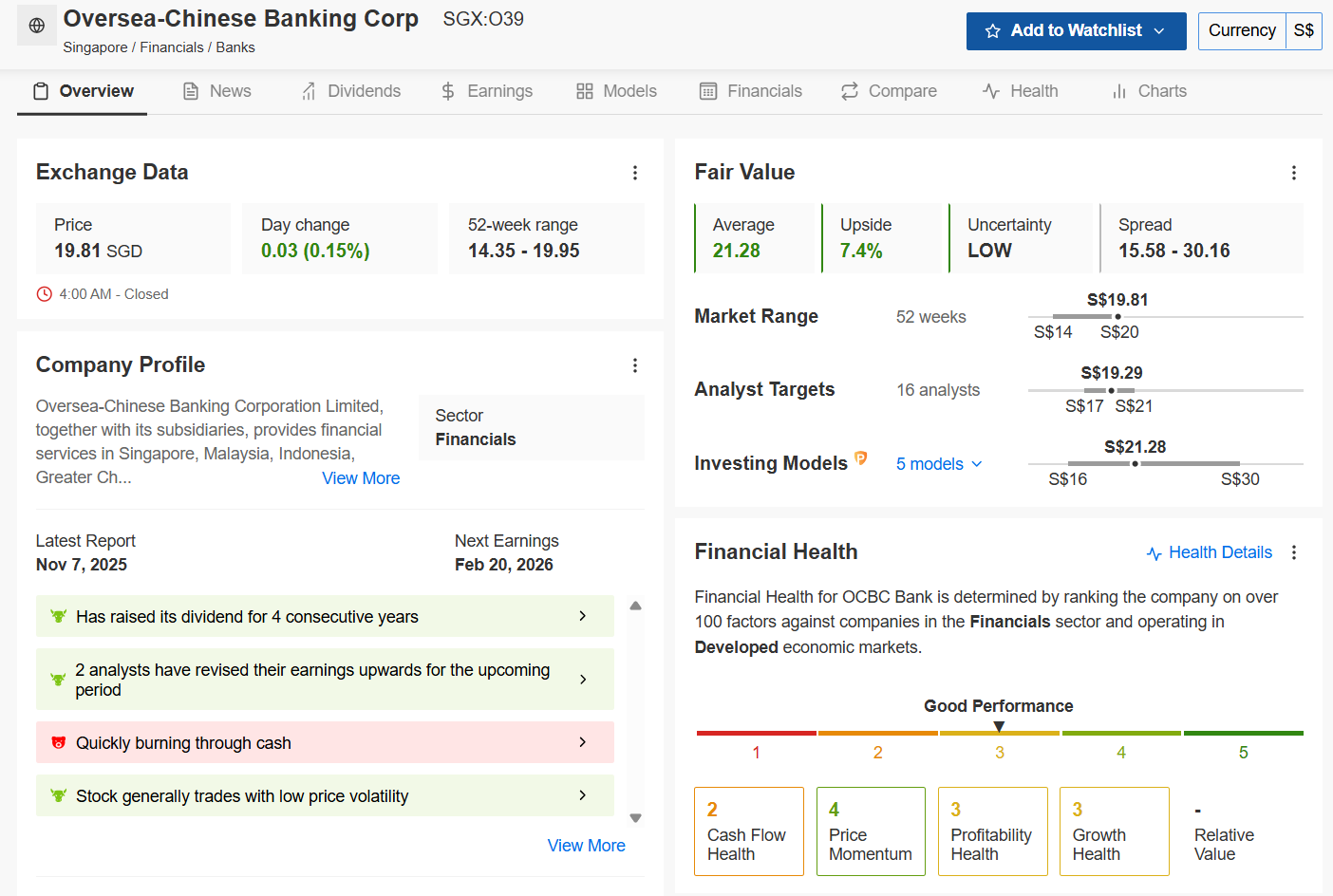

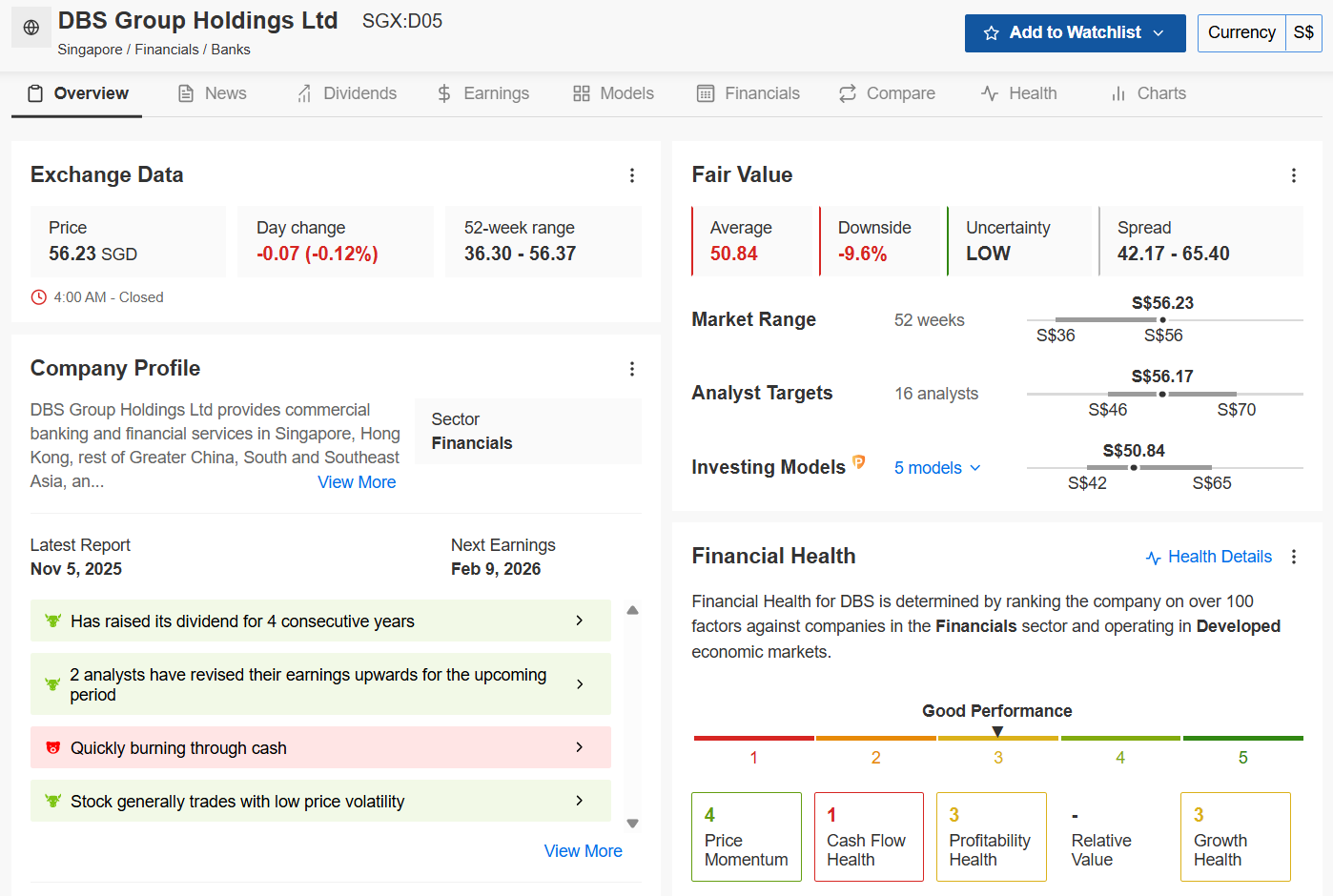

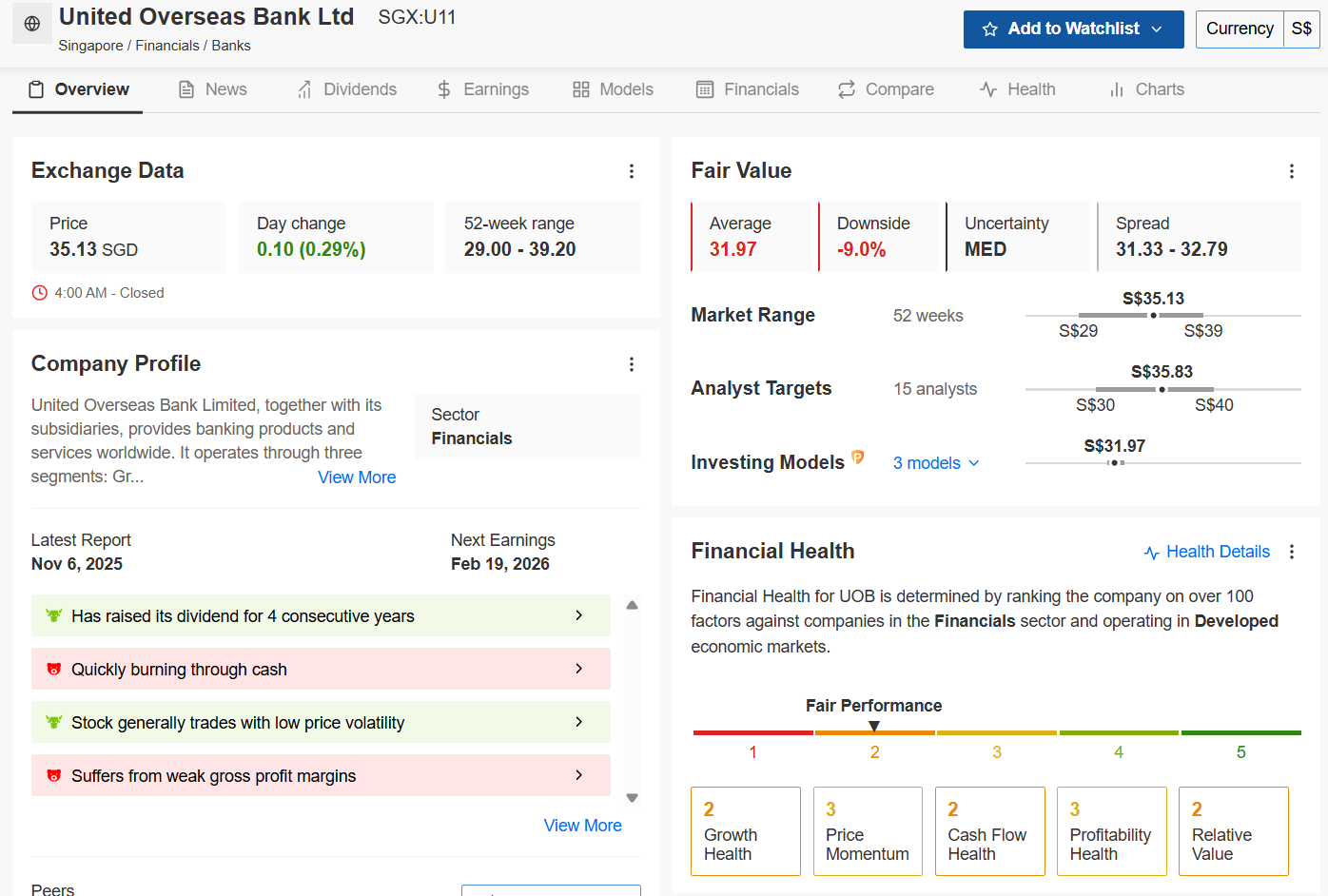

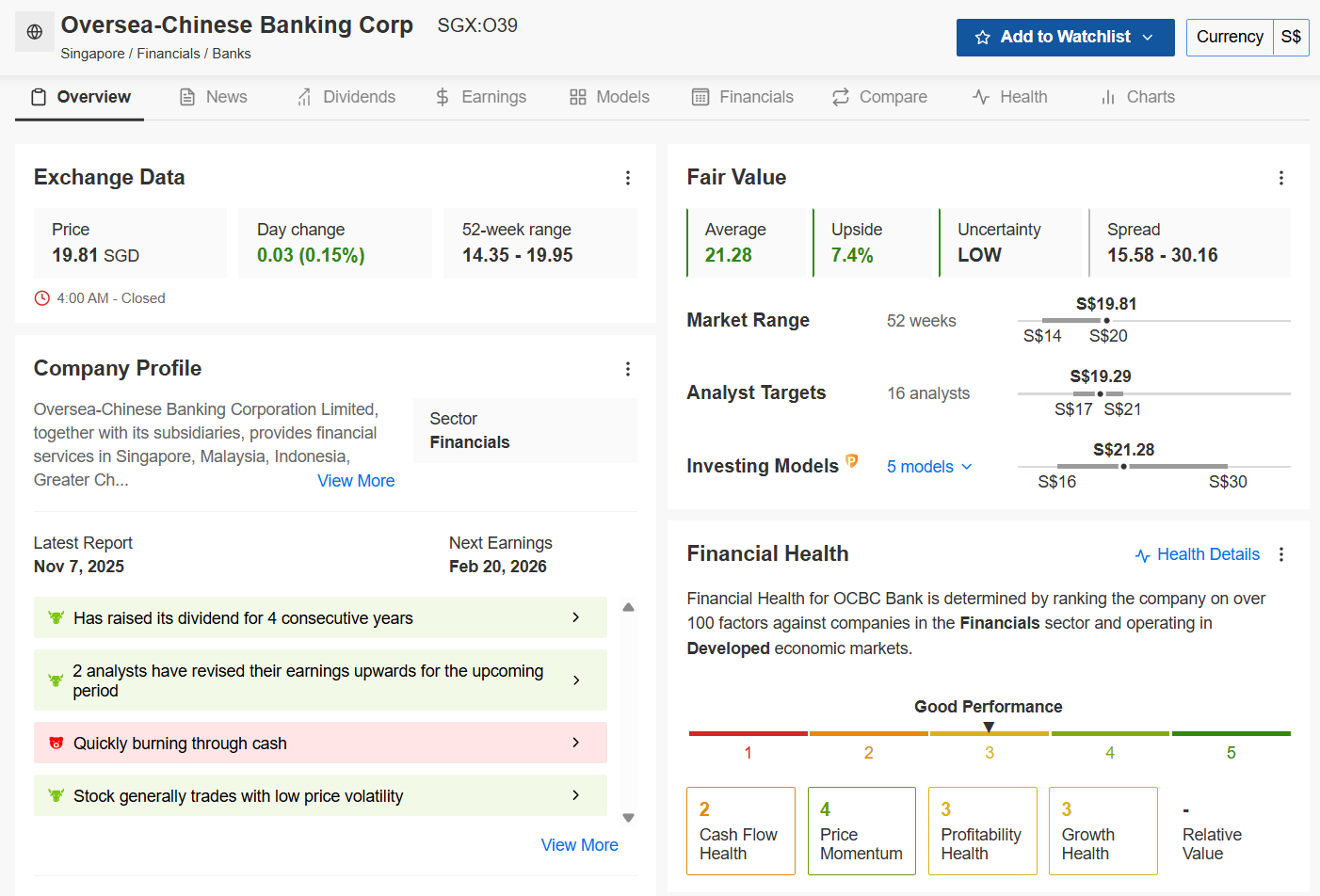

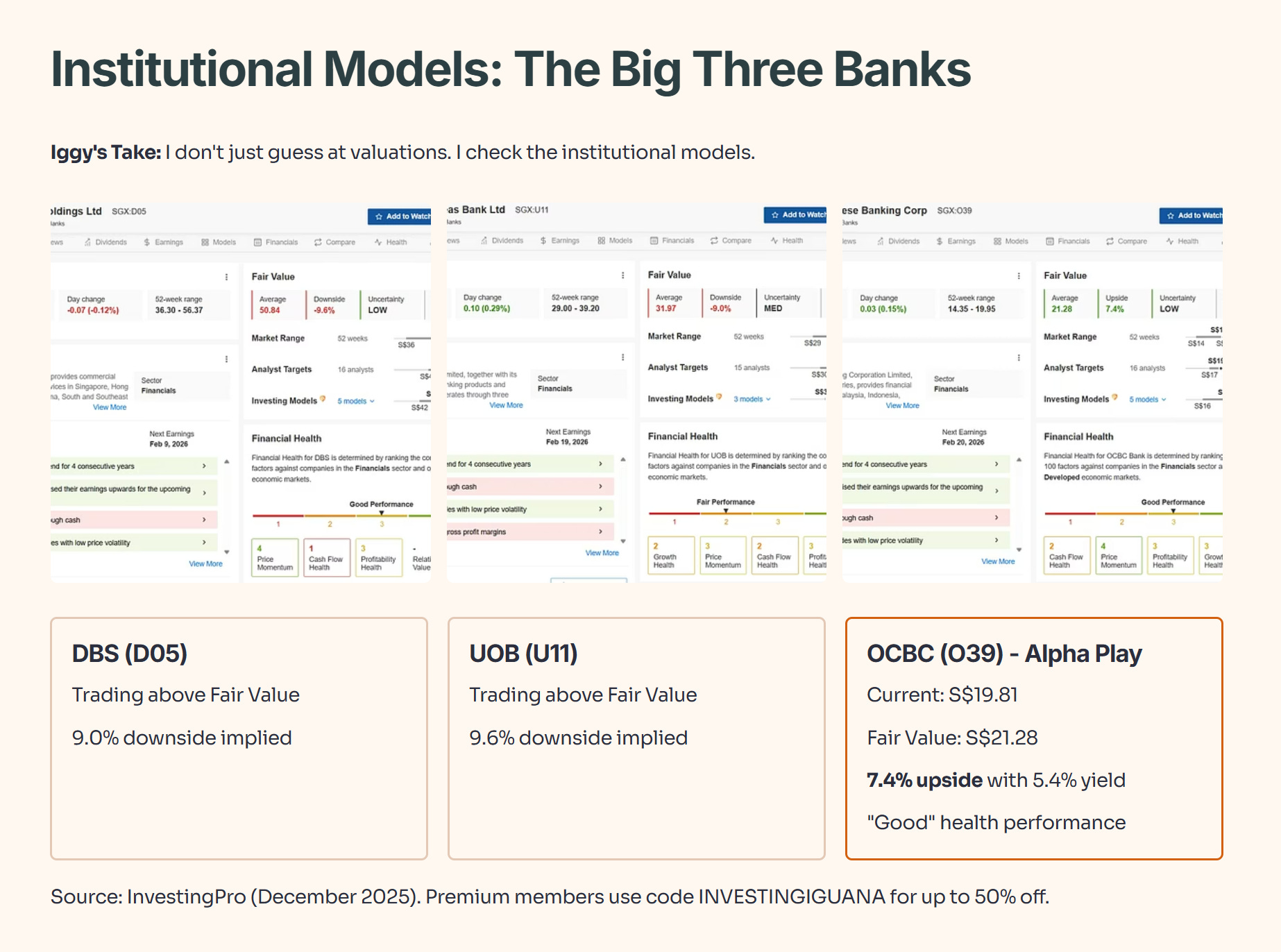

Iggy’s Take: I don’t just guess at valuations. I check the institutional models.

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

The data currently shows a fascinating divergence. While DBS (D05) and UOB (U11) are trading above their InvestingPro Fair Value (implying a 9.0% to 9.6% downside), OCBC (O39) remains the “Alpha” play. It is currently trading at S$19.81, showing a **7.4% upside** to its Fair Value of S$21.28 with a “Good” health performance.

Section 4: The “Investor’s Playbook”—Actionable Steps