Stuck at 2.5%? How to Double Your Yield with 3 S-REITs Poised for Growth

As interest rates fall, a new opportunity is emerging for savvy investors. We identify the three S-REITs with the financial strength to turn lower borrowing costs into growing cash distributions...

Editor’s Note: This post has been updated on October 19, 2025, to ensure it is fresh and accurate, and now includes the latest analysis on the impact of falling interest rates on S-REIT dividend growth.

If you’ve been watching your CPF Ordinary Account earn a steady 2.5% while Singapore REITs quietly climb back to 5-6% yields, you’re probably wondering what changed. The answer is simple: interest rates are falling, and three specific S-REITs are positioned to ride this wave straight into 2026 with growing dividends. This isn’t about chasing hot tips—it’s about understanding which REITs have the operational strength, portfolio quality, and financial discipline to turn rate cuts into real cash distributions for investors.

The Singapore REIT sector rebounded 9% since July 2025 as the interest rate environment shifted dramatically. The 10-year Singapore government bond yield dropped from 2.92% at the start of 2025 to just 1.77% by September. With economists expecting another 125 basis points in Fed rate cuts between September 2025 and March 2026, the math is getting interesting for REIT investors. Lower borrowing costs mean higher distribution per unit growth, and three REITs stand out as prime beneficiaries.

For our Singaporean readers, this is the CPF question. For our Malaysian friends, the same logic applies when comparing high-yield S-REITs against your EPF guaranteed dividend.” This small nod keeps them engaged and validates their readership

In This Article:

• The CPF Question: Should You Consider REITs?

• Why Interest Rates Matter More Than You Think

• The Three S-REITs Ready to Deliver

• CICT: Singapore’s Commercial Property Champion

• FCT: The Suburban Retail Fortress

• MLT: The High-Yield Recovery Play

• The Sector Picture: Who Wins in 2026

• What Makes 2026 Different

• The Risks You Need to Know

• How to Position Your Portfolio

• The Verdict: Buy, But Stay SelectiveThe CPF Question: Should You Consider REITs?

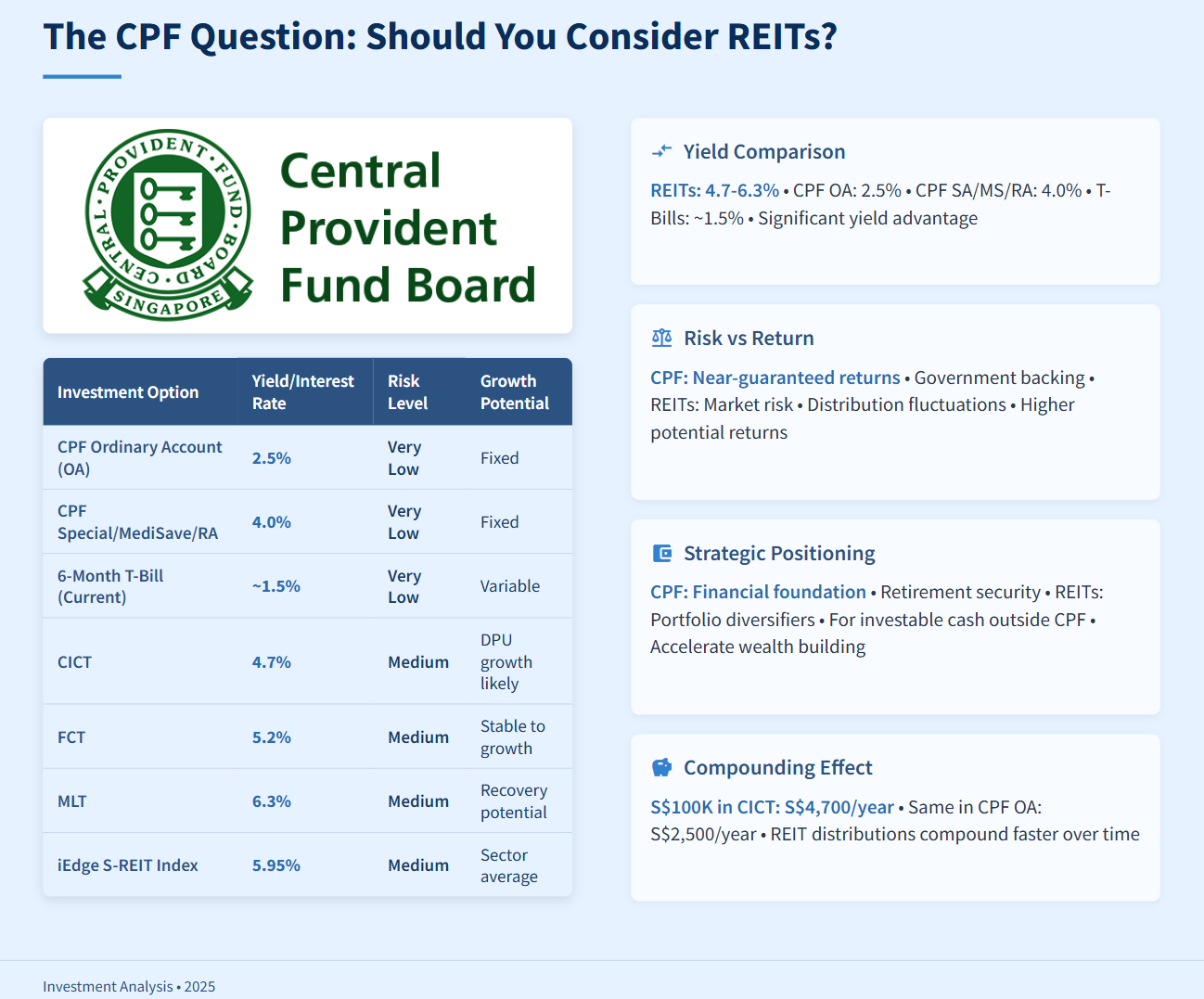

Let’s address the elephant in the room. Your CPF Ordinary Account earns 2.5% annually. Your CPF Special, MediSave, and Retirement Accounts earn 4% through 2026 thanks to the government’s extended floor rate. Meanwhile, the three REITs discussed here yield between 4.7% and 6.3%.

TABLE 1: CPF Rates vs S-REIT Dividend Yields - Where Should Your Money Work?

The math shows REITs offering significantly higher yields than CPF accounts or T-bills. But this comparison requires context. CPF provides near-guaranteed returns with government backing. REITs carry market risk, and distributions can fluctuate.

The key insight: REITs aren’t CPF replacements—they’re portfolio diversifiers for your investable cash outside CPF. If you have savings earning low interest rates in regular bank accounts, or if you’ve already maxed out your CPF contributions and want to grow your wealth faster, REITs present a compelling option.

CPF should form your financial foundation. The guaranteed 4% on Special, MediSave, and Retirement Accounts is excellent for retirement security. But once you have adequate CPF savings and emergency funds, deploying additional capital into quality REITs can accelerate wealth building through higher yields and potential capital appreciation.

For example, a S$100,000 investment in CICT yielding 4.7% generates S$4,700 in annual distributions. The same amount in a CPF OA earns S$2,500. Over 20 years, assuming stable yields and reinvested distributions, the REIT investment compounds significantly faster.

The risk trade-off involves market volatility and operational performance. CICT’s unit price can fluctuate with market sentiment, interest rate expectations, and property market conditions. But if you hold for the long term and the REIT maintains its distributions, you collect those higher yields year after year.

Why Interest Rates Matter More Than You Think

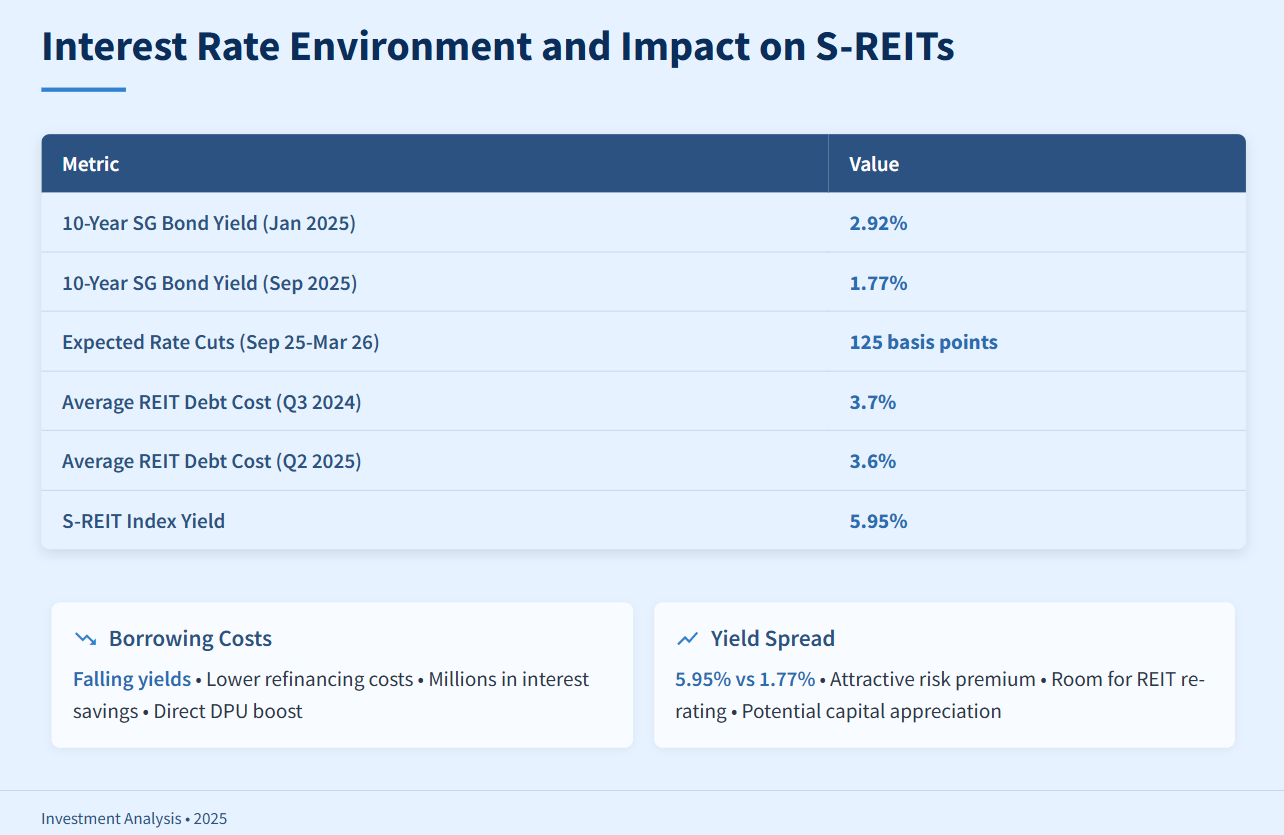

REITs live and die by their cost of capital. Think of it this way: when a REIT borrows money at 4% to buy properties that earn 6% in rental yield, the spread creates value. But when rates spike and borrowing costs hit 5%, that spread shrinks fast. The past two years hammered S-REITs precisely because of this dynamic.

Now the tide is turning. The average S-REIT debt cost already fell from 3.7% in Q3 2024 to 3.6% in Q2 2025. That might sound like a tiny drop, but multiply it across billions in debt, and you’re talking about millions in annual interest savings flowing straight into distributions.

TABLE 2: Interest Rate Environment and Impact on S-REITs

The data shows a clear downward trend in borrowing costs. As older high-cost debt gets refinanced at today’s lower rates, the savings compound quickly. REITs with significant refinancing activity in 2025 and 2026 will see the biggest boost to their distribution per unit.

The Three S-REITs Ready to Deliver

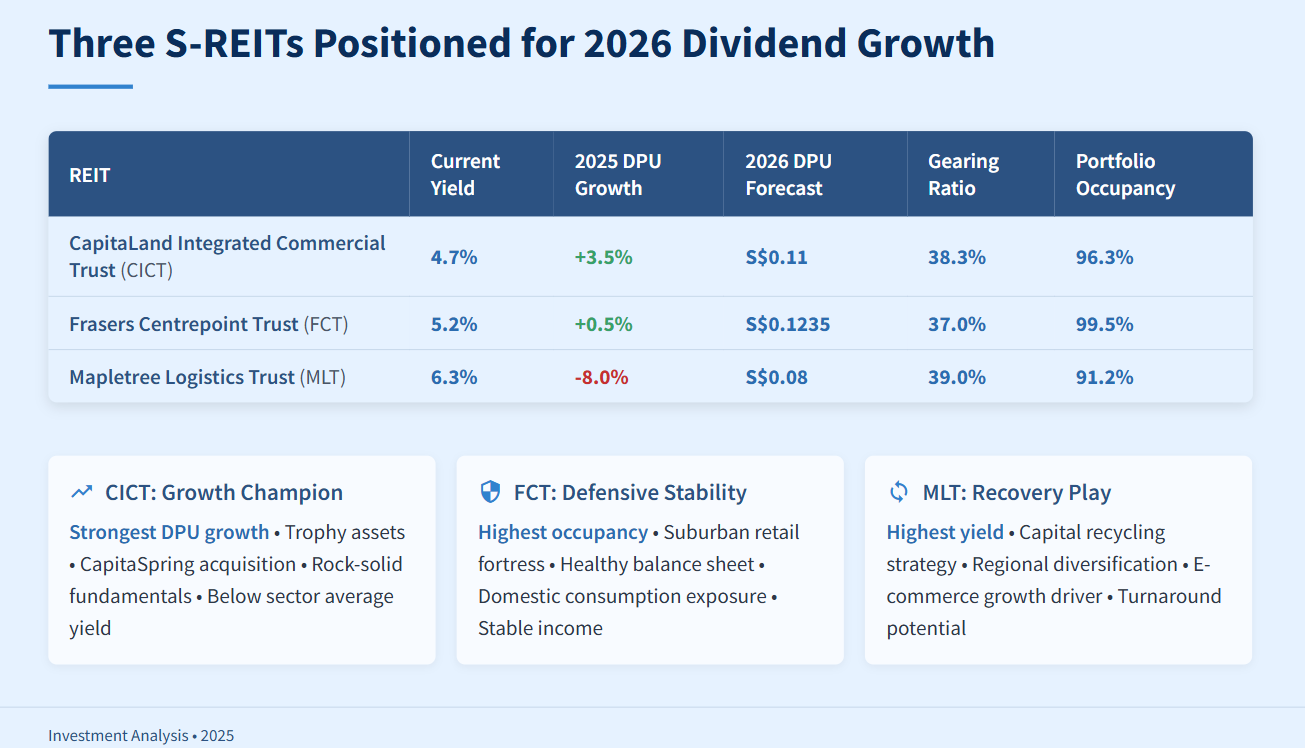

Not all REITs benefit equally from falling rates. The winners share three traits: strong operational fundamentals with positive rental reversions, healthy balance sheets with gearing below 40%, and portfolios concentrated in Singapore’s resilient property sectors. Three REITs check all these boxes.

TABLE 3: Three S-REITs Positioned for 2026 Dividend Growth

This table reveals the investment thesis clearly. CICT offers the strongest DPU growth momentum with rock-solid fundamentals. FCT provides defensive stability with the highest occupancy in the group. MLT presents a recovery play with the highest yield today, banking on operational improvements to reverse recent DPU declines.

CICT: Singapore’s Commercial Property Champion

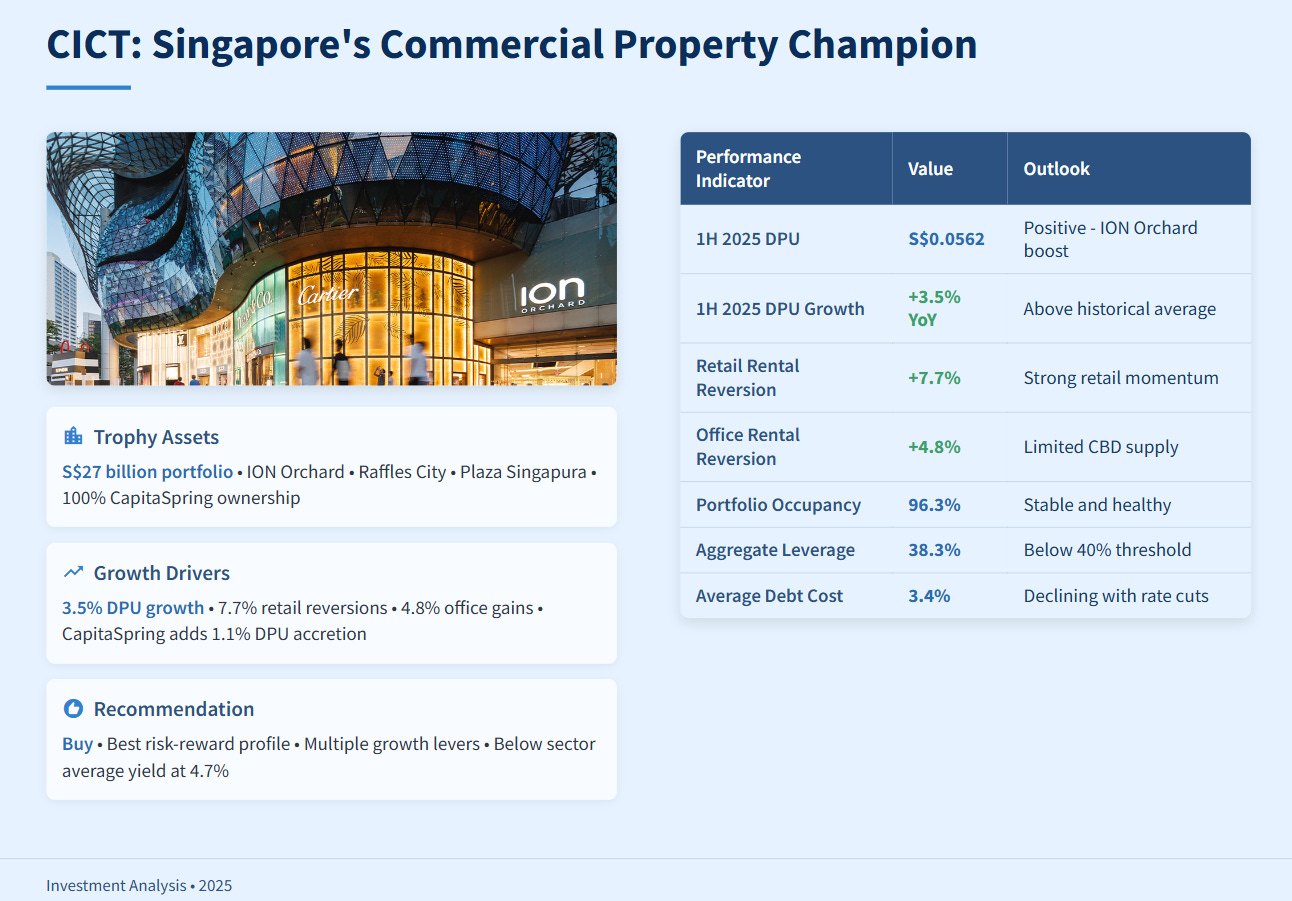

CapitaLand Integrated Commercial Trust dominates Singapore’s prime commercial real estate landscape. With a portfolio worth S$27 billion after recent acquisitions, CICT owns the trophy assets: ION Orchard, Raffles City, Plaza Singapura, and now 100% of CapitaSpring.

The first half of 2025 told the growth story clearly. CICT’s DPU jumped 3.5% year-on-year to S$0.0562, driven by ION Orchard’s contribution and lower interest expenses. The retail portfolio achieved rental reversions of 7.7%, while office properties posted 4.8% gains. These aren’t marginal improvements—they represent real pricing power in a market where Grade A office supply remains tight.

TABLE 4: CICT Performance Breakdown and Growth Drivers

The CapitaSpring acquisition deserves special attention. CICT bought the remaining 55% stake for S$1.045 billion, bringing its ownership to 100%. This Grade A office tower in Raffles Place operates at 99.9% occupancy—basically full. The deal adds 1.1% DPU accretion immediately, and that’s before factoring in the rental upside from Singapore’s limited pipeline of new CBD office buildings.

CICT’s leverage sits comfortably at 38.3%, leaving substantial debt headroom for future acquisitions or simply weathering any market turbulence. With 95% of the portfolio in Singapore, CICT benefits directly from the strong local economy and favorable SORA rate movements. As Singapore’s borrowing rates fall faster than US rates, CICT’s refinancing savings accelerate.

The 2026 forecast of S$0.11 DPU implies continued growth above 4%, supported by the full-year contribution from ION Orchard and CapitaSpring, ongoing asset enhancements, and declining financing costs. At a 4.7% yield today, CICT trades below the sector average despite having the strongest fundamentals in the group.

Recommendation: Buy. CICT offers the best risk-reward profile among Singapore commercial REITs, with multiple growth levers converging in 2026.

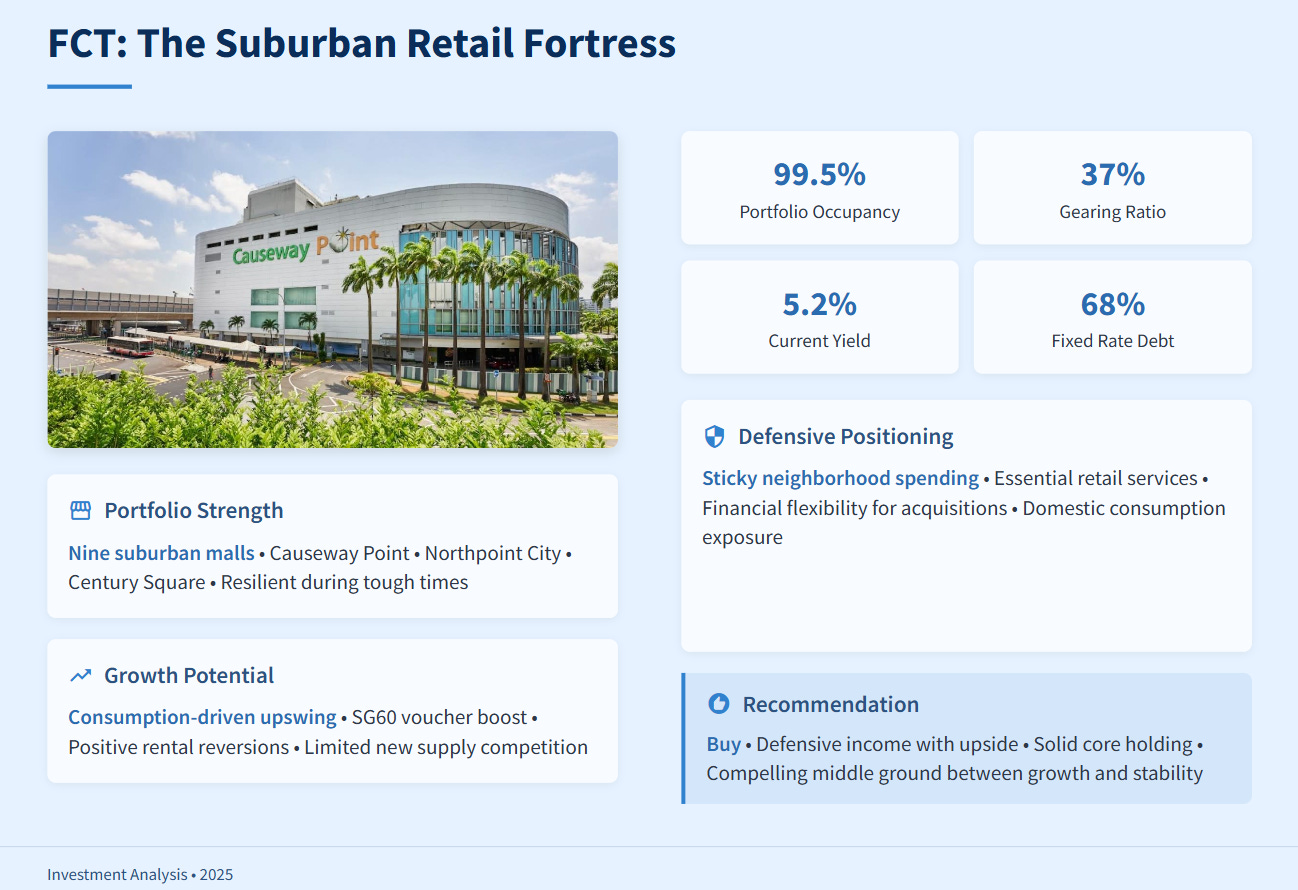

FCT: The Suburban Retail Fortress

Frasers Centrepoint Trust operates nine suburban shopping malls across Singapore, including Causeway Point, Northpoint City, and Century Square. While that might sound boring compared to Orchard Road glamour, suburban retail proved remarkably resilient during tough times and now stands poised for a consumption-driven upswing.

FCT’s 1H 2025 DPU of S$0.06054 edged up 0.5% year-on-year. That modest growth masked strong operational performance. Portfolio occupancy hit 99.5%—essentially full—with positive rental reversions as shopper traffic and tenant sales improved. The SG60 vouchers distributed to Singaporeans boosted retail spending, and suburban malls captured their fair share.

The real story for FCT involves its defensive positioning combined with growth potential. With gearing at just 37%, FCT maintains one of the healthiest balance sheets in the sector. This financial flexibility allows FCT to pursue selective acquisitions or asset enhancements without stressing the capital structure.

FCT’s 2026 DPU forecast of S$0.1235 suggests growth will accelerate as the full benefit of lower interest rates flows through. The REIT’s debt cost remains competitive, and with 68% of borrowings on fixed rates, FCT has already locked in favorable terms for the near future.

Suburban malls face less competition from new supply compared to downtown locations. Neighborhood spending remains sticky—people still need groceries, food courts, and basic retail services close to home. This defensive characteristic makes FCT attractive during uncertain economic periods, while the rate cut tailwind adds upside.

At a 5.2% current yield, FCT offers a compelling middle ground between growth and stability. The combination of near-full occupancy, healthy balance sheet, and exposure to domestic consumption makes FCT a solid core holding.

Recommendation: Buy. FCT provides defensive income with upside from rate cuts and sustained domestic consumption trends.

MLT: The High-Yield Recovery Play

Mapletree Logistics Trust sits in a different position. The 6.3% yield tells you the market harbors doubts. The REIT’s 1Q FY2026 results showed DPU down 8% year-on-year, and occupancy slipped to 91.2%. China operations continue struggling, and the broader logistics sector faces oversupply concerns in some markets.

But here’s the contrarian case: MLT trades at a discount precisely because of these known issues, and management is addressing them systematically. The capital recycling strategy targets S$150 million in divestments for the remainder of FY2026, allowing MLT to exit underperforming assets and redeploy capital into higher-quality properties.

When you exclude China from the rental reversion calculation, MLT achieved positive reversions of 2.8% in 1Q FY2026. That’s not spectacular, but it shows the core portfolio outside China still generates organic growth. The regional diversification across Singapore, Hong Kong, Japan, Australia, and other markets provides multiple growth engines even if one market underperforms.

MLT’s gearing at 39% is higher than CICT or FCT, but still manageable. The average debt cost has room to fall as existing loans get refinanced at lower rates. With 80% of borrowings on fixed rates and no refinancing risk in FY2025, MLT has time to execute its turnaround strategy.

The 2026 DPU forecast of S$0.08 implies a recovery from current levels as divestments complete, operational improvements materialize, and interest savings kick in. E-commerce growth in Asia continues driving structural demand for quality logistics facilities. MLT’s portfolio includes modern assets in strategic locations that benefit from this trend.

The risk with MLT involves execution and market conditions. If trade tensions escalate or economic growth disappoints, logistics demand could soften further. But for investors willing to accept higher risk in exchange for that 6.3% yield and recovery potential, MLT offers asymmetric upside.

Recommendation: Hold with selective buying. MLT suits investors seeking high current income who believe in the logistics sector recovery story and can tolerate short-term volatility.

The Sector Picture: Who Wins in 2026

Understanding the broader S-REIT sector dynamics helps explain why these three REITs stand out. Different property types face different outlooks heading into 2026.

TABLE 6: S-REIT Sector Performance and 2026 Outlook

Retail and office REITs with Singapore exposure benefited most in 2025 and carry that momentum into 2026. The combination of domestic consumption strength, tourism recovery, and limited new supply in prime locations creates pricing power. This explains CICT’s strong rental reversions and FCT’s high occupancy.

Industrial and logistics REITs face a more nuanced picture. While e-commerce growth supports structural demand, near-term concerns about manufacturing slowdowns and trade tensions create caution. This uncertainty explains MLT’s discounted valuation despite its quality portfolio.

Healthcare REITs like Parkway Life REIT offer defensive characteristics with stable long-term leases. Data centre REITs benefit from AI infrastructure buildout but trade at premium valuations reflecting high growth expectations.

For investors building a REIT portfolio in late 2025 and 2026, the sweet spot involves retail and office REITs with strong Singapore exposure and healthy balance sheets. That’s exactly what CICT and FCT deliver.

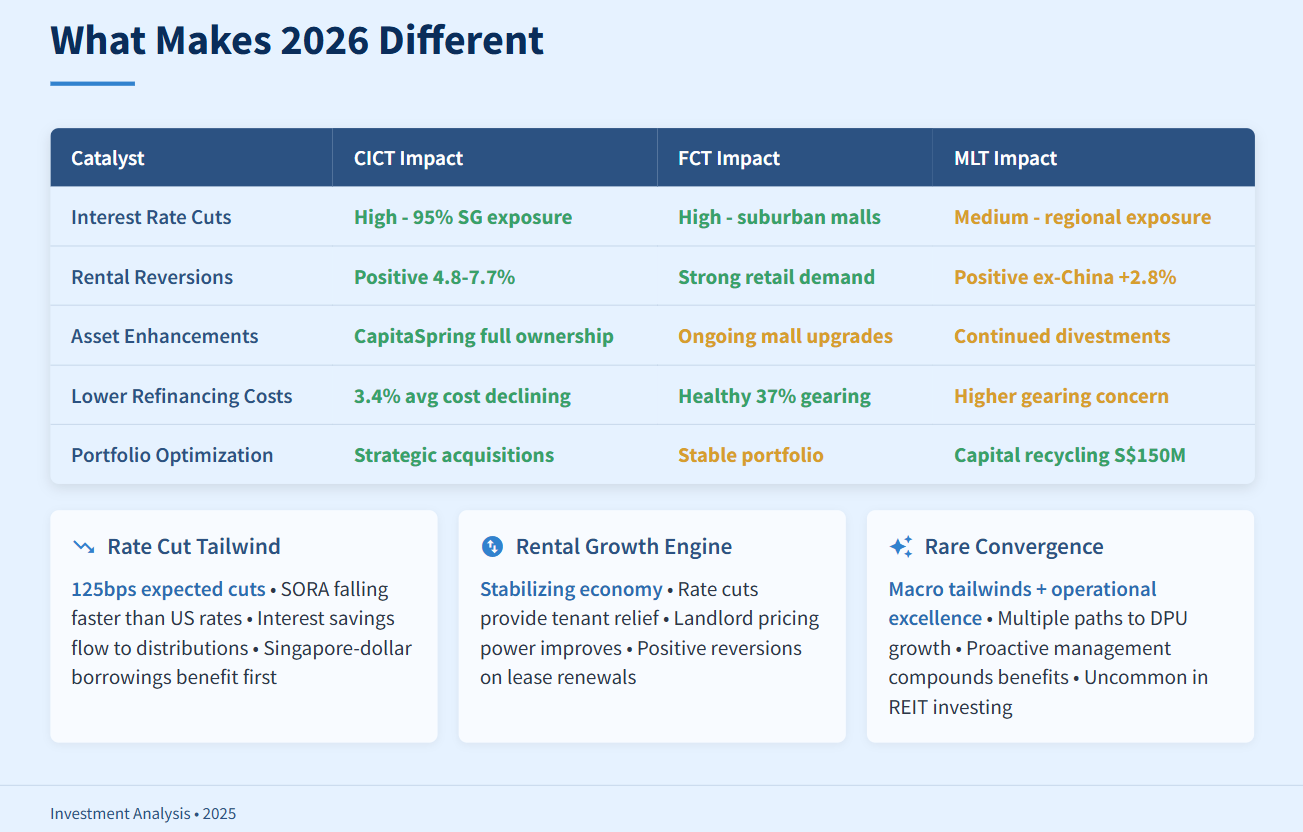

What Makes 2026 Different

Several factors converge to make 2026 a potentially strong year for the featured S-REITs. Understanding these catalysts helps explain why now matters.

TABLE 6: 2026 Growth Catalysts - How Each REIT Benefits

Interest rate cuts represent the biggest tailwind. As REITs refinance maturing debt at lower rates, the interest savings drop straight to the bottom line. REITs with significant Singapore-dollar borrowings benefit faster because SORA rates fall more aggressively than US rates.

Rental reversions provide the second growth engine. In a rising rate environment, landlords struggled to push rents higher as tenants faced their own cost pressures. Now, with the economy stabilizing and rate cuts providing relief across the board, tenant affordability improves. This creates space for landlords to achieve positive rental reversions on lease renewals.

Asset enhancements and portfolio optimization represent REIT-specific initiatives that compound the macro tailwinds. CICT’s CapitaSpring consolidation adds immediate DPU accretion and sets up future rental growth from a fully controlled asset. FCT’s ongoing mall upgrades keep properties competitive and support tenant sales. MLT’s capital recycling exits underperformers and redeploys into better opportunities.

The combination of favorable macro conditions and proactive management creates multiple paths to DPU growth in 2026. That’s rare in REIT investing, where you typically rely on either market tailwinds or operational excellence—seldom both at once.

The Risks You Need to Know

Let’s be clear about what could go wrong. REITs aren’t risk-free income machines, and 2026 could disappoint under certain scenarios.

Economic slowdown represents the primary risk. If Singapore’s economy weakens significantly, retail spending drops and office tenants struggle. Both CICT and FCT depend on sustained economic activity. While Singapore’s economy remains resilient, global headwinds from trade tensions or financial market turbulence could spill over.

Interest rates rising instead of falling would reverse the entire thesis. If inflation proves stickier than expected and central banks pause or reverse rate cuts, REIT borrowing costs could stabilize or increase. This would eliminate the refinancing tailwind and potentially pressure valuations as bond yields rise.

Property oversupply in specific segments poses sector-specific risks. The industrial/logistics sector already shows signs of oversupply in Singapore and some regional markets. While this primarily affects MLT, any broader property market weakness could weigh on sentiment across all S-REITs.

Geopolitical tensions and trade wars could disrupt the logistics sector specifically. If tariffs escalate or supply chains restructure away from certain regions, logistics demand patterns shift. MLT’s regional exposure makes it vulnerable to these disruptions.

Leverage and refinancing risks shouldn’t be ignored. While all three REITs maintain manageable gearing today, any deterioration in operating performance combined with tight credit conditions could create stress. MLT’s higher gearing at 39% leaves less margin for error.

Valuation risk exists if you’re buying after the recent sector rally. S-REITs have already rebounded 9% since July 2025. Some of the good news may already be priced in. If the market gets ahead of itself, near-term returns could disappoint even if the long-term thesis plays out.

These risks require monitoring but don’t invalidate the investment case. The key involves position sizing appropriately, maintaining portfolio diversification, and having a long-term perspective. REITs work best as core holdings held through cycles, not trading vehicles.

How to Position Your Portfolio

For Singaporean investors considering these REITs, practical implementation matters. Here’s how to think about portfolio construction.