Sukuk: The Ethical Bond Alternative Singapore Investors Can’t Ignore

How to build a stable, faith-aligned income pillar without compromising returns—or your values.

You want the safety and predictable income of bonds, but you need your investments to align with ethical or faith-based principles. Maybe you’ve heard whispers about “Islamic bonds” but dismissed them as a niche product only for Muslim investors. Or perhaps you’re tired of feeling stuck between your values and your portfolio stability.

Here’s what most Singapore investors miss: Sukuk aren’t just an ethical alternative—they’re a legitimate fixed-income asset class that delivers competitive yields, lower volatility during market turbulence, and genuine asset backing. The global sukuk market just crossed the $1 trillion milestone in 2024, and Singapore has positioned itself as a regional Islamic finance hub with government-backed frameworks and tax-neutral treatment.

In This Article:

• What Makes Sukuk Different From Regular Bonds?

• The Three Shariah Principles That Define Sukuk

• How Sukuk Yields Compare

• The Risk Profile You Need to Understand

• Your Actionable Investment Options in Singapore

• Why This Matters for Singapore Investors Right Now

• The Bottom Line: Should Sukuk Be in Your Portfolio?What Makes Sukuk Different From Regular Bonds?

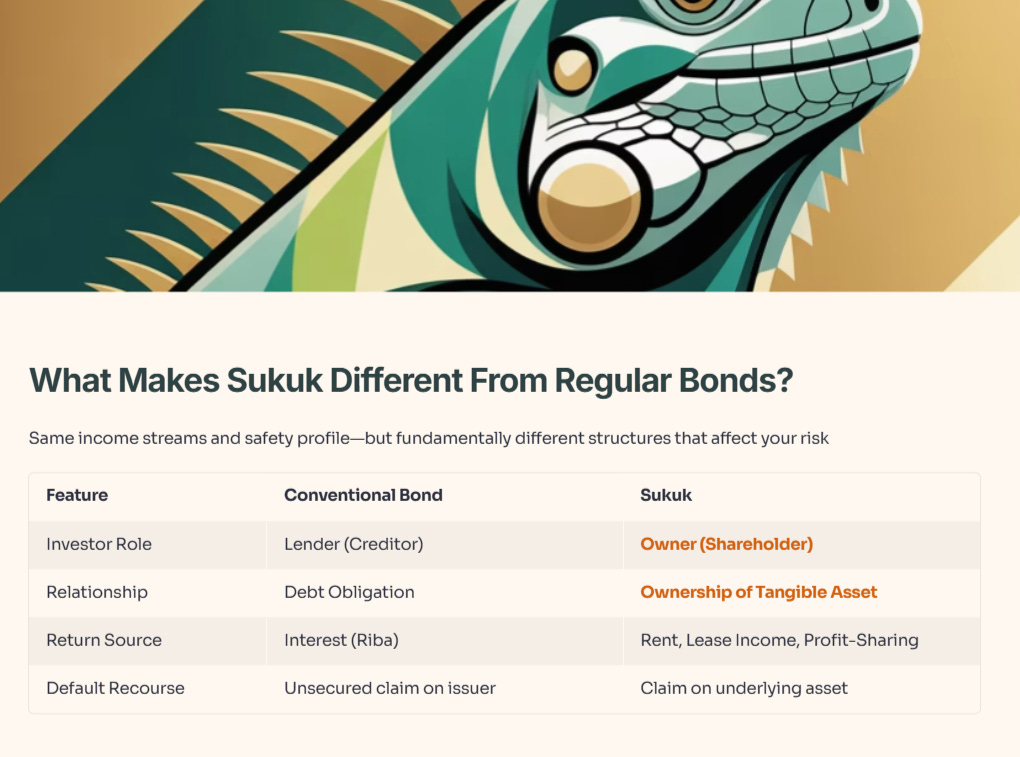

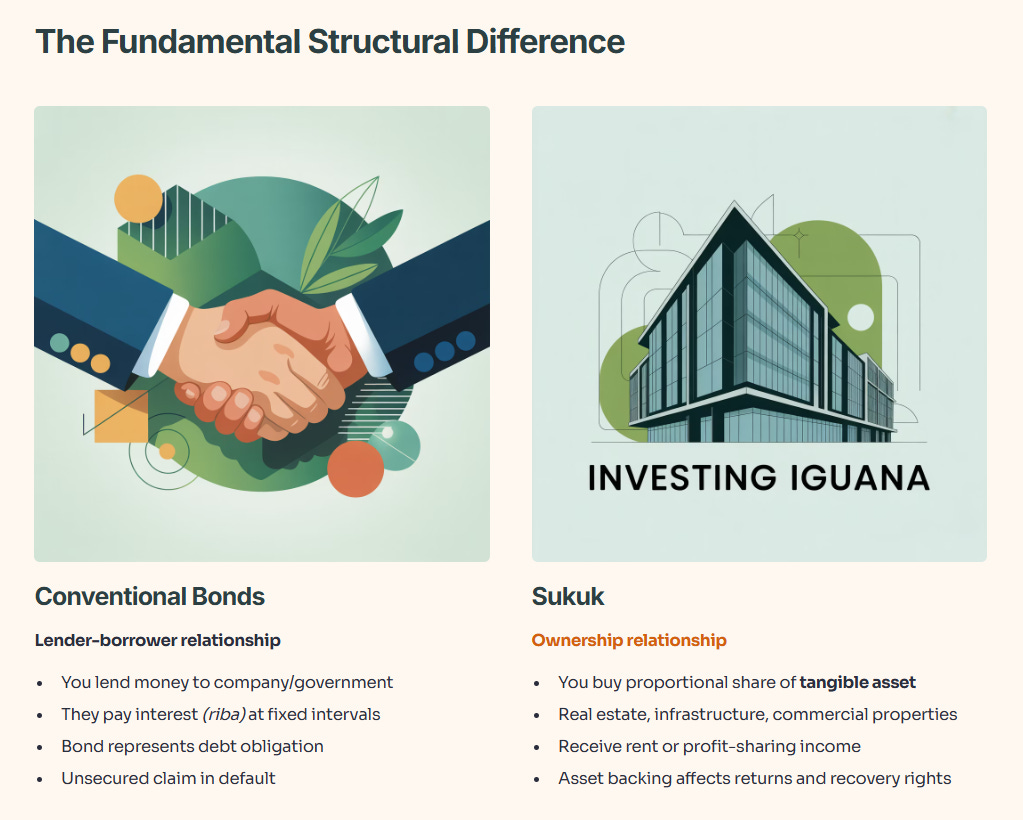

Let’s cut through the confusion. Sukuk and conventional bonds both provide regular income streams and raise capital for issuers. Both are generally safer than equities. But the fundamental structure is completely different—and that difference matters for your risk profile.

Conventional bonds create a lender-borrower relationship. You lend money to a company or government, and they promise to pay you interest (riba) at fixed intervals. Your bond represents a debt obligation.

Sukuk create an ownership relationship. You don’t lend money—you buy a proportional share of an actual, tangible asset. This could be real estate, infrastructure projects, or commercial properties. You lease that asset back to the issuer and receive rent or profit-sharing. This asset-backing principle creates genuine structural differences that affect your returns, risks, and recovery rights.

⚡️ Iggy’s Take: Welcome to The Investing Iguana! Our community just hit 1.3 million reads and 65,000 likes, and we were recently ranked 8th in Tiger Brokers’ 2024 Influential Tigers. Join our paid Substack for deeper context and a sharper edge in Singapore’s markets.

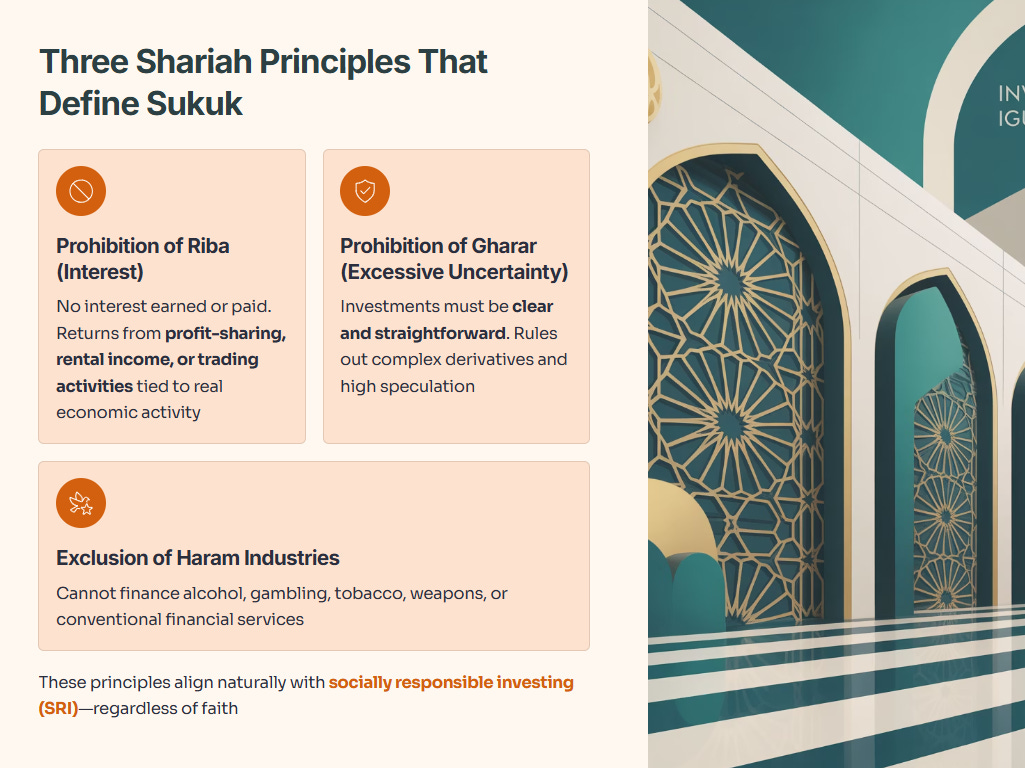

The Three Shariah Principles That Define Sukuk

Sukuk must comply with three core Islamic finance prohibitions that also happen to align with socially responsible investing (SRI) principles:

Prohibition of Riba (Interest): No interest can be earned or paid. Returns must come from profit-sharing, rental income, or trading activities tied to real economic activity.

Prohibition of Gharar (Excessive Uncertainty): Investments must be clear, straightforward, and avoid high speculation. This rules out complex derivatives and speculative products.

Exclusion of Haram Industries: Sukuk cannot finance companies involved in alcohol, gambling, tobacco, weapons, or conventional financial services.

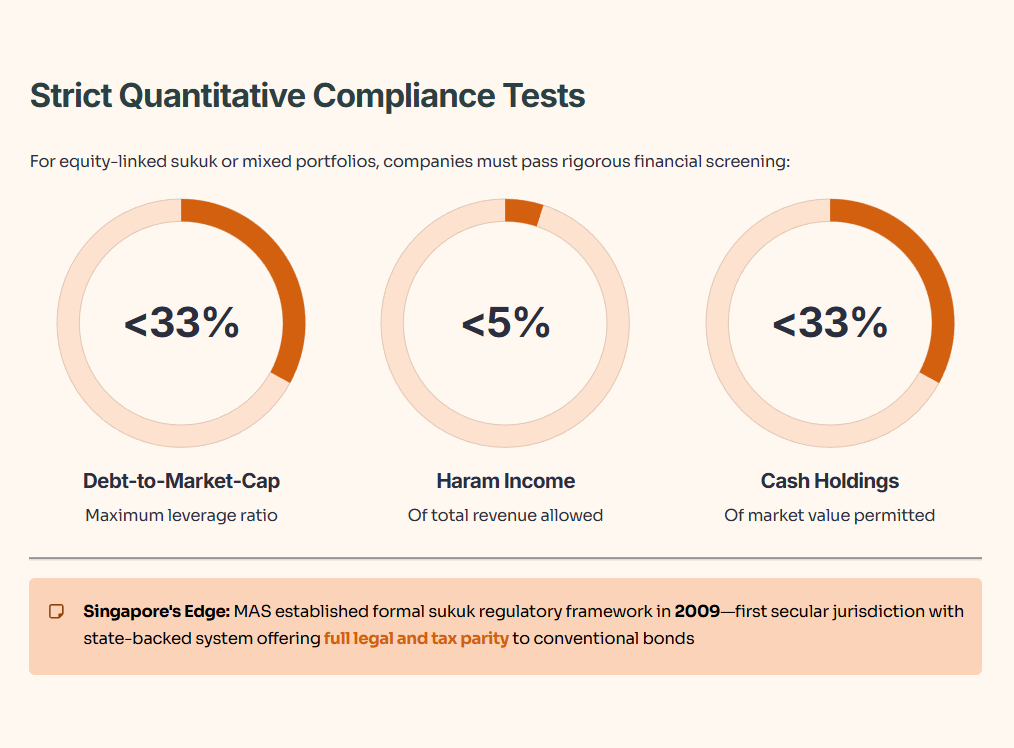

For equity-linked sukuk or mixed portfolios, companies must also pass strict quantitative financial ratio tests to ensure compliance:

Debt-to-market-cap below 33%.

Haram income below 5% of total revenue.

Cash holdings below 33% of market value.

Singapore’s Monetary Authority (MAS) established a formal regulatory framework for sukuk in 2009. This makes Singapore the first secular jurisdiction to create a state-backed system with full legal and tax parity to conventional bonds.

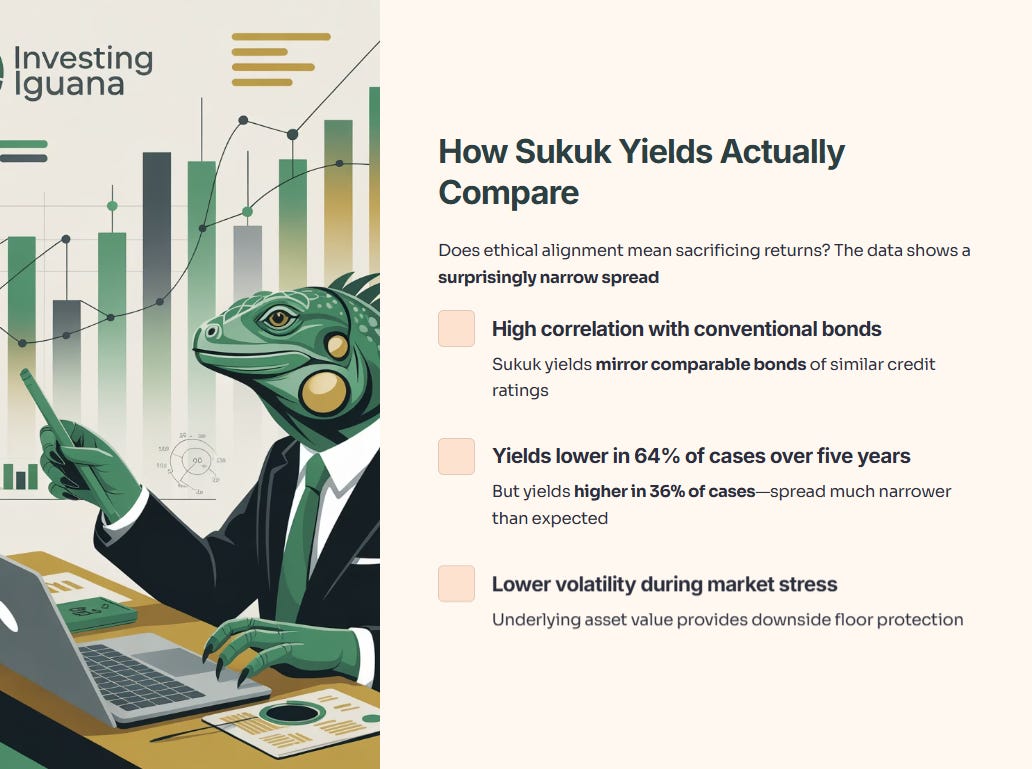

How Sukuk Yields Compare

Does pursuing ethical alignment mean sacrificing returns? The research suggests a narrow spread.

Multiple studies show that sukuk yields generally mirror or maintain a high correlation with conventional bond yields of similar credit ratings. Over a recent five-year period, sukuk yielded less than comparable bonds in 64% of cases, with yields higher in 36% of cases. The spread is much narrower than most investors expect.

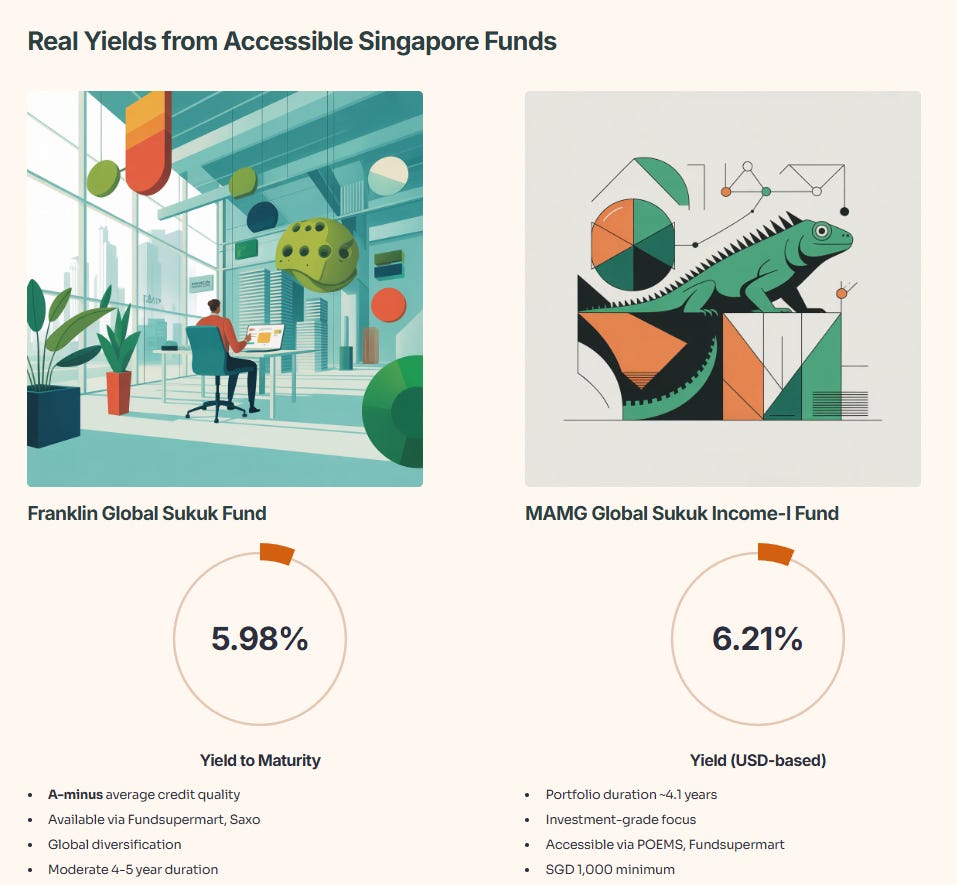

For context, two accessible funds for Singapore investors offer competitive yields:

Franklin Global Sukuk Fund: Yield to maturity of 5.98% (A-minus average credit quality).

MAMG Global Sukuk Income-I Fund: Yields approximately 6.21% (portfolio duration around 4.1 years).

Crucially, during periods of market stress, sukuk have shown lower volatility than conventional bonds because the underlying asset value provides a floor. This suggests sukuk can serve as a valuable buffer against market instability—exactly what you want from a stability pillar in your portfolio.

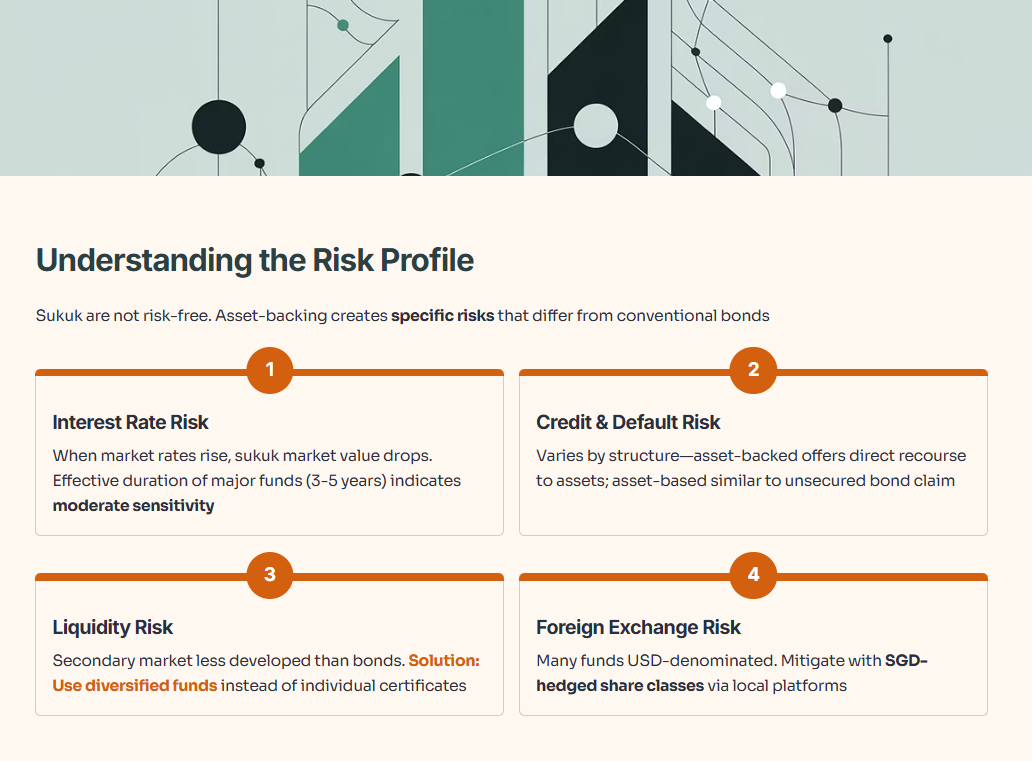

The Risk Profile You Need to Understand

Sukuk are not risk-free. The asset-backing structure introduces specific risks that differ from conventional bonds.

1. Interest Rate Risk

Like conventional bonds, sukuk pricing is indirectly exposed to interest rate fluctuations. When market rates rise, the market value of your existing sukuk drops. The effective duration of major sukuk funds (around 3 to 5 years) indicates moderate interest rate sensitivity.

2. Credit and Default Risk

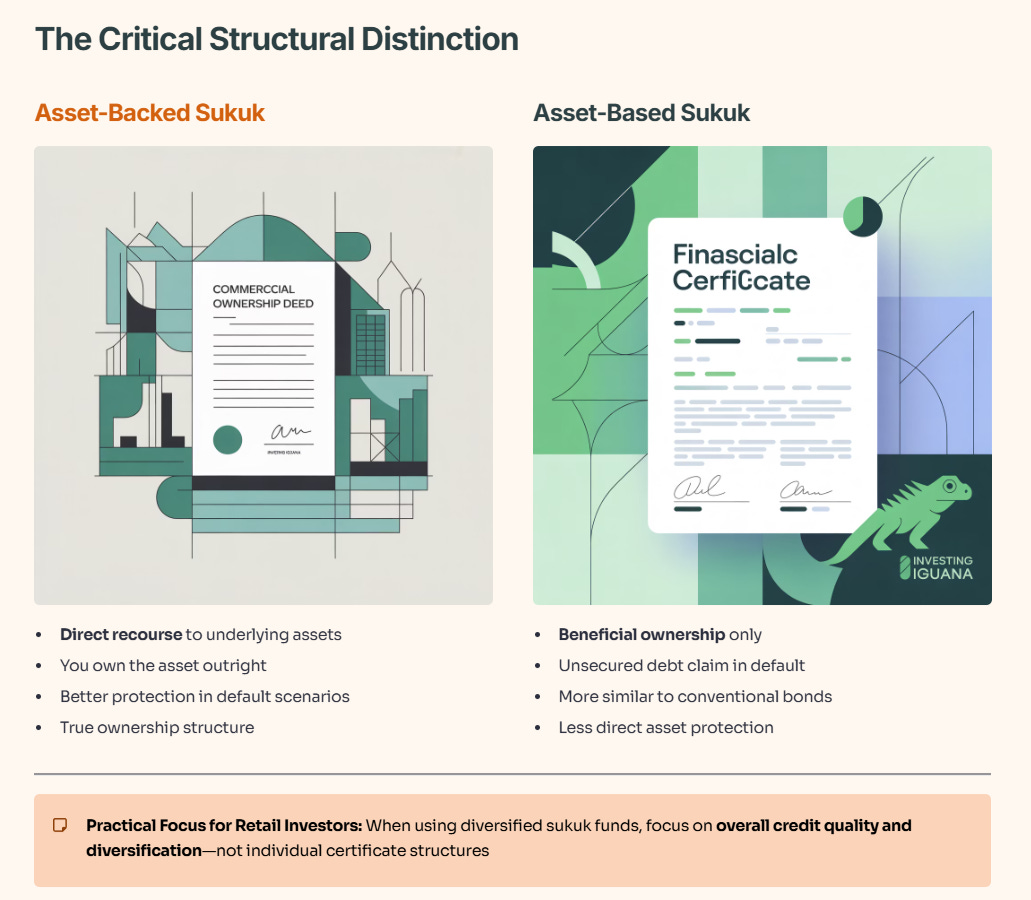

The key distinction here is between the two main structures:

Asset-backed Sukuk: You have a direct recourse to the underlying assets if the issuer defaults (you own the asset).

Asset-based Sukuk: You only have beneficial ownership and, in a default scenario, you often have an unsecured debt claim, making it more similar to a conventional bond

For the retail investor using a diversified fund, the main practical focus should be on the fund’s overall credit quality and diversification, not the individual legal structure of every certificate.

3. Liquidity Risk

The secondary market for individual sukuk certificates is generally less developed than the conventional bond market, which can limit liquidity. For retail investors, using sukuk funds rather than buying individual certificates solves this problem entirely.

4. Foreign Exchange Risk

Many global sukuk funds are denominated in USD or regional currencies. Unfavorable exchange rate movements affect your returns. If you invest via SGD-hedged share classes available through platforms like Fundsupermart, this risk is mitigated, though it may add a small cost.

Your Actionable Investment Options in Singapore

Singapore offers accessible, practical pathways to access sukuk, categorized here by minimum investment and accessibility: