EXCLUSIVE: Suntec REIT Results: The 23% DPU Jump is a “Rate Mirage” – Don’t Get Blinded by the Shine

The headlines are screaming about a 23.2% jump in H2 DPU, and yield-hungry retail investors are already salivating. But here is the cold, hard truth: Net Property Income (NPI) actually fell 1.6%.

The headlines are screaming about a 23.2% jump in H2 DPU, and yield-hungry retail investors are already salivating. But here is the cold, hard truth: Net Property Income (NPI) actually fell 1.6% in the second half of 2025.

If you think Suntec’s underlying business suddenly became a money-printing machine, you’re reading the wrong report. This DPU “pop” is almost entirely a result of a favorable interest rate pivot and lower financing costs. While the dividend looks juicy today, the operational engine is sputtering in Australia, and the Singapore flagship is doing all the heavy lifting. We are looking at a recovery built on financial engineering, not organic growth.

In This Article:

The “Concept Deep Dive”: The Mechanics of Interest Expense Sensitivity

The “Leverage Pivot” Explained

Financial Optimization: Pros vs. Cons

The Iggy Audit: Singapore Strength vs. Australian Deadweight

Peer Comparison Table

The Analysis:

The Data Fortress

3-Year Dividend Ledger

Financial Health Checklist

Commentary: The dividend is “Safe” for 2026

The Scenario Matrix (2026 Forecast)

Sensitivity Analysis Table

InvestingPro Reality Check

Iggy's Verdict🦎 About Iggy the Investing Iguana

Welcome to the Iguana Pit! If you’re new here, I’m Iggy: your guide through the dense jungle of the Singapore markets. My mission is simple: to spot the predators before they spot your portfolio.

We are now 5,800+ subscribers strong across YouTube and Substack, focusing purely on the data-driven alpha that mainstream media misses.

🚀 Join the “Elite 150” Inner Circle

Real alpha is found behind the velvet rope. Stop following the herd and start following the data with our 150+ paid members.

📺 The YouTube Edge (S$3/mo): Beat the Delay.

Instant Access: Watch new videos the moment they drop.

The Free Tier Trap: Free subscribers wait up to 14 days to see the same video. (By then, the news is old and the trade is gone).

📝 The Substack Deep-Dive (US$6/mo): Unlock the Vault.

Zero Paywalls: Read the full “Deep Dive” articles and “Substack Exclusive” articles found only on Substack.

Visual Alpha: Download exclusive Infographic Cheatsheets not available to free readers.

💎 The Ultimate Value Pass (S$9/mo): (BEST VALUE)

Get It All: Paid via YouTube, this bundle grants you Instant Video Access AND Full Substack Access.

The Math: You save ~30% compared to buying them separately. It’s the “Smart Money” move.

Why wait 2 weeks for old news? Get the data while it’s fresh. 👉 Join Here: https://www.youtube.com/@InvestingIguana/membership

The “Concept Deep Dive”: The Mechanics of Interest Expense Sensitivity

In the world of REITs, there are two ways to grow distributions: Operational Excellence (raising rents, cutting vacancies) and Financial Optimization (lowering the cost of debt). Suntec REIT has just given us a masterclass in the latter.

The “Leverage Pivot” Explained

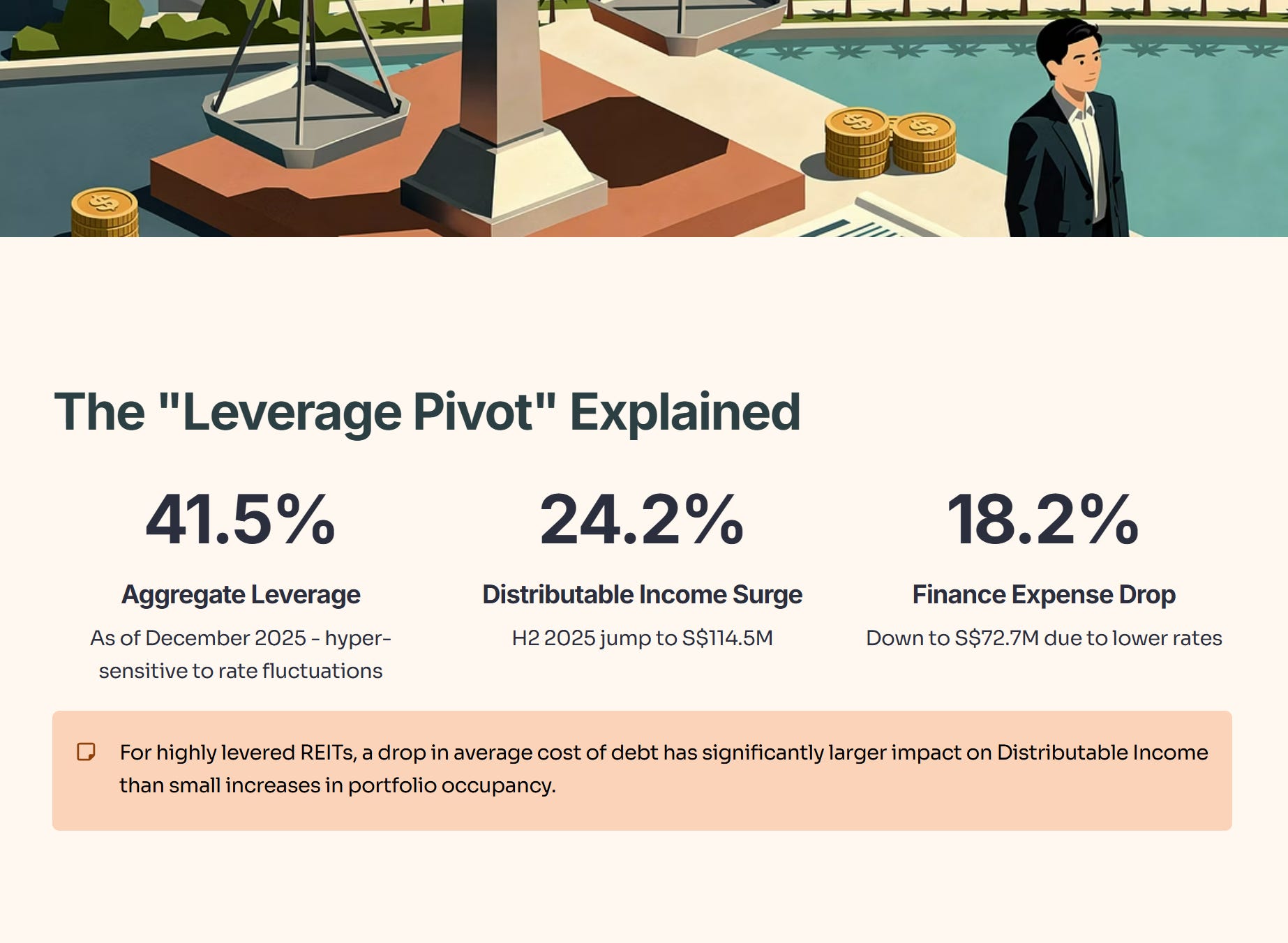

When a REIT operates with high gearing—Suntec’s aggregate leverage was 41.5% as of December 2025—it becomes hyper-sensitive to interest rate fluctuations. In 2023 and 2024, Suntec was the “whipping boy” of S-REITs because its financing costs were cannibalizing its profits. However, this sword cuts both ways.

For a highly levered REIT, a drop in the average cost of debt has a significantly larger impact on the Distributable Income than a small increase in portfolio occupancy. In H2 2025, Suntec’s distributable income from operations surged 24.2% to S$114.5 million, primarily because finance expenses dropped 18.2% to S$72.7 million due to lower interest rates and debt repayment.

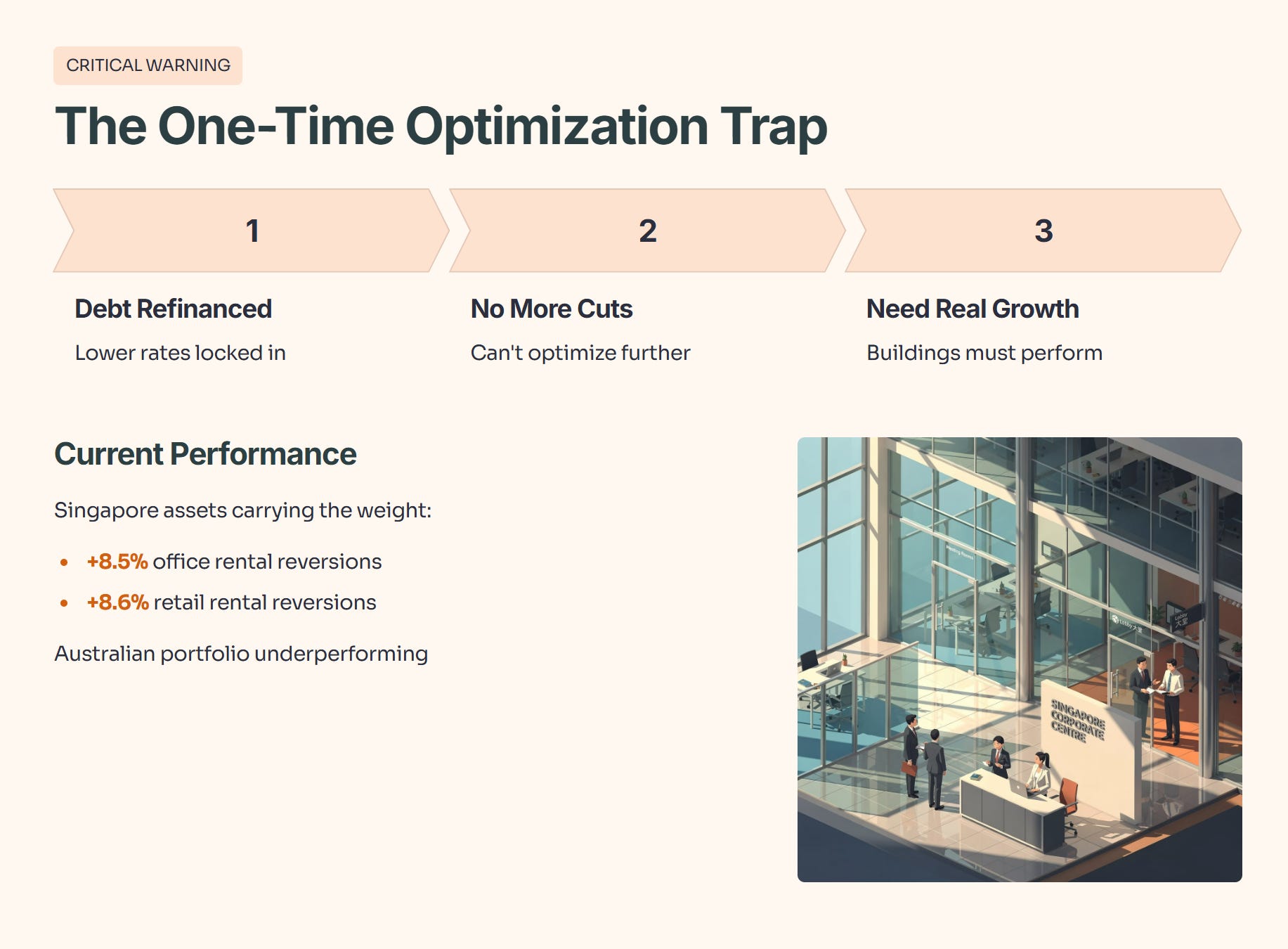

The danger? This is a one-time optimization. Once the debt is refinanced at lower rates, you can’t “cut” your way to growth anymore. To sustain this 23% DPU momentum, the actual buildings—the malls and offices—need to perform. Right now, the Singapore assets, which achieved +8.5% and +8.6% rental reversions in office and retail respectively, are carrying the weight of an underperforming Australian portfolio.

Financial Optimization: Pros vs. Cons