Tech Up 79%, Banks Down 8.5% | SGX Weekly Movers & Shakers 26 Apr | 🦖EP1572

Your dividends, SRS payouts, and bank interest all depend on those 8.5% losses

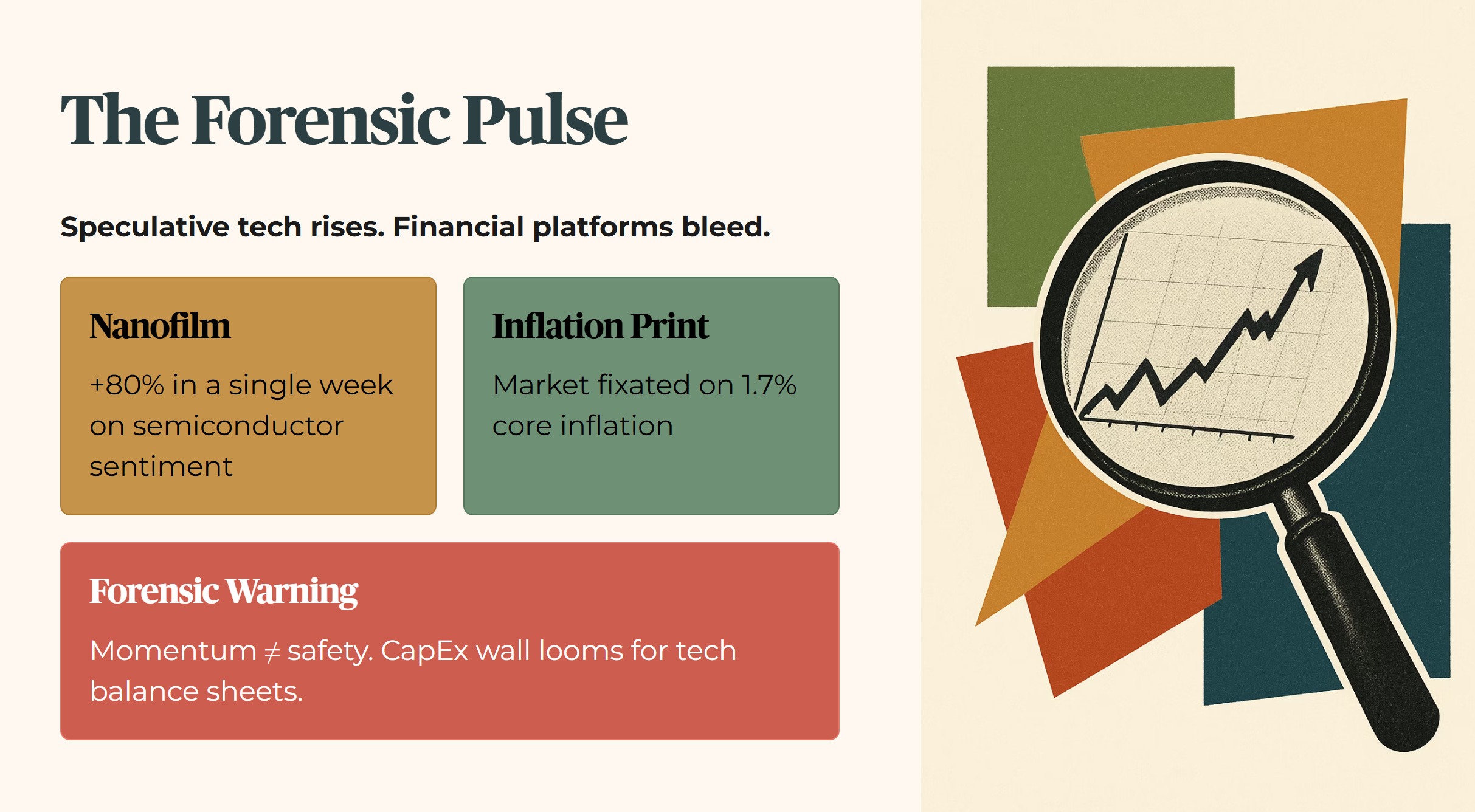

The Forensic Pulse: Speculative Tech Rises while Financial Platforms Bleed

Nanofilm has surged nearly 80% in a single week while the broader market remains fixated on a 1.7% core inflation print. If you mistake this momentum for a forensic safety net, you are ignoring the capital expenditure wall that tech-heavy balance sheets must soon climb.

In This Article:

The Macro Pulse

This Weeks Forensic Movers The Gainers

This Weeks Forensic Warnings The Losers

The Forensic Yield Spread Monitor

The Macro Connector

The Window Is Already Open

Iggy’s Weekly Verdict

Iggy’s Forensic Disclaimer

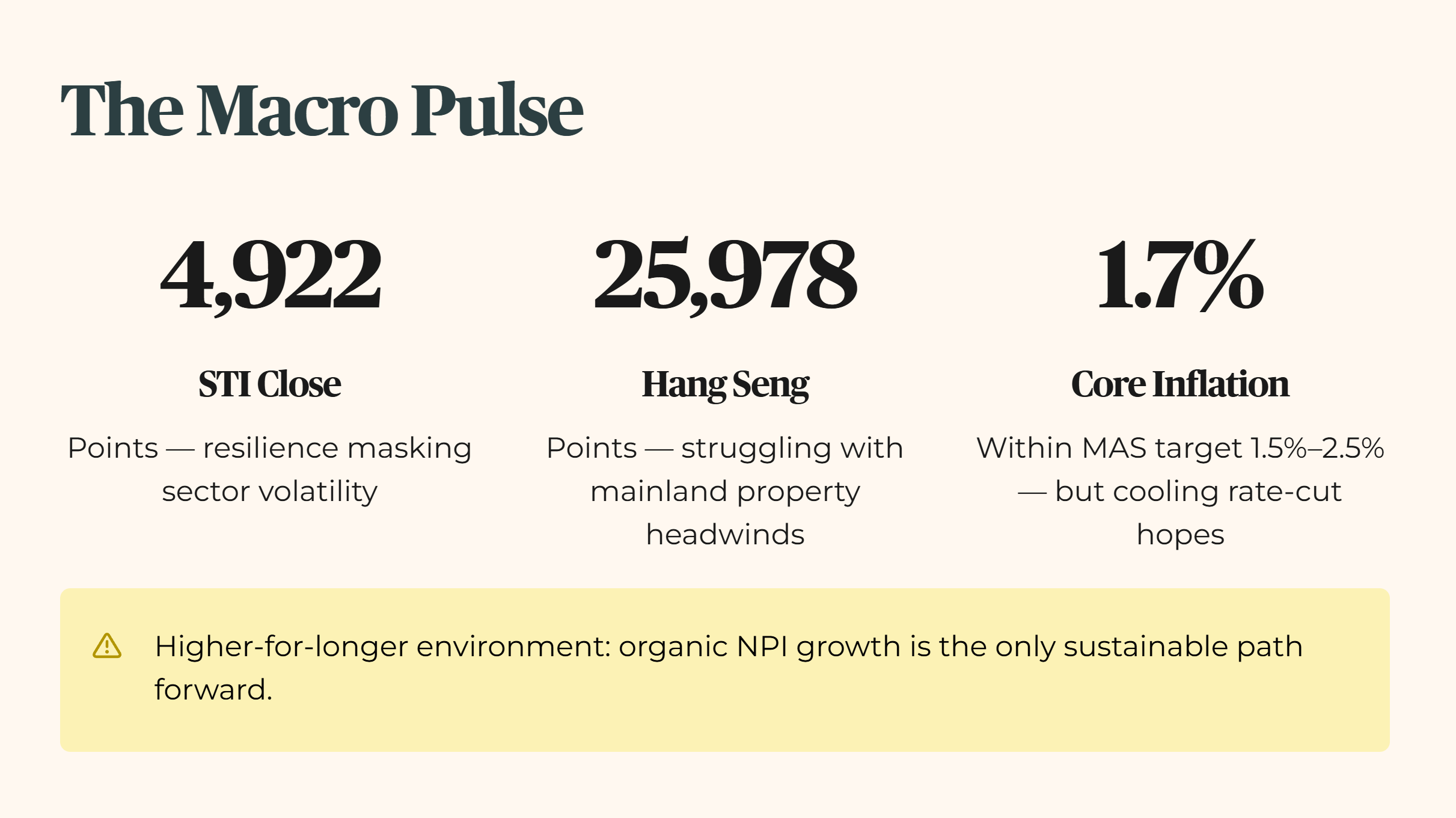

The Macro Pulse

The Straits Times Index closed the week at 4,922.86 points. This is a significant climb that masks deep underlying volatility across the industrial sectors. While the local index showed resilience at this level, the regional picture remains fractured. The Hang Seng Index finished at 25,978.07 as it struggled with persistent property headwinds on the mainland.

The primary driver for this week’s SGX direction was the March inflation data release. Core inflation ticked up to 1.7%, remaining within the MAS target range of 1.5% to 2.5% for 2026. However, the slight acceleration has cooled expectations for any near-term easing of the risk-free rate benchmark. Investors are now sitting in a higher-for-longer environment where organic NPI growth is the only sustainable path forward.

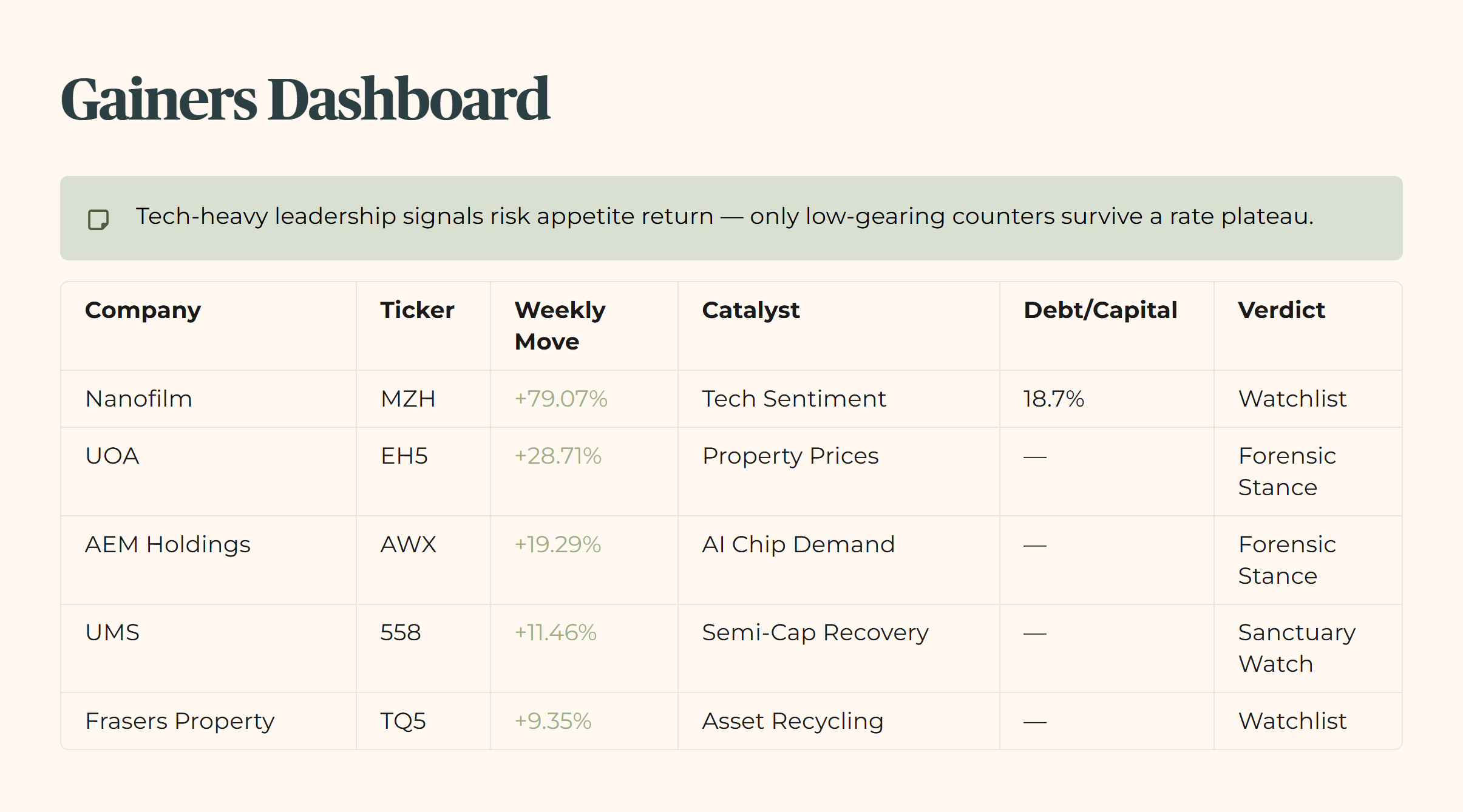

This Week’s Forensic Movers — The Gainers

Forensic Verdict: The top gainers this week are dominated by high-beta technology players benefiting from a sectoral rotation, but their forensic durability remains tied to upcoming capital expenditure cycles.

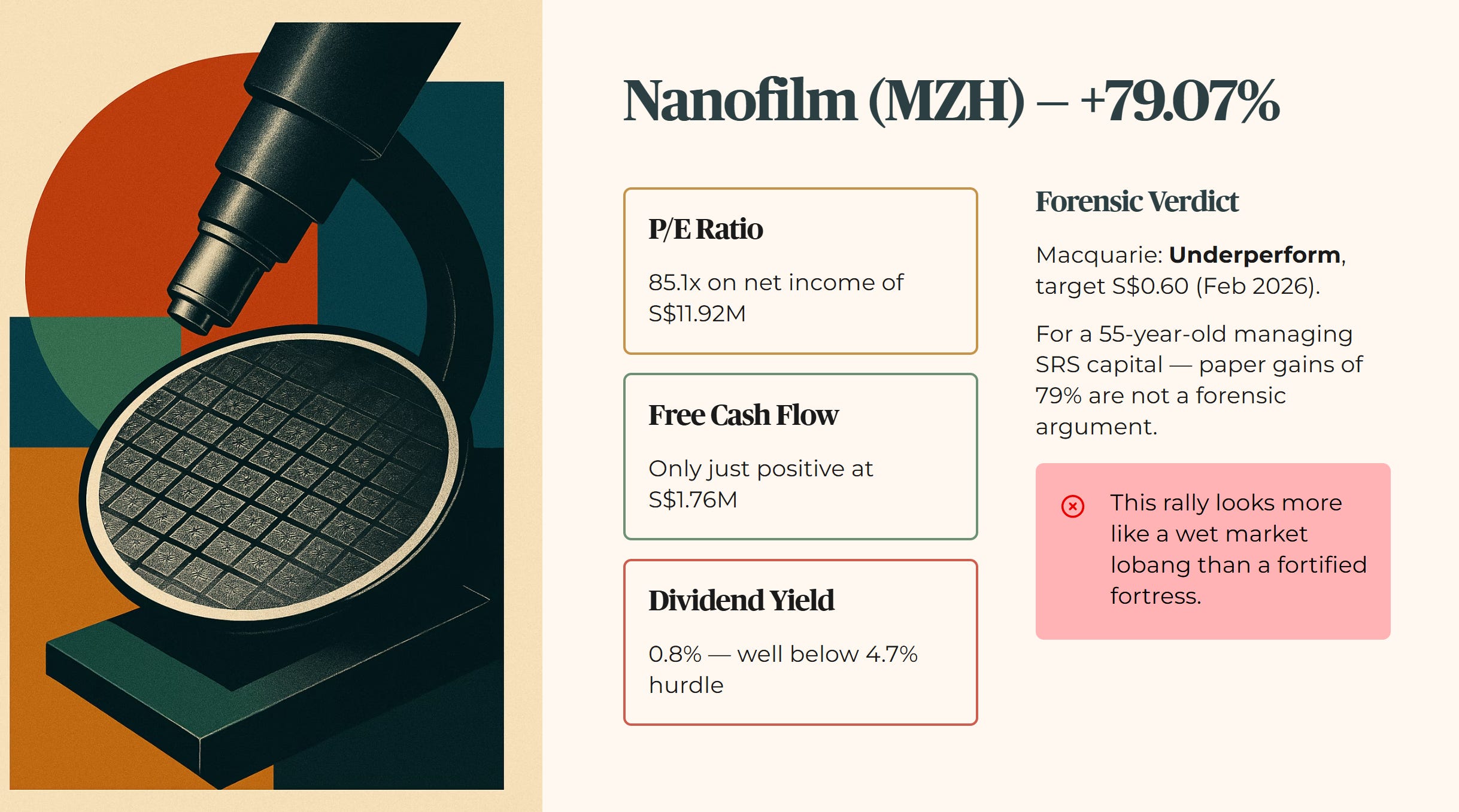

Nanofilm (MZH) — +79.07%

The week’s standout mover surged on semiconductor sentiment. The forensic reality is less tidy. At a P/E of 85.1x on net income of S$11.92M, the valuation requires perfect execution on its Nanofabrication contracts. Free cash flow has only just turned positive at S$1.76M for the full year, and the dividend yield of 0.8% sits well below the 4.7% hurdle. Macquarie maintained an underperform rating with a target of S$0.60 as recently as February 2026. For a 55-year-old investor managing SRS capital, paper gains of 79% are not a forensic argument. A single earnings miss could reopen the gap to that analyst target quickly. This rally looks more like a wet market lobang than a fortified fortress.

UMS (558) — +11.46%

Climbed on the back of its strong relationship with Applied Materials and a historically disciplined balance sheet. The forensic interpretation here is one of relative fortress quality in the mid-cap space, though its dividend yield must be weighed against the 3.2% forensic floor. For the retail investor, UMS represents a more conservative way to play the tech rally compared to the high-beta volatility of Nanofilm.

AEM Holdings (AWX) — +19.29%

Tracked the global recovery in testing and handling equipment demand for the AI chip sector. Despite the rally, the stock remains sensitive to the capital expenditure budgets of its key customer, making the forensic gap between fair value and market price a narrow one. A 50-year-old investor should treat this as a cyclical play rather than a foundational income generator.

UOA (EH5) — +28.71%

Rose as investors reacted to the URA report of a 0.9% rise in private home prices for Q1 2026. Forensically, this suggests a stabilising NAV that provides a temporary shield against the higher-rate environment. For the heartland landlord, this move signals that the debt wall for residential developers is being pushed back by resilient local demand.

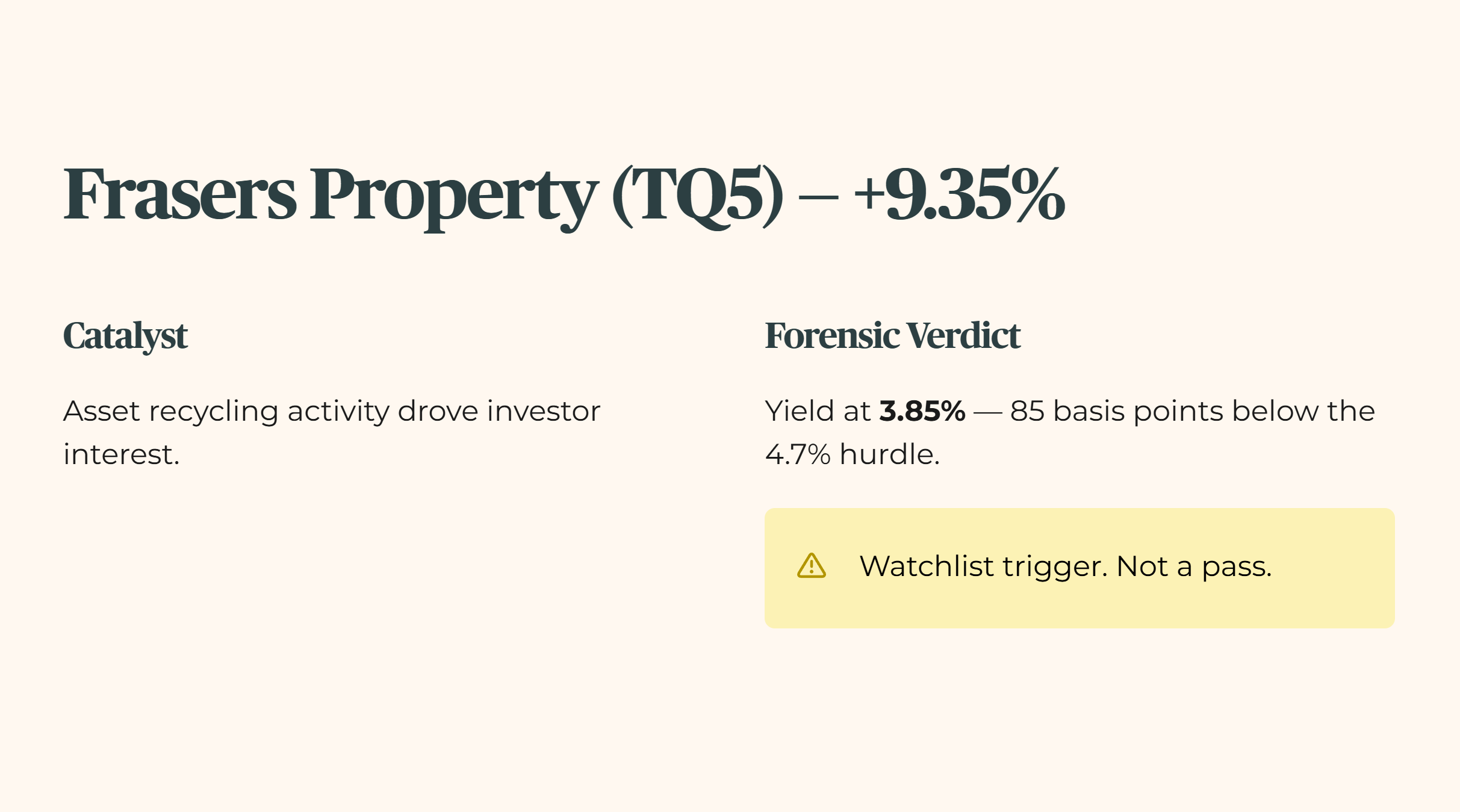

Frasers Property (TQ5) — +9.35%

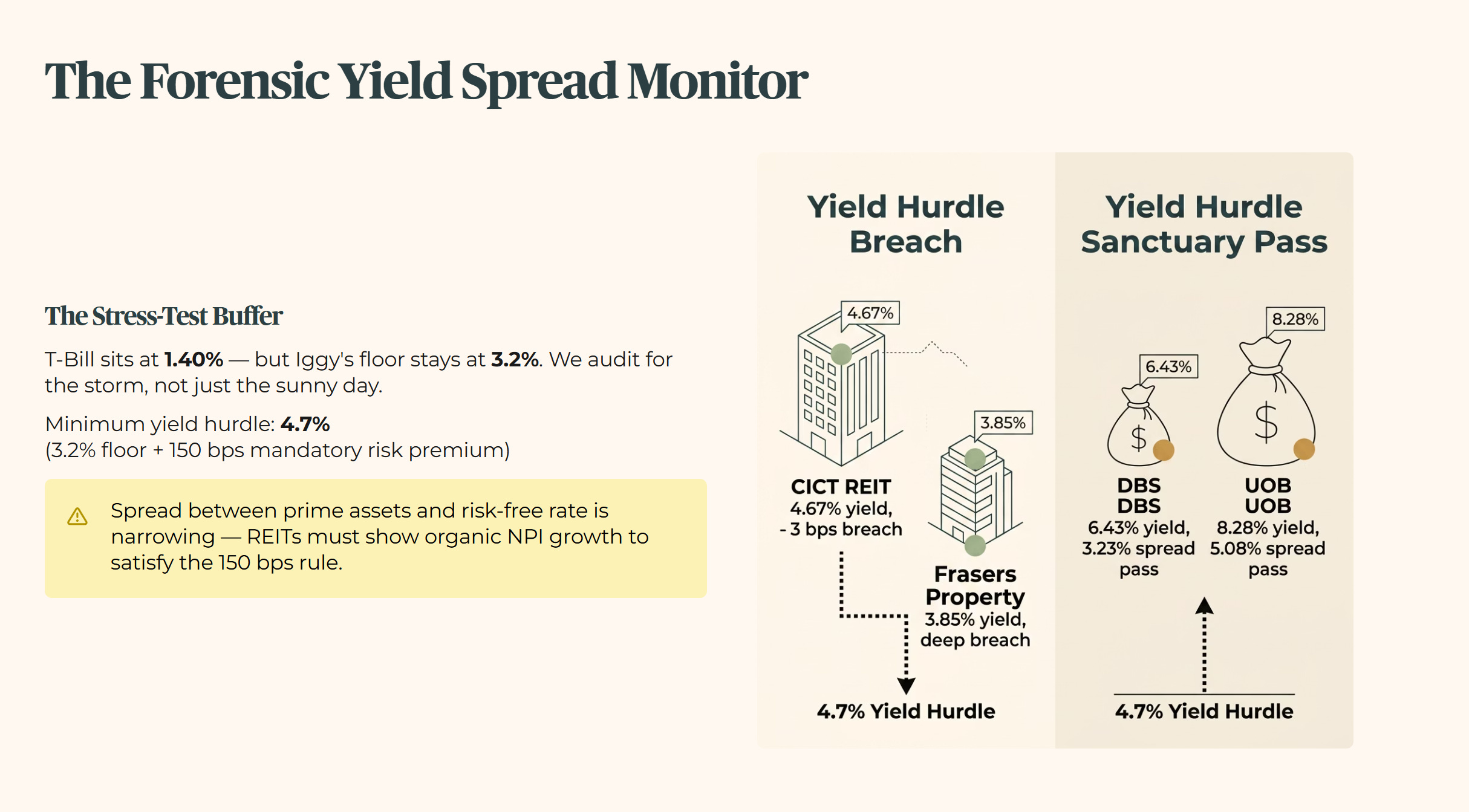

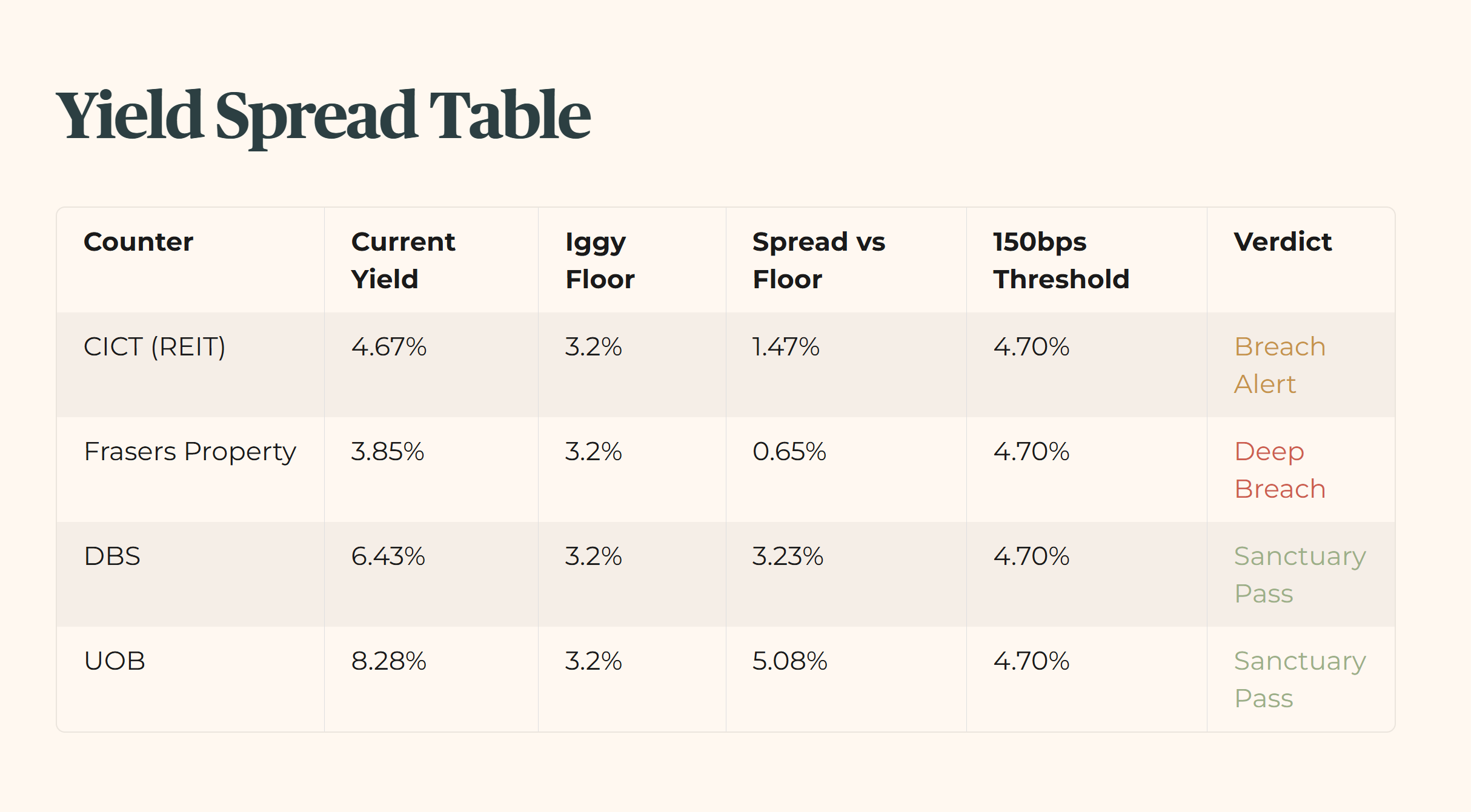

Asset recycling activity drove interest here, but the yield at 3.85% remains 85 basis points below the 4.7% hurdle. The forensic verdict is a watchlist trigger, not a pass.

Table 1: Gainers Dashboard

Forensic Verdict: Tech-heavy leadership suggests a return of risk appetite, but only counters with low gearing will survive a potential rate plateau.

Note: Debt/Capital for EH5, AWX, 558, and TQ5 pending Research Dossier verification. Willie to populate before next publish cycle.

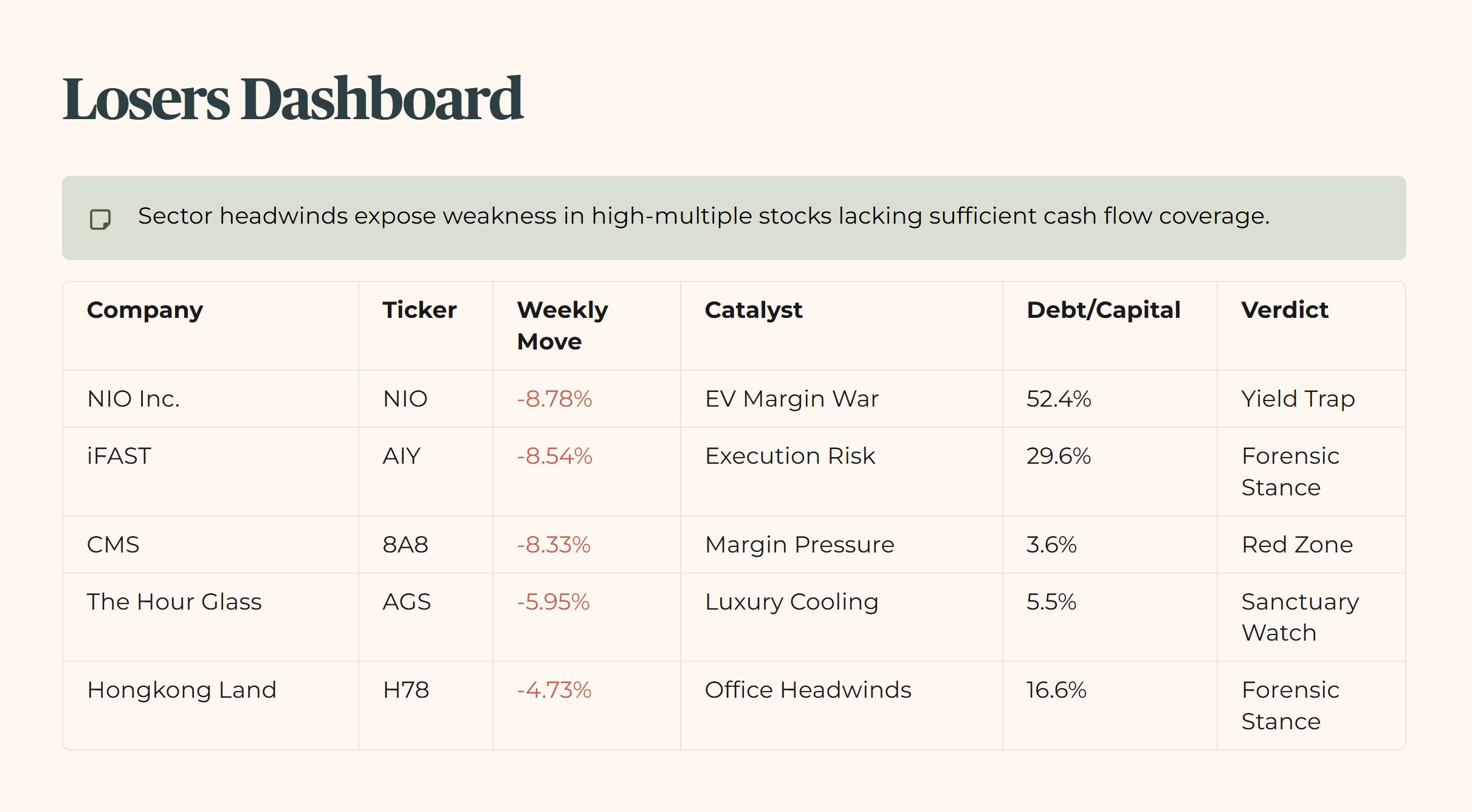

This Week’s Forensic Warnings — The Losers

Forensic Verdict: The losers list highlights a cooling of interest in wealth management platforms and luxury retail, sectors that are highly sensitive to discretionary spending and capital flow shifts.

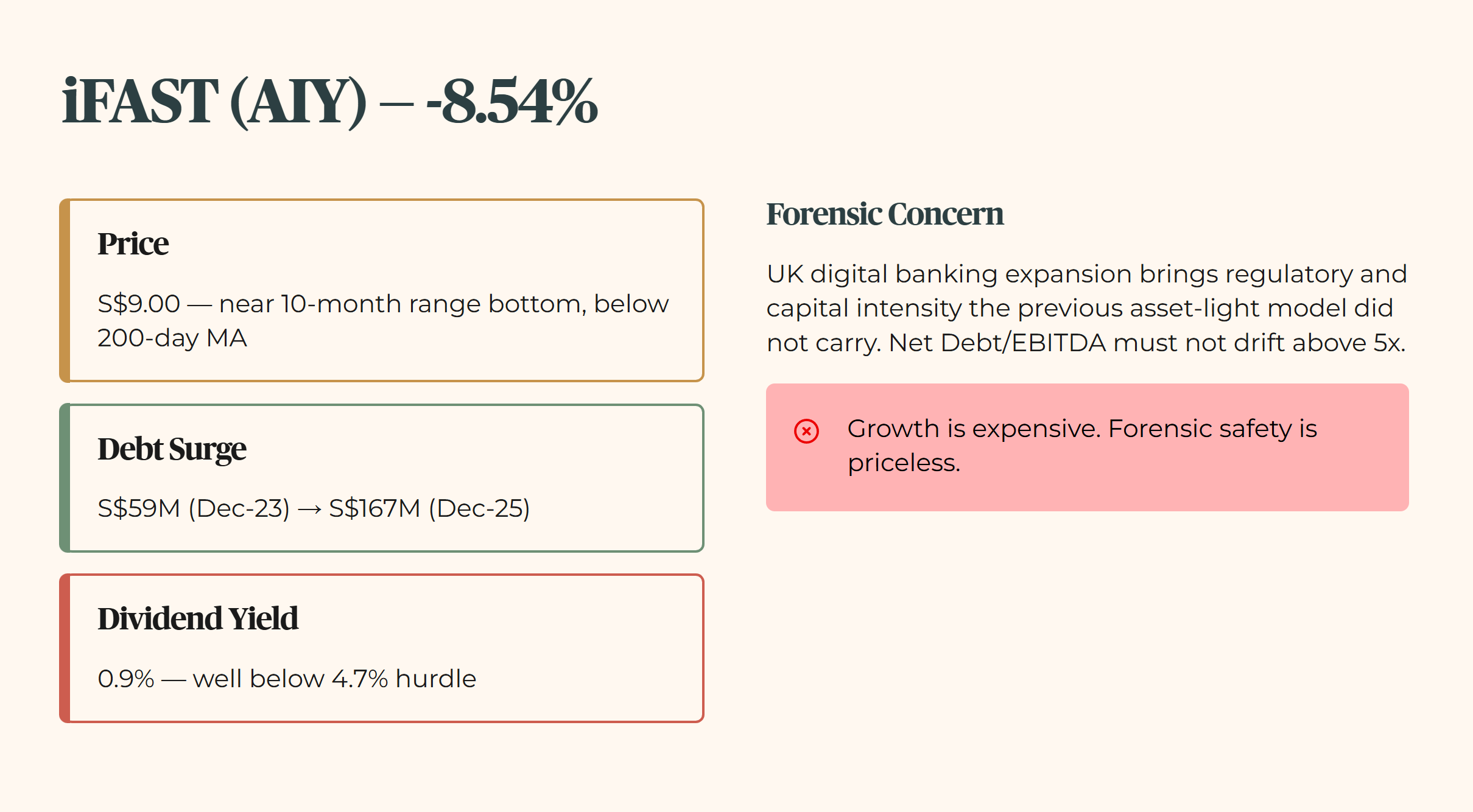

iFAST (AIY) — -8.54%

Shares continued their consolidation despite growth in its digital banking and global pension segments. The current price of S$9.00 sits near the bottom of its 10-month trading range and below the 200-day moving average. The forensic concern is not the price move itself but the balance sheet trajectory. Total debt has risen from S$59M in Dec-23 to S$167M in Dec-25, while the expansion into UK digital banking brings regulatory and capital intensity that the previous asset-light platform model did not carry. Net Debt/EBITDA requires monitoring to ensure it does not drift into the yellow flag zone above 5x. The dividend yield of 0.9% sits well below the 4.7% hurdle. Growth is expensive. Forensic safety is priceless.

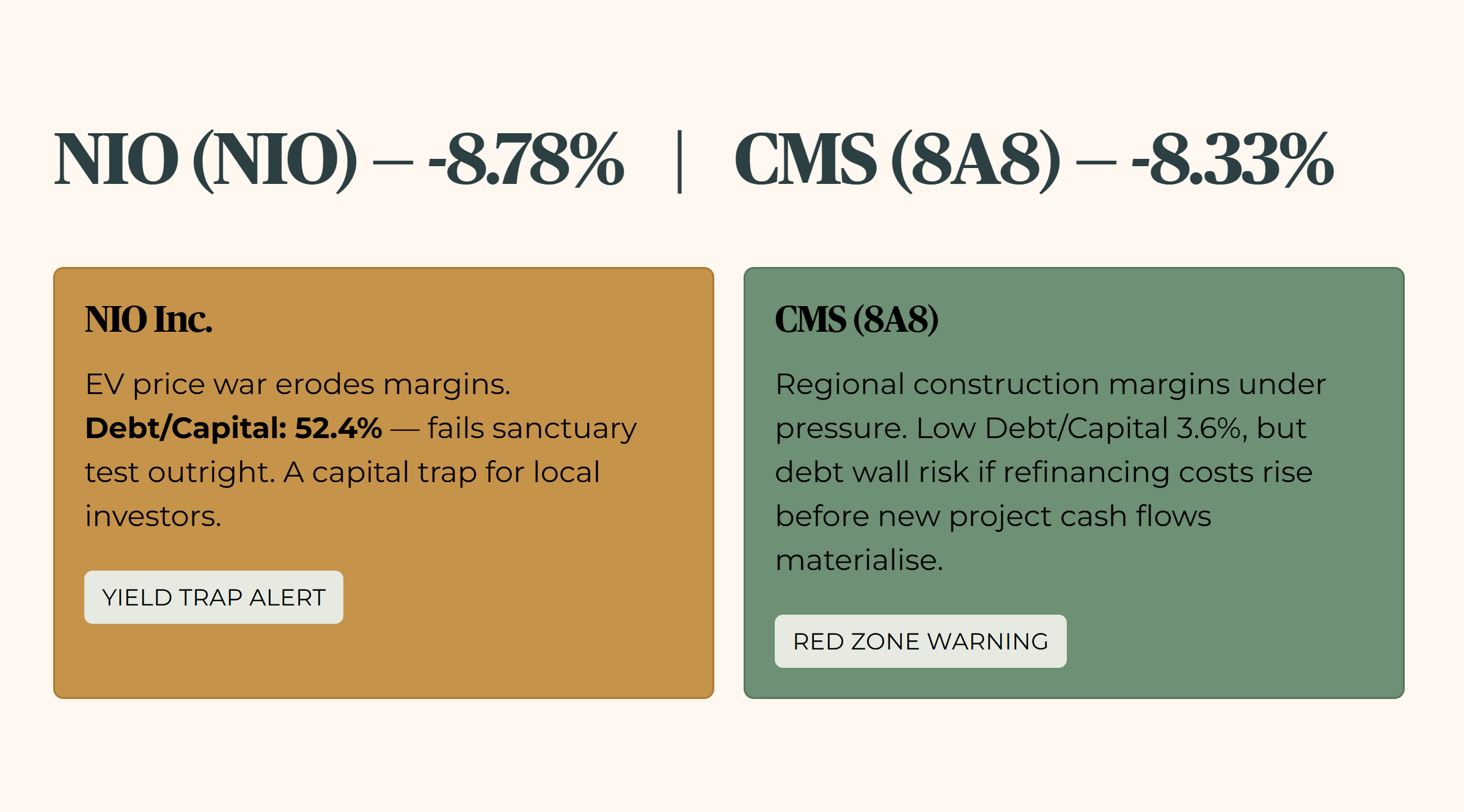

NIO Inc. (NIO) — -8.78%

The EV price war in China continues to erode margins and burn through cash reserves. At a Debt/Capital of 52.4%, this is a speculative asset that fails the sanctuary test outright. For the local investor, this is a reminder that regional growth stories can quickly become capital traps when the balance sheet cannot fund the burn.

CMS (8A8) — -8.33%

Declined amid concerns over regional construction margins and slowing infrastructure spending in parts of ASEAN. Despite a low Debt/Capital of 3.6%, the forensic concern is the debt wall risk if refinancing costs rise before new project cash flows materialise. Interest coverage ratio improvement is the signal to watch before this exits the red zone.

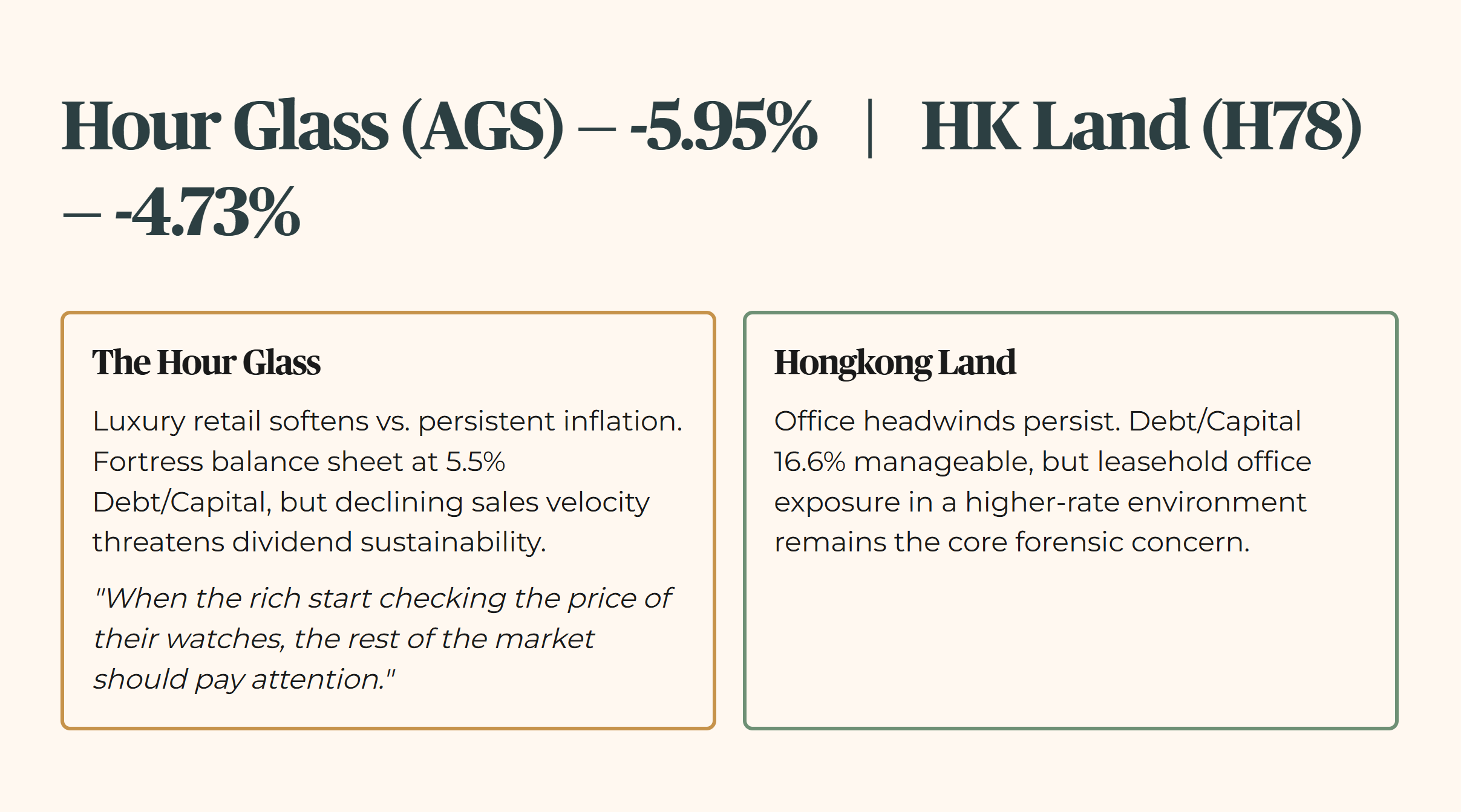

The Hour Glass (AGS) — -5.95%

Slipped as luxury retail sentiment softens against persistent inflation and cooling high-net-worth discretionary spending. The company maintains a fortress-leaning balance sheet at 5.5% Debt/Capital, but declining sales velocity is a warning sign for dividend sustainability. When the rich start checking the price of their watches, the rest of the market should pay attention.

Hongkong Land (H78) — -4.73%

Office headwinds continue to weigh on sentiment. Debt/Capital at 16.6% is manageable, but the structural challenge of leasehold office exposure in a higher-rate environment remains the core forensic concern.

Table 2: Losers Dashboard

Forensic Verdict: Sector-specific headwinds are exposing the weakness in high-multiple stocks that lack sufficient cash flow coverage.

The Forensic Yield Spread Monitor

Forensic Verdict: The spread between prime assets and the risk-free rate is narrowing, making the 150 basis point rule more difficult for REITs to satisfy without organic NPI growth.

Note on the Stress-Test Buffer: For this audit, I apply a conservative floor of 3.2%. We audit for the storm, not just the sunny day. While the T-Bill sits at 1.40%, I do not lower my standards to match a temporary market dip. My floor remains at 3.2% to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle is 4.7% — that is the 3.2% floor plus 150 basis points of mandatory risk premium.

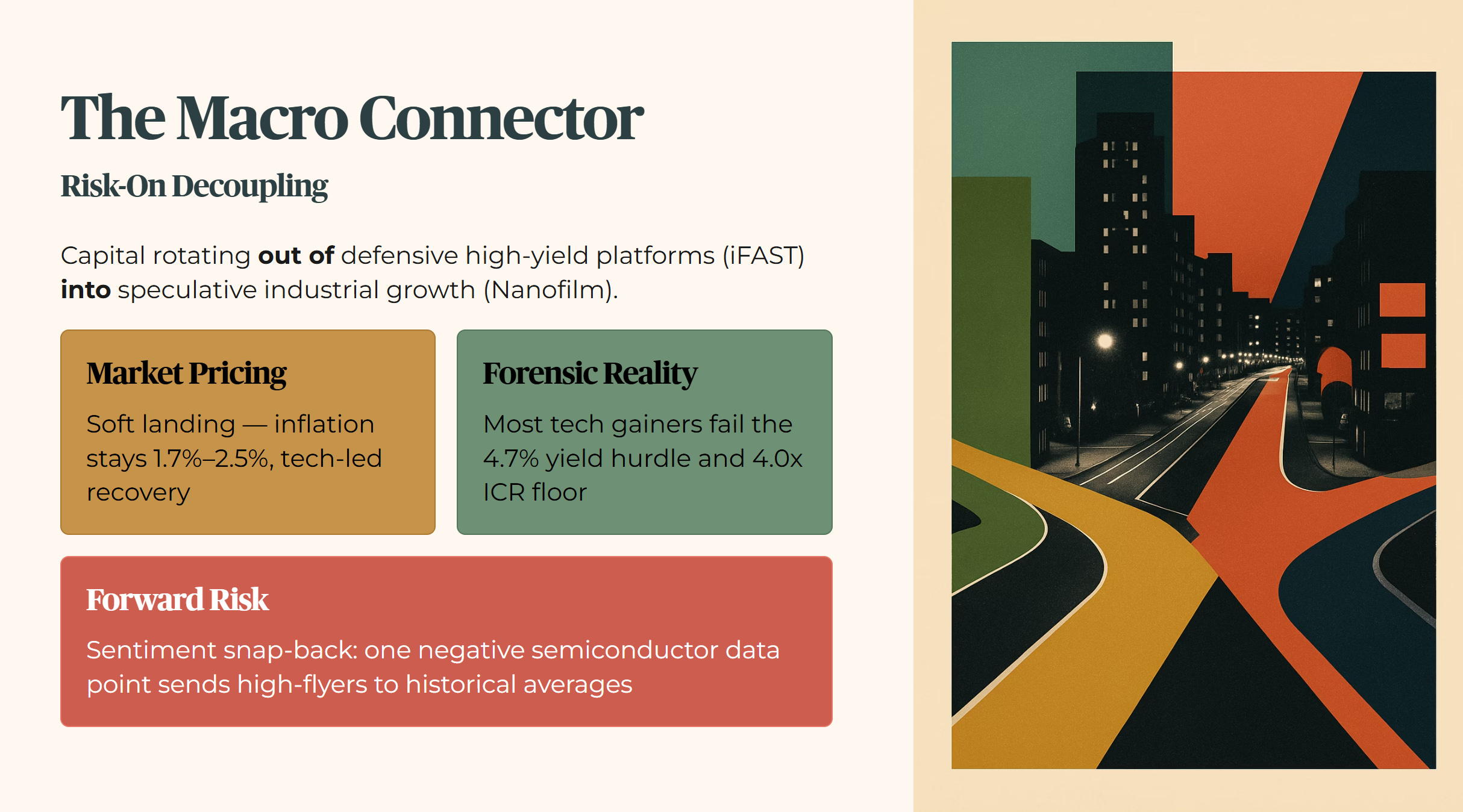

The Macro Connector

The connecting theme this week is the risk-on decoupling. Capital is rotating out of defensive, high-yield platforms like iFAST and into speculative industrial growth like Nanofilm. This suggests the market is beginning to price in a soft landing where inflation stays within the 1.7% to 2.5% range, allowing for a tech-led recovery. But the forensic reality is that most of these tech gainers do not meet the 4.7% yield hurdle and fail the 4.0x ICR floor required for true portfolio sanctuary. The forward risk is a sentiment snap-back where a single negative data point on global semiconductor demand sends these high-flyers back to their historical averages.

The Window Is Already Open

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

Iggy’s Weekly Verdict

The most important takeaway for a heartland investor this week is the CICT asset recycling move. By selling Asia Square Tower 2 and acquiring Paragon, CICT is shifting from a leasehold office profile to a freehold retail and medical mix. This is a direct response to the debt wall and the need for higher-yielding, resilient assets in a high-rate environment. And let’s be honest, they are not wrong. But here is the uncomfortable truth: the current yield of 4.67% still sits 3 basis points below the mandatory 4.7% hurdle. This move connects explicitly to the active thesis tracked in the Iggy Operational Log: the LHN Asset-Light Pivot.

For my own portfolio construction, I am tracking the interest coverage ratio of the semiconductor equipment makers. This is a personal forensic boundary, not a recommendation.

Iggy’s Forensic Disclaimer

This content is produced for educational and informational purposes only. I am not a financial advisor — I am a retail investor who applies forensic analysis to my own portfolio and shares that process publicly. Nothing here constitutes a recommendation to buy, sell, or hold any security, and no specific target prices or personalised financial advice are offered. Stocks assessed under Iggy’s Forensic Yield Standard are benchmarked against a 4.7% minimum yield hurdle; stocks flagged as Growth Watch fall below this threshold but demonstrate clean balance sheet metrics and an identifiable growth catalyst — these carry a materially different risk profile and are not suitable as yield replacements for income-dependent investors. All data is sourced from public filings and verified sources; where data is unverified it is explicitly flagged. All investments carry risk, including the potential loss of principal, and past performance is not indicative of future results. If you are making investment decisions involving CPF, SRS, or personal capital, please conduct your own due diligence or consult a MAS-licensed financial adviser before committing funds.